Bechtel Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

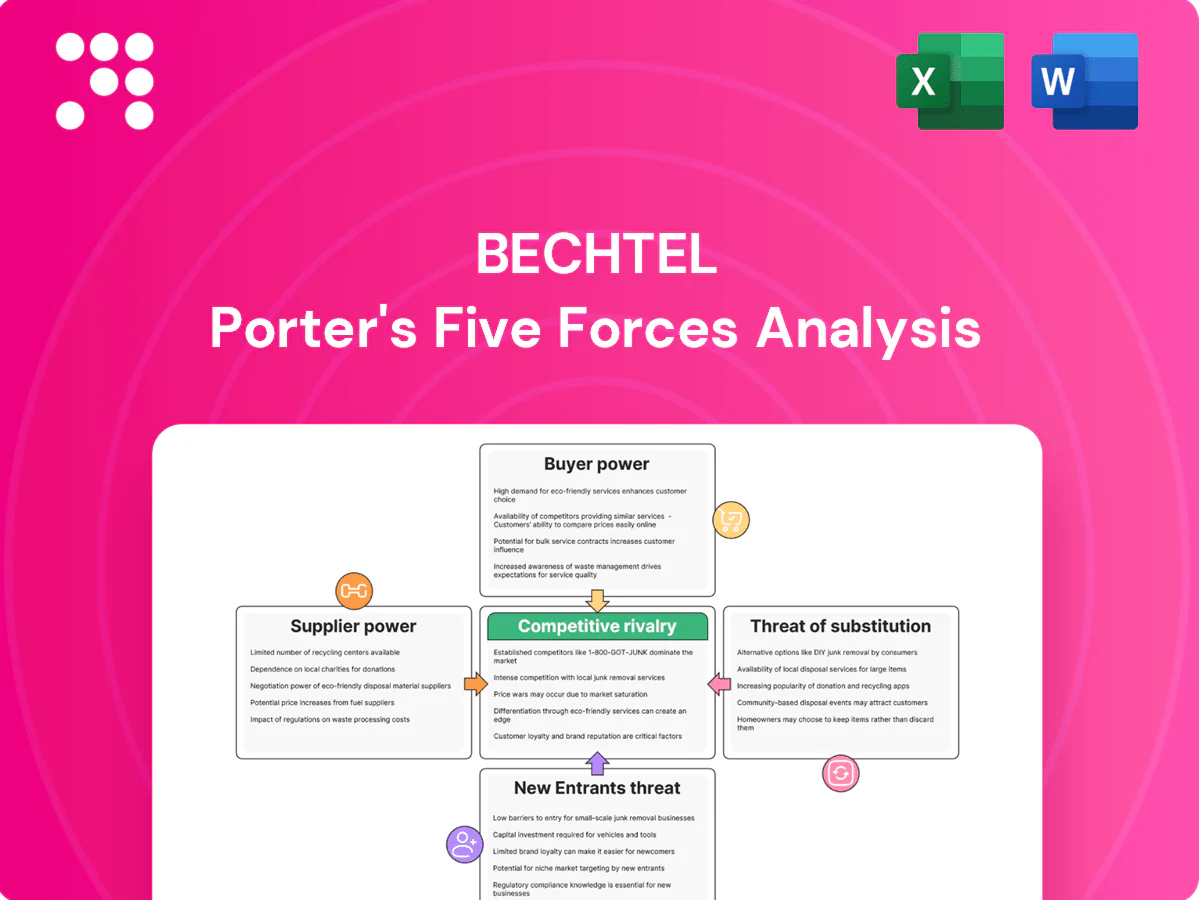

Bechtel’s Porter's Five Forces snapshot highlights strong supplier relationships, project-level bargaining power, high barriers from scale and reputation, and moderate threat from substitutes and new entrants. This brief view outlines competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Specialized materials scarcity

Bechtel depends on niche suppliers of high-grade steel, specialty alloys and advanced composites, a sector where global crude steel output reached about 1.86 billion tonnes in 2024 (World Steel Association) but production of specialty grades remains concentrated among few producers, raising switching costs and lead-time risks. Long-term frame agreements and dual-sourcing temper supplier power but cannot eliminate occasional bottlenecks. Project scheduling buffers and early procurement are therefore critical mitigants, often extending lead-time cushions by months on major projects.

