BDO Unibank Boston Consulting Group Matrix

Actionable Strategy Starts Here

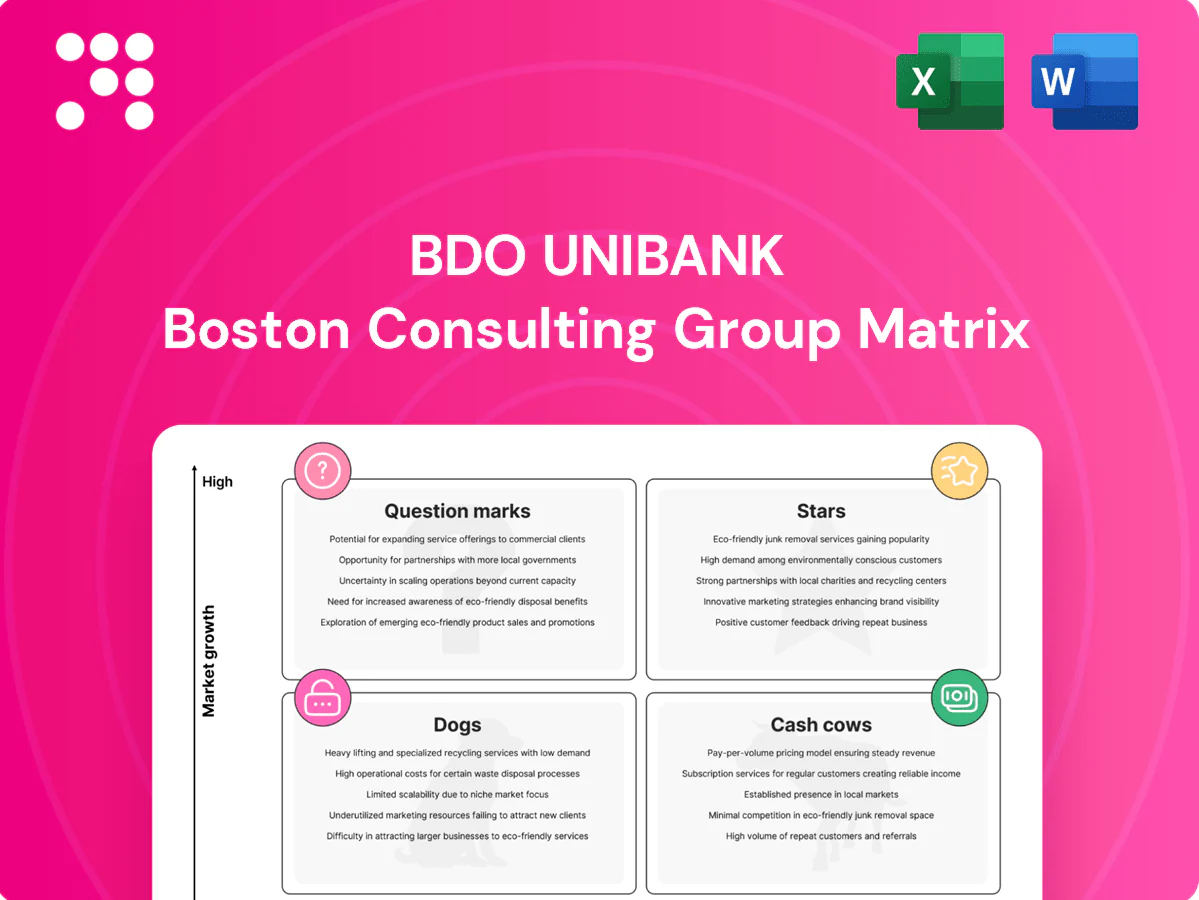

Want to see exactly where BDO Unibank’s products sit — Stars, Cash Cows, Dogs, or Question Marks — and why it matters for your capital and product bets? Grab the full BCG Matrix for quadrant-by-quadrant placement, crisp strategic moves, and data-backed recommendations you can act on right away. Purchase now and get a ready-to-use Word report plus an Excel summary — skip the guesswork and start shaping smarter investment decisions today.

