Beingmate SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Beingmate’s SWOT highlights a strong brand presence and distribution network but flags supply-chain risks and competitive pressure in the infant-nutrition market. Our full SWOT uncovers revenue sensitivities, regulatory exposures, and strategic levers to drive recovery and growth. Purchase the complete, editable Word + Excel report for research-backed insights and actionable strategy you can present or implement immediately.

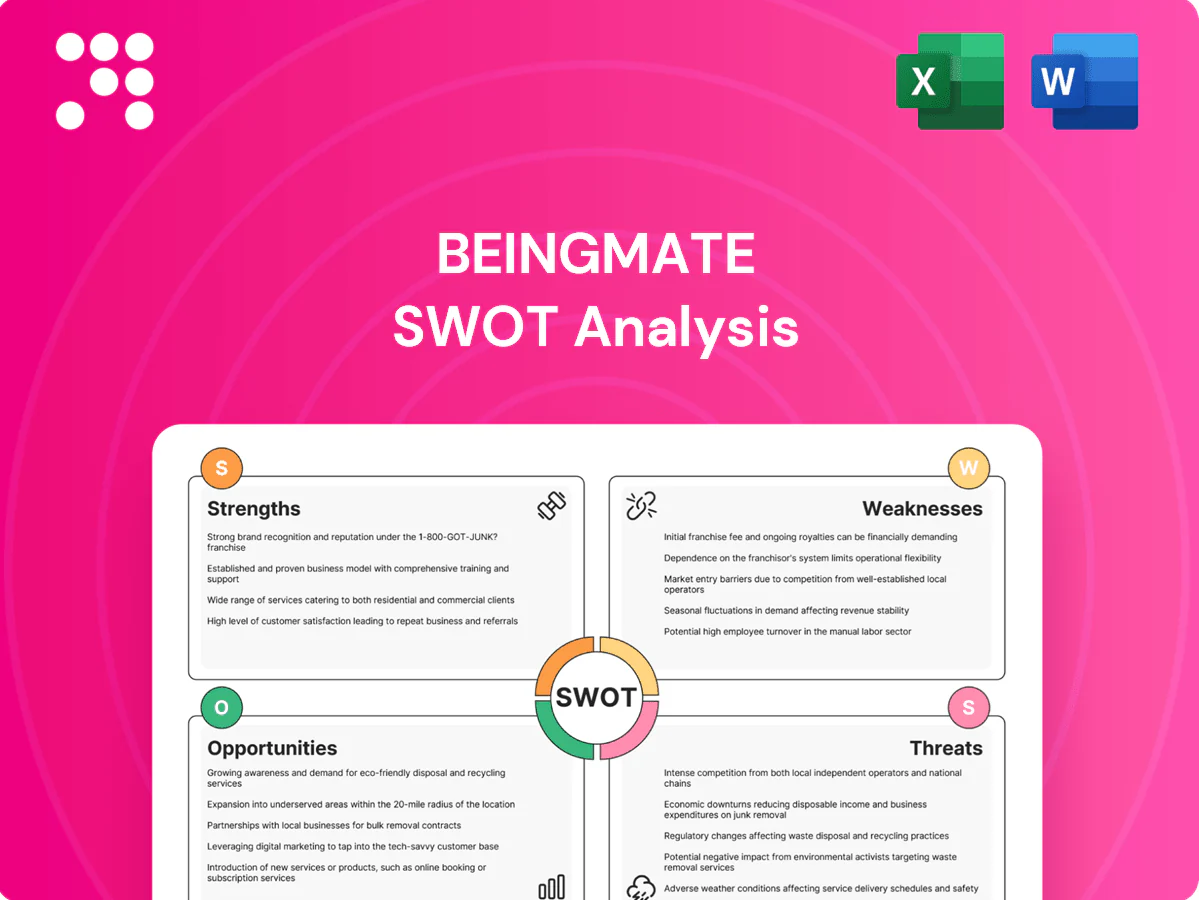

Strengths

Established infant nutrition brand

Beingmate, founded in 1992, leverages a recognized presence in China’s infant nutrition market—valued at over RMB 200 billion in 2023 with roughly 9.56 million births that year—to sustain consumer trust and repeat purchases. Brand familiarity eases rollout of line extensions and premium SKUs, while longstanding market knowledge sharpens caregiver messaging and creates a high barrier to smaller newcomers.

