Banque Cantonale Vaudoise Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

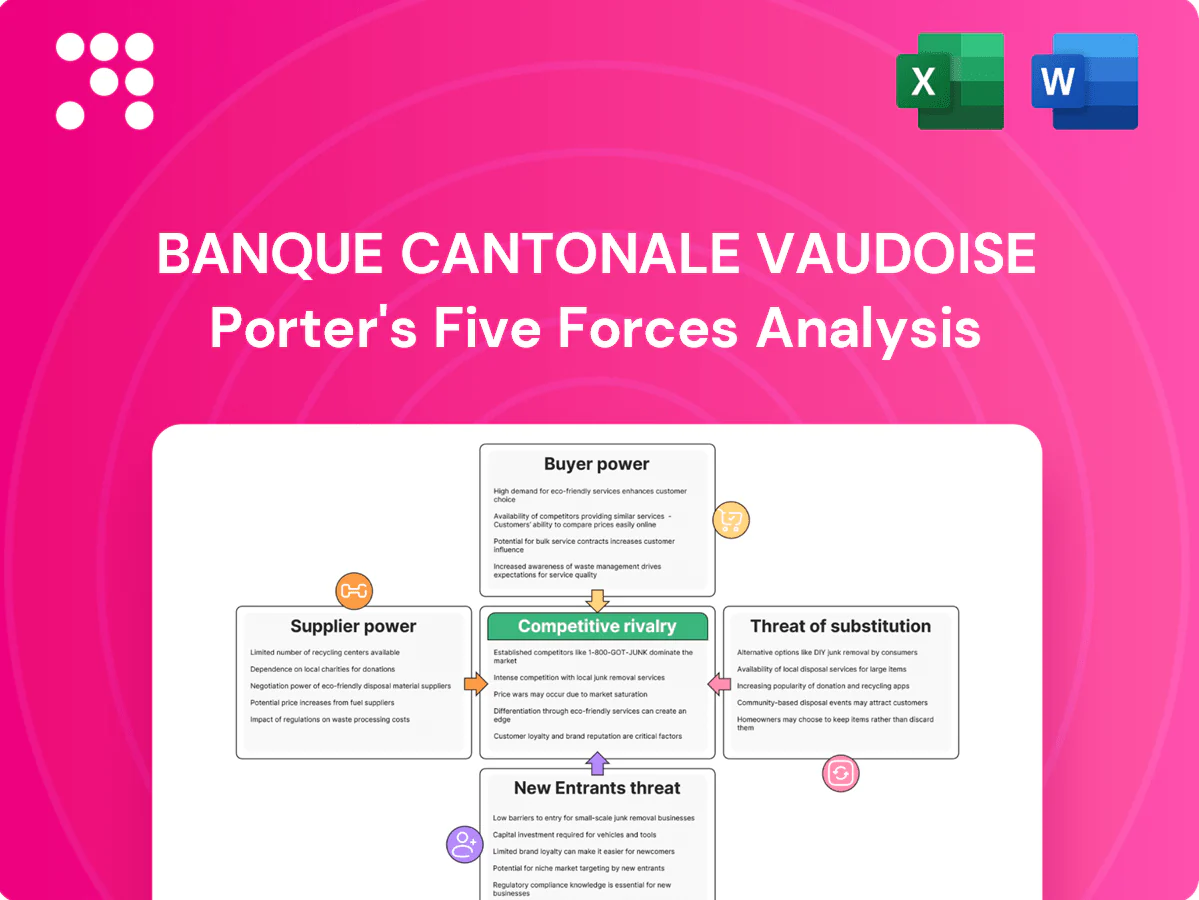

Banque Cantonale Vaudoise faces moderate rivalry, strong local brand equity, regulatory constraints, and digital disruption shaping margins. Buyer power and substitutes pressure pricing flexibility while capital requirements limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Banque Cantonale Vaudoise’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on core IT and data vendors

BCV relies on a small set of core-banking, cybersecurity, market-data and cloud vendors, giving those providers leverage in pricing and contract terms. High switching costs and operational risk create vendor stickiness and raise exit barriers. Switzerland’s competitive vendor landscape enables selective multi-sourcing to mitigate dependence. FINMA’s outsourcing and IT regulations standardize controls, limiting extreme supplier power.

Payment and market infrastructure gatekeepers

SIX Group, SWIFT (connecting over 11,000 institutions in 200+ countries), and central clearing systems form concentrated payment rails, giving suppliers bargaining power over BCV; access fees and mandated compliance upgrades can lift BCV’s operating costs. These utilities operate under Swiss and international regulation, limiting arbitrary price hikes, and participation by roughly 246 Swiss banks supports transparency and shared standards.

