BCB Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

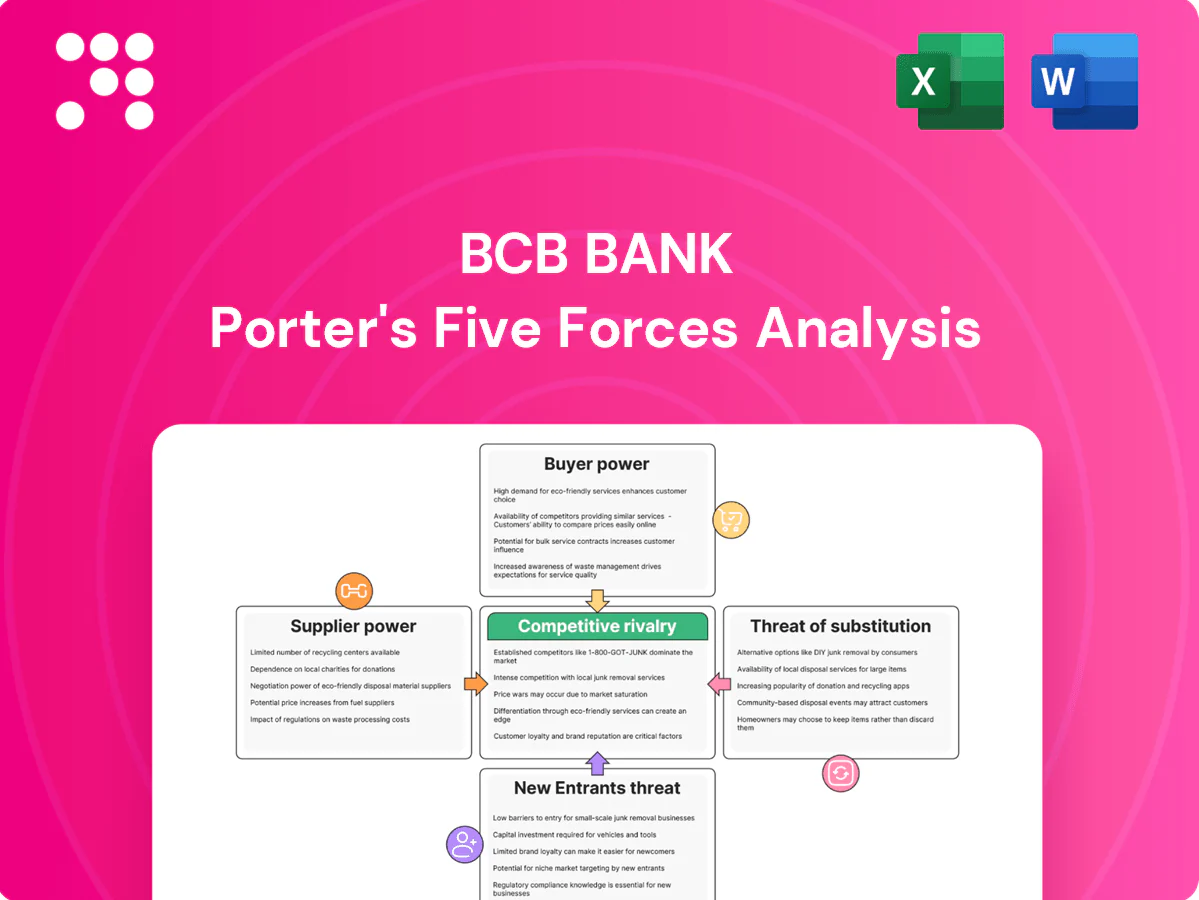

BCB Bank faces moderate buyer power and tightening margin pressure from digital rivals, while supplier leverage and regulatory barriers shape its cost and capital access. Competitive rivalry is intensifying as fintechs target niche segments, and threat of new entrants hinges on scale and compliance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic recommendations.

Suppliers Bargaining Power

Core tech and payments vendors

BCB depends on concentrated core processors, cloud services and payment networks, with top public cloud vendors (AWS, Azure, GCP) holding roughly two-thirds of the market in 2024, creating strong vendor leverage through lock-in and multiyear contracts. Integration complexity and bespoke interfaces raise switching costs and operational risk. Community bank consortia and standardized platforms can secure volume discounts and SLA clauses to mitigate pricing power and service risk.