OEM equipment dependence

Large rotating equipment, turbines, HV components and control systems are concentrated among a few OEMs; GE, Siemens Energy and Mitsubishi Power held about 85% of the heavy‑duty gas turbine market in 2024, concentrating sourcing risk.

Technical lock‑in and warranty terms (commonly 24–60 months) strengthen OEM leverage over aftermarket pricing and upgrades.

Bechtel offsets this with competitive bid lists and lifecycle TCO analyses, which industry benchmarks show can reduce procurement plus O&M costs by roughly 10%.

Project standardization further cuts integration risks and narrows price variance across sites.

Skilled labor and unions

Skilled craft labor, welders, and specialized trades are tight in peak cycles and geographies, with US construction employment around 7.8 million in 2024 and unionization in construction near 18%, boosting supplier leverage. Union agreements, prevailing wages, and site constraints raise costs and scheduling risk. Workforce development and modularization (reducing on-site labor up to 30%) lower intensity, while flexible staffing and global mobility smooth spikes.

Logistics and geopolitics

Logistics and geopolitics drive supplier power for Bechtel: heavy-lift shipping, cross-border customs friction and 2024 sanctions regimes raised delivery uncertainty and cost, and carriers and freight forwarders gained leverage during capacity crunches. Early logistics engineering and alternative-route planning reduce exposure, while local content strategies de-risk import dependencies and limit supplier hold-up.

- Heavy-lift bottlenecks: capacity concentration

- Customs/sanctions: route delays and cost inflation in 2024

- Mitigants: early logistics engineering

- Mitigants: local content to lower import risk

Commodity and energy volatility

Steel, copper, cement and fuel price swings (steel ±25% 2023–24, copper ±15%, cement +8–12% regionally, diesel transport cost spikes ~30%) cascade into supplier quotes; index-linked contracts increasingly push volatility to buyers. Bechtel mitigates with hedging, escalation clauses and bulk-buy programs and applies value-engineering to redesign around constrained inputs.

- hedging

- escalation-clauses

- bulk-buy-programs

- value-engineering

Supplier power in turbines and steel spikes cost risk; early sourcing, dual approaches mitigate

Supplier power is high for specialty steels, turbines and HV gear (heavy gas turbines: GE/Siemens/Mitsubishi ~85% share in 2024) and is amplified by price swings (steel ±25% 2023–24, copper ±15%). Bechtel uses long‑term frames, dual sourcing, hedging and value engineering to cut exposure. Logistics, customs and labor tightness raise hold‑up risk; early procurement and modularization are key mitigants.

| Item | 2024 data | Impact |

|---|---|---|

| Turbine market | ~85% top 3 | High OEM leverage |

| Steel output | 1.86bn t | Supply concentration |

| Price volatility | Steel ±25% | Cost risk |

What is included in the product

Concise Porter's Five Forces assessment of Bechtel, revealing competitive rivalry, supplier and buyer power, substitute threats, and barriers to entry shaping its project-based engineering and construction margins. Includes strategic insights on disruptive entrants, regulatory risks, and negotiation leverage to inform investor and executive decision-making.

A concise, one-sheet Bechtel Porter's Five Forces snapshot—quickly pinpoint competitive pressures and strategic levers to resolve procurement bottlenecks, contractor rivalry, and regulatory pain points for faster, board-ready decisions.

Customers Bargaining Power

Mega-project client concentration

National governments, IOCs, miners and utilities award multi-billion-dollar projects (commonly >$5bn), creating concentrated spend that gives clients strong negotiating leverage. Clients push for favorable pricing, risk transfer and enhanced transparency on schedules and costs. The global infrastructure investment shortfall is estimated at about 94 trillion dollars to 2040, keeping competition intense. Referenceability and repeat work partially rebalance power for contractors.

Competitive tendering pressure

Open tenders and prequalified bid lists drive higher bid counts and intense price competition; detailed RFPs enable apples-to-apples comparisons that compress margins—industry contractor EBIT ran about 3–7% in 2024. Bechtel differentiates through documented execution track record, safety performance and schedule certainty. Early contractor involvement, used increasingly in 2024, shifts selection from low price to delivered value.

