Bekaert Handling Group A/S PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of Bekaert Handling Group A/S reveals how political shifts, macroeconomic cycles, and rapid tech innovation shape its strategic risks and opportunities. Packed with actionable insights, this briefing helps investors and strategists anticipate regulatory, social, and environmental impacts. Purchase the full analysis to access the complete, fully editable report and make smarter decisions today.

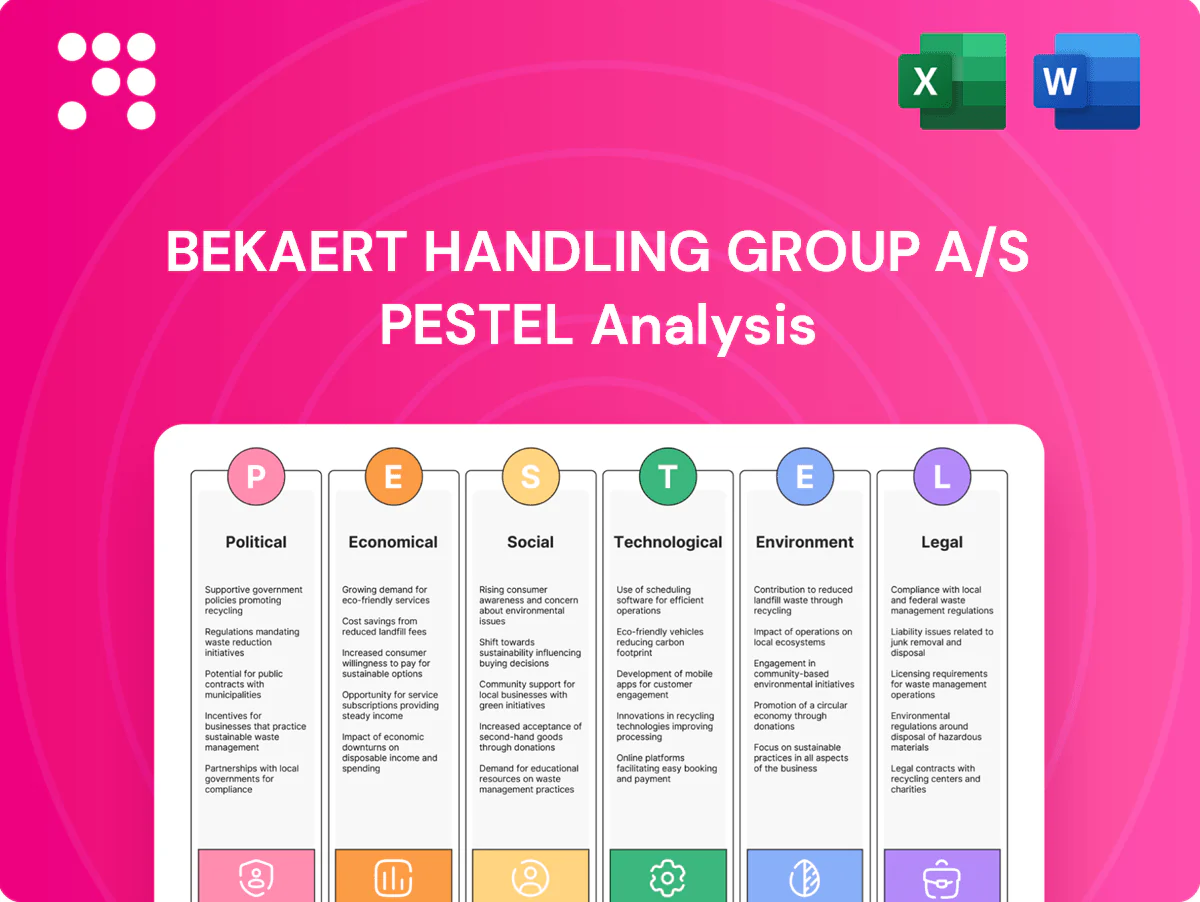

Political factors

EU trade policy

EU Single Market of 27 states guarantees tariff-free movement across the bloc, shaping sourcing and cross-border exports for Bekaert Handling Group A/S. EU–US two‑way trade in goods and services was roughly €1 trillion in 2023, while goods trade with China was around €760 billion, meaning shifts in relations alter landed polymer, fabric and component costs. Monitoring anti-dumping measures in industrial textiles and steel remains essential, and active engagement with trade bodies helps anticipate rule changes.