Depositors as funding suppliers

Depositors fund lending with low-cost deposits, giving retail and commercial customers indirect supplier power through rate sensitivity; rising rates or competitive promos can force higher deposit costs—industry deposit beta in 2024 was roughly 30–40%. Relationship banking, insured balances and convenience reduce churn, while product bundling and treasury services deepen stickiness.

Wholesale funding providers

Access to FHLB advances, brokered CDs and interbank lines gives BCB Bank flexibility but at market-driven costs; with the federal funds target at 5.25–5.50% (July 2024), wholesale rates rose sharply. In tight liquidity providers gain pricing power and impose covenants. Overreliance raises interest expense and refinancing risk. Strong liquidity reduces dependence.

Talent and compliance expertise

Skilled lenders, risk officers and compliance staff are scarce in the NY/NJ market, raising supplier leverage as banks compete for a thin talent pool; wage inflation and rising regulatory complexity further increase dependence on specialized hires. Strong culture, clear career paths and local roots help BCB Bank retain staff and moderate cost pressure, while automation and targeted training programs can reduce reliance on scarce specialists.

Regulators as license gatekeepers

Regulators control charters, approvals and capital standards, effectively supplying market access and, in 2024, continued to tighten oversight after post‑pandemic reforms, raising compliance costs and narrowing strategic optionality for BCB Bank.

- Heightened scrutiny: higher compliance spend in 2024

- Predictable supervision: levels playing field vs under‑regulated entrants

- Proactive risk management: preserves strategic flexibility

Cloud concentration and higher funding costs squeeze banks: deposit beta 30–40%, cloud ~66%

BCB faces concentrated vendor leverage: top public cloud vendors held ~66% market share in 2024, raising lock‑in and switching costs. Deposit suppliers exhibit 2024 deposit beta ~30–40%, pressuring funding costs when rates rise. Wholesale liquidity costs rose with fed funds at 5.25–5.50% (Jul 2024), adding covenant risk. Skilled talent and tighter 2024 regulation increase operational supplier power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Cloud vendors | ~66% market share | High lock‑in |

| Depositors | Deposit beta 30–40% | Funding cost sensitivity |

| Wholesale | Fed funds 5.25–5.50% | Higher funding cost |

What is included in the product

Tailored Porter's Five Forces analysis for BCB Bank that uncovers competitive drivers, buyer and supplier power, threat of substitutes, and entry barriers, highlighting disruptive threats and strategic levers to protect market share and profitability.

One-sheet Porter's Five Forces for BCB Bank that instantly highlights competitive pressures and relief strategies for fast boardroom decisions. Customize force levels, swap in your data, and export a clean spider chart—ready to drop into decks or integrate with broader reports.

Customers Bargaining Power

Rate-sensitive retail depositors

Rate-sensitive retail depositors actively compare APYs across banks and fintechs, with top online savings accounts exceeding 4% in 2024 and 1-year CDs near 5%, pressuring BCB to raise pricing. Faster digital account opening and instant e-KYC lower switching friction, increasing churn risk. Loyalty programs and local branch relationships can damp pure rate shopping, while clear value propositions (convenience, advice) help retain core balances.

Small and mid-sized businesses

SMBs—which account for roughly 90% of businesses and about 50% of employment globally (World Bank)—demand competitively priced credit, treasury and payments with fast decisions and often multi-bank and auctioned loan terms, giving them meaningful bargaining power. Relationship managers, tailored credit packages and bundled cash-management and payments can offset price pressure by raising SMB switching costs.

Mortgage and CRE borrowers

Mortgage and CRE borrowers shop rates and terms widely—Freddie Mac showed the US 30-year fixed averaged about 7.0% in 2024—using brokers and online marketplaces that compress spreads and fees. Competitive pressure shaved lender margins and drove fee discounting while CBRE data put national CRE cap rates near 6.8% in 2024. Speed, certainty of close, and local underwriting expertise justify modest premiums, and prudent structuring balances credit risk with win rates.

