Bank Of Chengdu Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

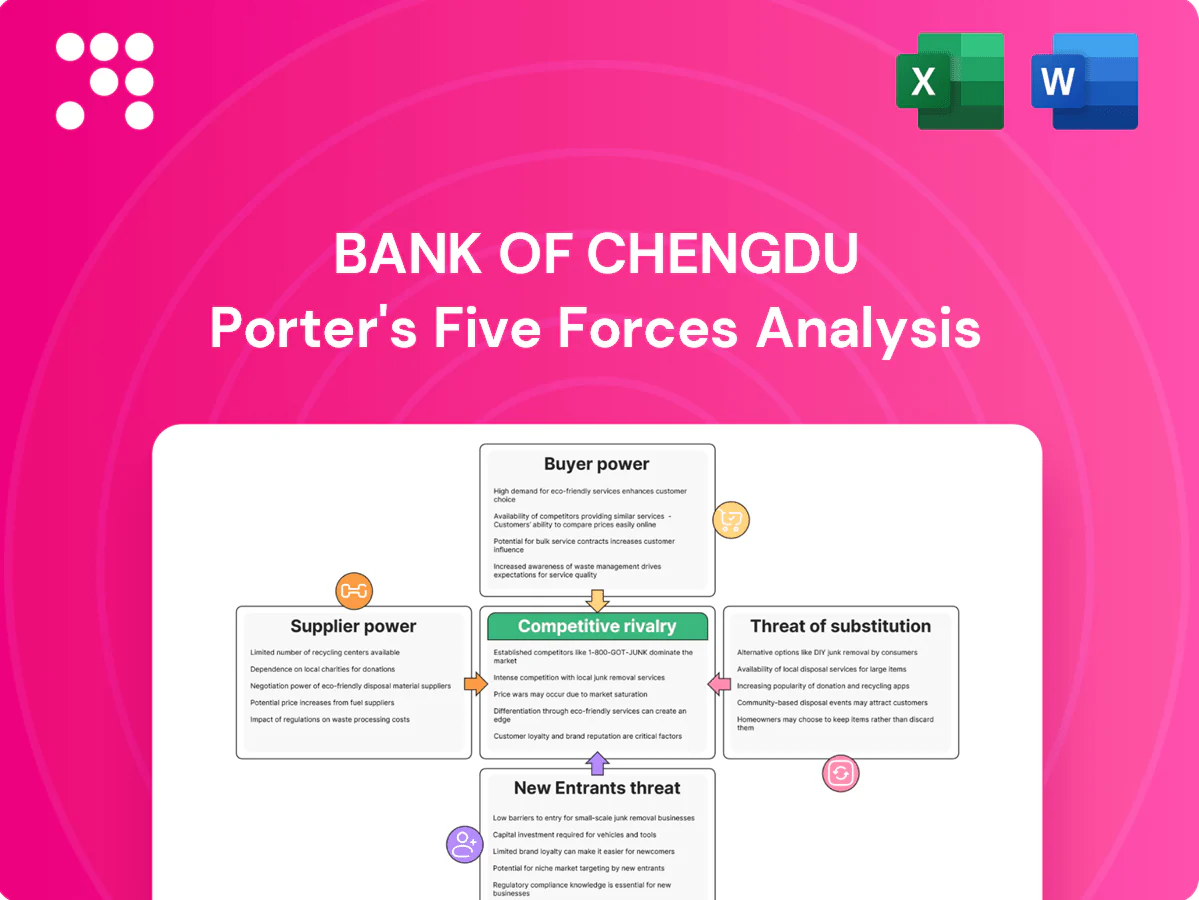

Bank of Chengdu’s Porter's Five Forces snapshot shows moderate rivalry, rising buyer expectations, manageable supplier power, limited threat from substitutes, and potential pressure from new entrants as fintech grows; strategic positioning and regional strengths mitigate some risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank Of Chengdu’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Stable retail deposits base

Household deposits remain Bank of Chengdu’s primary low-cost funding input, keeping supplier power moderate; China’s deposit insurance cap of 500,000 CNY and regulatory rate frameworks limit depositor leverage. Rapid digital adoption—about 1.06 billion internet users in China—facilitates rate comparison and wealth alternatives, pressuring pricing, so service quality and convenience are key to retaining this stable base.

