Beat Porter's Five Forces Analysis

From Overview to Strategy Blueprint

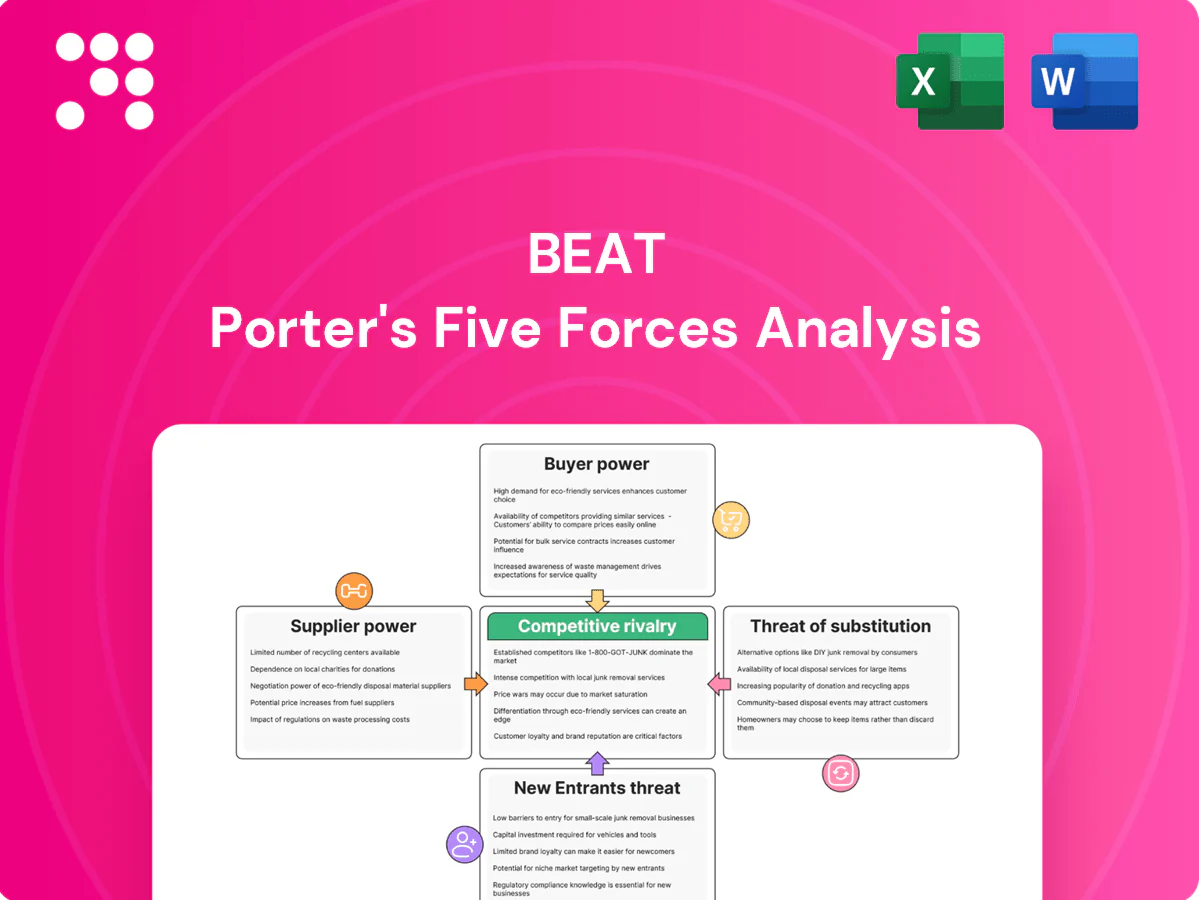

This snapshot highlights Beat’s competitive landscape—buyer and supplier power, threat of entrants and substitutes, and industry rivalry—but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, Excel/Word deliverables, and actionable strategic insights to inform investment or planning decisions.