Diverse product portfolio

Beingmate offers infant formula and complementary foods with multi-stage formulations (stages 1–4), enabling cross-selling and customer retention across the full infant lifecycle. The breadth across formula and complementary nutrition smooths revenue volatility from any single category and supports tailored SKUs across premium-to-value tiers. This diversified portfolio also facilitates channel-specific bundles and pricing strategies to boost shopper lifetime value.

Nationwide distribution reach

Beingmate’s multi-channel coverage across mother-baby stores, pharmacies, supermarkets and e-commerce (Tmall, JD) increases product accessibility and visibility. Broad national reach drives scale efficiencies in logistics and marketing and helps lower per-unit costs. Presence in lower-tier cities expands the addressable market amid China’s 9.56 million births in 2023. This diversified mix reduces dependence on any single channel.

R&D and quality focus

Beingmate’s in-house R&D drives formulation improvements and helps meet evolving Chinese standards, strengthening compliance in a tightly regulated infant-nutrition market. A strong quality focus is essential in this safety-sensitive category and supports brand trust. R&D also enables differentiation through functional ingredients and faster responses to regulatory and scientific shifts.

- R&D-backed compliance

- Quality = brand trust

- Functional-ingredient differentiation

- Quicker regulatory response

Supply-chain integration potential

Beingmate, founded 1992, can use supply-chain integration to tighten control over sourcing, processing and manufacturing, stabilizing product quality and margins. Integration lowers exposure to supplier disruptions and supports full traceability that parents increasingly demand. Consolidated procurement at scale improves cost competitiveness and bargaining power.

1992-founded leader taps RMB200bn market, 9.56m births

Beingmate, founded 1992, leverages strong brand in China infant nutrition market >RMB200bn (2023) and 9.56m births, supporting repeat purchase and premium SKUs. Multi-stage formulas and complementary foods enable lifecycle cross-selling and revenue smoothing. Multi-channel reach (Tmall, JD, mom-and-baby stores) plus in-house R&D and integrated supply chain boost quality, compliance and margins.

| Metric | Value |

|---|---|

| Founded | 1992 |

| Market size (2023) | >RMB200bn |

| Births (2023) | 9.56m |

| Channels | Tmall, JD, retail |

| R&D | In-house |

What is included in the product

Provides a concise SWOT analysis of Beingmate, outlining internal strengths and weaknesses and external opportunities and threats to map its competitive position and strategic risks.

Provides a concise SWOT matrix for fast, visual strategy alignment, relieving analysis bottlenecks for cross-functional teams. Editable format enables quick updates as priorities shift, making it easy to integrate into reports and presentations.

Weaknesses

Intense domestic and foreign competition

Beingmate faces stiff competition from leading domestic dairy groups Yili, Mengniu and Feihe and global brands Nestle, Danone and Abbott in China’s infant-formula market, which exceeds RMB 100 billion.

Escalating marketing spend and price/promotional wars compress margins as retailers and e-commerce platforms fight for share. Online channels now represent over 40% of sales, making traffic and shelf space costly to secure.

Strict product regulations and formula recipes limit meaningful differentiation, squeezing premiumization strategies and R&D levers.

Brand recovery challenges

Past performance volatility erodes caregiver confidence versus incumbents, with studies showing trust-driven purchases dominate the RMB 200bn+ China infant-formula market (2023). Rebuilding trust typically requires 3–5 years of sustained quality proof points and endorsements. Negative legacy perceptions raise CAC—new-customer costs can be 5–25× higher than retention, inflating marketing spend.