Performance and LD clauses

Buyers enforce stringent KPIs, liquidated damages commonly set at 0.1–0.5% of contract value per day (caps typically 5–10%), and 12–24 month warranties, shifting interface and delay risks onto EPCs. Risk allocation drives Bechtel to negotiate risk-sharing, defined relief events, and realistic baselines to limit exposure. By 2024, digital progress tracking—used by a majority of large EPCs—supports time-stamped claims and mitigations, tightening evidence for negotiations.

Scope changes and financing

Clients adjust scope as permits, ESG rules and financing milestones evolve; as of 2024 these links have become standard in large EPC contracts. Change orders frequently become contentious, straining cash flow and margins. Robust change management and earned-value controls preserve margins while lender and export credit agency ties align incentives and reduce disputes.

- Scope drift tied to permits/ESG/finance

- Change orders → cash-flow risk

- Earned-value controls protect margins

- Lender/ECA alignment lowers dispute risk

Switching costs vs. multi-sourcing

Once detailed design begins, switching EPCs is costly and risky, reducing buyer power; ENR ranked Bechtel #1 in its 2024 Top 400 Contractors, underscoring market position that increases stickiness. Clients still retain leverage by splitting packages across multiple contractors, a common multi-sourcing tactic. Bechtel’s integrated EPCM and PMO offerings plus robust handover documentation lower interface risk and sustain client trust.

Clients award >$5bn EPCs; tight KPIs, LDs and change-order risk squeeze contractors

Clients (often national governments/IOCs) award multi-billion-dollar projects (> $5bn), concentrating spend and driving strong price/risk leverage; industry EPC EBIT ran ~3–7% in 2024. Stringent KPIs, liquidated damages (0.1–0.5%/day, caps 5–10%) and change-order risk shift costs to contractors, though Bechtel’s ENR #1 2024 rank, execution track record and rising switching costs at detailed design increase contractor stickiness.

| Metric | 2024 Value |

|---|---|

| Typical project size | > $5bn |

| Industry EPC EBIT | 3–7% |

| Liquidated damages | 0.1–0.5%/day (caps 5–10%) |

| Bechtel rank | ENR #1 (2024) |

Preview Before You Purchase

Bechtel Porter's Five Forces Analysis

This preview shows the complete Bechtel Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or abridgments. The file is fully formatted, actionable, and ready for download upon payment. Use it as-is for strategic insight and decision-making.

Go Beyond the Preview—Access the Full Strategic Report

Bechtel’s Porter's Five Forces snapshot highlights strong supplier relationships, project-level bargaining power, high barriers from scale and reputation, and moderate threat from substitutes and new entrants. This brief view outlines competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Specialized materials scarcity

Bechtel depends on niche suppliers of high-grade steel, specialty alloys and advanced composites, a sector where global crude steel output reached about 1.86 billion tonnes in 2024 (World Steel Association) but production of specialty grades remains concentrated among few producers, raising switching costs and lead-time risks. Long-term frame agreements and dual-sourcing temper supplier power but cannot eliminate occasional bottlenecks. Project scheduling buffers and early procurement are therefore critical mitigants, often extending lead-time cushions by months on major projects.

OEM equipment dependence

Large rotating equipment, turbines, HV components and control systems are concentrated among a few OEMs; GE, Siemens Energy and Mitsubishi Power held about 85% of the heavy‑duty gas turbine market in 2024, concentrating sourcing risk.

Technical lock‑in and warranty terms (commonly 24–60 months) strengthen OEM leverage over aftermarket pricing and upgrades.

Bechtel offsets this with competitive bid lists and lifecycle TCO analyses, which industry benchmarks show can reduce procurement plus O&M costs by roughly 10%.

Project standardization further cuts integration risks and narrows price variance across sites.

Skilled labor and unions

Skilled craft labor, welders, and specialized trades are tight in peak cycles and geographies, with US construction employment around 7.8 million in 2024 and unionization in construction near 18%, boosting supplier leverage. Union agreements, prevailing wages, and site constraints raise costs and scheduling risk. Workforce development and modularization (reducing on-site labor up to 30%) lower intensity, while flexible staffing and global mobility smooth spikes.