High-balance clients

High-balance clients (commonly defined as deposits or lending relationships above $1,000,000) wield strong pricing leverage, negotiating preferential rates and fees; in 2024 such clients remain core to liquidity strategies. Their exit can create funding gaps and concentration risk for BCB, so dedicated coverage teams and bespoke packaging are used to improve retention and margins. Diversifying the loan and deposit book reduces single-client bargaining power and systemic exposure.

- Large-client threshold: $1,000,000

- Mitigation: dedicated coverage teams

- Retention: bespoke pricing and packages

- Risk control: diversify to lower single-client concentration

Digitally savvy customers

Digitally savvy customers demand seamless mobile journeys, instant payments, and 24/7 support, with mobile banking penetration topping 70% in many markets by 2024 and instant payment volumes rising ~20% year-over-year; poor UX drives switches to fintechs, elevating buyer power. Continuous app enhancements and strong service recovery lower churn, while partnerships accelerate feature delivery and reduce time-to-market.

- Mobile penetration: >70% (2024)

- Instant payments growth: ~20% YoY (2024)

- Poor UX -> higher churn

- App upgrades + service recovery = reduced buyer power

- Partnerships speed feature delivery

Deposit rates (>4%) and 1yr CDs (~5%) raise funding costs; mobile (>70%) fuels churn

Retail depositors push rates (top online savings >4%, 1yr CDs ~5% in 2024), increasing funding costs; SMBs demand competitive credit/treasury with fast decisions, raising price pressure. High-balance clients (>$1,000,000) extract preferential pricing, posing concentration risk; mortgage/CRE rate shopping (30yr ~7.0%, CRE cap ~6.8% in 2024) compresses spreads. Mobile penetration >70% and instant payments +20% YoY heighten churn risk, so tailored coverage and UX reduce bargaining power.

| Metric | 2024 |

|---|---|

| Top online savings APY | >4% |

| 1yr CD | ~5% |

| 30yr mortgage | ~7.0% |

| CRE cap rate | ~6.8% |

| Mobile penetration | >70% |

| Instant payments growth | ~20% YoY |

| Large-client threshold | $1,000,000 |

Same Document Delivered

BCB Bank Porter's Five Forces Analysis

This preview is the exact BCB Bank Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file shown is the professionally formatted, final document ready for immediate download and use. Purchase grants instant access to this identical deliverable.

Don't Miss the Bigger Picture

BCB Bank faces moderate buyer power and tightening margin pressure from digital rivals, while supplier leverage and regulatory barriers shape its cost and capital access. Competitive rivalry is intensifying as fintechs target niche segments, and threat of new entrants hinges on scale and compliance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic recommendations.

Suppliers Bargaining Power

Core tech and payments vendors

BCB depends on concentrated core processors, cloud services and payment networks, with top public cloud vendors (AWS, Azure, GCP) holding roughly two-thirds of the market in 2024, creating strong vendor leverage through lock-in and multiyear contracts. Integration complexity and bespoke interfaces raise switching costs and operational risk. Community bank consortia and standardized platforms can secure volume discounts and SLA clauses to mitigate pricing power and service risk.

Depositors as funding suppliers

Depositors fund lending with low-cost deposits, giving retail and commercial customers indirect supplier power through rate sensitivity; rising rates or competitive promos can force higher deposit costs—industry deposit beta in 2024 was roughly 30–40%. Relationship banking, insured balances and convenience reduce churn, while product bundling and treasury services deepen stickiness.

Wholesale funding providers

Access to FHLB advances, brokered CDs and interbank lines gives BCB Bank flexibility but at market-driven costs; with the federal funds target at 5.25–5.50% (July 2024), wholesale rates rose sharply. In tight liquidity providers gain pricing power and impose covenants. Overreliance raises interest expense and refinancing risk. Strong liquidity reduces dependence.

Talent and compliance expertise

Skilled lenders, risk officers and compliance staff are scarce in the NY/NJ market, raising supplier leverage as banks compete for a thin talent pool; wage inflation and rising regulatory complexity further increase dependence on specialized hires. Strong culture, clear career paths and local roots help BCB Bank retain staff and moderate cost pressure, while automation and targeted training programs can reduce reliance on scarce specialists.