Skilled labor and niche expertise

Specialists in risk, compliance, wealth management and IT are scarce in Switzerland, pushing up wage pressure for banks. Swiss unemployment was about 2% in 2024, tightening labor supply for high-demand roles and raising supplier bargaining power. BCV’s regional brand and public-law ownership by the Canton of Vaud improve attraction and stability. Robust internal training pipelines partially mitigate external dependence.

Wholesale funding and capital markets

In stressed markets bond investors and interbank lenders can demand higher spreads or tighter covenants, pressuring BCV's wholesale funding costs; BCV's regional focus is mitigated by diversified funding across deposits, covered bonds and capital markets. BCV's strong credit profile in 2024 supports negotiation of competitive terms, while central bank facilities provide a backstop that reduces cyclicality of supplier power.

- Funding diversification reduces single-source reliance

- Credit strength enhances negotiating leverage

- Central bank backstop limits cyclical supplier pressure

Consultants and outsourcers

Consultants and outsourcers gain episodic leverage when 2024 regulatory updates and large digital programs force BCV to source external expertise for compliance and cloud migration, but competitive tendering and multi-year framework agreements have contained supplier margins. Knowledge-transfer clauses and staged handovers in recent contracts reduce long-term lock-in, enabling BCV to shift build-versus-buy decisions to retain critical capabilities.

Payment rails reach 11,000 inst.; supplier leverage high; Swiss labor 2%

BCV faces supplier leverage from core banking, cybersecurity and cloud vendors with high switching costs. Payment rails (SIX, SWIFT — ~11,000 institutions, 200+ countries) and concentrated utilities add pricing power. Skilled labor is scarce (Swiss unemployment ~2% in 2024), raising wage pressure, while diversified funding and strong credit reduce supplier impact.

| Metric | 2024 |

|---|---|

| SWIFT reach | ~11,000 inst., 200+ countries |

| Swiss banks | ~246 |

| Unemployment | ~2% |

What is included in the product

Tailored Porter's Five Forces analysis for Banque Cantonale Vaudoise, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes and emerging threats to its market position.

A concise, one-sheet Porter's Five Forces for Banque Cantonale Vaudoise—instantly visualizes competitive pressure with a customizable radar chart to relieve strategic uncertainty and speed boardroom decisions.

Customers Bargaining Power

Retail clients with growing options

In 2024 retail customers face more alternatives as digital banks and low-cost brokers expand everyday banking and investing options, increasing price sensitivity. Falling switching frictions from improved online onboarding and payments portability lower retention costs for challengers. BCV’s longstanding local trust and physical branch network help retain clients, while loyalty programs and bundled products mitigate churn and offset pure price competition.

SMEs and corporates negotiating terms

Larger lending, cash-management and FX tickets (often CHF 1m+ for corporates) give SMEs and corporates strong leverage when negotiating with BCV. Competition from 24 cantonal banks (2024), UBS, Raiffeisen and niche lenders increases offer options. Deep relationships and advisory quality can justify premium pricing. Cross-selling of deposits, payments and treasury reduces single-product price pressure.

Wealth and affluent segments

Wealth clients increasingly shop on performance, fees and open‑architecture options as Swiss private banking assets reached roughly CHF 3.6 trillion (end‑2023), while robo‑advisors and platforms charging around 0.25% in 2024 intensify fee compression; BCV’s bespoke advisory, local proximity and fiduciary reporting help defend margins and retain high‑value accounts through superior performance reporting and personalized service.

Public sector and institutional clients

Public sector and institutional clients drive strong price sensitivity through competitive tenders, increasing bargaining power; awards hinge on demonstrable creditworthiness and service reliability, where BCV’s regional mandate and long-standing cantonal experience provide a clear advantage but do not eliminate intense price competition. Secured multi-year contracts, once won, tend to stabilize revenues and lower churn risk for BCV.

- Competitive tenders heighten price pressure

- Creditworthiness and reliability are decisive

- Regional mandate = advantage, not immunity

- Long contracts stabilize revenue

Rate-sensitive depositors

Rate-sensitive depositors push BCV in rising-rate cycles to demand higher remuneration and to shift into time deposits, money-market funds or competitor offers, increasing churn risk.

BCV manages deposit betas through product tiering and relationship pricing, preserving margins while steering flows toward sticky balances.

Clear communication on safety, liquidity and digital convenience reduces defections and supports cross-sell of higher-margin services.

