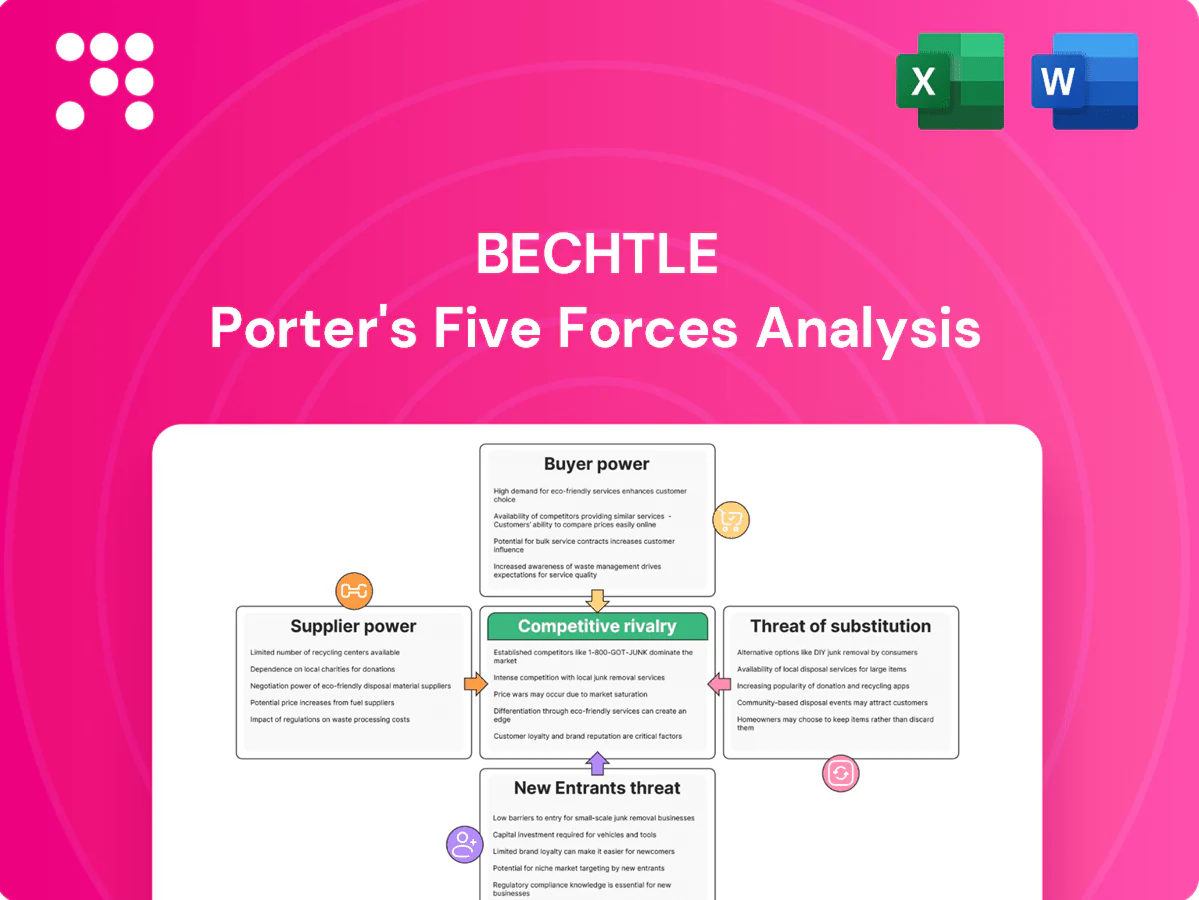

Bechtle Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Bechtle faces moderate buyer power and rising competitive intensity from cloud and managed-service players, while supplier leverage is tempered by scale and partnerships; regulatory and tech shifts add both risk and opportunity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bechtle’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on tier-1 OEMs and software giants

Bechtle relies heavily on tier-1 vendors—Microsoft, HPE, Dell, Cisco, VMware—for core hardware, software and licensing; in fiscal 2024 Bechtle reported group revenue of about €8.1bn, so vendor pricing/programs materially affect margins. Partner tiers and rebate schemes can swing gross margins by several percentage points, making supplier concentration a leverage point; diversifying vendors and expanding higher-margin services reduces that dependency.