Suppliers Bargaining Power

Scarce Web3 talent

Specialized blockchain engineers, cryptographers, and token economists remain scarce, with LinkedIn and job aggregators showing over 10,000 global blockchain roles open in 2024, giving talent leverage on pay and terms. Beat risks bidding wars with exchanges, Layer‑1s, and Big Tech, where hiring premiums often reach 20–40% over comparable engineering roles. Hiring delays of 6–12 months can slow product roadmaps and deal due diligence, and long ramp times increase dependence on key individuals.

Cloud & node infrastructure

Reliance on hyperscalers and node/API providers concentrates vendor power: in 2024 AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) together controlled about 66% of global cloud IaaS/PaaS spend, funneling traffic to RPC/indexing/custody vendors. Pricing changes or API throttling can quickly raise operating costs and hurt uptime and margins. Vendor lock-in from proprietary APIs and managed services increases switching costs for deployed services. Integrated compliance features like cloud KMS and HSM further tether critical workloads.

Protocol & tooling ecosystems

Foundations, middleware, and oracle providers set technical roadmaps Beat must follow, with oracle leader Chainlink reporting over 2,000 integrations by 2024, creating lock-in risk. Changes in fee models or deprecation of tools can force costly refactors and higher engineering spend. Access to grants or ecosystem support is selectively allocated, and standards fragmentation—dozens of competing cross-chain standards by 2024—increases coordination costs across chains.

Deal flow gatekeepers

Deal-flow gatekeepers—top VCs, accelerators, and banks controlling proprietary pipelines—can demand favorable co-invest terms, especially as hot rounds compress diligence windows and push higher valuations; VC dry powder exceeded $300B in 2024, concentrating leverage. Preferential allocations often require strategic concessions, and reduced access raises adverse selection risk for outsiders.

Regulatory/compliance vendors

KYC/AML providers, chain-analytics firms and licensing advisors are indispensable in FinTech and digital assets; in 2024 vendor tools underpin onboarding and compliance for over 90% of regulated crypto firms. Their methodologies and jurisdictional coverage directly constrain product scope and market access, and per-seat or price-escalator licensing can erode unit economics. Switching vendors requires recertification, retraining and regulator notifications, often taking months and adding material compliance spend.

- Vendor reliance: >90% of regulated crypto firms (2024)

- Coverage gaps: ~10–15% of jurisdictions affected

- Cost pressure: per-seat/escalators materially reduce margins

- Switching burden: months for recertification and notifications

Suppliers power: pay premiums 20-40%, VC dry powder $300B+

Suppliers hold strong leverage: 10,000+ global blockchain roles in 2024 lift wage premiums 20–40% and extend hiring 6–12 months. Hyperscalers (AWS 32%, Azure 23%, GCP 11%) and Chainlink (2,000+ integrations) create vendor lock‑in; VC dry powder >$300B and >90% reliance on KYC tools amplify gatekeeper power.

| Metric | 2024 |

|---|---|

| Blockchain roles open | 10,000+ |

| AWS/Azure/GCP share | 32%/23%/11% |

| Chainlink integrations | 2,000+ |

| VC dry powder | $300B+ |

What is included in the product

Comprehensive Five Forces analysis of Beat, uncovering competitive rivalry, buyer/supplier power, substitutes, and entry threats with industry data and strategic commentary. Identifies disruptive forces and market dynamics shaping pricing, profitability, and barriers to entry; fully editable Word format for reports and decks.

Beat Porter's Five Forces delivers a one-sheet, customizable summary with pressure sliders, instant spider chart and clean layout—ready for decks, scenario tabs and dashboards; swap your own data and use without macros to relieve analysis bottlenecks for non-finance users.

Customers Bargaining Power

Enterprise concentration

Large APAC conglomerates and financial institutions routinely negotiate 10–20% volume discounts and strict SLAs, with procurement cycles extending sales timelines by 30–90 days and pressuring payment terms; marquee client referenceability boosts buyer leverage, and losing a single major account can cut supplier revenue by 10–40%, per 2024 industry surveys.