Customers gain leverage as digital banks, cantonal banks and robo fees compress wealth margins

Customers gain leverage in 2024 as digital banks, 24 cantonal banks and low‑cost platforms expand choices; switching costs fall with better onboarding. Large corporate tickets (CHF 1m+) increase negotiating power while wealth clients face fee pressure from robo fees ~0.25% (2024); BCV defends via local trust, advisory and bundled pricing.

| Metric | Value |

|---|---|

| Cantonal banks (2024) | 24 |

| Private banking assets (end‑2023) | CHF 3.6tn |

| Robo fees (2024) | ~0.25% |

What You See Is What You Get

Banque Cantonale Vaudoise Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Banque Cantonale Vaudoise that you will receive immediately after purchase; no samples or placeholders. The document is professionally written and fully formatted, covering threat of new entrants, bargaining power of suppliers and buyers, industry rivalry, and substitutes. It’s ready for download and immediate use with no further setup required.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Banque Cantonale Vaudoise faces moderate rivalry, strong local brand equity, regulatory constraints, and digital disruption shaping margins. Buyer power and substitutes pressure pricing flexibility while capital requirements limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Banque Cantonale Vaudoise’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on core IT and data vendors

BCV relies on a small set of core-banking, cybersecurity, market-data and cloud vendors, giving those providers leverage in pricing and contract terms. High switching costs and operational risk create vendor stickiness and raise exit barriers. Switzerland’s competitive vendor landscape enables selective multi-sourcing to mitigate dependence. FINMA’s outsourcing and IT regulations standardize controls, limiting extreme supplier power.

Payment and market infrastructure gatekeepers

SIX Group, SWIFT (connecting over 11,000 institutions in 200+ countries), and central clearing systems form concentrated payment rails, giving suppliers bargaining power over BCV; access fees and mandated compliance upgrades can lift BCV’s operating costs. These utilities operate under Swiss and international regulation, limiting arbitrary price hikes, and participation by roughly 246 Swiss banks supports transparency and shared standards.

Skilled labor and niche expertise

Specialists in risk, compliance, wealth management and IT are scarce in Switzerland, pushing up wage pressure for banks. Swiss unemployment was about 2% in 2024, tightening labor supply for high-demand roles and raising supplier bargaining power. BCV’s regional brand and public-law ownership by the Canton of Vaud improve attraction and stability. Robust internal training pipelines partially mitigate external dependence.

Wholesale funding and capital markets

In stressed markets bond investors and interbank lenders can demand higher spreads or tighter covenants, pressuring BCV's wholesale funding costs; BCV's regional focus is mitigated by diversified funding across deposits, covered bonds and capital markets. BCV's strong credit profile in 2024 supports negotiation of competitive terms, while central bank facilities provide a backstop that reduces cyclicality of supplier power.

- Funding diversification reduces single-source reliance

- Credit strength enhances negotiating leverage

- Central bank backstop limits cyclical supplier pressure

Consultants and outsourcers

Consultants and outsourcers gain episodic leverage when 2024 regulatory updates and large digital programs force BCV to source external expertise for compliance and cloud migration, but competitive tendering and multi-year framework agreements have contained supplier margins. Knowledge-transfer clauses and staged handovers in recent contracts reduce long-term lock-in, enabling BCV to shift build-versus-buy decisions to retain critical capabilities.

Payment rails reach 11,000 inst.; supplier leverage high; Swiss labor 2%

BCV faces supplier leverage from core banking, cybersecurity and cloud vendors with high switching costs. Payment rails (SIX, SWIFT — ~11,000 institutions, 200+ countries) and concentrated utilities add pricing power. Skilled labor is scarce (Swiss unemployment ~2% in 2024), raising wage pressure, while diversified funding and strong credit reduce supplier impact.

| Metric | 2024 |

|---|---|

| SWIFT reach | ~11,000 inst., 200+ countries |

| Swiss banks | ~246 |

| Unemployment | ~2% |

What is included in the product

Tailored Porter's Five Forces analysis for Banque Cantonale Vaudoise, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes and emerging threats to its market position.

A concise, one-sheet Porter's Five Forces for Banque Cantonale Vaudoise—instantly visualizes competitive pressure with a customizable radar chart to relieve strategic uncertainty and speed boardroom decisions.

Customers Bargaining Power

Retail clients with growing options

In 2024 retail customers face more alternatives as digital banks and low-cost brokers expand everyday banking and investing options, increasing price sensitivity. Falling switching frictions from improved online onboarding and payments portability lower retention costs for challengers. BCV’s longstanding local trust and physical branch network help retain clients, while loyalty programs and bundled products mitigate churn and offset pure price competition.