Logistics and geopolitics

Logistics and geopolitics drive supplier power for Bechtel: heavy-lift shipping, cross-border customs friction and 2024 sanctions regimes raised delivery uncertainty and cost, and carriers and freight forwarders gained leverage during capacity crunches. Early logistics engineering and alternative-route planning reduce exposure, while local content strategies de-risk import dependencies and limit supplier hold-up.

- Heavy-lift bottlenecks: capacity concentration

- Customs/sanctions: route delays and cost inflation in 2024

- Mitigants: early logistics engineering

- Mitigants: local content to lower import risk

Commodity and energy volatility

Steel, copper, cement and fuel price swings (steel ±25% 2023–24, copper ±15%, cement +8–12% regionally, diesel transport cost spikes ~30%) cascade into supplier quotes; index-linked contracts increasingly push volatility to buyers. Bechtel mitigates with hedging, escalation clauses and bulk-buy programs and applies value-engineering to redesign around constrained inputs.

- hedging

- escalation-clauses

- bulk-buy-programs

- value-engineering

Supplier power in turbines and steel spikes cost risk; early sourcing, dual approaches mitigate

Supplier power is high for specialty steels, turbines and HV gear (heavy gas turbines: GE/Siemens/Mitsubishi ~85% share in 2024) and is amplified by price swings (steel ±25% 2023–24, copper ±15%). Bechtel uses long‑term frames, dual sourcing, hedging and value engineering to cut exposure. Logistics, customs and labor tightness raise hold‑up risk; early procurement and modularization are key mitigants.

| Item | 2024 data | Impact |

|---|---|---|

| Turbine market | ~85% top 3 | High OEM leverage |

| Steel output | 1.86bn t | Supply concentration |

| Price volatility | Steel ±25% | Cost risk |

What is included in the product

Concise Porter's Five Forces assessment of Bechtel, revealing competitive rivalry, supplier and buyer power, substitute threats, and barriers to entry shaping its project-based engineering and construction margins. Includes strategic insights on disruptive entrants, regulatory risks, and negotiation leverage to inform investor and executive decision-making.

A concise, one-sheet Bechtel Porter's Five Forces snapshot—quickly pinpoint competitive pressures and strategic levers to resolve procurement bottlenecks, contractor rivalry, and regulatory pain points for faster, board-ready decisions.

Customers Bargaining Power

Mega-project client concentration

National governments, IOCs, miners and utilities award multi-billion-dollar projects (commonly >$5bn), creating concentrated spend that gives clients strong negotiating leverage. Clients push for favorable pricing, risk transfer and enhanced transparency on schedules and costs. The global infrastructure investment shortfall is estimated at about 94 trillion dollars to 2040, keeping competition intense. Referenceability and repeat work partially rebalance power for contractors.

Competitive tendering pressure

Open tenders and prequalified bid lists drive higher bid counts and intense price competition; detailed RFPs enable apples-to-apples comparisons that compress margins—industry contractor EBIT ran about 3–7% in 2024. Bechtel differentiates through documented execution track record, safety performance and schedule certainty. Early contractor involvement, used increasingly in 2024, shifts selection from low price to delivered value.

Performance and LD clauses

Buyers enforce stringent KPIs, liquidated damages commonly set at 0.1–0.5% of contract value per day (caps typically 5–10%), and 12–24 month warranties, shifting interface and delay risks onto EPCs. Risk allocation drives Bechtel to negotiate risk-sharing, defined relief events, and realistic baselines to limit exposure. By 2024, digital progress tracking—used by a majority of large EPCs—supports time-stamped claims and mitigations, tightening evidence for negotiations.

Scope changes and financing

Clients adjust scope as permits, ESG rules and financing milestones evolve; as of 2024 these links have become standard in large EPC contracts. Change orders frequently become contentious, straining cash flow and margins. Robust change management and earned-value controls preserve margins while lender and export credit agency ties align incentives and reduce disputes.

- Scope drift tied to permits/ESG/finance

- Change orders → cash-flow risk

- Earned-value controls protect margins

- Lender/ECA alignment lowers dispute risk

Switching costs vs. multi-sourcing

Once detailed design begins, switching EPCs is costly and risky, reducing buyer power; ENR ranked Bechtel #1 in its 2024 Top 400 Contractors, underscoring market position that increases stickiness. Clients still retain leverage by splitting packages across multiple contractors, a common multi-sourcing tactic. Bechtel’s integrated EPCM and PMO offerings plus robust handover documentation lower interface risk and sustain client trust.