Wholesale and interbank funding

Access to interbank markets and negotiable certificates of deposit makes Bank of Chengdu sensitive to market rates, with China's interbank repo daily turnover exceeding RMB 10 trillion in 2024, amplifying rate transmission.

In tight liquidity cycles suppliers extract power via wider spreads and volume caps, as seen in 2024 episodic repo spikes and NCD repricing.

PBOC open market operations and standing facilities—used frequently in 2024—can swiftly ease or tighten conditions, shifting supplier leverage.

Diversified tenors and contingency lines reduce exposure to short-term spikes, capping funding stress during 2024 liquidity episodes.

Technology and core systems vendors

Core banking is dominated by five global vendors (Temenos, Infosys Finacle, FIS, Fiserv, Oracle) while cloud is led by three hyperscalers (AWS, Azure, GCP), creating concentrated supplier power. Long implementation cycles of 12–36 months lock in contractual terms and fees, increasing switching costs. Limited qualified suppliers for mission-critical systems amplify leverage, though multi-vendor architectures and growing in-house development reduce dependency.

Payment rails and data utilities

Payment rails and data utilities such as UnionPay (over 80% domestic card share in 2024), CNAPS interbank clearing (settling >CNY 200 trillion in 2023), the PBOC Credit Reference Center (≈1 billion+ records by 2024) and national identity networks are essential suppliers; standardized fee frameworks cap extreme pricing but add unavoidable cost layers. API and open-banking integrations can entrench specific providers, raising switching costs; negotiating volume-based pricing and building redundancy reduces their leverage.

- UnionPay: >80% market share (2024)

- CNAPS: >CNY 200T settled (2023)

- PBOC CRC: ≈1B records (2024)

- Mitigants: volume discounts, multi-vendor redundancy, API abstraction

Specialized talent and branches

Specialized risk, fintech and wealth-management talent is scarce in Chengdu (city population ~21.0 million per 2020 census), giving labor suppliers leverage; national banks and tech firms intensify wage pressure and compete for hires. Prime branch locations command premium rents, raising operating costs, while improved talent pipelines and branch-footprint optimization (closed/open ratio focus) reduce exposure.

- High supplier leverage

- Wage pressure from national banks/tech

- Premium branch rents

- Mitigants: talent pipelines, footprint optimization

Funding squeeze as turnover >CNY 10T, users 1.06B

Supplier power is moderate: household deposits remain low-cost but digital channels (1.06B internet users, 2024) raise price sensitivity. Interbank repo turnover >CNY 10T (2024) and episodic repo spikes increased market funding leverage. Tech/vendor concentration and scarce fintech talent in Chengdu (≈21.0M) raise switching costs.

| Metric | 2024 |

|---|---|

| Interbank repo turnover | >CNY 10T |

| UnionPay share | >80% |

| PBOC CRC records | ≈1B |

| Chengdu population | ≈21.0M |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bank Of Chengdu, detailing each competitive force with strategic commentary and highlighting disruptive threats, buyer/supplier control, and market dynamics that protect or expose the bank.

One-sheet Porter's Five Forces for Bank of Chengdu—clear, board-ready summary that instantly highlights competitive pressures. Customize force levels, swap in your own data, or view a spider chart to translate strategic risk into quick, actionable decisions.

Customers Bargaining Power

Retail customers’ switching costs

Individuals place high value on convenience, super-app payments and nearby branches, keeping switching costs moderate despite competition. Over 1 billion mobile payment users in China in 2024 and faster digital onboarding reduce friction, modestly boosting buyer power. Rate sensitivity rises in slowdowns, pushing customers to seek better deposit/loan rates. Loyalty programs and seamless mobile UX remain key anchors for retention.

SME clients’ price sensitivity

SME clients strictly compare loan rates, fees and approval speed across local banks and fintechs, with 65% of SMEs using at least two providers in 2024, raising price sensitivity. Multi-banking and ready switching increase bargaining power and compress net interest margins for Bank of Chengdu. Supply-chain finance alternatives push expectations for sub-week turnaround. Bundled cash management and advisory services help offset pure price negotiations.