Hyperscaler program dependency

Azure, AWS and Google Cloud together hold about 66% of the 2024 global cloud infrastructure market (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11%), giving them decisive control over partner margins, incentives and technical roadmaps. Sudden partner program changes have tightened economics for resellers in 2024, so Bechtle must maintain multi-cloud competencies to reduce single-vendor exposure. Strong co-selling alignment with hyperscalers can partially rebalance supplier influence.

Niche software and cybersecurity suppliers

Specialist software and cybersecurity vendors hold differentiated IP with few substitutes, strengthening supplier leverage as the global cybersecurity market exceeded 200 billion USD in 2024. Certification and vendor enablement (Microsoft, Cisco, Palo Alto) create measurable switching costs for Bechtle and its clients through trained personnel and accredited integrations. Suppliers can enforce minimum purchase levels and restrict discounting, while Bechtle dilutes this power by bundling across its hundreds of vendor partnerships and value-added services.

IT distribution and logistics intermediaries

Distributors like ALSO, Ingram Micro and TD Synnex control availability, credit terms and delivery SLAs, and tight component cycles—notably semiconductor constraints since 2020—have increased their leverage over resellers. Bechtle’s EUR 6–7bn+ IT purchasing scale (2024 run-rate) secures better allocations and rebate tiers, while multi-distributor sourcing mitigates single-supplier exposure and SLA risk.

- Major distributors: channel control, inventory leverage

- Bechtle scale: stronger allocations & rebates

- Multi-sourcing: lowers dependency

Skilled talent as a critical supplier

In 2024 certified engineers, architects and security experts remain scarce and mobile, giving them leverage through wage inflation and premium certifications; delivery capacity constraints are pushing project prices and timelines up, while workforce development programs and nearshore hubs are increasingly used to mitigate this supplier power.

- Scarcity: certified specialists retain high mobility

- Compensation: wage inflation strengthens bargaining

- Capacity: delivery limits affect pricing/timelines

- Mitigation: training programs and nearshore hubs

Hyperscaler supplier power strains margins as €8.1bn revenue depends on AWS/Azure/GCP

Bechtle faces strong supplier power from tier-1 vendors and hyperscalers; €8.1bn 2024 revenue makes margins sensitive to partner programs. Hyperscalers hold ~66% cloud IaaS (AWS 32%, Azure 23%, Google 11%), raising dependency; distributors and specialist vendors add leverage, while company scale and multi-sourcing mitigate risk.

| Metric | 2024 |

|---|---|

| Revenue | €8.1bn |

| Cloud share (AWS/Azure/GCP) | 32/23/11% |

| Purchasing run-rate | €6–7bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Bechtle, detailing supplier and buyer power, threat of substitutes, competitive rivalry, and barriers protecting incumbency, with strategic commentary on emerging digital disruptors and margin pressures.

A concise one-sheet Porter's Five Forces for Bechtle that highlights supplier, buyer, rival, entrant and substitute pressures with quantified drivers—ideal for quick strategic decisions and slide-ready presentations.

Customers Bargaining Power

Large enterprise and public sector procurement

Framework contracts, formal tenders and strict SLAs give large enterprise and public buyers clear pricing and contractual leverage, forcing suppliers to trade margin for scale and long-term commitments. Public procurement—accounting for roughly 14% of EU GDP—boosts transparency and price comparability, intensifying buyer power. Bechtle’s catalog of public-sector references and compliance certifications lowers switching friction for these customers.

Multi-sourcing and easy switching among integrators

Clients increasingly multi-source, splitting workloads across several system houses, which raises substitutability as comparable vendor certifications proliferate; in 2024 Bechtle reported revenues above EUR 7bn, underscoring scale but not immunity to churn. This dynamic fuels more frequent rebidding and rate pressure, though sticky managed services and proprietary IP bundles help lower churn and protect margins.

