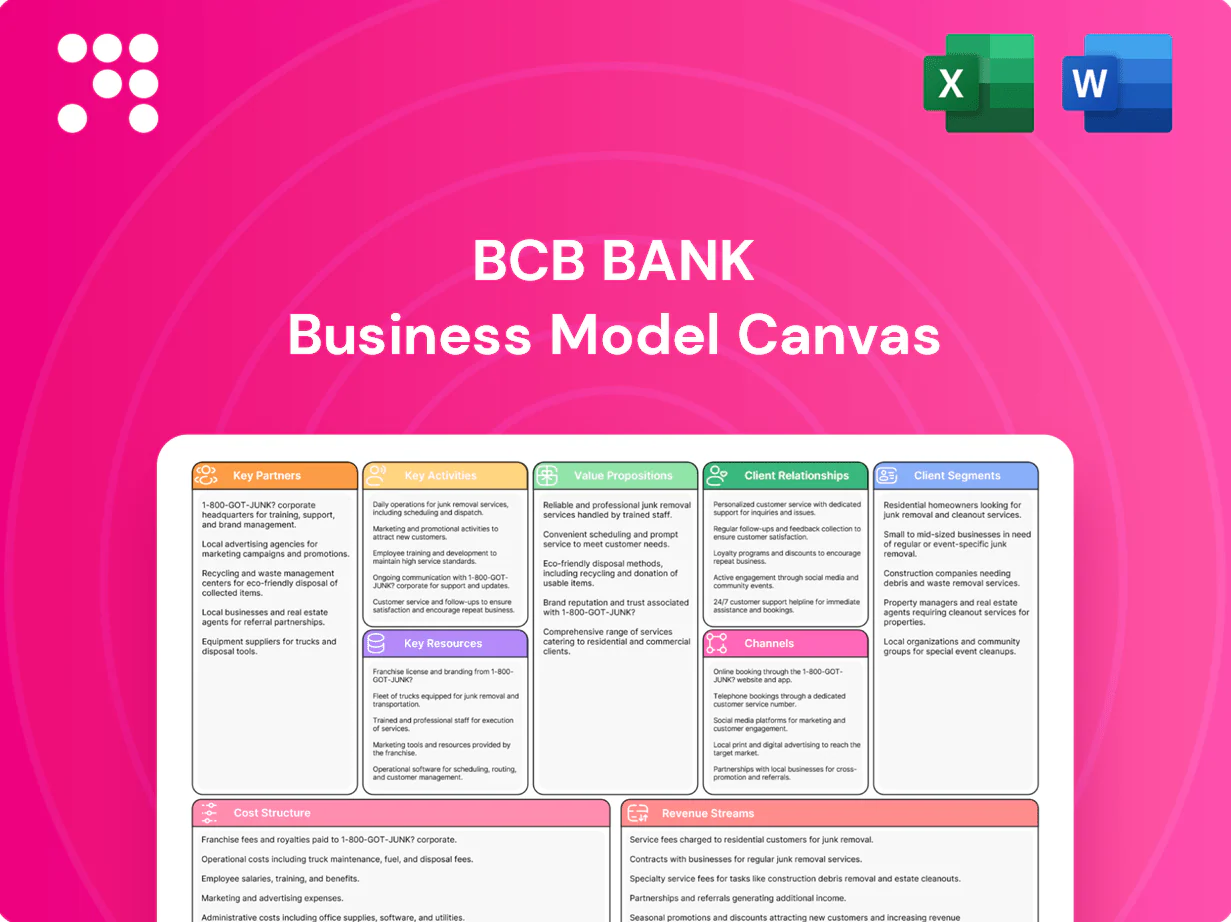

BCB Bank Business Model Canvas

Business Model Canvas for Retail Banks: Actionable Map of Customers, Revenue & Channels

Unlock BCB Bank’s strategic blueprint with our Business Model Canvas: concise mapping of customer segments, value propositions, channels, revenue streams and cost drivers. Ideal for investors, consultants and founders seeking actionable, company-specific insights. Purchase the full, editable Canvas in Word and Excel to benchmark and implement proven banking strategies.

Partnerships

Correspondent and syndication banks

BCB partners with regional and national correspondent and syndication banks to join larger commercial credits, sharing risk and expanding lending capacity. In 2024 global syndicated loan issuance topped roughly 2 trillion USD, reinforcing reciprocal deal flow and liquidity options for participants. These partnerships prevent overconcentration while enabling larger ticket lending and secondary market exits.

