Bath & Body Works Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

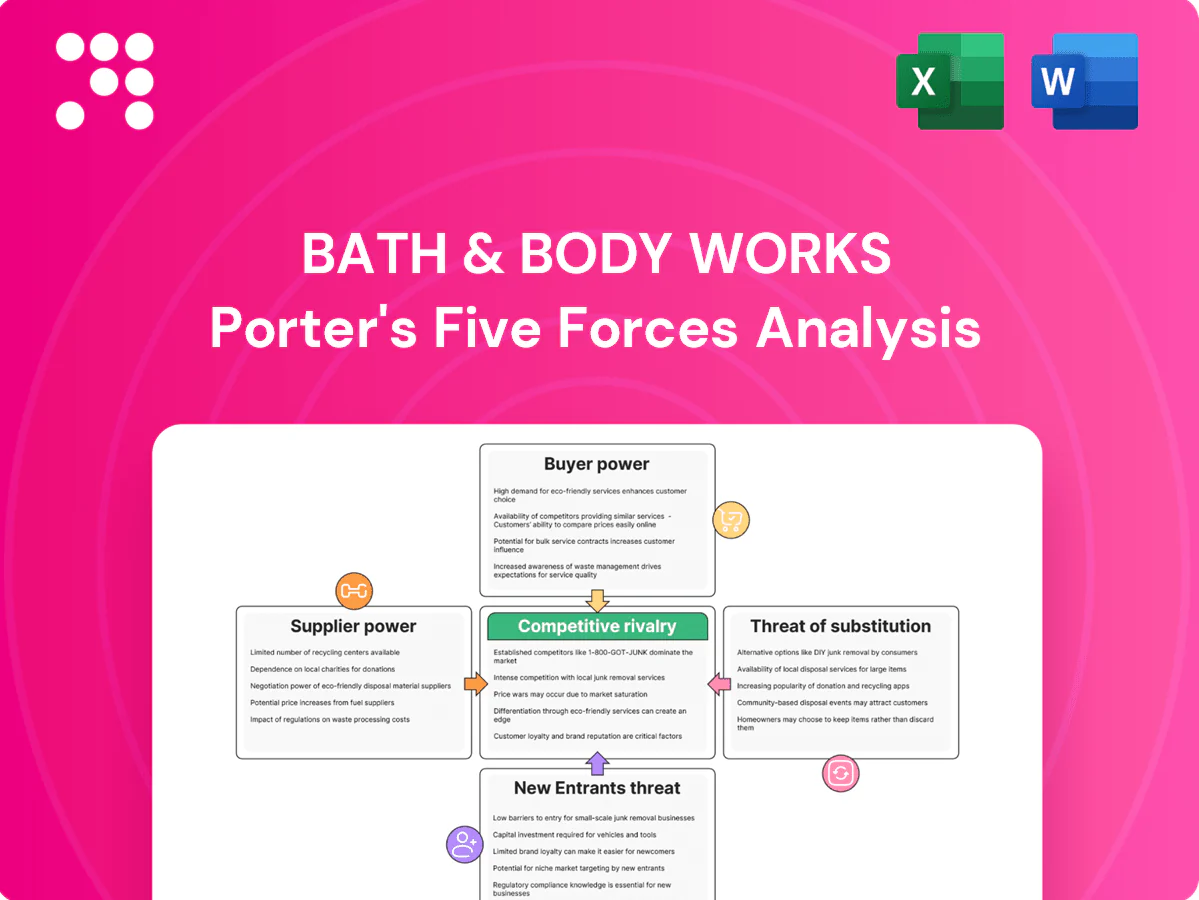

Bath & Body Works faces intense rivalry from specialty and mass‑market personal care brands, with strong loyalty, frequent promotions and store footprint advantages. Buyer power is moderate—differentiated scents limit switching though private‑labels pressure prices—while suppliers exert limited power despite raw‑material volatility. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bath & Body Works’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified ingredient base

Bath & Body Works sources fragrances, oils, wax, plastics and glass from numerous global vendors, diluting supplier concentration and limiting price-setting power; the company operates about 1,700 stores and reported roughly $7.0B net sales in fiscal 2024. Specialty fragrance compounds and premium wax blends still create pockets of supplier leverage. Strategic sourcing and dual-sourcing programs reduce disruption risk and bargaining pressure.