Commoditized hardware and licensing

Standard hardware and licensing are highly price-transparent, with 2024 surveys showing over 60% of B2B buyers using online quotes/marketplaces to compare offers. Distribution margins for commoditized hardware typically sit in the 3–7% range, while software resale margins often run 5–15%, forcing expected discounts. Thin margins make value-add services and lifecycle management essential to defend price and protect overall profitability.

Managed services with SLA leverage

- Long-term contracts: lower churn, include penalties/credits

- Buyers demand: outcome-based pricing, flexibility (53% in 2024)

- Renewals: primary negotiation moments

- Defenses: strict KPIs, automation — ~10% fewer concessions

Demand for vertical expertise and compliance

Regulated sectors increasingly demand domain knowledge and certifications such as ISO 27001 and GDPR-aligned processes, reinforced by the 2024 EU NIS2 expansion raising cybersecurity obligations across member states. Where Bechtle provides sector-specific solutions and certified services, buyer power weakens as clients prioritize compliance. Tailored architectures and reference templates raise switching costs and deepen account entrenchment.

- Certification focus: ISO 27001, GDPR, NIS2

- Effect: lower buyer leverage

- Switching costs: tailored architectures

- Entrenchment: reference architectures/templates

Scale eases pressure but churn persists, tenders, outcome SLAs and certifications force discounts

Large buyers use framework contracts, public procurement (~14% EU GDP) and tenders to force discounts; Bechtle’s >EUR 7bn 2024 scale helps but does not eliminate churn. 2024: 53% of buyers demand outcome-based SLAs, hardware margins 3–7%, software resale 5–15%, automation cut concessions ~10%. Certifications (ISO 27001, NIS2) raise switching costs for regulated clients.

| Metric | 2024 Value |

|---|---|

| Bechtle revenue | EUR 7bn+ |

| Public procurement | ~14% EU GDP |

| Buyers preferring outcome SLAs | 53% |

| Hardware margins | 3–7% |

| Software resale margins | 5–15% |

| Automation effect | ~10% fewer concessions |

Preview Before You Purchase

Bechtle Porter's Five Forces Analysis

This Bechtle Porter’s Five Forces analysis provides an in-depth assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, tailored to Bechtle’s IT services and distribution model. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or samples. It’s ready for download and immediate use to inform strategic or investment decisions.

From Overview to Strategy Blueprint

Bechtle faces moderate buyer power and rising competitive intensity from cloud and managed-service players, while supplier leverage is tempered by scale and partnerships; regulatory and tech shifts add both risk and opportunity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bechtle’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on tier-1 OEMs and software giants

Bechtle relies heavily on tier-1 vendors—Microsoft, HPE, Dell, Cisco, VMware—for core hardware, software and licensing; in fiscal 2024 Bechtle reported group revenue of about €8.1bn, so vendor pricing/programs materially affect margins. Partner tiers and rebate schemes can swing gross margins by several percentage points, making supplier concentration a leverage point; diversifying vendors and expanding higher-margin services reduces that dependency.

Hyperscaler program dependency

Azure, AWS and Google Cloud together hold about 66% of the 2024 global cloud infrastructure market (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11%), giving them decisive control over partner margins, incentives and technical roadmaps. Sudden partner program changes have tightened economics for resellers in 2024, so Bechtle must maintain multi-cloud competencies to reduce single-vendor exposure. Strong co-selling alignment with hyperscalers can partially rebalance supplier influence.

Niche software and cybersecurity suppliers

Specialist software and cybersecurity vendors hold differentiated IP with few substitutes, strengthening supplier leverage as the global cybersecurity market exceeded 200 billion USD in 2024. Certification and vendor enablement (Microsoft, Cisco, Palo Alto) create measurable switching costs for Bechtle and its clients through trained personnel and accredited integrations. Suppliers can enforce minimum purchase levels and restrict discounting, while Bechtle dilutes this power by bundling across its hundreds of vendor partnerships and value-added services.