Regulators as license gatekeepers

Regulators control charters, approvals and capital standards, effectively supplying market access and, in 2024, continued to tighten oversight after post‑pandemic reforms, raising compliance costs and narrowing strategic optionality for BCB Bank.

- Heightened scrutiny: higher compliance spend in 2024

- Predictable supervision: levels playing field vs under‑regulated entrants

- Proactive risk management: preserves strategic flexibility

Cloud concentration and higher funding costs squeeze banks: deposit beta 30–40%, cloud ~66%

BCB faces concentrated vendor leverage: top public cloud vendors held ~66% market share in 2024, raising lock‑in and switching costs. Deposit suppliers exhibit 2024 deposit beta ~30–40%, pressuring funding costs when rates rise. Wholesale liquidity costs rose with fed funds at 5.25–5.50% (Jul 2024), adding covenant risk. Skilled talent and tighter 2024 regulation increase operational supplier power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Cloud vendors | ~66% market share | High lock‑in |

| Depositors | Deposit beta 30–40% | Funding cost sensitivity |

| Wholesale | Fed funds 5.25–5.50% | Higher funding cost |

What is included in the product

Tailored Porter's Five Forces analysis for BCB Bank that uncovers competitive drivers, buyer and supplier power, threat of substitutes, and entry barriers, highlighting disruptive threats and strategic levers to protect market share and profitability.

One-sheet Porter's Five Forces for BCB Bank that instantly highlights competitive pressures and relief strategies for fast boardroom decisions. Customize force levels, swap in your data, and export a clean spider chart—ready to drop into decks or integrate with broader reports.

Customers Bargaining Power

Rate-sensitive retail depositors

Rate-sensitive retail depositors actively compare APYs across banks and fintechs, with top online savings accounts exceeding 4% in 2024 and 1-year CDs near 5%, pressuring BCB to raise pricing. Faster digital account opening and instant e-KYC lower switching friction, increasing churn risk. Loyalty programs and local branch relationships can damp pure rate shopping, while clear value propositions (convenience, advice) help retain core balances.

Small and mid-sized businesses

SMBs—which account for roughly 90% of businesses and about 50% of employment globally (World Bank)—demand competitively priced credit, treasury and payments with fast decisions and often multi-bank and auctioned loan terms, giving them meaningful bargaining power. Relationship managers, tailored credit packages and bundled cash-management and payments can offset price pressure by raising SMB switching costs.

Mortgage and CRE borrowers

Mortgage and CRE borrowers shop rates and terms widely—Freddie Mac showed the US 30-year fixed averaged about 7.0% in 2024—using brokers and online marketplaces that compress spreads and fees. Competitive pressure shaved lender margins and drove fee discounting while CBRE data put national CRE cap rates near 6.8% in 2024. Speed, certainty of close, and local underwriting expertise justify modest premiums, and prudent structuring balances credit risk with win rates.

High-balance clients

High-balance clients (commonly defined as deposits or lending relationships above $1,000,000) wield strong pricing leverage, negotiating preferential rates and fees; in 2024 such clients remain core to liquidity strategies. Their exit can create funding gaps and concentration risk for BCB, so dedicated coverage teams and bespoke packaging are used to improve retention and margins. Diversifying the loan and deposit book reduces single-client bargaining power and systemic exposure.

- Large-client threshold: $1,000,000

- Mitigation: dedicated coverage teams

- Retention: bespoke pricing and packages

- Risk control: diversify to lower single-client concentration

Digitally savvy customers

Digitally savvy customers demand seamless mobile journeys, instant payments, and 24/7 support, with mobile banking penetration topping 70% in many markets by 2024 and instant payment volumes rising ~20% year-over-year; poor UX drives switches to fintechs, elevating buyer power. Continuous app enhancements and strong service recovery lower churn, while partnerships accelerate feature delivery and reduce time-to-market.