Low switching costs in pilots

POCs for blockchain services are modular and reversible, enabling competitors to replicate core features quickly; Gartner forecasted enterprise blockchain spending near $19 billion in 2024, reflecting intense vendor activity that shortens imitation cycles. Buyers often multi-home across providers to benchmark outcomes, increasing price sensitivity and forcing Beat to differentiate on performance, integrations, and measurable ROI rather than price alone.

Deal terms in investments

Startups can choose VC, CVC, or strategic capital and negotiate valuation and protective rights; in 2024 deal structures increasingly included pro-rata and liquidation preference clauses. Hot sectors in 2024 let founders push investor-unfriendly terms as competition for allocations rose. Beat may need to offer strategic value or follow-on certainty to win slots in competitive rounds where investees hold stronger bargaining power.

High information transparency

- Open-source dashboards: public performance metrics (2024)

- Token/deal data: improved price/fee comparison (2024)

- Reduced information rents → stronger buyer negotiation

Demand for credibility

Buyers demand demonstrable credibility: compliance, security certifications and audited code are procurement gating items; in 2024 roughly 71% of enterprise buyers prioritized certifications in vendor selection. Any trust lapse typically triggers re-tendering or churn, forcing Beat to absorb recurring audit and assurance costs and accept strict reporting covenants that can constrain margins.

- Compliance as gate: certifications required

- Churn risk: re-tendering on lapses

- Ongoing cost: continuous audits/assurance

- Covenants: stringent reporting imposed by clients

Buyers squeeze margins: APAC corporates demand 10–20% discounts, extend payments 30–90 days

Buyers wield strong leverage: large APAC corporates secure 10–20% volume discounts and extend procurement 30–90 days, squeezing payment terms and margins. Enterprise blockchain spend reached about $19B in 2024, driving vendor competition and customer multi-homing. Certification/security are gating factors—71% of enterprise buyers prioritized certifications in 2024—while loss of a major account can cut supplier revenue 10–40%.

| Metric | 2024 | Impact |

|---|---|---|

| Volume discounts | 10–20% | Margin pressure |

| Procurement delay | 30–90 days | Sales cycle lengthening |

| Blockchain spend | $19B | Intense vendor competition |

| Certifications | 71% buyers | Procurement gate |

| Major account loss | 10–40% revenue | High concentration risk |

Full Version Awaits

Beat Porter's Five Forces Analysis

This preview shows the exact Beat Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of entry, and substitutes with actionable insights. No placeholders or samples—this is the final deliverable.

From Overview to Strategy Blueprint

This snapshot highlights Beat’s competitive landscape—buyer and supplier power, threat of entrants and substitutes, and industry rivalry—but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, Excel/Word deliverables, and actionable strategic insights to inform investment or planning decisions.

Suppliers Bargaining Power

Scarce Web3 talent

Specialized blockchain engineers, cryptographers, and token economists remain scarce, with LinkedIn and job aggregators showing over 10,000 global blockchain roles open in 2024, giving talent leverage on pay and terms. Beat risks bidding wars with exchanges, Layer‑1s, and Big Tech, where hiring premiums often reach 20–40% over comparable engineering roles. Hiring delays of 6–12 months can slow product roadmaps and deal due diligence, and long ramp times increase dependence on key individuals.

Cloud & node infrastructure

Reliance on hyperscalers and node/API providers concentrates vendor power: in 2024 AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) together controlled about 66% of global cloud IaaS/PaaS spend, funneling traffic to RPC/indexing/custody vendors. Pricing changes or API throttling can quickly raise operating costs and hurt uptime and margins. Vendor lock-in from proprietary APIs and managed services increases switching costs for deployed services. Integrated compliance features like cloud KMS and HSM further tether critical workloads.

Protocol & tooling ecosystems

Foundations, middleware, and oracle providers set technical roadmaps Beat must follow, with oracle leader Chainlink reporting over 2,000 integrations by 2024, creating lock-in risk. Changes in fee models or deprecation of tools can force costly refactors and higher engineering spend. Access to grants or ecosystem support is selectively allocated, and standards fragmentation—dozens of competing cross-chain standards by 2024—increases coordination costs across chains.