Fintech and core technology providers

Core processors, digital banking vendors, and payments partners enable mobile, online, and real-time services while delivering regulatory-grade security through standards such as PCI DSS and ISO 27001. These partnerships accelerate feature rollout—BCB can leverage ready APIs and connectors to shorten delivery cycles and scale payment rails. Integration with certified vendors lowers time-to-market and reduces development costs by replacing bespoke builds with proven platforms.

Broker-dealers and loan brokers

Partnerships with mortgage brokers and commercial loan originators broaden BCB Bank’s pipeline, leveraging brokers who handled about one-third of U.S. mortgage originations in 2024 to source high-quality borrowers in New Jersey and New York metros. Structured referral arrangements align incentives and enforce common underwriting standards and documentation requirements, improving referral-to-funding conversion and credit quality.

Title, appraisal, and legal firms

Trusted title, appraisal and legal firms enable secure, compliant mortgage and CRE lending, centralizing chain-of-title and valuation expertise. Standardized processes and SLAs shorten cycle times—ICE Mortgage Technology reported a 2024 national average mortgage close of 45 days, with SLAs commonly cutting internal turnaround by ~30%. Independent validation improves credit quality and creates robust audit trails that lower post-close defect risk.

- trusted-partners: title, appraisal, legal

- SLA-impact: 45d avg close (2024); ~30% faster with SLAs

- risk-mitigation: independent validation, stronger audit trails

Community organizations and chambers

Local nonprofits, chambers, and municipal entities boost BCB Bank brand visibility and trust, opening doors to households and small businesses in target neighborhoods. Collaborative financial education and outreach programs increase deposits and measurable inclusion; community banks held about 14% of U.S. domestic deposits in 2024 (FDIC). These partnerships create referral pipelines and joint product offerings that drive account growth.

- Target access: small-business and household referrals

- Impact: partnership-driven deposit growth

- Metric: community banks ~14% of U.S. deposits (FDIC 2024)

Partner network speeds lending, digital services and deposits while lowering concentration risk

BCB leverages correspondent/syndication banks, fintech processors, brokers, title/appraisal/legal firms, and community partners to expand lending capacity, accelerate digital services, source loans, ensure compliance, and grow deposits. 2024 benchmarks: global syndicated loans ~2T USD; community banks ~14% of US deposits; avg mortgage close 45 days. These partnerships reduce concentration, speed go-to-market, and improve credit controls.

| Partner | Role | 2024 Metric |

|---|---|---|

| Correspondents | Risk sharing | ~2T syndicated loans |

| Fintech/vendors | Digital/Payments | PCI DSS/ISO27001 |

| Brokers | Origination | ~33% mortgage originations |

| Title/Legal | Validation | 45d avg close |

| Community Orgs | Deposit/referrals | 14% US deposits |

What is included in the product

A tailored Business Model Canvas for BCB Bank detailing customer segments, channels, value propositions, revenue and cost streams, key resources and partners, and operational plans across the 9 BMC blocks, with linked SWOT, competitive advantages, and polished narrative for investor presentations and strategic decisions.

High-level view of BCB Bank’s business model with editable cells, relieving strategic alignment and presentation pain points. Shareable layout saves hours structuring analyses and enables fast, board-ready summaries for teams and advisors.

Activities

Deposit gathering and liquidity management

BCB Bank focuses on gathering checking, savings and money-market balances to fund lending, mirroring U.S. banks that held roughly $16.9 trillion in deposits at year-end 2024. Pricing, relationship banking and branch outreach drive acquisition and retention, with targeted rate tiers and product bundling. Rigorous ALM disciplines—duration management, liquidity buffers and stress-testing—optimize cost of funds and limit interest-rate risk.

Underwriting and portfolio management

Rigorous credit analysis underpins underwriting for commercial, residential, and construction loans, using borrower cash-flow, LTV, and scenario modelling to set risk-adjusted pricing. Ongoing monitoring, covenant tracking, and periodic stress testing preserve asset quality and enable timely remediation. Data-driven policies align origination targets with risk appetite to balance growth and risk-adjusted returns.