- Mobile penetration: >70% (2024)

- Instant payments growth: ~20% YoY (2024)

- Poor UX -> higher churn

- App upgrades + service recovery = reduced buyer power

- Partnerships speed feature delivery

Deposit rates (>4%) and 1yr CDs (~5%) raise funding costs; mobile (>70%) fuels churn

Retail depositors push rates (top online savings >4%, 1yr CDs ~5% in 2024), increasing funding costs; SMBs demand competitive credit/treasury with fast decisions, raising price pressure. High-balance clients (>$1,000,000) extract preferential pricing, posing concentration risk; mortgage/CRE rate shopping (30yr ~7.0%, CRE cap ~6.8% in 2024) compresses spreads. Mobile penetration >70% and instant payments +20% YoY heighten churn risk, so tailored coverage and UX reduce bargaining power.

| Metric | 2024 |

|---|---|

| Top online savings APY | >4% |

| 1yr CD | ~5% |

| 30yr mortgage | ~7.0% |

| CRE cap rate | ~6.8% |

| Mobile penetration | >70% |

| Instant payments growth | ~20% YoY |

| Large-client threshold | $1,000,000 |

Same Document Delivered

BCB Bank Porter's Five Forces Analysis

This preview is the exact BCB Bank Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file shown is the professionally formatted, final document ready for immediate download and use. Purchase grants instant access to this identical deliverable.

Description

Don't Miss the Bigger Picture

BCB Bank faces moderate buyer power and tightening margin pressure from digital rivals, while supplier leverage and regulatory barriers shape its cost and capital access. Competitive rivalry is intensifying as fintechs target niche segments, and threat of new entrants hinges on scale and compliance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic recommendations.

Suppliers Bargaining Power

Core tech and payments vendors

BCB depends on concentrated core processors, cloud services and payment networks, with top public cloud vendors (AWS, Azure, GCP) holding roughly two-thirds of the market in 2024, creating strong vendor leverage through lock-in and multiyear contracts. Integration complexity and bespoke interfaces raise switching costs and operational risk. Community bank consortia and standardized platforms can secure volume discounts and SLA clauses to mitigate pricing power and service risk.

Depositors as funding suppliers

Depositors fund lending with low-cost deposits, giving retail and commercial customers indirect supplier power through rate sensitivity; rising rates or competitive promos can force higher deposit costs—industry deposit beta in 2024 was roughly 30–40%. Relationship banking, insured balances and convenience reduce churn, while product bundling and treasury services deepen stickiness.

Wholesale funding providers

Access to FHLB advances, brokered CDs and interbank lines gives BCB Bank flexibility but at market-driven costs; with the federal funds target at 5.25–5.50% (July 2024), wholesale rates rose sharply. In tight liquidity providers gain pricing power and impose covenants. Overreliance raises interest expense and refinancing risk. Strong liquidity reduces dependence.

Talent and compliance expertise

Skilled lenders, risk officers and compliance staff are scarce in the NY/NJ market, raising supplier leverage as banks compete for a thin talent pool; wage inflation and rising regulatory complexity further increase dependence on specialized hires. Strong culture, clear career paths and local roots help BCB Bank retain staff and moderate cost pressure, while automation and targeted training programs can reduce reliance on scarce specialists.

Regulators as license gatekeepers

Regulators control charters, approvals and capital standards, effectively supplying market access and, in 2024, continued to tighten oversight after post‑pandemic reforms, raising compliance costs and narrowing strategic optionality for BCB Bank.

- Heightened scrutiny: higher compliance spend in 2024

- Predictable supervision: levels playing field vs under‑regulated entrants

- Proactive risk management: preserves strategic flexibility

Cloud concentration and higher funding costs squeeze banks: deposit beta 30–40%, cloud ~66%

BCB faces concentrated vendor leverage: top public cloud vendors held ~66% market share in 2024, raising lock‑in and switching costs. Deposit suppliers exhibit 2024 deposit beta ~30–40%, pressuring funding costs when rates rise. Wholesale liquidity costs rose with fed funds at 5.25–5.50% (Jul 2024), adding covenant risk. Skilled talent and tighter 2024 regulation increase operational supplier power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Cloud vendors | ~66% market share | High lock‑in |

| Depositors | Deposit beta 30–40% | Funding cost sensitivity |

| Wholesale | Fed funds 5.25–5.50% | Higher funding cost |

What is included in the product

Tailored Porter's Five Forces analysis for BCB Bank that uncovers competitive drivers, buyer and supplier power, threat of substitutes, and entry barriers, highlighting disruptive threats and strategic levers to protect market share and profitability.