Deal flow gatekeepers

Deal-flow gatekeepers—top VCs, accelerators, and banks controlling proprietary pipelines—can demand favorable co-invest terms, especially as hot rounds compress diligence windows and push higher valuations; VC dry powder exceeded $300B in 2024, concentrating leverage. Preferential allocations often require strategic concessions, and reduced access raises adverse selection risk for outsiders.

Regulatory/compliance vendors

KYC/AML providers, chain-analytics firms and licensing advisors are indispensable in FinTech and digital assets; in 2024 vendor tools underpin onboarding and compliance for over 90% of regulated crypto firms. Their methodologies and jurisdictional coverage directly constrain product scope and market access, and per-seat or price-escalator licensing can erode unit economics. Switching vendors requires recertification, retraining and regulator notifications, often taking months and adding material compliance spend.

- Vendor reliance: >90% of regulated crypto firms (2024)

- Coverage gaps: ~10–15% of jurisdictions affected

- Cost pressure: per-seat/escalators materially reduce margins

- Switching burden: months for recertification and notifications

Suppliers power: pay premiums 20-40%, VC dry powder $300B+

Suppliers hold strong leverage: 10,000+ global blockchain roles in 2024 lift wage premiums 20–40% and extend hiring 6–12 months. Hyperscalers (AWS 32%, Azure 23%, GCP 11%) and Chainlink (2,000+ integrations) create vendor lock‑in; VC dry powder >$300B and >90% reliance on KYC tools amplify gatekeeper power.

| Metric | 2024 |

|---|---|

| Blockchain roles open | 10,000+ |

| AWS/Azure/GCP share | 32%/23%/11% |

| Chainlink integrations | 2,000+ |

| VC dry powder | $300B+ |

What is included in the product

Comprehensive Five Forces analysis of Beat, uncovering competitive rivalry, buyer/supplier power, substitutes, and entry threats with industry data and strategic commentary. Identifies disruptive forces and market dynamics shaping pricing, profitability, and barriers to entry; fully editable Word format for reports and decks.

Beat Porter's Five Forces delivers a one-sheet, customizable summary with pressure sliders, instant spider chart and clean layout—ready for decks, scenario tabs and dashboards; swap your own data and use without macros to relieve analysis bottlenecks for non-finance users.

Customers Bargaining Power

Enterprise concentration

Large APAC conglomerates and financial institutions routinely negotiate 10–20% volume discounts and strict SLAs, with procurement cycles extending sales timelines by 30–90 days and pressuring payment terms; marquee client referenceability boosts buyer leverage, and losing a single major account can cut supplier revenue by 10–40%, per 2024 industry surveys.

Low switching costs in pilots

POCs for blockchain services are modular and reversible, enabling competitors to replicate core features quickly; Gartner forecasted enterprise blockchain spending near $19 billion in 2024, reflecting intense vendor activity that shortens imitation cycles. Buyers often multi-home across providers to benchmark outcomes, increasing price sensitivity and forcing Beat to differentiate on performance, integrations, and measurable ROI rather than price alone.

Deal terms in investments

Startups can choose VC, CVC, or strategic capital and negotiate valuation and protective rights; in 2024 deal structures increasingly included pro-rata and liquidation preference clauses. Hot sectors in 2024 let founders push investor-unfriendly terms as competition for allocations rose. Beat may need to offer strategic value or follow-on certainty to win slots in competitive rounds where investees hold stronger bargaining power.

High information transparency

- Open-source dashboards: public performance metrics (2024)

- Token/deal data: improved price/fee comparison (2024)

- Reduced information rents → stronger buyer negotiation

Demand for credibility

Buyers demand demonstrable credibility: compliance, security certifications and audited code are procurement gating items; in 2024 roughly 71% of enterprise buyers prioritized certifications in vendor selection. Any trust lapse typically triggers re-tendering or churn, forcing Beat to absorb recurring audit and assurance costs and accept strict reporting covenants that can constrain margins.

