Beacon Porter's Five Forces Analysis

Don't Miss the Bigger Picture

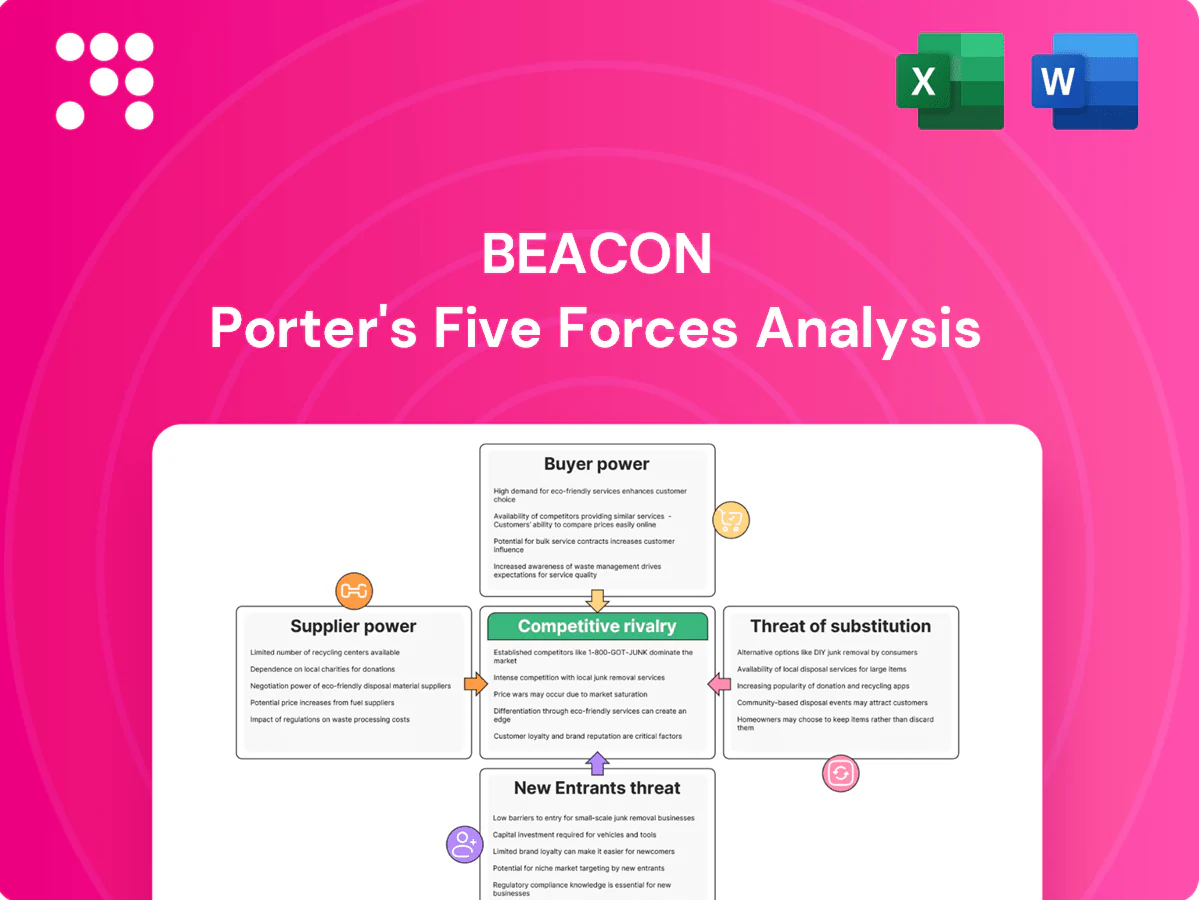

Beacon's Porter’s Five Forces snapshot highlights competitive intensity, buyer and supplier power, and threat vectors shaping margins. This brief overview identifies where Beacon holds advantage and where external pressures could erode value. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Consolidated manufacturers

Roofing and building-materials manufacturing remains moderately consolidated in 2024, giving key suppliers measurable leverage on pricing and allocation for branded shingles, membranes and insulation.

Limited alternative sources for prime SKUs raise dependence, and allocation policies tightened during 2024 demand spikes, pressuring lead times and margins.

Beacon offsets supplier power through multi-sourcing, regional alternative SKUs and scale-based negotiations tied to annual purchase volumes.

Branded product importance

Contractors often specify well-known brands to meet warranty and customer expectations, with a 2024 industry survey reporting 62% of commercial projects listing brand requirements, strengthening supplier bargaining power. Brand pull makes substitution harder despite Beacon’s broad inventory and national distribution that maintains alternative SKUs. Co-marketing and preferred-program agreements can channel 40–55% of volume to select manufacturers, reinforcing stickiness.