Product mix concentration in formula

Beingmate derives the majority of its revenue from infant formula, leaving top-line exposed to birth-rate cycles—China recorded about 9.56 million births in 2023—plus tightening regulation in the dairy and baby-food sector. Complementary foods and snacks remain smaller contributors, so limited product diversification heightens revenue sensitivity to demographic and policy shocks. This concentration constrains risk-sharing across categories and increases volatility in annual sales.

Channel execution variability

Disparate distributor capabilities create uneven in-store presence and service, reducing shelf share in key mother-baby chains; execution gaps have been linked to conversion drops in categories where in-store conversion often outperforms online. E-commerce algorithms and promotions squeeze margins, with promotional discounting commonly exceeding 20% on major platforms. Omnichannel inventory alignment remains complex, raising stock-out and overstock risk.

Cost structure pressure

Beingmate faces cost-structure pressure as volatile milk powder, whey and specialty-ingredient markets—with commodity swings reaching up to 30% in 2022–2024—directly inflate COGS and compress margins. Mandatory compliance, expanded testing and traceability systems add recurring fixed costs that scale poorly. Smaller scale versus national leaders weakens bargaining power and narrows room for price promotions, limiting margin flexibility.

- Ingredient swings: up to 30% (2022–2024)

- Higher fixed compliance/testing costs

- Smaller scale = lower bargaining power

- Limited promotional leeway, tighter margins

Infant-formula supplier squeezed by giants — online >40%, input costs up to 30%

Beingmate is squeezed by dominant rivals (Yili, Mengniu, Feihe, Nestle) in a RMB 200bn+ infant-formula market, with online channels >40% raising traffic costs and promotional discounts ~20%+. Volatile ingredient costs (up to 30% 2022–24) and rising compliance/testing lift fixed COGS, while heavy revenue concentration in formula amplifies risk amid China’s 9.56M births (2023).

| Metric | Value |

|---|---|

| Market size (infant formula) | RMB 200bn+ |

| Online share | >40% |

| Births (2023) | 9.56M |

| Ingredient volatility | up to 30% (2022–24) |

| Promo depth | ~20%+ |

Preview the Actual Deliverable

Beingmate SWOT Analysis

This is the actual Beingmate SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, so what you see is what you'll download after payment. Purchase unlocks the complete, editable version with full detail and structured findings.

Make Insightful Decisions Backed by Expert Research

Beingmate’s SWOT highlights a strong brand presence and distribution network but flags supply-chain risks and competitive pressure in the infant-nutrition market. Our full SWOT uncovers revenue sensitivities, regulatory exposures, and strategic levers to drive recovery and growth. Purchase the complete, editable Word + Excel report for research-backed insights and actionable strategy you can present or implement immediately.

Strengths

Established infant nutrition brand

Beingmate, founded in 1992, leverages a recognized presence in China’s infant nutrition market—valued at over RMB 200 billion in 2023 with roughly 9.56 million births that year—to sustain consumer trust and repeat purchases. Brand familiarity eases rollout of line extensions and premium SKUs, while longstanding market knowledge sharpens caregiver messaging and creates a high barrier to smaller newcomers.

Diverse product portfolio

Beingmate offers infant formula and complementary foods with multi-stage formulations (stages 1–4), enabling cross-selling and customer retention across the full infant lifecycle. The breadth across formula and complementary nutrition smooths revenue volatility from any single category and supports tailored SKUs across premium-to-value tiers. This diversified portfolio also facilitates channel-specific bundles and pricing strategies to boost shopper lifetime value.

Nationwide distribution reach

Beingmate’s multi-channel coverage across mother-baby stores, pharmacies, supermarkets and e-commerce (Tmall, JD) increases product accessibility and visibility. Broad national reach drives scale efficiencies in logistics and marketing and helps lower per-unit costs. Presence in lower-tier cities expands the addressable market amid China’s 9.56 million births in 2023. This diversified mix reduces dependence on any single channel.