Branded fragrance houses influence

Prestige fragrance houses and compounders control unique scent IP and technical expertise, driving supplier leverage in a global fragrance market estimated at $52.6 billion in 2024 and with premium/branded scents representing over 60% of value. When hero SKUs hinge on signature notes, switching costs and supplier power rise, risking margin pressure. Long-term contracts, in-house R&D and private formulations can rebalance power and cut dependency. Collaborative development schedules align incentives around seasonal launches, reducing stockouts and time-to-shelf.

Packaging and component constraints

Custom molds for candles, pumps and caps create tooling lead times of 8–16 weeks and tooling costs commonly in the $10k–50k range, giving component suppliers leverage; capacity tightness in peak Q4 holiday seasons can raise component costs by an estimated 10–20% or cause delays. Multi-vendor qualification and standardizing components reduce single-supplier risk, while logistics planning and safety stock (months of cover) temper short-term price pressure.

Commodity and freight volatility

Input costs for wax, paperboard and glass remain sensitive to energy and transport markets; pulp and paperboard costs rose roughly 10–15% y/y into 2024 while industrial glass raw material prices climbed amid energy pressures, and global container freight rates in 2024 averaged about 25% above 2019 levels, temporarily strengthening supplier leverage during spikes.

- Hedging: long-term contracts reduce short-term supplier power

- Regional sourcing: lowers freight exposure

- Scale purchasing: B&BW buying power offsets peaks

- Cost engineering/reformulation: provides additional input flexibility

ESG and compliance requirements

Regulatory shifts and clean-ingredient commitments have narrowed eligible personal-care suppliers, boosting vendor leverage as Bath & Body Works navigates stricter EU and US ingredient rules; Bath & Body Works reported fiscal 2024 net sales of about $7.3 billion, increasing exposure to supplier pricing shifts. Verified sustainable feedstocks and certifications can command premiums, while supplier audits and joint partnerships limit overconcentration and ensure compliance. Transparency programs protect brand equity and help moderate cost creep.

- Supplier pool shrink → higher bargaining power

- Certifications → price premium pressure

- Audits/partnerships → reduce concentration risk

- Transparency → preserves brand, tempers margin erosion

Moderate supplier power amid scent supply concentration and rising input costs

Bath & Body Works faces moderate supplier power: diversified global vendors and scale (fiscal 2024 net sales ~$7.3B) limit leverage, but specialty fragrance houses, tooling lead times and certified inputs create concentrated pockets of power. Input cost volatility (paperboard +10–15% y/y; global freight ~+25% vs 2019) raises short-term pressure; hedging, dual-sourcing and private formulations mitigate risk.

| Metric | 2024 / Note |

|---|---|

| Net sales | $7.3B |

| Fragrance market | $52.6B |

| Paperboard change | +10–15% y/y |

| Freight vs 2019 | +25% |

| Tooling cost | $10k–50k |

What is included in the product

Tailored analysis of Bath & Body Works' competitive landscape, evaluating supplier and buyer power, threat of new entrants and substitutes, and industry rivalry to reveal pricing and margin pressures, emerging threats, and entry barriers—fully editable for inclusion in reports or presentations.

A clear, one-sheet summary of Bath & Body Works' Five Forces—ideal for quickly identifying competitive pain points and prioritizing strategic fixes to protect margins and market share.

Customers Bargaining Power

Highly price-aware shoppers

Consumers compare promotions across specialty and mass channels, raising price sensitivity as weekly deals and bundles push shoppers to wait for markdowns; Bath & Body Works operates ~1,700 stores and reported heavy promotion cadence in 2024. Frequent sales increase customer bargaining power, though a loyalty base of roughly 45 million members and limited editions shift focus from pure price. Value messaging and tiered pricing help manage elasticity and protect margins.

Low switching costs

Low switching costs: alternatives are abundant in-store and online—Bath & Body Works operates about 1,700 stores in North America (2024) and competes with numerous mass and specialty retailers, so disappointed customers can quickly switch brands or retailers. Differentiated fragrances and limited-edition collections help reduce churn, while subscription and auto-replenish options increase convenience lock-in.

Omnichannel transparency

Online reviews, social media, and price-tracking tools give buyers real-time leverage, forcing Bath & Body Works—with over 1,700 stores in 2024—to defend pricing during peak seasons when transparency can compress margins. This visibility amplifies promotional sensitivity, but the brand’s strong storytelling and experiential stores support premium pricing and repeat purchase. Consistent cross-channel pricing and unified promotions limit arbitrage and protect gross margins.