Stars

Digital banking & mobile app

BDO Mobile continues strong user growth as Filipinos shift banking to phones, with BDO remaining the Philippines largest bank by assets in 2024. Usage, login frequency and digital transactions have climbed sharply amid nationwide digital adoption, helping BDO keep high share while the market expands. BDO’s brand and cross‑sell muscle sustain retention; ongoing investment in UX, security and embedded services is needed to defend leadership.

Retail deposits & CASA franchise

BDO’s massive low‑cost deposit base underpins its CASA‑heavy retail franchise as the Philippines’ largest bank by assets; its dense network of over 1,400 branches and strong brand keep share high amid ongoing financial inclusion. The retail market continues growing as customers go cash‑lite, supported by digital funnels and healthy deposit growth in 2024. Fund the flywheel with analytics, product bundles, and rewards to lock in primacy.

Remittances & overseas Filipino channels

OFW remittance flows remained resilient in 2024, with Philippine inward remittances exceeding $40 billion as digital corridors expanded; BDO’s extensive branch and partner network keeps volumes high while online channels grow rapidly. High market share plus rising digital penetration fits a classic Star profile. Recommend doubling down on instant crediting, FX convenience, and fee‑transparent pricing to capture further digital share.

Consumer lending (auto, personal)

In BCG matrix BDO's consumer lending (auto, personal) sits in Stars as consumer credit penetration in the Philippines is climbing from a low base—household debt remains around 20% of GDP (2023–24), well below regional peers. BDO leverages the Philippines' largest branch network and proven risk models to hold share as demand rises. To scale safely it needs targeted marketing and underwriting investment. Build pre‑approved offers and ecosystem partnerships to stay ahead.

- Household debt ~20% of GDP (2023–24)

- BDO: market-leading distribution and risk capabilities

- Priorities: marketing + underwriting spend, pre-approved offers, ecosystem partnerships

Credit cards & payments acquiring

Card spend and merchant acceptance are expanding as the Philippine economy formalizes; BDO leverages scale, co‑brands and nationwide merchant reach to hold a leading acquiring position while reporting assets of about PHP 4.7 trillion in 2024. Rapid acquiring growth drives higher rewards and capex burn, but the business is strategically positioned to convert scale into durable margins. Maintaining promos, strict risk controls and enhanced merchant solutions should shift the unit toward cash‑cow economics.

- Market position: leading acquirer with nationwide merchant footprint (BDO assets ~PHP 4.7T, 2024)

- Growth tradeoff: high customer acquisition and rewards compress near‑term cash flow

- Strategy: sustain promos, tighten risk, expand merchant value‑added services to boost take‑rates

Digital banking & remittances fuel scale; prioritize underwriting, UX, instant FX, merchant VAS

BDO’s digital banking, consumer lending and merchant acquiring classify as Stars—BDO assets ~PHP4.7T (2024) with mobile users and digital transactions rising sharply.

OFW remittances >$40B (2024) and household debt ~20% of GDP (2023–24) underpin healthy loan growth and card spend expansion.

Priorities: scale underwriting, UX/security, instant FX/credit, and merchant VAS to convert Stars into durable profits.

| Segment | 2024 metric | Implication |

|---|---|---|

| Assets | PHP4.7T | Scale advantage |

| Remittances | $40B+ | Transaction volume |

| Household debt | ~20% GDP | Loan room |

What is included in the product

Comprehensive BCG Matrix review of BDO Unibank's units, with strategic moves—invest, hold or divest—per quadrant and trend context.

One-page BDO Unibank BCG Matrix placing each unit in a quadrant, export-ready for C-level decks and A4 prints.

Cash Cows

Corporate lending & cash management

BDO, the Philippines largest bank by assets in 2024, treats large‑corporate lending and cash management as a mature, high‑share franchise with entrenched wallet share and low churn.

Margins are steady and cross‑sell is rich, generating consistent cash with only modest growth needs; returns are cash‑cow stable rather than high‑growth.

Priority: invest in efficiency programs and API-driven platforms to reduce operating cost per client and deepen stickiness across treasury and cash management services.