SMEs and corporates negotiating terms

Larger lending, cash-management and FX tickets (often CHF 1m+ for corporates) give SMEs and corporates strong leverage when negotiating with BCV. Competition from 24 cantonal banks (2024), UBS, Raiffeisen and niche lenders increases offer options. Deep relationships and advisory quality can justify premium pricing. Cross-selling of deposits, payments and treasury reduces single-product price pressure.

Wealth and affluent segments

Wealth clients increasingly shop on performance, fees and open‑architecture options as Swiss private banking assets reached roughly CHF 3.6 trillion (end‑2023), while robo‑advisors and platforms charging around 0.25% in 2024 intensify fee compression; BCV’s bespoke advisory, local proximity and fiduciary reporting help defend margins and retain high‑value accounts through superior performance reporting and personalized service.

Public sector and institutional clients

Public sector and institutional clients drive strong price sensitivity through competitive tenders, increasing bargaining power; awards hinge on demonstrable creditworthiness and service reliability, where BCV’s regional mandate and long-standing cantonal experience provide a clear advantage but do not eliminate intense price competition. Secured multi-year contracts, once won, tend to stabilize revenues and lower churn risk for BCV.

- Competitive tenders heighten price pressure

- Creditworthiness and reliability are decisive

- Regional mandate = advantage, not immunity

- Long contracts stabilize revenue

Rate-sensitive depositors

Rate-sensitive depositors push BCV in rising-rate cycles to demand higher remuneration and to shift into time deposits, money-market funds or competitor offers, increasing churn risk.

BCV manages deposit betas through product tiering and relationship pricing, preserving margins while steering flows toward sticky balances.

Clear communication on safety, liquidity and digital convenience reduces defections and supports cross-sell of higher-margin services.

Customers gain leverage as digital banks, cantonal banks and robo fees compress wealth margins

Customers gain leverage in 2024 as digital banks, 24 cantonal banks and low‑cost platforms expand choices; switching costs fall with better onboarding. Large corporate tickets (CHF 1m+) increase negotiating power while wealth clients face fee pressure from robo fees ~0.25% (2024); BCV defends via local trust, advisory and bundled pricing.

| Metric | Value |

|---|---|

| Cantonal banks (2024) | 24 |

| Private banking assets (end‑2023) | CHF 3.6tn |

| Robo fees (2024) | ~0.25% |

What You See Is What You Get

Banque Cantonale Vaudoise Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Banque Cantonale Vaudoise that you will receive immediately after purchase; no samples or placeholders. The document is professionally written and fully formatted, covering threat of new entrants, bargaining power of suppliers and buyers, industry rivalry, and substitutes. It’s ready for download and immediate use with no further setup required.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Banque Cantonale Vaudoise faces moderate rivalry, strong local brand equity, regulatory constraints, and digital disruption shaping margins. Buyer power and substitutes pressure pricing flexibility while capital requirements limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Banque Cantonale Vaudoise’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on core IT and data vendors

BCV relies on a small set of core-banking, cybersecurity, market-data and cloud vendors, giving those providers leverage in pricing and contract terms. High switching costs and operational risk create vendor stickiness and raise exit barriers. Switzerland’s competitive vendor landscape enables selective multi-sourcing to mitigate dependence. FINMA’s outsourcing and IT regulations standardize controls, limiting extreme supplier power.

Payment and market infrastructure gatekeepers

SIX Group, SWIFT (connecting over 11,000 institutions in 200+ countries), and central clearing systems form concentrated payment rails, giving suppliers bargaining power over BCV; access fees and mandated compliance upgrades can lift BCV’s operating costs. These utilities operate under Swiss and international regulation, limiting arbitrary price hikes, and participation by roughly 246 Swiss banks supports transparency and shared standards.

Skilled labor and niche expertise

Specialists in risk, compliance, wealth management and IT are scarce in Switzerland, pushing up wage pressure for banks. Swiss unemployment was about 2% in 2024, tightening labor supply for high-demand roles and raising supplier bargaining power. BCV’s regional brand and public-law ownership by the Canton of Vaud improve attraction and stability. Robust internal training pipelines partially mitigate external dependence.

Wholesale funding and capital markets

In stressed markets bond investors and interbank lenders can demand higher spreads or tighter covenants, pressuring BCV's wholesale funding costs; BCV's regional focus is mitigated by diversified funding across deposits, covered bonds and capital markets. BCV's strong credit profile in 2024 supports negotiation of competitive terms, while central bank facilities provide a backstop that reduces cyclicality of supplier power.