IT distribution and logistics intermediaries

Distributors like ALSO, Ingram Micro and TD Synnex control availability, credit terms and delivery SLAs, and tight component cycles—notably semiconductor constraints since 2020—have increased their leverage over resellers. Bechtle’s EUR 6–7bn+ IT purchasing scale (2024 run-rate) secures better allocations and rebate tiers, while multi-distributor sourcing mitigates single-supplier exposure and SLA risk.

- Major distributors: channel control, inventory leverage

- Bechtle scale: stronger allocations & rebates

- Multi-sourcing: lowers dependency

Skilled talent as a critical supplier

In 2024 certified engineers, architects and security experts remain scarce and mobile, giving them leverage through wage inflation and premium certifications; delivery capacity constraints are pushing project prices and timelines up, while workforce development programs and nearshore hubs are increasingly used to mitigate this supplier power.

- Scarcity: certified specialists retain high mobility

- Compensation: wage inflation strengthens bargaining

- Capacity: delivery limits affect pricing/timelines

- Mitigation: training programs and nearshore hubs

Hyperscaler supplier power strains margins as €8.1bn revenue depends on AWS/Azure/GCP

Bechtle faces strong supplier power from tier-1 vendors and hyperscalers; €8.1bn 2024 revenue makes margins sensitive to partner programs. Hyperscalers hold ~66% cloud IaaS (AWS 32%, Azure 23%, Google 11%), raising dependency; distributors and specialist vendors add leverage, while company scale and multi-sourcing mitigate risk.

| Metric | 2024 |

|---|---|

| Revenue | €8.1bn |

| Cloud share (AWS/Azure/GCP) | 32/23/11% |

| Purchasing run-rate | €6–7bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Bechtle, detailing supplier and buyer power, threat of substitutes, competitive rivalry, and barriers protecting incumbency, with strategic commentary on emerging digital disruptors and margin pressures.

A concise one-sheet Porter's Five Forces for Bechtle that highlights supplier, buyer, rival, entrant and substitute pressures with quantified drivers—ideal for quick strategic decisions and slide-ready presentations.

Customers Bargaining Power

Large enterprise and public sector procurement

Framework contracts, formal tenders and strict SLAs give large enterprise and public buyers clear pricing and contractual leverage, forcing suppliers to trade margin for scale and long-term commitments. Public procurement—accounting for roughly 14% of EU GDP—boosts transparency and price comparability, intensifying buyer power. Bechtle’s catalog of public-sector references and compliance certifications lowers switching friction for these customers.

Multi-sourcing and easy switching among integrators

Clients increasingly multi-source, splitting workloads across several system houses, which raises substitutability as comparable vendor certifications proliferate; in 2024 Bechtle reported revenues above EUR 7bn, underscoring scale but not immunity to churn. This dynamic fuels more frequent rebidding and rate pressure, though sticky managed services and proprietary IP bundles help lower churn and protect margins.

Commoditized hardware and licensing

Standard hardware and licensing are highly price-transparent, with 2024 surveys showing over 60% of B2B buyers using online quotes/marketplaces to compare offers. Distribution margins for commoditized hardware typically sit in the 3–7% range, while software resale margins often run 5–15%, forcing expected discounts. Thin margins make value-add services and lifecycle management essential to defend price and protect overall profitability.

Managed services with SLA leverage

- Long-term contracts: lower churn, include penalties/credits

- Buyers demand: outcome-based pricing, flexibility (53% in 2024)

- Renewals: primary negotiation moments

- Defenses: strict KPIs, automation — ~10% fewer concessions

Demand for vertical expertise and compliance

Regulated sectors increasingly demand domain knowledge and certifications such as ISO 27001 and GDPR-aligned processes, reinforced by the 2024 EU NIS2 expansion raising cybersecurity obligations across member states. Where Bechtle provides sector-specific solutions and certified services, buyer power weakens as clients prioritize compliance. Tailored architectures and reference templates raise switching costs and deepen account entrenchment.