Clients award >$5bn EPCs; tight KPIs, LDs and change-order risk squeeze contractors

Clients (often national governments/IOCs) award multi-billion-dollar projects (> $5bn), concentrating spend and driving strong price/risk leverage; industry EPC EBIT ran ~3–7% in 2024. Stringent KPIs, liquidated damages (0.1–0.5%/day, caps 5–10%) and change-order risk shift costs to contractors, though Bechtel’s ENR #1 2024 rank, execution track record and rising switching costs at detailed design increase contractor stickiness.

| Metric | 2024 Value |

|---|---|

| Typical project size | > $5bn |

| Industry EPC EBIT | 3–7% |

| Liquidated damages | 0.1–0.5%/day (caps 5–10%) |

| Bechtel rank | ENR #1 (2024) |

Preview Before You Purchase

Bechtel Porter's Five Forces Analysis

This preview shows the complete Bechtel Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or abridgments. The file is fully formatted, actionable, and ready for download upon payment. Use it as-is for strategic insight and decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Bechtel’s Porter's Five Forces snapshot highlights strong supplier relationships, project-level bargaining power, high barriers from scale and reputation, and moderate threat from substitutes and new entrants. This brief view outlines competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Specialized materials scarcity

Bechtel depends on niche suppliers of high-grade steel, specialty alloys and advanced composites, a sector where global crude steel output reached about 1.86 billion tonnes in 2024 (World Steel Association) but production of specialty grades remains concentrated among few producers, raising switching costs and lead-time risks. Long-term frame agreements and dual-sourcing temper supplier power but cannot eliminate occasional bottlenecks. Project scheduling buffers and early procurement are therefore critical mitigants, often extending lead-time cushions by months on major projects.

OEM equipment dependence

Large rotating equipment, turbines, HV components and control systems are concentrated among a few OEMs; GE, Siemens Energy and Mitsubishi Power held about 85% of the heavy‑duty gas turbine market in 2024, concentrating sourcing risk.

Technical lock‑in and warranty terms (commonly 24–60 months) strengthen OEM leverage over aftermarket pricing and upgrades.

Bechtel offsets this with competitive bid lists and lifecycle TCO analyses, which industry benchmarks show can reduce procurement plus O&M costs by roughly 10%.

Project standardization further cuts integration risks and narrows price variance across sites.

Skilled labor and unions

Skilled craft labor, welders, and specialized trades are tight in peak cycles and geographies, with US construction employment around 7.8 million in 2024 and unionization in construction near 18%, boosting supplier leverage. Union agreements, prevailing wages, and site constraints raise costs and scheduling risk. Workforce development and modularization (reducing on-site labor up to 30%) lower intensity, while flexible staffing and global mobility smooth spikes.

Logistics and geopolitics

Logistics and geopolitics drive supplier power for Bechtel: heavy-lift shipping, cross-border customs friction and 2024 sanctions regimes raised delivery uncertainty and cost, and carriers and freight forwarders gained leverage during capacity crunches. Early logistics engineering and alternative-route planning reduce exposure, while local content strategies de-risk import dependencies and limit supplier hold-up.

- Heavy-lift bottlenecks: capacity concentration

- Customs/sanctions: route delays and cost inflation in 2024

- Mitigants: early logistics engineering

- Mitigants: local content to lower import risk

Commodity and energy volatility

Steel, copper, cement and fuel price swings (steel ±25% 2023–24, copper ±15%, cement +8–12% regionally, diesel transport cost spikes ~30%) cascade into supplier quotes; index-linked contracts increasingly push volatility to buyers. Bechtel mitigates with hedging, escalation clauses and bulk-buy programs and applies value-engineering to redesign around constrained inputs.