- Compliance as gate: certifications required

- Churn risk: re-tendering on lapses

- Ongoing cost: continuous audits/assurance

- Covenants: stringent reporting imposed by clients

Buyers squeeze margins: APAC corporates demand 10–20% discounts, extend payments 30–90 days

Buyers wield strong leverage: large APAC corporates secure 10–20% volume discounts and extend procurement 30–90 days, squeezing payment terms and margins. Enterprise blockchain spend reached about $19B in 2024, driving vendor competition and customer multi-homing. Certification/security are gating factors—71% of enterprise buyers prioritized certifications in 2024—while loss of a major account can cut supplier revenue 10–40%.

| Metric | 2024 | Impact |

|---|---|---|

| Volume discounts | 10–20% | Margin pressure |

| Procurement delay | 30–90 days | Sales cycle lengthening |

| Blockchain spend | $19B | Intense vendor competition |

| Certifications | 71% buyers | Procurement gate |

| Major account loss | 10–40% revenue | High concentration risk |

Full Version Awaits

Beat Porter's Five Forces Analysis

This preview shows the exact Beat Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of entry, and substitutes with actionable insights. No placeholders or samples—this is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

This snapshot highlights Beat’s competitive landscape—buyer and supplier power, threat of entrants and substitutes, and industry rivalry—but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, Excel/Word deliverables, and actionable strategic insights to inform investment or planning decisions.

Suppliers Bargaining Power

Scarce Web3 talent

Specialized blockchain engineers, cryptographers, and token economists remain scarce, with LinkedIn and job aggregators showing over 10,000 global blockchain roles open in 2024, giving talent leverage on pay and terms. Beat risks bidding wars with exchanges, Layer‑1s, and Big Tech, where hiring premiums often reach 20–40% over comparable engineering roles. Hiring delays of 6–12 months can slow product roadmaps and deal due diligence, and long ramp times increase dependence on key individuals.

Cloud & node infrastructure

Reliance on hyperscalers and node/API providers concentrates vendor power: in 2024 AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) together controlled about 66% of global cloud IaaS/PaaS spend, funneling traffic to RPC/indexing/custody vendors. Pricing changes or API throttling can quickly raise operating costs and hurt uptime and margins. Vendor lock-in from proprietary APIs and managed services increases switching costs for deployed services. Integrated compliance features like cloud KMS and HSM further tether critical workloads.

Protocol & tooling ecosystems

Foundations, middleware, and oracle providers set technical roadmaps Beat must follow, with oracle leader Chainlink reporting over 2,000 integrations by 2024, creating lock-in risk. Changes in fee models or deprecation of tools can force costly refactors and higher engineering spend. Access to grants or ecosystem support is selectively allocated, and standards fragmentation—dozens of competing cross-chain standards by 2024—increases coordination costs across chains.

Deal flow gatekeepers

Deal-flow gatekeepers—top VCs, accelerators, and banks controlling proprietary pipelines—can demand favorable co-invest terms, especially as hot rounds compress diligence windows and push higher valuations; VC dry powder exceeded $300B in 2024, concentrating leverage. Preferential allocations often require strategic concessions, and reduced access raises adverse selection risk for outsiders.

Regulatory/compliance vendors

KYC/AML providers, chain-analytics firms and licensing advisors are indispensable in FinTech and digital assets; in 2024 vendor tools underpin onboarding and compliance for over 90% of regulated crypto firms. Their methodologies and jurisdictional coverage directly constrain product scope and market access, and per-seat or price-escalator licensing can erode unit economics. Switching vendors requires recertification, retraining and regulator notifications, often taking months and adding material compliance spend.