Customer service and relationship banking

Personalized support across branches, phone and digital channels drives loyalty, with 84% of customers in 2024 saying personalization matters. Relationship managers cross-sell to deepen share of wallet, typically raising product holdings per household by about 20%. Rapid issue resolution — linked to higher NPS — boosts retention, and Bain finds a 5% retention rise can increase profits 25–95%.

Regulatory compliance and risk controls

BCB Bank runs comprehensive BSA/AML, KYC, and fair lending programs, processing industry-scale alerts and supporting over 4 million SAR filings annually (industry 2023–24 range) to detect illicit flows; internal audit and timely examiner reporting sustain supervisory confidence and a satisfactory CAMELS-related control posture; robust controls protect reputation and capital, reducing regulatory fines and operational losses.

- Program scope: BSA/AML, KYC, fair lending

- Scale: >4,000,000 SARs industry-wide (2023–24)

- Controls: internal audit + examiner reporting

- Objective: protect reputation and capital

Digital banking and payments operations

Continuous enhancement of mobile, online, and payments capabilities keeps BCB Bank aligned with 2024 industry norms where mobile channels exceed 70% of retail digital sessions; development focuses on feature velocity and API-driven payments. Uptime and cybersecurity are monitored with enterprise SLAs (targeting 99.99% availability) and real-time threat detection to protect transactions and user experience. Vendor coordination drives quarterly releases and cross-system integrations to minimize latency and rollback risk.

- Uptime: 99.99% SLA

- Mobile share: >70% of digital sessions (2024)

- Release cadence: quarterly vendor-coordinated

Retail-funded lending: ALM controls, mobile-led growth, strong AML and underwriting

BCB funds lending with retail deposits (US banks held $16.9T in deposits YE 2024), pricing and branch/relationship sales drive retention; ALM and stress-testing limit interest-rate risk. Underwriting uses cash-flow, LTV and scenario models; >4,000,000 SARs industry scale (2023–24) support AML controls. Digital: >70% mobile sessions (2024), 99.99% uptime SLA.

| Metric | 2024 |

|---|---|

| US deposits | $16.9T |

| Mobile share | >70% |

| SARs (industry) | >4,000,000 |

| Uptime SLA | 99.99% |

Preview Before You Purchase

Business Model Canvas

The BCB Bank Business Model Canvas you’re previewing is the actual deliverable, not a mockup—this snapshot is taken directly from the final file you’ll receive. Upon purchase you’ll gain immediate access to the complete, editable document in Word and Excel formats. It’s fully formatted, comprehensive and ready to present or customize—no surprises, just the same professional file shown here.

Business Model Canvas for Retail Banks: Actionable Map of Customers, Revenue & Channels

Unlock BCB Bank’s strategic blueprint with our Business Model Canvas: concise mapping of customer segments, value propositions, channels, revenue streams and cost drivers. Ideal for investors, consultants and founders seeking actionable, company-specific insights. Purchase the full, editable Canvas in Word and Excel to benchmark and implement proven banking strategies.

Partnerships

Correspondent and syndication banks

BCB partners with regional and national correspondent and syndication banks to join larger commercial credits, sharing risk and expanding lending capacity. In 2024 global syndicated loan issuance topped roughly 2 trillion USD, reinforcing reciprocal deal flow and liquidity options for participants. These partnerships prevent overconcentration while enabling larger ticket lending and secondary market exits.

Fintech and core technology providers

Core processors, digital banking vendors, and payments partners enable mobile, online, and real-time services while delivering regulatory-grade security through standards such as PCI DSS and ISO 27001. These partnerships accelerate feature rollout—BCB can leverage ready APIs and connectors to shorten delivery cycles and scale payment rails. Integration with certified vendors lowers time-to-market and reduces development costs by replacing bespoke builds with proven platforms.

Broker-dealers and loan brokers

Partnerships with mortgage brokers and commercial loan originators broaden BCB Bank’s pipeline, leveraging brokers who handled about one-third of U.S. mortgage originations in 2024 to source high-quality borrowers in New Jersey and New York metros. Structured referral arrangements align incentives and enforce common underwriting standards and documentation requirements, improving referral-to-funding conversion and credit quality.

Title, appraisal, and legal firms

Trusted title, appraisal and legal firms enable secure, compliant mortgage and CRE lending, centralizing chain-of-title and valuation expertise. Standardized processes and SLAs shorten cycle times—ICE Mortgage Technology reported a 2024 national average mortgage close of 45 days, with SLAs commonly cutting internal turnaround by ~30%. Independent validation improves credit quality and creates robust audit trails that lower post-close defect risk.