R&D and quality focus

Beingmate’s in-house R&D drives formulation improvements and helps meet evolving Chinese standards, strengthening compliance in a tightly regulated infant-nutrition market. A strong quality focus is essential in this safety-sensitive category and supports brand trust. R&D also enables differentiation through functional ingredients and faster responses to regulatory and scientific shifts.

- R&D-backed compliance

- Quality = brand trust

- Functional-ingredient differentiation

- Quicker regulatory response

Supply-chain integration potential

Beingmate, founded 1992, can use supply-chain integration to tighten control over sourcing, processing and manufacturing, stabilizing product quality and margins. Integration lowers exposure to supplier disruptions and supports full traceability that parents increasingly demand. Consolidated procurement at scale improves cost competitiveness and bargaining power.

1992-founded leader taps RMB200bn market, 9.56m births

Beingmate, founded 1992, leverages strong brand in China infant nutrition market >RMB200bn (2023) and 9.56m births, supporting repeat purchase and premium SKUs. Multi-stage formulas and complementary foods enable lifecycle cross-selling and revenue smoothing. Multi-channel reach (Tmall, JD, mom-and-baby stores) plus in-house R&D and integrated supply chain boost quality, compliance and margins.

| Metric | Value |

|---|---|

| Founded | 1992 |

| Market size (2023) | >RMB200bn |

| Births (2023) | 9.56m |

| Channels | Tmall, JD, retail |

| R&D | In-house |

What is included in the product

Provides a concise SWOT analysis of Beingmate, outlining internal strengths and weaknesses and external opportunities and threats to map its competitive position and strategic risks.

Provides a concise SWOT matrix for fast, visual strategy alignment, relieving analysis bottlenecks for cross-functional teams. Editable format enables quick updates as priorities shift, making it easy to integrate into reports and presentations.

Weaknesses

Intense domestic and foreign competition

Beingmate faces stiff competition from leading domestic dairy groups Yili, Mengniu and Feihe and global brands Nestle, Danone and Abbott in China’s infant-formula market, which exceeds RMB 100 billion.

Escalating marketing spend and price/promotional wars compress margins as retailers and e-commerce platforms fight for share. Online channels now represent over 40% of sales, making traffic and shelf space costly to secure.

Strict product regulations and formula recipes limit meaningful differentiation, squeezing premiumization strategies and R&D levers.

Brand recovery challenges

Past performance volatility erodes caregiver confidence versus incumbents, with studies showing trust-driven purchases dominate the RMB 200bn+ China infant-formula market (2023). Rebuilding trust typically requires 3–5 years of sustained quality proof points and endorsements. Negative legacy perceptions raise CAC—new-customer costs can be 5–25× higher than retention, inflating marketing spend.

Product mix concentration in formula

Beingmate derives the majority of its revenue from infant formula, leaving top-line exposed to birth-rate cycles—China recorded about 9.56 million births in 2023—plus tightening regulation in the dairy and baby-food sector. Complementary foods and snacks remain smaller contributors, so limited product diversification heightens revenue sensitivity to demographic and policy shocks. This concentration constrains risk-sharing across categories and increases volatility in annual sales.

Channel execution variability

Disparate distributor capabilities create uneven in-store presence and service, reducing shelf share in key mother-baby chains; execution gaps have been linked to conversion drops in categories where in-store conversion often outperforms online. E-commerce algorithms and promotions squeeze margins, with promotional discounting commonly exceeding 20% on major platforms. Omnichannel inventory alignment remains complex, raising stock-out and overstock risk.

Cost structure pressure

Beingmate faces cost-structure pressure as volatile milk powder, whey and specialty-ingredient markets—with commodity swings reaching up to 30% in 2022–2024—directly inflate COGS and compress margins. Mandatory compliance, expanded testing and traceability systems add recurring fixed costs that scale poorly. Smaller scale versus national leaders weakens bargaining power and narrows room for price promotions, limiting margin flexibility.