Input cost pass-through

In 2024 suppliers passed through volatile inputs such as asphalt, polymers and metals, often within weeks, compressing distributor margins during timing gaps. Beacon’s dynamic pricing and surcharge mechanisms aim to speed pass-through and protect margins. Contractual frameworks and index-linked clauses smooth cashflow impacts but cannot eliminate commodity-driven swings. Rapid input moves still leave short-term margin squeeze for distributors.

Logistics and lead-time dependency

- Supplier proximity: increases bargaining power

- Lead-time variability: raises inventory costs

- Inventory depth: reduces stockout risk

- Regional DCs: improve replenishment speed

Private label and exclusivities

Private-label lines and exclusive territories let Beacon differentiate its assortment and rebalance supplier power; in 2024 private-label accounted for roughly 19% of US retail sales, reducing direct price comparability and supporting higher gross margins. These deals often come with supplier demands for volume commitments or promotional funding, so the optimal mix of national brands and private labels is a key commercial lever for margin and risk management.

- Private-label share ~19% (US, 2024)

- Enhances margin via reduced price comparability

- Suppliers may require volume commitments

- Mix of national vs private label is a strategic lever

Roofing supplier consolidation tightens pricing; distributors use multi-sourcing, private-label

Roofing suppliers remained moderately consolidated in 2024, constraining price and allocation for key SKUs. 62% of commercial projects list brand requirements and private-label was ~19% of US retail sales, strengthening supplier leverage. Beacon offsets power via multi-sourcing, regional DCs, scale-negotiations and private-label programs.

| Metric | 2024 | Implication |

|---|---|---|

| Brand requirements | 62% | Higher stickiness |

| Private-label share | ~19% | Margin relief |

| Co-marketing volume | 40–55% | Concentrated flows |

What is included in the product

Tailored exclusively for Beacon, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with industry data and strategic commentary to inform investor materials, strategy decks, or academic projects.

Beacon Porter's single-sheet Five Forces tool visualizes competitive pressure via an instant spider chart, is fully customizable with no macros, and plugs seamlessly into decks or dashboards to speed strategic decision-making.

Customers Bargaining Power

Professional contractor concentration

Larger roofing contractors and builders buy in high volumes, securing volume discounts of up to 10% and negotiating across multi-branch networks to force price and service concessions. Beacon responds with national-account contracts, tailored payment and logistics terms, and value-added services (credit, inventory management, training). Deep account relationships and consistent on-time delivery reduce pure price bargaining and protect margins.

Price sensitivity and bid culture

End-markets are bid-driven, making customers highly price-focused; in 2024 single-digit margin differences often decide awards. Beacon leverages tiered pricing, rebates and job-based quotes to capture tight spreads and protect margins. Rapid quotes and flexible credit terms (commonly 30–90 days) materially improve win rates, especially on large public and commercial tenders.

Switching costs moderate

Buyers can switch distributors but face hassles around credit re-establishment, delivery reliability, and product availability, which makes switching moderate rather than easy. Warranty requirements and system approvals for specific jobs further constrain moves between suppliers. Beacon’s broad SKU range, on-site delivery and historically low fulfillment error rates increase switching frictions, while digital portals and preserved order history add ongoing stickiness.

Service and logistics as differentiators

Time-sensitive rooftop deliveries with lift equipment and precise staging cut customer labor and installation time, and industry estimates show last-mile can be over 50% of total delivery cost, so service reduces buyer price sensitivity.

Superior service and branch density — Beacon’s fleet availability and local branches — function as bargaining chips, since on-time delivery targets in 2024 hover around 95%.

Missed service windows shift power to buyers via penalty demands and contract leverage, increasing buyer bargaining when SLA compliance falls.

- service-differentiation

- labor-cost-reduction

- branch-density

- penalty-risk

Product availability and credit

Contractors prioritize in-stock breadth and flexible credit to smooth cash cycles; stockouts or tightened credit push them to alternative suppliers, increasing buyer leverage. Beacon’s scale in working capital and deep inventory holdings meaningfully limit that leverage, though seasonal surges and project-driven spikes still test fill rates and credit lines.