- trusted-partners: title, appraisal, legal

- SLA-impact: 45d avg close (2024); ~30% faster with SLAs

- risk-mitigation: independent validation, stronger audit trails

Community organizations and chambers

Local nonprofits, chambers, and municipal entities boost BCB Bank brand visibility and trust, opening doors to households and small businesses in target neighborhoods. Collaborative financial education and outreach programs increase deposits and measurable inclusion; community banks held about 14% of U.S. domestic deposits in 2024 (FDIC). These partnerships create referral pipelines and joint product offerings that drive account growth.

- Target access: small-business and household referrals

- Impact: partnership-driven deposit growth

- Metric: community banks ~14% of U.S. deposits (FDIC 2024)

Partner network speeds lending, digital services and deposits while lowering concentration risk

BCB leverages correspondent/syndication banks, fintech processors, brokers, title/appraisal/legal firms, and community partners to expand lending capacity, accelerate digital services, source loans, ensure compliance, and grow deposits. 2024 benchmarks: global syndicated loans ~2T USD; community banks ~14% of US deposits; avg mortgage close 45 days. These partnerships reduce concentration, speed go-to-market, and improve credit controls.

| Partner | Role | 2024 Metric |

|---|---|---|

| Correspondents | Risk sharing | ~2T syndicated loans |

| Fintech/vendors | Digital/Payments | PCI DSS/ISO27001 |

| Brokers | Origination | ~33% mortgage originations |

| Title/Legal | Validation | 45d avg close |

| Community Orgs | Deposit/referrals | 14% US deposits |

What is included in the product

A tailored Business Model Canvas for BCB Bank detailing customer segments, channels, value propositions, revenue and cost streams, key resources and partners, and operational plans across the 9 BMC blocks, with linked SWOT, competitive advantages, and polished narrative for investor presentations and strategic decisions.

High-level view of BCB Bank’s business model with editable cells, relieving strategic alignment and presentation pain points. Shareable layout saves hours structuring analyses and enables fast, board-ready summaries for teams and advisors.

Activities

Deposit gathering and liquidity management

BCB Bank focuses on gathering checking, savings and money-market balances to fund lending, mirroring U.S. banks that held roughly $16.9 trillion in deposits at year-end 2024. Pricing, relationship banking and branch outreach drive acquisition and retention, with targeted rate tiers and product bundling. Rigorous ALM disciplines—duration management, liquidity buffers and stress-testing—optimize cost of funds and limit interest-rate risk.

Underwriting and portfolio management

Rigorous credit analysis underpins underwriting for commercial, residential, and construction loans, using borrower cash-flow, LTV, and scenario modelling to set risk-adjusted pricing. Ongoing monitoring, covenant tracking, and periodic stress testing preserve asset quality and enable timely remediation. Data-driven policies align origination targets with risk appetite to balance growth and risk-adjusted returns.

Customer service and relationship banking

Personalized support across branches, phone and digital channels drives loyalty, with 84% of customers in 2024 saying personalization matters. Relationship managers cross-sell to deepen share of wallet, typically raising product holdings per household by about 20%. Rapid issue resolution — linked to higher NPS — boosts retention, and Bain finds a 5% retention rise can increase profits 25–95%.

Regulatory compliance and risk controls

BCB Bank runs comprehensive BSA/AML, KYC, and fair lending programs, processing industry-scale alerts and supporting over 4 million SAR filings annually (industry 2023–24 range) to detect illicit flows; internal audit and timely examiner reporting sustain supervisory confidence and a satisfactory CAMELS-related control posture; robust controls protect reputation and capital, reducing regulatory fines and operational losses.

- Program scope: BSA/AML, KYC, fair lending

- Scale: >4,000,000 SARs industry-wide (2023–24)

- Controls: internal audit + examiner reporting

- Objective: protect reputation and capital

Digital banking and payments operations

Continuous enhancement of mobile, online, and payments capabilities keeps BCB Bank aligned with 2024 industry norms where mobile channels exceed 70% of retail digital sessions; development focuses on feature velocity and API-driven payments. Uptime and cybersecurity are monitored with enterprise SLAs (targeting 99.99% availability) and real-time threat detection to protect transactions and user experience. Vendor coordination drives quarterly releases and cross-system integrations to minimize latency and rollback risk.