Treasury & trading services

Treasury & trading services generate dependable flows from FX, fixed income and balance‑sheet management, sustaining strong fee income and surplus cash; BDO remains the Philippines largest bank by assets, anchoring market share. Market growth is modest, so sharpening pricing, automation and risk‑based trading can widen spreads and lift returns without heavy capital spend.

Transaction services & fees

Transaction services and fees—payments, bills pay, and service charges—remain BDO Unibank cash cows in 2024, delivering predictable, recurring income across mature corridors. Usage growth is slow but the customer base is large, supporting steady fee capture. Strong operating leverage means incremental volumes translate to outsized profit contribution. Continued process tightening and expanded self‑service channels will improve margins further.

Trust & wealth management (core affluent)

BDO’s trust and wealth management for core affluent delivers steady AUM growth without volatility, leveraging BDO’s position as the Philippines’ largest bank by assets and a sizable advisor book that generates recurring advisory and custody fees with low incremental cost.

- Stable fee income

- Low marginal cost

- Upsell via advisory tools

- Product shelf to lift yields

Branch & ATM network monetization

Physical reach remains a moat even as branch growth moderates; as of 2024 BDO operated c.1,400 branches and over 4,000 ATMs, anchoring fee income and deep customer relationships. Fee income from the footprint provides reliable non‑interest revenue while operating costs fall as transactions migrate digital. Rationalize low‑performing locations, intensify branch sales, and keep ATMs efficient.

- Branch scale: c.1,400 branches, >4,000 ATMs (2024)

- Revenue: steady fee income from transactions and relationships

- Actions: rationalize, push sales, optimize ATM operations

Lending, treasury, fees & wealth: cash cows across c.1,400 branches & >4,000 ATMs

BDO’s large‑corporate lending, treasury, transaction fees and wealth are cash cows in 2024: mature, high‑share franchises with steady margins and low capex needs. Strong operating leverage across c.1,400 branches and >4,000 ATMs sustains recurring fee income; focus on automation, pricing and efficiency to lift returns.

| Metric | 2024 |

|---|---|

| Branches | c.1,400 |

| ATMs | >4,000 |

| Strategic focus | Efficiency, API, pricing |

What You’re Viewing Is Included

BDO Unibank BCG Matrix

The file you're previewing is the exact BDO Unibank BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just a polished, ready-to-use strategic report. It arrives fully editable and formatted for presentation or printing. Buy once and download immediately—what you see is what you get.

Actionable Strategy Starts Here

Want to see exactly where BDO Unibank’s products sit — Stars, Cash Cows, Dogs, or Question Marks — and why it matters for your capital and product bets? Grab the full BCG Matrix for quadrant-by-quadrant placement, crisp strategic moves, and data-backed recommendations you can act on right away. Purchase now and get a ready-to-use Word report plus an Excel summary — skip the guesswork and start shaping smarter investment decisions today.

Stars

Digital banking & mobile app

BDO Mobile continues strong user growth as Filipinos shift banking to phones, with BDO remaining the Philippines largest bank by assets in 2024. Usage, login frequency and digital transactions have climbed sharply amid nationwide digital adoption, helping BDO keep high share while the market expands. BDO’s brand and cross‑sell muscle sustain retention; ongoing investment in UX, security and embedded services is needed to defend leadership.

Retail deposits & CASA franchise

BDO’s massive low‑cost deposit base underpins its CASA‑heavy retail franchise as the Philippines’ largest bank by assets; its dense network of over 1,400 branches and strong brand keep share high amid ongoing financial inclusion. The retail market continues growing as customers go cash‑lite, supported by digital funnels and healthy deposit growth in 2024. Fund the flywheel with analytics, product bundles, and rewards to lock in primacy.

Remittances & overseas Filipino channels

OFW remittance flows remained resilient in 2024, with Philippine inward remittances exceeding $40 billion as digital corridors expanded; BDO’s extensive branch and partner network keeps volumes high while online channels grow rapidly. High market share plus rising digital penetration fits a classic Star profile. Recommend doubling down on instant crediting, FX convenience, and fee‑transparent pricing to capture further digital share.