- In-stock breadth

- Flexible credit

- Reduced buyer leverage

- Seasonal surge risk

Large contractors secure up to 10% discounts; service, 95% OT and 30–90d credit reduce price pressure

Large contractors secure up to 10% volume discounts; Beacon offsets pressure via national accounts, tailored credit (30–90 days) and 95% on-time delivery (2024), reducing pure price bargaining. Last-mile >50% of delivery cost makes service a key differentiator; switching friction from credit, warranties and broad SKU range keeps buyer power moderate.

| Metric | 2024 Value | Implication |

|---|---|---|

| Volume discount | up to 10% | High buyer leverage |

| On-time delivery | 95% | Reduces price pressure |

| Last-mile cost | >50% | Service-driven stickiness |

| Credit terms | 30–90 days | Win-rate driver |

Preview the Actual Deliverable

Beacon Porter's Five Forces Analysis

This preview displays Beacon Porter's Five Forces Analysis exactly as delivered—no placeholders, edits, or excerpts. The file shown is the full, professionally formatted report you'll receive instantly upon purchase. It's ready for immediate use in decision-making or presentation.

Don't Miss the Bigger Picture

Beacon's Porter’s Five Forces snapshot highlights competitive intensity, buyer and supplier power, and threat vectors shaping margins. This brief overview identifies where Beacon holds advantage and where external pressures could erode value. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Consolidated manufacturers

Roofing and building-materials manufacturing remains moderately consolidated in 2024, giving key suppliers measurable leverage on pricing and allocation for branded shingles, membranes and insulation.

Limited alternative sources for prime SKUs raise dependence, and allocation policies tightened during 2024 demand spikes, pressuring lead times and margins.

Beacon offsets supplier power through multi-sourcing, regional alternative SKUs and scale-based negotiations tied to annual purchase volumes.

Branded product importance

Contractors often specify well-known brands to meet warranty and customer expectations, with a 2024 industry survey reporting 62% of commercial projects listing brand requirements, strengthening supplier bargaining power. Brand pull makes substitution harder despite Beacon’s broad inventory and national distribution that maintains alternative SKUs. Co-marketing and preferred-program agreements can channel 40–55% of volume to select manufacturers, reinforcing stickiness.

Input cost pass-through

In 2024 suppliers passed through volatile inputs such as asphalt, polymers and metals, often within weeks, compressing distributor margins during timing gaps. Beacon’s dynamic pricing and surcharge mechanisms aim to speed pass-through and protect margins. Contractual frameworks and index-linked clauses smooth cashflow impacts but cannot eliminate commodity-driven swings. Rapid input moves still leave short-term margin squeeze for distributors.

Logistics and lead-time dependency

- Supplier proximity: increases bargaining power

- Lead-time variability: raises inventory costs

- Inventory depth: reduces stockout risk

- Regional DCs: improve replenishment speed

Private label and exclusivities

Private-label lines and exclusive territories let Beacon differentiate its assortment and rebalance supplier power; in 2024 private-label accounted for roughly 19% of US retail sales, reducing direct price comparability and supporting higher gross margins. These deals often come with supplier demands for volume commitments or promotional funding, so the optimal mix of national brands and private labels is a key commercial lever for margin and risk management.

- Private-label share ~19% (US, 2024)

- Enhances margin via reduced price comparability

- Suppliers may require volume commitments

- Mix of national vs private label is a strategic lever

Roofing supplier consolidation tightens pricing; distributors use multi-sourcing, private-label

Roofing suppliers remained moderately consolidated in 2024, constraining price and allocation for key SKUs. 62% of commercial projects list brand requirements and private-label was ~19% of US retail sales, strengthening supplier leverage. Beacon offsets power via multi-sourcing, regional DCs, scale-negotiations and private-label programs.

| Metric | 2024 | Implication |

|---|---|---|

| Brand requirements | 62% | Higher stickiness |

| Private-label share | ~19% | Margin relief |

| Co-marketing volume | 40–55% | Concentrated flows |

What is included in the product

Tailored exclusively for Beacon, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with industry data and strategic commentary to inform investor materials, strategy decks, or academic projects.

Beacon Porter's single-sheet Five Forces tool visualizes competitive pressure via an instant spider chart, is fully customizable with no macros, and plugs seamlessly into decks or dashboards to speed strategic decision-making.

Customers Bargaining Power

Professional contractor concentration

Larger roofing contractors and builders buy in high volumes, securing volume discounts of up to 10% and negotiating across multi-branch networks to force price and service concessions. Beacon responds with national-account contracts, tailored payment and logistics terms, and value-added services (credit, inventory management, training). Deep account relationships and consistent on-time delivery reduce pure price bargaining and protect margins.