- Ingredient swings: up to 30% (2022–2024)

- Higher fixed compliance/testing costs

- Smaller scale = lower bargaining power

- Limited promotional leeway, tighter margins

Infant-formula supplier squeezed by giants — online >40%, input costs up to 30%

Beingmate is squeezed by dominant rivals (Yili, Mengniu, Feihe, Nestle) in a RMB 200bn+ infant-formula market, with online channels >40% raising traffic costs and promotional discounts ~20%+. Volatile ingredient costs (up to 30% 2022–24) and rising compliance/testing lift fixed COGS, while heavy revenue concentration in formula amplifies risk amid China’s 9.56M births (2023).

| Metric | Value |

|---|---|

| Market size (infant formula) | RMB 200bn+ |

| Online share | >40% |

| Births (2023) | 9.56M |

| Ingredient volatility | up to 30% (2022–24) |

| Promo depth | ~20%+ |

Preview the Actual Deliverable

Beingmate SWOT Analysis

This is the actual Beingmate SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, so what you see is what you'll download after payment. Purchase unlocks the complete, editable version with full detail and structured findings.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Beingmate’s SWOT highlights a strong brand presence and distribution network but flags supply-chain risks and competitive pressure in the infant-nutrition market. Our full SWOT uncovers revenue sensitivities, regulatory exposures, and strategic levers to drive recovery and growth. Purchase the complete, editable Word + Excel report for research-backed insights and actionable strategy you can present or implement immediately.

Strengths

Established infant nutrition brand

Beingmate, founded in 1992, leverages a recognized presence in China’s infant nutrition market—valued at over RMB 200 billion in 2023 with roughly 9.56 million births that year—to sustain consumer trust and repeat purchases. Brand familiarity eases rollout of line extensions and premium SKUs, while longstanding market knowledge sharpens caregiver messaging and creates a high barrier to smaller newcomers.

Diverse product portfolio

Beingmate offers infant formula and complementary foods with multi-stage formulations (stages 1–4), enabling cross-selling and customer retention across the full infant lifecycle. The breadth across formula and complementary nutrition smooths revenue volatility from any single category and supports tailored SKUs across premium-to-value tiers. This diversified portfolio also facilitates channel-specific bundles and pricing strategies to boost shopper lifetime value.

Nationwide distribution reach

Beingmate’s multi-channel coverage across mother-baby stores, pharmacies, supermarkets and e-commerce (Tmall, JD) increases product accessibility and visibility. Broad national reach drives scale efficiencies in logistics and marketing and helps lower per-unit costs. Presence in lower-tier cities expands the addressable market amid China’s 9.56 million births in 2023. This diversified mix reduces dependence on any single channel.

R&D and quality focus

Beingmate’s in-house R&D drives formulation improvements and helps meet evolving Chinese standards, strengthening compliance in a tightly regulated infant-nutrition market. A strong quality focus is essential in this safety-sensitive category and supports brand trust. R&D also enables differentiation through functional ingredients and faster responses to regulatory and scientific shifts.

- R&D-backed compliance

- Quality = brand trust

- Functional-ingredient differentiation

- Quicker regulatory response

Supply-chain integration potential

Beingmate, founded 1992, can use supply-chain integration to tighten control over sourcing, processing and manufacturing, stabilizing product quality and margins. Integration lowers exposure to supplier disruptions and supports full traceability that parents increasingly demand. Consolidated procurement at scale improves cost competitiveness and bargaining power.