- Uptime: 99.99% SLA

- Mobile share: >70% of digital sessions (2024)

- Release cadence: quarterly vendor-coordinated

Retail-funded lending: ALM controls, mobile-led growth, strong AML and underwriting

BCB funds lending with retail deposits (US banks held $16.9T in deposits YE 2024), pricing and branch/relationship sales drive retention; ALM and stress-testing limit interest-rate risk. Underwriting uses cash-flow, LTV and scenario models; >4,000,000 SARs industry scale (2023–24) support AML controls. Digital: >70% mobile sessions (2024), 99.99% uptime SLA.

| Metric | 2024 |

|---|---|

| US deposits | $16.9T |

| Mobile share | >70% |

| SARs (industry) | >4,000,000 |

| Uptime SLA | 99.99% |

Preview Before You Purchase

Business Model Canvas

The BCB Bank Business Model Canvas you’re previewing is the actual deliverable, not a mockup—this snapshot is taken directly from the final file you’ll receive. Upon purchase you’ll gain immediate access to the complete, editable document in Word and Excel formats. It’s fully formatted, comprehensive and ready to present or customize—no surprises, just the same professional file shown here.

Description

Business Model Canvas for Retail Banks: Actionable Map of Customers, Revenue & Channels

Unlock BCB Bank’s strategic blueprint with our Business Model Canvas: concise mapping of customer segments, value propositions, channels, revenue streams and cost drivers. Ideal for investors, consultants and founders seeking actionable, company-specific insights. Purchase the full, editable Canvas in Word and Excel to benchmark and implement proven banking strategies.

Partnerships

Correspondent and syndication banks

BCB partners with regional and national correspondent and syndication banks to join larger commercial credits, sharing risk and expanding lending capacity. In 2024 global syndicated loan issuance topped roughly 2 trillion USD, reinforcing reciprocal deal flow and liquidity options for participants. These partnerships prevent overconcentration while enabling larger ticket lending and secondary market exits.

Fintech and core technology providers

Core processors, digital banking vendors, and payments partners enable mobile, online, and real-time services while delivering regulatory-grade security through standards such as PCI DSS and ISO 27001. These partnerships accelerate feature rollout—BCB can leverage ready APIs and connectors to shorten delivery cycles and scale payment rails. Integration with certified vendors lowers time-to-market and reduces development costs by replacing bespoke builds with proven platforms.

Broker-dealers and loan brokers

Partnerships with mortgage brokers and commercial loan originators broaden BCB Bank’s pipeline, leveraging brokers who handled about one-third of U.S. mortgage originations in 2024 to source high-quality borrowers in New Jersey and New York metros. Structured referral arrangements align incentives and enforce common underwriting standards and documentation requirements, improving referral-to-funding conversion and credit quality.

Title, appraisal, and legal firms

Trusted title, appraisal and legal firms enable secure, compliant mortgage and CRE lending, centralizing chain-of-title and valuation expertise. Standardized processes and SLAs shorten cycle times—ICE Mortgage Technology reported a 2024 national average mortgage close of 45 days, with SLAs commonly cutting internal turnaround by ~30%. Independent validation improves credit quality and creates robust audit trails that lower post-close defect risk.

- trusted-partners: title, appraisal, legal

- SLA-impact: 45d avg close (2024); ~30% faster with SLAs

- risk-mitigation: independent validation, stronger audit trails

Community organizations and chambers

Local nonprofits, chambers, and municipal entities boost BCB Bank brand visibility and trust, opening doors to households and small businesses in target neighborhoods. Collaborative financial education and outreach programs increase deposits and measurable inclusion; community banks held about 14% of U.S. domestic deposits in 2024 (FDIC). These partnerships create referral pipelines and joint product offerings that drive account growth.