Price sensitivity and bid culture

End-markets are bid-driven, making customers highly price-focused; in 2024 single-digit margin differences often decide awards. Beacon leverages tiered pricing, rebates and job-based quotes to capture tight spreads and protect margins. Rapid quotes and flexible credit terms (commonly 30–90 days) materially improve win rates, especially on large public and commercial tenders.

Switching costs moderate

Buyers can switch distributors but face hassles around credit re-establishment, delivery reliability, and product availability, which makes switching moderate rather than easy. Warranty requirements and system approvals for specific jobs further constrain moves between suppliers. Beacon’s broad SKU range, on-site delivery and historically low fulfillment error rates increase switching frictions, while digital portals and preserved order history add ongoing stickiness.

Service and logistics as differentiators

Time-sensitive rooftop deliveries with lift equipment and precise staging cut customer labor and installation time, and industry estimates show last-mile can be over 50% of total delivery cost, so service reduces buyer price sensitivity.

Superior service and branch density — Beacon’s fleet availability and local branches — function as bargaining chips, since on-time delivery targets in 2024 hover around 95%.

Missed service windows shift power to buyers via penalty demands and contract leverage, increasing buyer bargaining when SLA compliance falls.

- service-differentiation

- labor-cost-reduction

- branch-density

- penalty-risk

Product availability and credit

Contractors prioritize in-stock breadth and flexible credit to smooth cash cycles; stockouts or tightened credit push them to alternative suppliers, increasing buyer leverage. Beacon’s scale in working capital and deep inventory holdings meaningfully limit that leverage, though seasonal surges and project-driven spikes still test fill rates and credit lines.

- In-stock breadth

- Flexible credit

- Reduced buyer leverage

- Seasonal surge risk

Large contractors secure up to 10% discounts; service, 95% OT and 30–90d credit reduce price pressure

Large contractors secure up to 10% volume discounts; Beacon offsets pressure via national accounts, tailored credit (30–90 days) and 95% on-time delivery (2024), reducing pure price bargaining. Last-mile >50% of delivery cost makes service a key differentiator; switching friction from credit, warranties and broad SKU range keeps buyer power moderate.

| Metric | 2024 Value | Implication |

|---|---|---|

| Volume discount | up to 10% | High buyer leverage |

| On-time delivery | 95% | Reduces price pressure |

| Last-mile cost | >50% | Service-driven stickiness |

| Credit terms | 30–90 days | Win-rate driver |

Preview the Actual Deliverable

Beacon Porter's Five Forces Analysis

This preview displays Beacon Porter's Five Forces Analysis exactly as delivered—no placeholders, edits, or excerpts. The file shown is the full, professionally formatted report you'll receive instantly upon purchase. It's ready for immediate use in decision-making or presentation.

Description

Don't Miss the Bigger Picture

Beacon's Porter’s Five Forces snapshot highlights competitive intensity, buyer and supplier power, and threat vectors shaping margins. This brief overview identifies where Beacon holds advantage and where external pressures could erode value. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Consolidated manufacturers

Roofing and building-materials manufacturing remains moderately consolidated in 2024, giving key suppliers measurable leverage on pricing and allocation for branded shingles, membranes and insulation.

Limited alternative sources for prime SKUs raise dependence, and allocation policies tightened during 2024 demand spikes, pressuring lead times and margins.

Beacon offsets supplier power through multi-sourcing, regional alternative SKUs and scale-based negotiations tied to annual purchase volumes.

Branded product importance

Contractors often specify well-known brands to meet warranty and customer expectations, with a 2024 industry survey reporting 62% of commercial projects listing brand requirements, strengthening supplier bargaining power. Brand pull makes substitution harder despite Beacon’s broad inventory and national distribution that maintains alternative SKUs. Co-marketing and preferred-program agreements can channel 40–55% of volume to select manufacturers, reinforcing stickiness.

Input cost pass-through

In 2024 suppliers passed through volatile inputs such as asphalt, polymers and metals, often within weeks, compressing distributor margins during timing gaps. Beacon’s dynamic pricing and surcharge mechanisms aim to speed pass-through and protect margins. Contractual frameworks and index-linked clauses smooth cashflow impacts but cannot eliminate commodity-driven swings. Rapid input moves still leave short-term margin squeeze for distributors.