Consumer lending (auto, personal)

In BCG matrix BDO's consumer lending (auto, personal) sits in Stars as consumer credit penetration in the Philippines is climbing from a low base—household debt remains around 20% of GDP (2023–24), well below regional peers. BDO leverages the Philippines' largest branch network and proven risk models to hold share as demand rises. To scale safely it needs targeted marketing and underwriting investment. Build pre‑approved offers and ecosystem partnerships to stay ahead.

- Household debt ~20% of GDP (2023–24)

- BDO: market-leading distribution and risk capabilities

- Priorities: marketing + underwriting spend, pre-approved offers, ecosystem partnerships

Credit cards & payments acquiring

Card spend and merchant acceptance are expanding as the Philippine economy formalizes; BDO leverages scale, co‑brands and nationwide merchant reach to hold a leading acquiring position while reporting assets of about PHP 4.7 trillion in 2024. Rapid acquiring growth drives higher rewards and capex burn, but the business is strategically positioned to convert scale into durable margins. Maintaining promos, strict risk controls and enhanced merchant solutions should shift the unit toward cash‑cow economics.

- Market position: leading acquirer with nationwide merchant footprint (BDO assets ~PHP 4.7T, 2024)

- Growth tradeoff: high customer acquisition and rewards compress near‑term cash flow

- Strategy: sustain promos, tighten risk, expand merchant value‑added services to boost take‑rates

Digital banking & remittances fuel scale; prioritize underwriting, UX, instant FX, merchant VAS

BDO’s digital banking, consumer lending and merchant acquiring classify as Stars—BDO assets ~PHP4.7T (2024) with mobile users and digital transactions rising sharply.

OFW remittances >$40B (2024) and household debt ~20% of GDP (2023–24) underpin healthy loan growth and card spend expansion.

Priorities: scale underwriting, UX/security, instant FX/credit, and merchant VAS to convert Stars into durable profits.

| Segment | 2024 metric | Implication |

|---|---|---|

| Assets | PHP4.7T | Scale advantage |

| Remittances | $40B+ | Transaction volume |

| Household debt | ~20% GDP | Loan room |

What is included in the product

Comprehensive BCG Matrix review of BDO Unibank's units, with strategic moves—invest, hold or divest—per quadrant and trend context.

One-page BDO Unibank BCG Matrix placing each unit in a quadrant, export-ready for C-level decks and A4 prints.

Cash Cows

Corporate lending & cash management

BDO, the Philippines largest bank by assets in 2024, treats large‑corporate lending and cash management as a mature, high‑share franchise with entrenched wallet share and low churn.

Margins are steady and cross‑sell is rich, generating consistent cash with only modest growth needs; returns are cash‑cow stable rather than high‑growth.

Priority: invest in efficiency programs and API-driven platforms to reduce operating cost per client and deepen stickiness across treasury and cash management services.

Treasury & trading services

Treasury & trading services generate dependable flows from FX, fixed income and balance‑sheet management, sustaining strong fee income and surplus cash; BDO remains the Philippines largest bank by assets, anchoring market share. Market growth is modest, so sharpening pricing, automation and risk‑based trading can widen spreads and lift returns without heavy capital spend.

Transaction services & fees

Transaction services and fees—payments, bills pay, and service charges—remain BDO Unibank cash cows in 2024, delivering predictable, recurring income across mature corridors. Usage growth is slow but the customer base is large, supporting steady fee capture. Strong operating leverage means incremental volumes translate to outsized profit contribution. Continued process tightening and expanded self‑service channels will improve margins further.

Trust & wealth management (core affluent)

BDO’s trust and wealth management for core affluent delivers steady AUM growth without volatility, leveraging BDO’s position as the Philippines’ largest bank by assets and a sizable advisor book that generates recurring advisory and custody fees with low incremental cost.

- Stable fee income

- Low marginal cost

- Upsell via advisory tools

- Product shelf to lift yields

Branch & ATM network monetization

Physical reach remains a moat even as branch growth moderates; as of 2024 BDO operated c.1,400 branches and over 4,000 ATMs, anchoring fee income and deep customer relationships. Fee income from the footprint provides reliable non‑interest revenue while operating costs fall as transactions migrate digital. Rationalize low‑performing locations, intensify branch sales, and keep ATMs efficient.