Gift-driven and seasonal demand

Peak gift-driven demand around holidays concentrates buyer leverage into short promotional windows; Bath & Body Works generated roughly $8.0 billion in net sales in 2024, making holiday-period promotions materially influential on full-year results.

High volumes around Thanksgiving–Christmas force retailers into aggressive discounts and bundle offers, while early-access drops and limited runs shift consumer focus from price to scarcity.

Inventory planning is calibrated to the seasonal cadence to align supply with demand and reduce markdown risk.

- Holiday concentration: drives promotional intensity

- Discount pressure: large seasonal markdowns common

- Scarcity tactics: early releases reduce price sensitivity

- Inventory alignment: minimizes year-end markdowns

Wholesale and landlord negotiations

While primarily DTC, wholesale partners still demand favorable terms and marketing support; Bath & Body Works operated about 1,700 stores in 2024 while e-commerce accounted for roughly 25% of sales, lowering reliance on third-party channels. Mall landlords shape traffic and occupancy costs, affecting in-store buyer expectations as foot traffic remains below pre‑pandemic peaks. Data-driven CRM personalization helps sustain margins by increasing AOV and repeat rates.

- Wholesale pressure: favors/marketing support

- Landlords: influence traffic, rent/occupancy

- Direct e‑commerce: ~25% sales (2024)

- CRM: boosts AOV/repeat purchases

Retail: $8B, 45M members, ~1,700 stores, ~25% e-commerce

Customers exert moderate-to-high bargaining power: easy switching, heavy promo sensitivity, and seasonal concentration push discounts, but 45 million loyalty members, differentiated limited editions, and experiential stores support pricing. Bath & Body Works operated ~1,700 stores, generated ~$8.0B net sales (2024), with e‑commerce ~25% of sales.

| Metric | Value | Impact |

|---|---|---|

| Stores | ~1,700 | Omnichannel reach |

| Net sales | $8.0B (2024) | Holiday leverage |

| Loyalty | 45M members | Reduced price sensitivity |

| E‑commerce | ~25% | Direct pricing control |

What You See Is What You Get

Bath & Body Works Porter's Five Forces Analysis

This preview shows the exact Bath & Body Works Porter's Five Forces analysis you'll receive upon purchase—no placeholders, no abridgments. The document includes fully formatted assessments of competitive rivalry, buyer and supplier power, threat of new entrants, and substitute products. It's the final file available for instant download and immediate use.

A Must-Have Tool for Decision-Makers

Bath & Body Works faces intense rivalry from specialty and mass‑market personal care brands, with strong loyalty, frequent promotions and store footprint advantages. Buyer power is moderate—differentiated scents limit switching though private‑labels pressure prices—while suppliers exert limited power despite raw‑material volatility. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bath & Body Works’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified ingredient base

Bath & Body Works sources fragrances, oils, wax, plastics and glass from numerous global vendors, diluting supplier concentration and limiting price-setting power; the company operates about 1,700 stores and reported roughly $7.0B net sales in fiscal 2024. Specialty fragrance compounds and premium wax blends still create pockets of supplier leverage. Strategic sourcing and dual-sourcing programs reduce disruption risk and bargaining pressure.

Branded fragrance houses influence

Prestige fragrance houses and compounders control unique scent IP and technical expertise, driving supplier leverage in a global fragrance market estimated at $52.6 billion in 2024 and with premium/branded scents representing over 60% of value. When hero SKUs hinge on signature notes, switching costs and supplier power rise, risking margin pressure. Long-term contracts, in-house R&D and private formulations can rebalance power and cut dependency. Collaborative development schedules align incentives around seasonal launches, reducing stockouts and time-to-shelf.

Packaging and component constraints

Custom molds for candles, pumps and caps create tooling lead times of 8–16 weeks and tooling costs commonly in the $10k–50k range, giving component suppliers leverage; capacity tightness in peak Q4 holiday seasons can raise component costs by an estimated 10–20% or cause delays. Multi-vendor qualification and standardizing components reduce single-supplier risk, while logistics planning and safety stock (months of cover) temper short-term price pressure.

Commodity and freight volatility

Input costs for wax, paperboard and glass remain sensitive to energy and transport markets; pulp and paperboard costs rose roughly 10–15% y/y into 2024 while industrial glass raw material prices climbed amid energy pressures, and global container freight rates in 2024 averaged about 25% above 2019 levels, temporarily strengthening supplier leverage during spikes.