One-sheet Porter's Five Forces for BCB Bank that instantly highlights competitive pressures and relief strategies for fast boardroom decisions. Customize force levels, swap in your data, and export a clean spider chart—ready to drop into decks or integrate with broader reports.

Customers Bargaining Power

Rate-sensitive retail depositors

Rate-sensitive retail depositors actively compare APYs across banks and fintechs, with top online savings accounts exceeding 4% in 2024 and 1-year CDs near 5%, pressuring BCB to raise pricing. Faster digital account opening and instant e-KYC lower switching friction, increasing churn risk. Loyalty programs and local branch relationships can damp pure rate shopping, while clear value propositions (convenience, advice) help retain core balances.

Small and mid-sized businesses

SMBs—which account for roughly 90% of businesses and about 50% of employment globally (World Bank)—demand competitively priced credit, treasury and payments with fast decisions and often multi-bank and auctioned loan terms, giving them meaningful bargaining power. Relationship managers, tailored credit packages and bundled cash-management and payments can offset price pressure by raising SMB switching costs.

Mortgage and CRE borrowers

Mortgage and CRE borrowers shop rates and terms widely—Freddie Mac showed the US 30-year fixed averaged about 7.0% in 2024—using brokers and online marketplaces that compress spreads and fees. Competitive pressure shaved lender margins and drove fee discounting while CBRE data put national CRE cap rates near 6.8% in 2024. Speed, certainty of close, and local underwriting expertise justify modest premiums, and prudent structuring balances credit risk with win rates.

High-balance clients

High-balance clients (commonly defined as deposits or lending relationships above $1,000,000) wield strong pricing leverage, negotiating preferential rates and fees; in 2024 such clients remain core to liquidity strategies. Their exit can create funding gaps and concentration risk for BCB, so dedicated coverage teams and bespoke packaging are used to improve retention and margins. Diversifying the loan and deposit book reduces single-client bargaining power and systemic exposure.

- Large-client threshold: $1,000,000

- Mitigation: dedicated coverage teams

- Retention: bespoke pricing and packages

- Risk control: diversify to lower single-client concentration

Digitally savvy customers

Digitally savvy customers demand seamless mobile journeys, instant payments, and 24/7 support, with mobile banking penetration topping 70% in many markets by 2024 and instant payment volumes rising ~20% year-over-year; poor UX drives switches to fintechs, elevating buyer power. Continuous app enhancements and strong service recovery lower churn, while partnerships accelerate feature delivery and reduce time-to-market.

- Mobile penetration: >70% (2024)

- Instant payments growth: ~20% YoY (2024)

- Poor UX -> higher churn

- App upgrades + service recovery = reduced buyer power

- Partnerships speed feature delivery

Deposit rates (>4%) and 1yr CDs (~5%) raise funding costs; mobile (>70%) fuels churn

Retail depositors push rates (top online savings >4%, 1yr CDs ~5% in 2024), increasing funding costs; SMBs demand competitive credit/treasury with fast decisions, raising price pressure. High-balance clients (>$1,000,000) extract preferential pricing, posing concentration risk; mortgage/CRE rate shopping (30yr ~7.0%, CRE cap ~6.8% in 2024) compresses spreads. Mobile penetration >70% and instant payments +20% YoY heighten churn risk, so tailored coverage and UX reduce bargaining power.

| Metric | 2024 |

|---|---|

| Top online savings APY | >4% |

| 1yr CD | ~5% |

| 30yr mortgage | ~7.0% |

| CRE cap rate | ~6.8% |

| Mobile penetration | >70% |

| Instant payments growth | ~20% YoY |

| Large-client threshold | $1,000,000 |

Same Document Delivered

BCB Bank Porter's Five Forces Analysis

This preview is the exact BCB Bank Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file shown is the professionally formatted, final document ready for immediate download and use. Purchase grants instant access to this identical deliverable.