Large corporates’ negotiating leverage

Large corporates, including blue-chip and state-linked entities, often demand bespoke pricing and credit limits, with single-client transaction volumes commonly in the CNY billions, prompting fee waivers and tighter spreads. Their volumes give them strong negotiating leverage and in 2024 the majority of mandates moved through relationship banking and syndications, intensifying competition. Offering integrated FX, DCM and cash solutions is critical to preserve wallet share.

Wealth and affluent segments

Affluent clients at Bank of Chengdu increasingly shop yields and product breadth across banks and securities firms; in 2024 mobile channels drove over 80% of retail banking transactions, boosting fee transparency and bargaining power. Suitability and risk-control services still command premium pricing; exclusive structured products and advisory deepen stickiness.

- Price-sensitive but service-driven

- Mobile transparency raises fee pressure

- Risk-control differentiator

- Exclusive products increase retention

Digital-first expectations

Buyers demand 24/7 digital service, instant payments and embedded finance; with China exceeding 1 billion mobile banking users in 2024, poor app experience drives rapid churn to rivals. Public ratings and feedback amplify non-price bargaining power, and app-store scores often determine acquisition. Continuous app upgrades and strict SLAs are therefore essential for retention.

- 24/7 digital service

- Instant payments

- Embedded finance

- Non-price power via ratings/public feedback

- Continuous upgrades + SLAs

Customers gain leverage: 1B+ mobile users, 80%+ txns

Customers exert moderate-to-strong bargaining power: retail convenience and >1B mobile payment users in 2024 lower switching costs; 80%+ retail transactions are mobile boosting fee transparency. 65% of SMEs use at least two providers, increasing price pressure and compressing NIMs. Large corporates command bespoke pricing and volumes, keeping negotiation leverage high.

| Metric | 2024 |

|---|---|

| Mobile payment users | 1B+ |

| Retail mobile txn share | 80%+ |

| SMEs using ≥2 providers | 65% |

Full Version Awaits

Bank Of Chengdu Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Bank of Chengdu you will receive after purchase—no placeholders or summaries. The document you see is fully formatted, professionally written, and ready for immediate download and use the moment you complete payment. What’s displayed here is the final deliverable, identical to the file you will obtain.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bank of Chengdu’s Porter's Five Forces snapshot shows moderate rivalry, rising buyer expectations, manageable supplier power, limited threat from substitutes, and potential pressure from new entrants as fintech grows; strategic positioning and regional strengths mitigate some risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank Of Chengdu’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Stable retail deposits base

Household deposits remain Bank of Chengdu’s primary low-cost funding input, keeping supplier power moderate; China’s deposit insurance cap of 500,000 CNY and regulatory rate frameworks limit depositor leverage. Rapid digital adoption—about 1.06 billion internet users in China—facilitates rate comparison and wealth alternatives, pressuring pricing, so service quality and convenience are key to retaining this stable base.

Wholesale and interbank funding

Access to interbank markets and negotiable certificates of deposit makes Bank of Chengdu sensitive to market rates, with China's interbank repo daily turnover exceeding RMB 10 trillion in 2024, amplifying rate transmission.

In tight liquidity cycles suppliers extract power via wider spreads and volume caps, as seen in 2024 episodic repo spikes and NCD repricing.

PBOC open market operations and standing facilities—used frequently in 2024—can swiftly ease or tighten conditions, shifting supplier leverage.

Diversified tenors and contingency lines reduce exposure to short-term spikes, capping funding stress during 2024 liquidity episodes.

Technology and core systems vendors

Core banking is dominated by five global vendors (Temenos, Infosys Finacle, FIS, Fiserv, Oracle) while cloud is led by three hyperscalers (AWS, Azure, GCP), creating concentrated supplier power. Long implementation cycles of 12–36 months lock in contractual terms and fees, increasing switching costs. Limited qualified suppliers for mission-critical systems amplify leverage, though multi-vendor architectures and growing in-house development reduce dependency.