- Hedging: long-term contracts reduce short-term supplier power

- Regional sourcing: lowers freight exposure

- Scale purchasing: B&BW buying power offsets peaks

- Cost engineering/reformulation: provides additional input flexibility

ESG and compliance requirements

Regulatory shifts and clean-ingredient commitments have narrowed eligible personal-care suppliers, boosting vendor leverage as Bath & Body Works navigates stricter EU and US ingredient rules; Bath & Body Works reported fiscal 2024 net sales of about $7.3 billion, increasing exposure to supplier pricing shifts. Verified sustainable feedstocks and certifications can command premiums, while supplier audits and joint partnerships limit overconcentration and ensure compliance. Transparency programs protect brand equity and help moderate cost creep.

- Supplier pool shrink → higher bargaining power

- Certifications → price premium pressure

- Audits/partnerships → reduce concentration risk

- Transparency → preserves brand, tempers margin erosion

Moderate supplier power amid scent supply concentration and rising input costs

Bath & Body Works faces moderate supplier power: diversified global vendors and scale (fiscal 2024 net sales ~$7.3B) limit leverage, but specialty fragrance houses, tooling lead times and certified inputs create concentrated pockets of power. Input cost volatility (paperboard +10–15% y/y; global freight ~+25% vs 2019) raises short-term pressure; hedging, dual-sourcing and private formulations mitigate risk.

| Metric | 2024 / Note |

|---|---|

| Net sales | $7.3B |

| Fragrance market | $52.6B |

| Paperboard change | +10–15% y/y |

| Freight vs 2019 | +25% |

| Tooling cost | $10k–50k |

What is included in the product

Tailored analysis of Bath & Body Works' competitive landscape, evaluating supplier and buyer power, threat of new entrants and substitutes, and industry rivalry to reveal pricing and margin pressures, emerging threats, and entry barriers—fully editable for inclusion in reports or presentations.

A clear, one-sheet summary of Bath & Body Works' Five Forces—ideal for quickly identifying competitive pain points and prioritizing strategic fixes to protect margins and market share.

Customers Bargaining Power

Highly price-aware shoppers

Consumers compare promotions across specialty and mass channels, raising price sensitivity as weekly deals and bundles push shoppers to wait for markdowns; Bath & Body Works operates ~1,700 stores and reported heavy promotion cadence in 2024. Frequent sales increase customer bargaining power, though a loyalty base of roughly 45 million members and limited editions shift focus from pure price. Value messaging and tiered pricing help manage elasticity and protect margins.

Low switching costs

Low switching costs: alternatives are abundant in-store and online—Bath & Body Works operates about 1,700 stores in North America (2024) and competes with numerous mass and specialty retailers, so disappointed customers can quickly switch brands or retailers. Differentiated fragrances and limited-edition collections help reduce churn, while subscription and auto-replenish options increase convenience lock-in.

Omnichannel transparency

Online reviews, social media, and price-tracking tools give buyers real-time leverage, forcing Bath & Body Works—with over 1,700 stores in 2024—to defend pricing during peak seasons when transparency can compress margins. This visibility amplifies promotional sensitivity, but the brand’s strong storytelling and experiential stores support premium pricing and repeat purchase. Consistent cross-channel pricing and unified promotions limit arbitrage and protect gross margins.

Gift-driven and seasonal demand

Peak gift-driven demand around holidays concentrates buyer leverage into short promotional windows; Bath & Body Works generated roughly $8.0 billion in net sales in 2024, making holiday-period promotions materially influential on full-year results.

High volumes around Thanksgiving–Christmas force retailers into aggressive discounts and bundle offers, while early-access drops and limited runs shift consumer focus from price to scarcity.

Inventory planning is calibrated to the seasonal cadence to align supply with demand and reduce markdown risk.

- Holiday concentration: drives promotional intensity

- Discount pressure: large seasonal markdowns common

- Scarcity tactics: early releases reduce price sensitivity

- Inventory alignment: minimizes year-end markdowns

Wholesale and landlord negotiations

While primarily DTC, wholesale partners still demand favorable terms and marketing support; Bath & Body Works operated about 1,700 stores in 2024 while e-commerce accounted for roughly 25% of sales, lowering reliance on third-party channels. Mall landlords shape traffic and occupancy costs, affecting in-store buyer expectations as foot traffic remains below pre‑pandemic peaks. Data-driven CRM personalization helps sustain margins by increasing AOV and repeat rates.