- Branch scale: c.1,400 branches, >4,000 ATMs (2024)

- Revenue: steady fee income from transactions and relationships

- Actions: rationalize, push sales, optimize ATM operations

Lending, treasury, fees & wealth: cash cows across c.1,400 branches & >4,000 ATMs

BDO’s large‑corporate lending, treasury, transaction fees and wealth are cash cows in 2024: mature, high‑share franchises with steady margins and low capex needs. Strong operating leverage across c.1,400 branches and >4,000 ATMs sustains recurring fee income; focus on automation, pricing and efficiency to lift returns.

| Metric | 2024 |

|---|---|

| Branches | c.1,400 |

| ATMs | >4,000 |

| Strategic focus | Efficiency, API, pricing |

What You’re Viewing Is Included

BDO Unibank BCG Matrix

The file you're previewing is the exact BDO Unibank BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just a polished, ready-to-use strategic report. It arrives fully editable and formatted for presentation or printing. Buy once and download immediately—what you see is what you get.

Description

Actionable Strategy Starts Here

Want to see exactly where BDO Unibank’s products sit — Stars, Cash Cows, Dogs, or Question Marks — and why it matters for your capital and product bets? Grab the full BCG Matrix for quadrant-by-quadrant placement, crisp strategic moves, and data-backed recommendations you can act on right away. Purchase now and get a ready-to-use Word report plus an Excel summary — skip the guesswork and start shaping smarter investment decisions today.

Stars

Digital banking & mobile app

BDO Mobile continues strong user growth as Filipinos shift banking to phones, with BDO remaining the Philippines largest bank by assets in 2024. Usage, login frequency and digital transactions have climbed sharply amid nationwide digital adoption, helping BDO keep high share while the market expands. BDO’s brand and cross‑sell muscle sustain retention; ongoing investment in UX, security and embedded services is needed to defend leadership.

Retail deposits & CASA franchise

BDO’s massive low‑cost deposit base underpins its CASA‑heavy retail franchise as the Philippines’ largest bank by assets; its dense network of over 1,400 branches and strong brand keep share high amid ongoing financial inclusion. The retail market continues growing as customers go cash‑lite, supported by digital funnels and healthy deposit growth in 2024. Fund the flywheel with analytics, product bundles, and rewards to lock in primacy.

Remittances & overseas Filipino channels

OFW remittance flows remained resilient in 2024, with Philippine inward remittances exceeding $40 billion as digital corridors expanded; BDO’s extensive branch and partner network keeps volumes high while online channels grow rapidly. High market share plus rising digital penetration fits a classic Star profile. Recommend doubling down on instant crediting, FX convenience, and fee‑transparent pricing to capture further digital share.

Consumer lending (auto, personal)

In BCG matrix BDO's consumer lending (auto, personal) sits in Stars as consumer credit penetration in the Philippines is climbing from a low base—household debt remains around 20% of GDP (2023–24), well below regional peers. BDO leverages the Philippines' largest branch network and proven risk models to hold share as demand rises. To scale safely it needs targeted marketing and underwriting investment. Build pre‑approved offers and ecosystem partnerships to stay ahead.

- Household debt ~20% of GDP (2023–24)

- BDO: market-leading distribution and risk capabilities

- Priorities: marketing + underwriting spend, pre-approved offers, ecosystem partnerships

Credit cards & payments acquiring

Card spend and merchant acceptance are expanding as the Philippine economy formalizes; BDO leverages scale, co‑brands and nationwide merchant reach to hold a leading acquiring position while reporting assets of about PHP 4.7 trillion in 2024. Rapid acquiring growth drives higher rewards and capex burn, but the business is strategically positioned to convert scale into durable margins. Maintaining promos, strict risk controls and enhanced merchant solutions should shift the unit toward cash‑cow economics.