Payment rails and data utilities

Payment rails and data utilities such as UnionPay (over 80% domestic card share in 2024), CNAPS interbank clearing (settling >CNY 200 trillion in 2023), the PBOC Credit Reference Center (≈1 billion+ records by 2024) and national identity networks are essential suppliers; standardized fee frameworks cap extreme pricing but add unavoidable cost layers. API and open-banking integrations can entrench specific providers, raising switching costs; negotiating volume-based pricing and building redundancy reduces their leverage.

- UnionPay: >80% market share (2024)

- CNAPS: >CNY 200T settled (2023)

- PBOC CRC: ≈1B records (2024)

- Mitigants: volume discounts, multi-vendor redundancy, API abstraction

Specialized talent and branches

Specialized risk, fintech and wealth-management talent is scarce in Chengdu (city population ~21.0 million per 2020 census), giving labor suppliers leverage; national banks and tech firms intensify wage pressure and compete for hires. Prime branch locations command premium rents, raising operating costs, while improved talent pipelines and branch-footprint optimization (closed/open ratio focus) reduce exposure.

- High supplier leverage

- Wage pressure from national banks/tech

- Premium branch rents

- Mitigants: talent pipelines, footprint optimization

Funding squeeze as turnover >CNY 10T, users 1.06B

Supplier power is moderate: household deposits remain low-cost but digital channels (1.06B internet users, 2024) raise price sensitivity. Interbank repo turnover >CNY 10T (2024) and episodic repo spikes increased market funding leverage. Tech/vendor concentration and scarce fintech talent in Chengdu (≈21.0M) raise switching costs.

| Metric | 2024 |

|---|---|

| Interbank repo turnover | >CNY 10T |

| UnionPay share | >80% |

| PBOC CRC records | ≈1B |

| Chengdu population | ≈21.0M |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bank Of Chengdu, detailing each competitive force with strategic commentary and highlighting disruptive threats, buyer/supplier control, and market dynamics that protect or expose the bank.

One-sheet Porter's Five Forces for Bank of Chengdu—clear, board-ready summary that instantly highlights competitive pressures. Customize force levels, swap in your own data, or view a spider chart to translate strategic risk into quick, actionable decisions.

Customers Bargaining Power

Retail customers’ switching costs

Individuals place high value on convenience, super-app payments and nearby branches, keeping switching costs moderate despite competition. Over 1 billion mobile payment users in China in 2024 and faster digital onboarding reduce friction, modestly boosting buyer power. Rate sensitivity rises in slowdowns, pushing customers to seek better deposit/loan rates. Loyalty programs and seamless mobile UX remain key anchors for retention.

SME clients’ price sensitivity

SME clients strictly compare loan rates, fees and approval speed across local banks and fintechs, with 65% of SMEs using at least two providers in 2024, raising price sensitivity. Multi-banking and ready switching increase bargaining power and compress net interest margins for Bank of Chengdu. Supply-chain finance alternatives push expectations for sub-week turnaround. Bundled cash management and advisory services help offset pure price negotiations.

Large corporates’ negotiating leverage

Large corporates, including blue-chip and state-linked entities, often demand bespoke pricing and credit limits, with single-client transaction volumes commonly in the CNY billions, prompting fee waivers and tighter spreads. Their volumes give them strong negotiating leverage and in 2024 the majority of mandates moved through relationship banking and syndications, intensifying competition. Offering integrated FX, DCM and cash solutions is critical to preserve wallet share.

Wealth and affluent segments

Affluent clients at Bank of Chengdu increasingly shop yields and product breadth across banks and securities firms; in 2024 mobile channels drove over 80% of retail banking transactions, boosting fee transparency and bargaining power. Suitability and risk-control services still command premium pricing; exclusive structured products and advisory deepen stickiness.

- Price-sensitive but service-driven

- Mobile transparency raises fee pressure

- Risk-control differentiator

- Exclusive products increase retention

Digital-first expectations

Buyers demand 24/7 digital service, instant payments and embedded finance; with China exceeding 1 billion mobile banking users in 2024, poor app experience drives rapid churn to rivals. Public ratings and feedback amplify non-price bargaining power, and app-store scores often determine acquisition. Continuous app upgrades and strict SLAs are therefore essential for retention.