- Wholesale pressure: favors/marketing support

- Landlords: influence traffic, rent/occupancy

- Direct e‑commerce: ~25% sales (2024)

- CRM: boosts AOV/repeat purchases

Retail: $8B, 45M members, ~1,700 stores, ~25% e-commerce

Customers exert moderate-to-high bargaining power: easy switching, heavy promo sensitivity, and seasonal concentration push discounts, but 45 million loyalty members, differentiated limited editions, and experiential stores support pricing. Bath & Body Works operated ~1,700 stores, generated ~$8.0B net sales (2024), with e‑commerce ~25% of sales.

| Metric | Value | Impact |

|---|---|---|

| Stores | ~1,700 | Omnichannel reach |

| Net sales | $8.0B (2024) | Holiday leverage |

| Loyalty | 45M members | Reduced price sensitivity |

| E‑commerce | ~25% | Direct pricing control |

What You See Is What You Get

Bath & Body Works Porter's Five Forces Analysis

This preview shows the exact Bath & Body Works Porter's Five Forces analysis you'll receive upon purchase—no placeholders, no abridgments. The document includes fully formatted assessments of competitive rivalry, buyer and supplier power, threat of new entrants, and substitute products. It's the final file available for instant download and immediate use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Bath & Body Works faces intense rivalry from specialty and mass‑market personal care brands, with strong loyalty, frequent promotions and store footprint advantages. Buyer power is moderate—differentiated scents limit switching though private‑labels pressure prices—while suppliers exert limited power despite raw‑material volatility. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bath & Body Works’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified ingredient base

Bath & Body Works sources fragrances, oils, wax, plastics and glass from numerous global vendors, diluting supplier concentration and limiting price-setting power; the company operates about 1,700 stores and reported roughly $7.0B net sales in fiscal 2024. Specialty fragrance compounds and premium wax blends still create pockets of supplier leverage. Strategic sourcing and dual-sourcing programs reduce disruption risk and bargaining pressure.

Branded fragrance houses influence

Prestige fragrance houses and compounders control unique scent IP and technical expertise, driving supplier leverage in a global fragrance market estimated at $52.6 billion in 2024 and with premium/branded scents representing over 60% of value. When hero SKUs hinge on signature notes, switching costs and supplier power rise, risking margin pressure. Long-term contracts, in-house R&D and private formulations can rebalance power and cut dependency. Collaborative development schedules align incentives around seasonal launches, reducing stockouts and time-to-shelf.

Packaging and component constraints

Custom molds for candles, pumps and caps create tooling lead times of 8–16 weeks and tooling costs commonly in the $10k–50k range, giving component suppliers leverage; capacity tightness in peak Q4 holiday seasons can raise component costs by an estimated 10–20% or cause delays. Multi-vendor qualification and standardizing components reduce single-supplier risk, while logistics planning and safety stock (months of cover) temper short-term price pressure.

Commodity and freight volatility

Input costs for wax, paperboard and glass remain sensitive to energy and transport markets; pulp and paperboard costs rose roughly 10–15% y/y into 2024 while industrial glass raw material prices climbed amid energy pressures, and global container freight rates in 2024 averaged about 25% above 2019 levels, temporarily strengthening supplier leverage during spikes.

- Hedging: long-term contracts reduce short-term supplier power

- Regional sourcing: lowers freight exposure

- Scale purchasing: B&BW buying power offsets peaks

- Cost engineering/reformulation: provides additional input flexibility

ESG and compliance requirements

Regulatory shifts and clean-ingredient commitments have narrowed eligible personal-care suppliers, boosting vendor leverage as Bath & Body Works navigates stricter EU and US ingredient rules; Bath & Body Works reported fiscal 2024 net sales of about $7.3 billion, increasing exposure to supplier pricing shifts. Verified sustainable feedstocks and certifications can command premiums, while supplier audits and joint partnerships limit overconcentration and ensure compliance. Transparency programs protect brand equity and help moderate cost creep.