- Certification focus: ISO 27001, GDPR, NIS2

- Effect: lower buyer leverage

- Switching costs: tailored architectures

- Entrenchment: reference architectures/templates

Scale eases pressure but churn persists, tenders, outcome SLAs and certifications force discounts

Large buyers use framework contracts, public procurement (~14% EU GDP) and tenders to force discounts; Bechtle’s >EUR 7bn 2024 scale helps but does not eliminate churn. 2024: 53% of buyers demand outcome-based SLAs, hardware margins 3–7%, software resale 5–15%, automation cut concessions ~10%. Certifications (ISO 27001, NIS2) raise switching costs for regulated clients.

| Metric | 2024 Value |

|---|---|

| Bechtle revenue | EUR 7bn+ |

| Public procurement | ~14% EU GDP |

| Buyers preferring outcome SLAs | 53% |

| Hardware margins | 3–7% |

| Software resale margins | 5–15% |

| Automation effect | ~10% fewer concessions |

Preview Before You Purchase

Bechtle Porter's Five Forces Analysis

This Bechtle Porter’s Five Forces analysis provides an in-depth assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, tailored to Bechtle’s IT services and distribution model. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or samples. It’s ready for download and immediate use to inform strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Bechtle faces moderate buyer power and rising competitive intensity from cloud and managed-service players, while supplier leverage is tempered by scale and partnerships; regulatory and tech shifts add both risk and opportunity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bechtle’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on tier-1 OEMs and software giants

Bechtle relies heavily on tier-1 vendors—Microsoft, HPE, Dell, Cisco, VMware—for core hardware, software and licensing; in fiscal 2024 Bechtle reported group revenue of about €8.1bn, so vendor pricing/programs materially affect margins. Partner tiers and rebate schemes can swing gross margins by several percentage points, making supplier concentration a leverage point; diversifying vendors and expanding higher-margin services reduces that dependency.

Hyperscaler program dependency

Azure, AWS and Google Cloud together hold about 66% of the 2024 global cloud infrastructure market (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11%), giving them decisive control over partner margins, incentives and technical roadmaps. Sudden partner program changes have tightened economics for resellers in 2024, so Bechtle must maintain multi-cloud competencies to reduce single-vendor exposure. Strong co-selling alignment with hyperscalers can partially rebalance supplier influence.

Niche software and cybersecurity suppliers

Specialist software and cybersecurity vendors hold differentiated IP with few substitutes, strengthening supplier leverage as the global cybersecurity market exceeded 200 billion USD in 2024. Certification and vendor enablement (Microsoft, Cisco, Palo Alto) create measurable switching costs for Bechtle and its clients through trained personnel and accredited integrations. Suppliers can enforce minimum purchase levels and restrict discounting, while Bechtle dilutes this power by bundling across its hundreds of vendor partnerships and value-added services.

IT distribution and logistics intermediaries

Distributors like ALSO, Ingram Micro and TD Synnex control availability, credit terms and delivery SLAs, and tight component cycles—notably semiconductor constraints since 2020—have increased their leverage over resellers. Bechtle’s EUR 6–7bn+ IT purchasing scale (2024 run-rate) secures better allocations and rebate tiers, while multi-distributor sourcing mitigates single-supplier exposure and SLA risk.

- Major distributors: channel control, inventory leverage

- Bechtle scale: stronger allocations & rebates

- Multi-sourcing: lowers dependency

Skilled talent as a critical supplier

In 2024 certified engineers, architects and security experts remain scarce and mobile, giving them leverage through wage inflation and premium certifications; delivery capacity constraints are pushing project prices and timelines up, while workforce development programs and nearshore hubs are increasingly used to mitigate this supplier power.