1992-founded leader taps RMB200bn market, 9.56m births

Beingmate, founded 1992, leverages strong brand in China infant nutrition market >RMB200bn (2023) and 9.56m births, supporting repeat purchase and premium SKUs. Multi-stage formulas and complementary foods enable lifecycle cross-selling and revenue smoothing. Multi-channel reach (Tmall, JD, mom-and-baby stores) plus in-house R&D and integrated supply chain boost quality, compliance and margins.

| Metric | Value |

|---|---|

| Founded | 1992 |

| Market size (2023) | >RMB200bn |

| Births (2023) | 9.56m |

| Channels | Tmall, JD, retail |

| R&D | In-house |

What is included in the product

Provides a concise SWOT analysis of Beingmate, outlining internal strengths and weaknesses and external opportunities and threats to map its competitive position and strategic risks.

Provides a concise SWOT matrix for fast, visual strategy alignment, relieving analysis bottlenecks for cross-functional teams. Editable format enables quick updates as priorities shift, making it easy to integrate into reports and presentations.

Weaknesses

Intense domestic and foreign competition

Beingmate faces stiff competition from leading domestic dairy groups Yili, Mengniu and Feihe and global brands Nestle, Danone and Abbott in China’s infant-formula market, which exceeds RMB 100 billion.

Escalating marketing spend and price/promotional wars compress margins as retailers and e-commerce platforms fight for share. Online channels now represent over 40% of sales, making traffic and shelf space costly to secure.

Strict product regulations and formula recipes limit meaningful differentiation, squeezing premiumization strategies and R&D levers.

Brand recovery challenges

Past performance volatility erodes caregiver confidence versus incumbents, with studies showing trust-driven purchases dominate the RMB 200bn+ China infant-formula market (2023). Rebuilding trust typically requires 3–5 years of sustained quality proof points and endorsements. Negative legacy perceptions raise CAC—new-customer costs can be 5–25× higher than retention, inflating marketing spend.

Product mix concentration in formula

Beingmate derives the majority of its revenue from infant formula, leaving top-line exposed to birth-rate cycles—China recorded about 9.56 million births in 2023—plus tightening regulation in the dairy and baby-food sector. Complementary foods and snacks remain smaller contributors, so limited product diversification heightens revenue sensitivity to demographic and policy shocks. This concentration constrains risk-sharing across categories and increases volatility in annual sales.

Channel execution variability

Disparate distributor capabilities create uneven in-store presence and service, reducing shelf share in key mother-baby chains; execution gaps have been linked to conversion drops in categories where in-store conversion often outperforms online. E-commerce algorithms and promotions squeeze margins, with promotional discounting commonly exceeding 20% on major platforms. Omnichannel inventory alignment remains complex, raising stock-out and overstock risk.

Cost structure pressure

Beingmate faces cost-structure pressure as volatile milk powder, whey and specialty-ingredient markets—with commodity swings reaching up to 30% in 2022–2024—directly inflate COGS and compress margins. Mandatory compliance, expanded testing and traceability systems add recurring fixed costs that scale poorly. Smaller scale versus national leaders weakens bargaining power and narrows room for price promotions, limiting margin flexibility.

- Ingredient swings: up to 30% (2022–2024)

- Higher fixed compliance/testing costs

- Smaller scale = lower bargaining power

- Limited promotional leeway, tighter margins

Infant-formula supplier squeezed by giants — online >40%, input costs up to 30%

Beingmate is squeezed by dominant rivals (Yili, Mengniu, Feihe, Nestle) in a RMB 200bn+ infant-formula market, with online channels >40% raising traffic costs and promotional discounts ~20%+. Volatile ingredient costs (up to 30% 2022–24) and rising compliance/testing lift fixed COGS, while heavy revenue concentration in formula amplifies risk amid China’s 9.56M births (2023).

| Metric | Value |

|---|---|

| Market size (infant formula) | RMB 200bn+ |

| Online share | >40% |

| Births (2023) | 9.56M |

| Ingredient volatility | up to 30% (2022–24) |

| Promo depth | ~20%+ |

Preview the Actual Deliverable

Beingmate SWOT Analysis

This is the actual Beingmate SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, so what you see is what you'll download after payment. Purchase unlocks the complete, editable version with full detail and structured findings.