- Market position: leading acquirer with nationwide merchant footprint (BDO assets ~PHP 4.7T, 2024)

- Growth tradeoff: high customer acquisition and rewards compress near‑term cash flow

- Strategy: sustain promos, tighten risk, expand merchant value‑added services to boost take‑rates

Digital banking & remittances fuel scale; prioritize underwriting, UX, instant FX, merchant VAS

BDO’s digital banking, consumer lending and merchant acquiring classify as Stars—BDO assets ~PHP4.7T (2024) with mobile users and digital transactions rising sharply.

OFW remittances >$40B (2024) and household debt ~20% of GDP (2023–24) underpin healthy loan growth and card spend expansion.

Priorities: scale underwriting, UX/security, instant FX/credit, and merchant VAS to convert Stars into durable profits.

| Segment | 2024 metric | Implication |

|---|---|---|

| Assets | PHP4.7T | Scale advantage |

| Remittances | $40B+ | Transaction volume |

| Household debt | ~20% GDP | Loan room |

What is included in the product

Comprehensive BCG Matrix review of BDO Unibank's units, with strategic moves—invest, hold or divest—per quadrant and trend context.

One-page BDO Unibank BCG Matrix placing each unit in a quadrant, export-ready for C-level decks and A4 prints.

Cash Cows

Corporate lending & cash management

BDO, the Philippines largest bank by assets in 2024, treats large‑corporate lending and cash management as a mature, high‑share franchise with entrenched wallet share and low churn.

Margins are steady and cross‑sell is rich, generating consistent cash with only modest growth needs; returns are cash‑cow stable rather than high‑growth.

Priority: invest in efficiency programs and API-driven platforms to reduce operating cost per client and deepen stickiness across treasury and cash management services.

Treasury & trading services

Treasury & trading services generate dependable flows from FX, fixed income and balance‑sheet management, sustaining strong fee income and surplus cash; BDO remains the Philippines largest bank by assets, anchoring market share. Market growth is modest, so sharpening pricing, automation and risk‑based trading can widen spreads and lift returns without heavy capital spend.

Transaction services & fees

Transaction services and fees—payments, bills pay, and service charges—remain BDO Unibank cash cows in 2024, delivering predictable, recurring income across mature corridors. Usage growth is slow but the customer base is large, supporting steady fee capture. Strong operating leverage means incremental volumes translate to outsized profit contribution. Continued process tightening and expanded self‑service channels will improve margins further.

Trust & wealth management (core affluent)

BDO’s trust and wealth management for core affluent delivers steady AUM growth without volatility, leveraging BDO’s position as the Philippines’ largest bank by assets and a sizable advisor book that generates recurring advisory and custody fees with low incremental cost.

- Stable fee income

- Low marginal cost

- Upsell via advisory tools

- Product shelf to lift yields

Branch & ATM network monetization

Physical reach remains a moat even as branch growth moderates; as of 2024 BDO operated c.1,400 branches and over 4,000 ATMs, anchoring fee income and deep customer relationships. Fee income from the footprint provides reliable non‑interest revenue while operating costs fall as transactions migrate digital. Rationalize low‑performing locations, intensify branch sales, and keep ATMs efficient.

- Branch scale: c.1,400 branches, >4,000 ATMs (2024)

- Revenue: steady fee income from transactions and relationships

- Actions: rationalize, push sales, optimize ATM operations

Lending, treasury, fees & wealth: cash cows across c.1,400 branches & >4,000 ATMs

BDO’s large‑corporate lending, treasury, transaction fees and wealth are cash cows in 2024: mature, high‑share franchises with steady margins and low capex needs. Strong operating leverage across c.1,400 branches and >4,000 ATMs sustains recurring fee income; focus on automation, pricing and efficiency to lift returns.

| Metric | 2024 |

|---|---|

| Branches | c.1,400 |

| ATMs | >4,000 |

| Strategic focus | Efficiency, API, pricing |

What You’re Viewing Is Included

BDO Unibank BCG Matrix

The file you're previewing is the exact BDO Unibank BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just a polished, ready-to-use strategic report. It arrives fully editable and formatted for presentation or printing. Buy once and download immediately—what you see is what you get.