- Scarcity: certified specialists retain high mobility

- Compensation: wage inflation strengthens bargaining

- Capacity: delivery limits affect pricing/timelines

- Mitigation: training programs and nearshore hubs

Hyperscaler supplier power strains margins as €8.1bn revenue depends on AWS/Azure/GCP

Bechtle faces strong supplier power from tier-1 vendors and hyperscalers; €8.1bn 2024 revenue makes margins sensitive to partner programs. Hyperscalers hold ~66% cloud IaaS (AWS 32%, Azure 23%, Google 11%), raising dependency; distributors and specialist vendors add leverage, while company scale and multi-sourcing mitigate risk.

| Metric | 2024 |

|---|---|

| Revenue | €8.1bn |

| Cloud share (AWS/Azure/GCP) | 32/23/11% |

| Purchasing run-rate | €6–7bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Bechtle, detailing supplier and buyer power, threat of substitutes, competitive rivalry, and barriers protecting incumbency, with strategic commentary on emerging digital disruptors and margin pressures.

A concise one-sheet Porter's Five Forces for Bechtle that highlights supplier, buyer, rival, entrant and substitute pressures with quantified drivers—ideal for quick strategic decisions and slide-ready presentations.

Customers Bargaining Power

Large enterprise and public sector procurement

Framework contracts, formal tenders and strict SLAs give large enterprise and public buyers clear pricing and contractual leverage, forcing suppliers to trade margin for scale and long-term commitments. Public procurement—accounting for roughly 14% of EU GDP—boosts transparency and price comparability, intensifying buyer power. Bechtle’s catalog of public-sector references and compliance certifications lowers switching friction for these customers.

Multi-sourcing and easy switching among integrators

Clients increasingly multi-source, splitting workloads across several system houses, which raises substitutability as comparable vendor certifications proliferate; in 2024 Bechtle reported revenues above EUR 7bn, underscoring scale but not immunity to churn. This dynamic fuels more frequent rebidding and rate pressure, though sticky managed services and proprietary IP bundles help lower churn and protect margins.

Commoditized hardware and licensing

Standard hardware and licensing are highly price-transparent, with 2024 surveys showing over 60% of B2B buyers using online quotes/marketplaces to compare offers. Distribution margins for commoditized hardware typically sit in the 3–7% range, while software resale margins often run 5–15%, forcing expected discounts. Thin margins make value-add services and lifecycle management essential to defend price and protect overall profitability.

Managed services with SLA leverage

- Long-term contracts: lower churn, include penalties/credits

- Buyers demand: outcome-based pricing, flexibility (53% in 2024)

- Renewals: primary negotiation moments

- Defenses: strict KPIs, automation — ~10% fewer concessions

Demand for vertical expertise and compliance

Regulated sectors increasingly demand domain knowledge and certifications such as ISO 27001 and GDPR-aligned processes, reinforced by the 2024 EU NIS2 expansion raising cybersecurity obligations across member states. Where Bechtle provides sector-specific solutions and certified services, buyer power weakens as clients prioritize compliance. Tailored architectures and reference templates raise switching costs and deepen account entrenchment.

- Certification focus: ISO 27001, GDPR, NIS2

- Effect: lower buyer leverage

- Switching costs: tailored architectures

- Entrenchment: reference architectures/templates

Scale eases pressure but churn persists, tenders, outcome SLAs and certifications force discounts

Large buyers use framework contracts, public procurement (~14% EU GDP) and tenders to force discounts; Bechtle’s >EUR 7bn 2024 scale helps but does not eliminate churn. 2024: 53% of buyers demand outcome-based SLAs, hardware margins 3–7%, software resale 5–15%, automation cut concessions ~10%. Certifications (ISO 27001, NIS2) raise switching costs for regulated clients.

| Metric | 2024 Value |

|---|---|

| Bechtle revenue | EUR 7bn+ |

| Public procurement | ~14% EU GDP |

| Buyers preferring outcome SLAs | 53% |

| Hardware margins | 3–7% |

| Software resale margins | 5–15% |

| Automation effect | ~10% fewer concessions |

Preview Before You Purchase

Bechtle Porter's Five Forces Analysis

This Bechtle Porter’s Five Forces analysis provides an in-depth assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, tailored to Bechtle’s IT services and distribution model. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or samples. It’s ready for download and immediate use to inform strategic or investment decisions.