Logistics and lead-time dependency

- Supplier proximity: increases bargaining power

- Lead-time variability: raises inventory costs

- Inventory depth: reduces stockout risk

- Regional DCs: improve replenishment speed

Private label and exclusivities

Private-label lines and exclusive territories let Beacon differentiate its assortment and rebalance supplier power; in 2024 private-label accounted for roughly 19% of US retail sales, reducing direct price comparability and supporting higher gross margins. These deals often come with supplier demands for volume commitments or promotional funding, so the optimal mix of national brands and private labels is a key commercial lever for margin and risk management.

- Private-label share ~19% (US, 2024)

- Enhances margin via reduced price comparability

- Suppliers may require volume commitments

- Mix of national vs private label is a strategic lever

Roofing supplier consolidation tightens pricing; distributors use multi-sourcing, private-label

Roofing suppliers remained moderately consolidated in 2024, constraining price and allocation for key SKUs. 62% of commercial projects list brand requirements and private-label was ~19% of US retail sales, strengthening supplier leverage. Beacon offsets power via multi-sourcing, regional DCs, scale-negotiations and private-label programs.

| Metric | 2024 | Implication |

|---|---|---|

| Brand requirements | 62% | Higher stickiness |

| Private-label share | ~19% | Margin relief |

| Co-marketing volume | 40–55% | Concentrated flows |

What is included in the product

Tailored exclusively for Beacon, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with industry data and strategic commentary to inform investor materials, strategy decks, or academic projects.

Beacon Porter's single-sheet Five Forces tool visualizes competitive pressure via an instant spider chart, is fully customizable with no macros, and plugs seamlessly into decks or dashboards to speed strategic decision-making.

Customers Bargaining Power

Professional contractor concentration

Larger roofing contractors and builders buy in high volumes, securing volume discounts of up to 10% and negotiating across multi-branch networks to force price and service concessions. Beacon responds with national-account contracts, tailored payment and logistics terms, and value-added services (credit, inventory management, training). Deep account relationships and consistent on-time delivery reduce pure price bargaining and protect margins.

Price sensitivity and bid culture

End-markets are bid-driven, making customers highly price-focused; in 2024 single-digit margin differences often decide awards. Beacon leverages tiered pricing, rebates and job-based quotes to capture tight spreads and protect margins. Rapid quotes and flexible credit terms (commonly 30–90 days) materially improve win rates, especially on large public and commercial tenders.

Switching costs moderate

Buyers can switch distributors but face hassles around credit re-establishment, delivery reliability, and product availability, which makes switching moderate rather than easy. Warranty requirements and system approvals for specific jobs further constrain moves between suppliers. Beacon’s broad SKU range, on-site delivery and historically low fulfillment error rates increase switching frictions, while digital portals and preserved order history add ongoing stickiness.

Service and logistics as differentiators

Time-sensitive rooftop deliveries with lift equipment and precise staging cut customer labor and installation time, and industry estimates show last-mile can be over 50% of total delivery cost, so service reduces buyer price sensitivity.

Superior service and branch density — Beacon’s fleet availability and local branches — function as bargaining chips, since on-time delivery targets in 2024 hover around 95%.

Missed service windows shift power to buyers via penalty demands and contract leverage, increasing buyer bargaining when SLA compliance falls.

- service-differentiation

- labor-cost-reduction

- branch-density

- penalty-risk

Product availability and credit

Contractors prioritize in-stock breadth and flexible credit to smooth cash cycles; stockouts or tightened credit push them to alternative suppliers, increasing buyer leverage. Beacon’s scale in working capital and deep inventory holdings meaningfully limit that leverage, though seasonal surges and project-driven spikes still test fill rates and credit lines.

- In-stock breadth

- Flexible credit

- Reduced buyer leverage

- Seasonal surge risk

Large contractors secure up to 10% discounts; service, 95% OT and 30–90d credit reduce price pressure

Large contractors secure up to 10% volume discounts; Beacon offsets pressure via national accounts, tailored credit (30–90 days) and 95% on-time delivery (2024), reducing pure price bargaining. Last-mile >50% of delivery cost makes service a key differentiator; switching friction from credit, warranties and broad SKU range keeps buyer power moderate.

| Metric | 2024 Value | Implication |

|---|---|---|

| Volume discount | up to 10% | High buyer leverage |

| On-time delivery | 95% | Reduces price pressure |

| Last-mile cost | >50% | Service-driven stickiness |

| Credit terms | 30–90 days | Win-rate driver |

Preview the Actual Deliverable

Beacon Porter's Five Forces Analysis

This preview displays Beacon Porter's Five Forces Analysis exactly as delivered—no placeholders, edits, or excerpts. The file shown is the full, professionally formatted report you'll receive instantly upon purchase. It's ready for immediate use in decision-making or presentation.