- Supplier pool shrink → higher bargaining power

- Certifications → price premium pressure

- Audits/partnerships → reduce concentration risk

- Transparency → preserves brand, tempers margin erosion

Moderate supplier power amid scent supply concentration and rising input costs

Bath & Body Works faces moderate supplier power: diversified global vendors and scale (fiscal 2024 net sales ~$7.3B) limit leverage, but specialty fragrance houses, tooling lead times and certified inputs create concentrated pockets of power. Input cost volatility (paperboard +10–15% y/y; global freight ~+25% vs 2019) raises short-term pressure; hedging, dual-sourcing and private formulations mitigate risk.

| Metric | 2024 / Note |

|---|---|

| Net sales | $7.3B |

| Fragrance market | $52.6B |

| Paperboard change | +10–15% y/y |

| Freight vs 2019 | +25% |

| Tooling cost | $10k–50k |

What is included in the product

Tailored analysis of Bath & Body Works' competitive landscape, evaluating supplier and buyer power, threat of new entrants and substitutes, and industry rivalry to reveal pricing and margin pressures, emerging threats, and entry barriers—fully editable for inclusion in reports or presentations.

A clear, one-sheet summary of Bath & Body Works' Five Forces—ideal for quickly identifying competitive pain points and prioritizing strategic fixes to protect margins and market share.

Customers Bargaining Power

Highly price-aware shoppers

Consumers compare promotions across specialty and mass channels, raising price sensitivity as weekly deals and bundles push shoppers to wait for markdowns; Bath & Body Works operates ~1,700 stores and reported heavy promotion cadence in 2024. Frequent sales increase customer bargaining power, though a loyalty base of roughly 45 million members and limited editions shift focus from pure price. Value messaging and tiered pricing help manage elasticity and protect margins.

Low switching costs

Low switching costs: alternatives are abundant in-store and online—Bath & Body Works operates about 1,700 stores in North America (2024) and competes with numerous mass and specialty retailers, so disappointed customers can quickly switch brands or retailers. Differentiated fragrances and limited-edition collections help reduce churn, while subscription and auto-replenish options increase convenience lock-in.

Omnichannel transparency

Online reviews, social media, and price-tracking tools give buyers real-time leverage, forcing Bath & Body Works—with over 1,700 stores in 2024—to defend pricing during peak seasons when transparency can compress margins. This visibility amplifies promotional sensitivity, but the brand’s strong storytelling and experiential stores support premium pricing and repeat purchase. Consistent cross-channel pricing and unified promotions limit arbitrage and protect gross margins.

Gift-driven and seasonal demand

Peak gift-driven demand around holidays concentrates buyer leverage into short promotional windows; Bath & Body Works generated roughly $8.0 billion in net sales in 2024, making holiday-period promotions materially influential on full-year results.

High volumes around Thanksgiving–Christmas force retailers into aggressive discounts and bundle offers, while early-access drops and limited runs shift consumer focus from price to scarcity.

Inventory planning is calibrated to the seasonal cadence to align supply with demand and reduce markdown risk.

- Holiday concentration: drives promotional intensity

- Discount pressure: large seasonal markdowns common

- Scarcity tactics: early releases reduce price sensitivity

- Inventory alignment: minimizes year-end markdowns

Wholesale and landlord negotiations

While primarily DTC, wholesale partners still demand favorable terms and marketing support; Bath & Body Works operated about 1,700 stores in 2024 while e-commerce accounted for roughly 25% of sales, lowering reliance on third-party channels. Mall landlords shape traffic and occupancy costs, affecting in-store buyer expectations as foot traffic remains below pre‑pandemic peaks. Data-driven CRM personalization helps sustain margins by increasing AOV and repeat rates.

- Wholesale pressure: favors/marketing support

- Landlords: influence traffic, rent/occupancy

- Direct e‑commerce: ~25% sales (2024)

- CRM: boosts AOV/repeat purchases

Retail: $8B, 45M members, ~1,700 stores, ~25% e-commerce

Customers exert moderate-to-high bargaining power: easy switching, heavy promo sensitivity, and seasonal concentration push discounts, but 45 million loyalty members, differentiated limited editions, and experiential stores support pricing. Bath & Body Works operated ~1,700 stores, generated ~$8.0B net sales (2024), with e‑commerce ~25% of sales.

| Metric | Value | Impact |

|---|---|---|

| Stores | ~1,700 | Omnichannel reach |

| Net sales | $8.0B (2024) | Holiday leverage |

| Loyalty | 45M members | Reduced price sensitivity |

| E‑commerce | ~25% | Direct pricing control |

What You See Is What You Get

Bath & Body Works Porter's Five Forces Analysis

This preview shows the exact Bath & Body Works Porter's Five Forces analysis you'll receive upon purchase—no placeholders, no abridgments. The document includes fully formatted assessments of competitive rivalry, buyer and supplier power, threat of new entrants, and substitute products. It's the final file available for instant download and immediate use.