- hedging

- escalation-clauses

- bulk-buy-programs

- value-engineering

Supplier power in turbines and steel spikes cost risk; early sourcing, dual approaches mitigate

Supplier power is high for specialty steels, turbines and HV gear (heavy gas turbines: GE/Siemens/Mitsubishi ~85% share in 2024) and is amplified by price swings (steel ±25% 2023–24, copper ±15%). Bechtel uses long‑term frames, dual sourcing, hedging and value engineering to cut exposure. Logistics, customs and labor tightness raise hold‑up risk; early procurement and modularization are key mitigants.

| Item | 2024 data | Impact |

|---|---|---|

| Turbine market | ~85% top 3 | High OEM leverage |

| Steel output | 1.86bn t | Supply concentration |

| Price volatility | Steel ±25% | Cost risk |

What is included in the product

Concise Porter's Five Forces assessment of Bechtel, revealing competitive rivalry, supplier and buyer power, substitute threats, and barriers to entry shaping its project-based engineering and construction margins. Includes strategic insights on disruptive entrants, regulatory risks, and negotiation leverage to inform investor and executive decision-making.

A concise, one-sheet Bechtel Porter's Five Forces snapshot—quickly pinpoint competitive pressures and strategic levers to resolve procurement bottlenecks, contractor rivalry, and regulatory pain points for faster, board-ready decisions.

Customers Bargaining Power

Mega-project client concentration

National governments, IOCs, miners and utilities award multi-billion-dollar projects (commonly >$5bn), creating concentrated spend that gives clients strong negotiating leverage. Clients push for favorable pricing, risk transfer and enhanced transparency on schedules and costs. The global infrastructure investment shortfall is estimated at about 94 trillion dollars to 2040, keeping competition intense. Referenceability and repeat work partially rebalance power for contractors.

Competitive tendering pressure

Open tenders and prequalified bid lists drive higher bid counts and intense price competition; detailed RFPs enable apples-to-apples comparisons that compress margins—industry contractor EBIT ran about 3–7% in 2024. Bechtel differentiates through documented execution track record, safety performance and schedule certainty. Early contractor involvement, used increasingly in 2024, shifts selection from low price to delivered value.

Performance and LD clauses

Buyers enforce stringent KPIs, liquidated damages commonly set at 0.1–0.5% of contract value per day (caps typically 5–10%), and 12–24 month warranties, shifting interface and delay risks onto EPCs. Risk allocation drives Bechtel to negotiate risk-sharing, defined relief events, and realistic baselines to limit exposure. By 2024, digital progress tracking—used by a majority of large EPCs—supports time-stamped claims and mitigations, tightening evidence for negotiations.

Scope changes and financing

Clients adjust scope as permits, ESG rules and financing milestones evolve; as of 2024 these links have become standard in large EPC contracts. Change orders frequently become contentious, straining cash flow and margins. Robust change management and earned-value controls preserve margins while lender and export credit agency ties align incentives and reduce disputes.

- Scope drift tied to permits/ESG/finance

- Change orders → cash-flow risk

- Earned-value controls protect margins

- Lender/ECA alignment lowers dispute risk

Switching costs vs. multi-sourcing

Once detailed design begins, switching EPCs is costly and risky, reducing buyer power; ENR ranked Bechtel #1 in its 2024 Top 400 Contractors, underscoring market position that increases stickiness. Clients still retain leverage by splitting packages across multiple contractors, a common multi-sourcing tactic. Bechtel’s integrated EPCM and PMO offerings plus robust handover documentation lower interface risk and sustain client trust.

Clients award >$5bn EPCs; tight KPIs, LDs and change-order risk squeeze contractors

Clients (often national governments/IOCs) award multi-billion-dollar projects (> $5bn), concentrating spend and driving strong price/risk leverage; industry EPC EBIT ran ~3–7% in 2024. Stringent KPIs, liquidated damages (0.1–0.5%/day, caps 5–10%) and change-order risk shift costs to contractors, though Bechtel’s ENR #1 2024 rank, execution track record and rising switching costs at detailed design increase contractor stickiness.

| Metric | 2024 Value |

|---|---|

| Typical project size | > $5bn |

| Industry EPC EBIT | 3–7% |

| Liquidated damages | 0.1–0.5%/day (caps 5–10%) |

| Bechtel rank | ENR #1 (2024) |

Preview Before You Purchase

Bechtel Porter's Five Forces Analysis

This preview shows the complete Bechtel Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or abridgments. The file is fully formatted, actionable, and ready for download upon payment. Use it as-is for strategic insight and decision-making.