- Target access: small-business and household referrals

- Impact: partnership-driven deposit growth

- Metric: community banks ~14% of U.S. deposits (FDIC 2024)

Partner network speeds lending, digital services and deposits while lowering concentration risk

BCB leverages correspondent/syndication banks, fintech processors, brokers, title/appraisal/legal firms, and community partners to expand lending capacity, accelerate digital services, source loans, ensure compliance, and grow deposits. 2024 benchmarks: global syndicated loans ~2T USD; community banks ~14% of US deposits; avg mortgage close 45 days. These partnerships reduce concentration, speed go-to-market, and improve credit controls.

| Partner | Role | 2024 Metric |

|---|---|---|

| Correspondents | Risk sharing | ~2T syndicated loans |

| Fintech/vendors | Digital/Payments | PCI DSS/ISO27001 |

| Brokers | Origination | ~33% mortgage originations |

| Title/Legal | Validation | 45d avg close |

| Community Orgs | Deposit/referrals | 14% US deposits |

What is included in the product

A tailored Business Model Canvas for BCB Bank detailing customer segments, channels, value propositions, revenue and cost streams, key resources and partners, and operational plans across the 9 BMC blocks, with linked SWOT, competitive advantages, and polished narrative for investor presentations and strategic decisions.

High-level view of BCB Bank’s business model with editable cells, relieving strategic alignment and presentation pain points. Shareable layout saves hours structuring analyses and enables fast, board-ready summaries for teams and advisors.

Activities

Deposit gathering and liquidity management

BCB Bank focuses on gathering checking, savings and money-market balances to fund lending, mirroring U.S. banks that held roughly $16.9 trillion in deposits at year-end 2024. Pricing, relationship banking and branch outreach drive acquisition and retention, with targeted rate tiers and product bundling. Rigorous ALM disciplines—duration management, liquidity buffers and stress-testing—optimize cost of funds and limit interest-rate risk.

Underwriting and portfolio management

Rigorous credit analysis underpins underwriting for commercial, residential, and construction loans, using borrower cash-flow, LTV, and scenario modelling to set risk-adjusted pricing. Ongoing monitoring, covenant tracking, and periodic stress testing preserve asset quality and enable timely remediation. Data-driven policies align origination targets with risk appetite to balance growth and risk-adjusted returns.

Customer service and relationship banking

Personalized support across branches, phone and digital channels drives loyalty, with 84% of customers in 2024 saying personalization matters. Relationship managers cross-sell to deepen share of wallet, typically raising product holdings per household by about 20%. Rapid issue resolution — linked to higher NPS — boosts retention, and Bain finds a 5% retention rise can increase profits 25–95%.

Regulatory compliance and risk controls

BCB Bank runs comprehensive BSA/AML, KYC, and fair lending programs, processing industry-scale alerts and supporting over 4 million SAR filings annually (industry 2023–24 range) to detect illicit flows; internal audit and timely examiner reporting sustain supervisory confidence and a satisfactory CAMELS-related control posture; robust controls protect reputation and capital, reducing regulatory fines and operational losses.

- Program scope: BSA/AML, KYC, fair lending

- Scale: >4,000,000 SARs industry-wide (2023–24)

- Controls: internal audit + examiner reporting

- Objective: protect reputation and capital

Digital banking and payments operations

Continuous enhancement of mobile, online, and payments capabilities keeps BCB Bank aligned with 2024 industry norms where mobile channels exceed 70% of retail digital sessions; development focuses on feature velocity and API-driven payments. Uptime and cybersecurity are monitored with enterprise SLAs (targeting 99.99% availability) and real-time threat detection to protect transactions and user experience. Vendor coordination drives quarterly releases and cross-system integrations to minimize latency and rollback risk.

- Uptime: 99.99% SLA

- Mobile share: >70% of digital sessions (2024)

- Release cadence: quarterly vendor-coordinated

Retail-funded lending: ALM controls, mobile-led growth, strong AML and underwriting

BCB funds lending with retail deposits (US banks held $16.9T in deposits YE 2024), pricing and branch/relationship sales drive retention; ALM and stress-testing limit interest-rate risk. Underwriting uses cash-flow, LTV and scenario models; >4,000,000 SARs industry scale (2023–24) support AML controls. Digital: >70% mobile sessions (2024), 99.99% uptime SLA.

| Metric | 2024 |

|---|---|

| US deposits | $16.9T |

| Mobile share | >70% |

| SARs (industry) | >4,000,000 |

| Uptime SLA | 99.99% |

Preview Before You Purchase

Business Model Canvas

The BCB Bank Business Model Canvas you’re previewing is the actual deliverable, not a mockup—this snapshot is taken directly from the final file you’ll receive. Upon purchase you’ll gain immediate access to the complete, editable document in Word and Excel formats. It’s fully formatted, comprehensive and ready to present or customize—no surprises, just the same professional file shown here.