- Funding diversification reduces single-source reliance

- Credit strength enhances negotiating leverage

- Central bank backstop limits cyclical supplier pressure

Consultants and outsourcers

Consultants and outsourcers gain episodic leverage when 2024 regulatory updates and large digital programs force BCV to source external expertise for compliance and cloud migration, but competitive tendering and multi-year framework agreements have contained supplier margins. Knowledge-transfer clauses and staged handovers in recent contracts reduce long-term lock-in, enabling BCV to shift build-versus-buy decisions to retain critical capabilities.

Payment rails reach 11,000 inst.; supplier leverage high; Swiss labor 2%

BCV faces supplier leverage from core banking, cybersecurity and cloud vendors with high switching costs. Payment rails (SIX, SWIFT — ~11,000 institutions, 200+ countries) and concentrated utilities add pricing power. Skilled labor is scarce (Swiss unemployment ~2% in 2024), raising wage pressure, while diversified funding and strong credit reduce supplier impact.

| Metric | 2024 |

|---|---|

| SWIFT reach | ~11,000 inst., 200+ countries |

| Swiss banks | ~246 |

| Unemployment | ~2% |

What is included in the product

Tailored Porter's Five Forces analysis for Banque Cantonale Vaudoise, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes and emerging threats to its market position.

A concise, one-sheet Porter's Five Forces for Banque Cantonale Vaudoise—instantly visualizes competitive pressure with a customizable radar chart to relieve strategic uncertainty and speed boardroom decisions.

Customers Bargaining Power

Retail clients with growing options

In 2024 retail customers face more alternatives as digital banks and low-cost brokers expand everyday banking and investing options, increasing price sensitivity. Falling switching frictions from improved online onboarding and payments portability lower retention costs for challengers. BCV’s longstanding local trust and physical branch network help retain clients, while loyalty programs and bundled products mitigate churn and offset pure price competition.

SMEs and corporates negotiating terms

Larger lending, cash-management and FX tickets (often CHF 1m+ for corporates) give SMEs and corporates strong leverage when negotiating with BCV. Competition from 24 cantonal banks (2024), UBS, Raiffeisen and niche lenders increases offer options. Deep relationships and advisory quality can justify premium pricing. Cross-selling of deposits, payments and treasury reduces single-product price pressure.

Wealth and affluent segments

Wealth clients increasingly shop on performance, fees and open‑architecture options as Swiss private banking assets reached roughly CHF 3.6 trillion (end‑2023), while robo‑advisors and platforms charging around 0.25% in 2024 intensify fee compression; BCV’s bespoke advisory, local proximity and fiduciary reporting help defend margins and retain high‑value accounts through superior performance reporting and personalized service.

Public sector and institutional clients

Public sector and institutional clients drive strong price sensitivity through competitive tenders, increasing bargaining power; awards hinge on demonstrable creditworthiness and service reliability, where BCV’s regional mandate and long-standing cantonal experience provide a clear advantage but do not eliminate intense price competition. Secured multi-year contracts, once won, tend to stabilize revenues and lower churn risk for BCV.

- Competitive tenders heighten price pressure

- Creditworthiness and reliability are decisive

- Regional mandate = advantage, not immunity

- Long contracts stabilize revenue

Rate-sensitive depositors

Rate-sensitive depositors push BCV in rising-rate cycles to demand higher remuneration and to shift into time deposits, money-market funds or competitor offers, increasing churn risk.

BCV manages deposit betas through product tiering and relationship pricing, preserving margins while steering flows toward sticky balances.

Clear communication on safety, liquidity and digital convenience reduces defections and supports cross-sell of higher-margin services.

Customers gain leverage as digital banks, cantonal banks and robo fees compress wealth margins

Customers gain leverage in 2024 as digital banks, 24 cantonal banks and low‑cost platforms expand choices; switching costs fall with better onboarding. Large corporate tickets (CHF 1m+) increase negotiating power while wealth clients face fee pressure from robo fees ~0.25% (2024); BCV defends via local trust, advisory and bundled pricing.

| Metric | Value |

|---|---|

| Cantonal banks (2024) | 24 |

| Private banking assets (end‑2023) | CHF 3.6tn |

| Robo fees (2024) | ~0.25% |

What You See Is What You Get

Banque Cantonale Vaudoise Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Banque Cantonale Vaudoise that you will receive immediately after purchase; no samples or placeholders. The document is professionally written and fully formatted, covering threat of new entrants, bargaining power of suppliers and buyers, industry rivalry, and substitutes. It’s ready for download and immediate use with no further setup required.