- Vendor reliance: >90% of regulated crypto firms (2024)

- Coverage gaps: ~10–15% of jurisdictions affected

- Cost pressure: per-seat/escalators materially reduce margins

- Switching burden: months for recertification and notifications

Suppliers power: pay premiums 20-40%, VC dry powder $300B+

Suppliers hold strong leverage: 10,000+ global blockchain roles in 2024 lift wage premiums 20–40% and extend hiring 6–12 months. Hyperscalers (AWS 32%, Azure 23%, GCP 11%) and Chainlink (2,000+ integrations) create vendor lock‑in; VC dry powder >$300B and >90% reliance on KYC tools amplify gatekeeper power.

| Metric | 2024 |

|---|---|

| Blockchain roles open | 10,000+ |

| AWS/Azure/GCP share | 32%/23%/11% |

| Chainlink integrations | 2,000+ |

| VC dry powder | $300B+ |

What is included in the product

Comprehensive Five Forces analysis of Beat, uncovering competitive rivalry, buyer/supplier power, substitutes, and entry threats with industry data and strategic commentary. Identifies disruptive forces and market dynamics shaping pricing, profitability, and barriers to entry; fully editable Word format for reports and decks.

Beat Porter's Five Forces delivers a one-sheet, customizable summary with pressure sliders, instant spider chart and clean layout—ready for decks, scenario tabs and dashboards; swap your own data and use without macros to relieve analysis bottlenecks for non-finance users.

Customers Bargaining Power

Enterprise concentration

Large APAC conglomerates and financial institutions routinely negotiate 10–20% volume discounts and strict SLAs, with procurement cycles extending sales timelines by 30–90 days and pressuring payment terms; marquee client referenceability boosts buyer leverage, and losing a single major account can cut supplier revenue by 10–40%, per 2024 industry surveys.

Low switching costs in pilots

POCs for blockchain services are modular and reversible, enabling competitors to replicate core features quickly; Gartner forecasted enterprise blockchain spending near $19 billion in 2024, reflecting intense vendor activity that shortens imitation cycles. Buyers often multi-home across providers to benchmark outcomes, increasing price sensitivity and forcing Beat to differentiate on performance, integrations, and measurable ROI rather than price alone.

Deal terms in investments

Startups can choose VC, CVC, or strategic capital and negotiate valuation and protective rights; in 2024 deal structures increasingly included pro-rata and liquidation preference clauses. Hot sectors in 2024 let founders push investor-unfriendly terms as competition for allocations rose. Beat may need to offer strategic value or follow-on certainty to win slots in competitive rounds where investees hold stronger bargaining power.

High information transparency

- Open-source dashboards: public performance metrics (2024)

- Token/deal data: improved price/fee comparison (2024)

- Reduced information rents → stronger buyer negotiation

Demand for credibility

Buyers demand demonstrable credibility: compliance, security certifications and audited code are procurement gating items; in 2024 roughly 71% of enterprise buyers prioritized certifications in vendor selection. Any trust lapse typically triggers re-tendering or churn, forcing Beat to absorb recurring audit and assurance costs and accept strict reporting covenants that can constrain margins.

- Compliance as gate: certifications required

- Churn risk: re-tendering on lapses

- Ongoing cost: continuous audits/assurance

- Covenants: stringent reporting imposed by clients

Buyers squeeze margins: APAC corporates demand 10–20% discounts, extend payments 30–90 days

Buyers wield strong leverage: large APAC corporates secure 10–20% volume discounts and extend procurement 30–90 days, squeezing payment terms and margins. Enterprise blockchain spend reached about $19B in 2024, driving vendor competition and customer multi-homing. Certification/security are gating factors—71% of enterprise buyers prioritized certifications in 2024—while loss of a major account can cut supplier revenue 10–40%.

| Metric | 2024 | Impact |

|---|---|---|

| Volume discounts | 10–20% | Margin pressure |

| Procurement delay | 30–90 days | Sales cycle lengthening |

| Blockchain spend | $19B | Intense vendor competition |

| Certifications | 71% buyers | Procurement gate |

| Major account loss | 10–40% revenue | High concentration risk |

Full Version Awaits

Beat Porter's Five Forces Analysis

This preview shows the exact Beat Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of entry, and substitutes with actionable insights. No placeholders or samples—this is the final deliverable.