- 24/7 digital service

- Instant payments

- Embedded finance

- Non-price power via ratings/public feedback

- Continuous upgrades + SLAs

Customers gain leverage: 1B+ mobile users, 80%+ txns

Customers exert moderate-to-strong bargaining power: retail convenience and >1B mobile payment users in 2024 lower switching costs; 80%+ retail transactions are mobile boosting fee transparency. 65% of SMEs use at least two providers, increasing price pressure and compressing NIMs. Large corporates command bespoke pricing and volumes, keeping negotiation leverage high.

| Metric | 2024 |

|---|---|

| Mobile payment users | 1B+ |

| Retail mobile txn share | 80%+ |

| SMEs using ≥2 providers | 65% |

Full Version Awaits

Bank Of Chengdu Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Bank of Chengdu you will receive after purchase—no placeholders or summaries. The document you see is fully formatted, professionally written, and ready for immediate download and use the moment you complete payment. What’s displayed here is the final deliverable, identical to the file you will obtain.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bank of Chengdu’s Porter's Five Forces snapshot shows moderate rivalry, rising buyer expectations, manageable supplier power, limited threat from substitutes, and potential pressure from new entrants as fintech grows; strategic positioning and regional strengths mitigate some risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank Of Chengdu’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Stable retail deposits base

Household deposits remain Bank of Chengdu’s primary low-cost funding input, keeping supplier power moderate; China’s deposit insurance cap of 500,000 CNY and regulatory rate frameworks limit depositor leverage. Rapid digital adoption—about 1.06 billion internet users in China—facilitates rate comparison and wealth alternatives, pressuring pricing, so service quality and convenience are key to retaining this stable base.

Wholesale and interbank funding

Access to interbank markets and negotiable certificates of deposit makes Bank of Chengdu sensitive to market rates, with China's interbank repo daily turnover exceeding RMB 10 trillion in 2024, amplifying rate transmission.

In tight liquidity cycles suppliers extract power via wider spreads and volume caps, as seen in 2024 episodic repo spikes and NCD repricing.

PBOC open market operations and standing facilities—used frequently in 2024—can swiftly ease or tighten conditions, shifting supplier leverage.

Diversified tenors and contingency lines reduce exposure to short-term spikes, capping funding stress during 2024 liquidity episodes.

Technology and core systems vendors

Core banking is dominated by five global vendors (Temenos, Infosys Finacle, FIS, Fiserv, Oracle) while cloud is led by three hyperscalers (AWS, Azure, GCP), creating concentrated supplier power. Long implementation cycles of 12–36 months lock in contractual terms and fees, increasing switching costs. Limited qualified suppliers for mission-critical systems amplify leverage, though multi-vendor architectures and growing in-house development reduce dependency.

Payment rails and data utilities

Payment rails and data utilities such as UnionPay (over 80% domestic card share in 2024), CNAPS interbank clearing (settling >CNY 200 trillion in 2023), the PBOC Credit Reference Center (≈1 billion+ records by 2024) and national identity networks are essential suppliers; standardized fee frameworks cap extreme pricing but add unavoidable cost layers. API and open-banking integrations can entrench specific providers, raising switching costs; negotiating volume-based pricing and building redundancy reduces their leverage.

- UnionPay: >80% market share (2024)

- CNAPS: >CNY 200T settled (2023)

- PBOC CRC: ≈1B records (2024)

- Mitigants: volume discounts, multi-vendor redundancy, API abstraction

Specialized talent and branches

Specialized risk, fintech and wealth-management talent is scarce in Chengdu (city population ~21.0 million per 2020 census), giving labor suppliers leverage; national banks and tech firms intensify wage pressure and compete for hires. Prime branch locations command premium rents, raising operating costs, while improved talent pipelines and branch-footprint optimization (closed/open ratio focus) reduce exposure.

- High supplier leverage

- Wage pressure from national banks/tech

- Premium branch rents

- Mitigants: talent pipelines, footprint optimization

Funding squeeze as turnover >CNY 10T, users 1.06B

Supplier power is moderate: household deposits remain low-cost but digital channels (1.06B internet users, 2024) raise price sensitivity. Interbank repo turnover >CNY 10T (2024) and episodic repo spikes increased market funding leverage. Tech/vendor concentration and scarce fintech talent in Chengdu (≈21.0M) raise switching costs.

| Metric | 2024 |

|---|---|

| Interbank repo turnover | >CNY 10T |

| UnionPay share | >80% |

| PBOC CRC records | ≈1B |

| Chengdu population | ≈21.0M |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bank Of Chengdu, detailing each competitive force with strategic commentary and highlighting disruptive threats, buyer/supplier control, and market dynamics that protect or expose the bank.

One-sheet Porter's Five Forces for Bank of Chengdu—clear, board-ready summary that instantly highlights competitive pressures. Customize force levels, swap in your own data, or view a spider chart to translate strategic risk into quick, actionable decisions.

Customers Bargaining Power

Retail customers’ switching costs

Individuals place high value on convenience, super-app payments and nearby branches, keeping switching costs moderate despite competition. Over 1 billion mobile payment users in China in 2024 and faster digital onboarding reduce friction, modestly boosting buyer power. Rate sensitivity rises in slowdowns, pushing customers to seek better deposit/loan rates. Loyalty programs and seamless mobile UX remain key anchors for retention.

SME clients’ price sensitivity

SME clients strictly compare loan rates, fees and approval speed across local banks and fintechs, with 65% of SMEs using at least two providers in 2024, raising price sensitivity. Multi-banking and ready switching increase bargaining power and compress net interest margins for Bank of Chengdu. Supply-chain finance alternatives push expectations for sub-week turnaround. Bundled cash management and advisory services help offset pure price negotiations.

Large corporates’ negotiating leverage

Large corporates, including blue-chip and state-linked entities, often demand bespoke pricing and credit limits, with single-client transaction volumes commonly in the CNY billions, prompting fee waivers and tighter spreads. Their volumes give them strong negotiating leverage and in 2024 the majority of mandates moved through relationship banking and syndications, intensifying competition. Offering integrated FX, DCM and cash solutions is critical to preserve wallet share.

Wealth and affluent segments

Affluent clients at Bank of Chengdu increasingly shop yields and product breadth across banks and securities firms; in 2024 mobile channels drove over 80% of retail banking transactions, boosting fee transparency and bargaining power. Suitability and risk-control services still command premium pricing; exclusive structured products and advisory deepen stickiness.

- Price-sensitive but service-driven

- Mobile transparency raises fee pressure

- Risk-control differentiator

- Exclusive products increase retention

Digital-first expectations

Buyers demand 24/7 digital service, instant payments and embedded finance; with China exceeding 1 billion mobile banking users in 2024, poor app experience drives rapid churn to rivals. Public ratings and feedback amplify non-price bargaining power, and app-store scores often determine acquisition. Continuous app upgrades and strict SLAs are therefore essential for retention.

- 24/7 digital service

- Instant payments

- Embedded finance

- Non-price power via ratings/public feedback

- Continuous upgrades + SLAs

Customers gain leverage: 1B+ mobile users, 80%+ txns

Customers exert moderate-to-strong bargaining power: retail convenience and >1B mobile payment users in 2024 lower switching costs; 80%+ retail transactions are mobile boosting fee transparency. 65% of SMEs use at least two providers, increasing price pressure and compressing NIMs. Large corporates command bespoke pricing and volumes, keeping negotiation leverage high.

| Metric | 2024 |

|---|---|

| Mobile payment users | 1B+ |

| Retail mobile txn share | 80%+ |

| SMEs using ≥2 providers | 65% |

Full Version Awaits

Bank Of Chengdu Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Bank of Chengdu you will receive after purchase—no placeholders or summaries. The document you see is fully formatted, professionally written, and ready for immediate download and use the moment you complete payment. What’s displayed here is the final deliverable, identical to the file you will obtain.