Industrial subsidies

National and EU incentives — notably Horizon Europe (€95.5bn 2021–27) and the Recovery and Resilience Facility (RRF, €723.8bn) — can materially reduce Bekaert Handling Group A/S capex for automation and green tech projects. Competing jurisdictions offering local subsidies may alter plant-location economics and ROI. Timely applications unlock grants for energy-efficiency upgrades and R&D, while policy reversals can disrupt long-term investment plans.

Geopolitical logistics

Conflicts and sanctions have disrupted sea lanes, driving war-risk premiums in hotspots like the Red Sea up over 200% in 2023–24 and lengthening lead times by several days. Routing via stable corridors can cut disruption risk for containerized shipments. Diversified suppliers in friendly jurisdictions improve resilience. Expanded US/EU export controls since 2023 restrict certain dual-use technologies, affecting transfers.

Standards harmonization

Alignment of packaging and handling standards across the 27‑country European Single Market lowers compliance friction and cross‑border testing; ISO reports over 24,000 International Standards (2024), reducing multiplicity of national specs. Divergent national rules raise testing and certification costs and time to market. Participation in standards committees lets Bekaert Handling influence practical requirements, while early compliance signals stronger tender competitiveness.

- Standards scale: ISO >24,000 (2024)

- EU market: 27 countries—reduces cross‑border friction

- Committee participation: shapes requirements

- Early compliance: competitive tender signal

Public procurement

Public procurement cycles drive demand for handling equipment—EU public procurement represented about 14% of GDP in recent years and global public tendering often tracks government capex, so SOE and infrastructure tenders materially affect order timing and volume. Local content rules (eg India/local preference policies) can force higher domestic sourcing or assembly, altering margins and supply chains. Transparent, audited bidding favors certified, safety-led suppliers and political shifts can quickly reallocate budgets across transport, energy or industrial projects.

- Procurement share: EU ~14% of GDP

- Local content: procurement preferences (eg India) reshape sourcing

- Compliance edge: certification and safety improve tender win-rate

- Political risk: sector reprioritization alters capex flows

EU market €1.0tn; funds lower capex; Red Sea risk > 200%

EU Single Market (27 states) eases cross‑border trade; EU–US goods/services two‑way ≈€1.0tn (2023) and EU–China goods ≈€760bn (2023), so geopolitical shifts affect component costs. Horizon Europe (€95.5bn 2021–27) and RRF (€723.8bn) cut capex for automation/green projects; EU public procurement ≈14% GDP. Red Sea war‑risk premiums rose >200% in 2023–24, extending lead times.

| Indicator | Value |

|---|---|

| EU states | 27 |

| Horizon Europe | €95.5bn (2021–27) |

| RRF | €723.8bn |

| EU–US trade (2023) | €1.0tn |

| War‑risk premium Red Sea | +>200% (2023–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bekaert Handling Group A/S across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking implications to help executives, consultants and investors identify risks, opportunities and strategic responses.

A clean, summarized PESTLE of Bekaert Handling Group A/S, visually segmented and editable, streamlines meetings and presentations, supports external risk and market-positioning discussions, and is easily shareable or dropped into slides for quick team alignment.

Economic factors

Industrial cycle

Industrial cycles drive Bekaert Handling demand: capital goods sales closely follow S&P Global manufacturing PMI, which hovered around 50 in 2024, and corporate capex trends; IMF projected global GDP growth of 3.2% in 2024 and 3.0% in 2025, shifting volumes in chemicals, agriculture and e-commerce. Backlog accumulation in upswings stabilizes utilization, while flexible cost structures (variable labor, outsourced logistics) have cushioned recent downturns.

Input inflation

Input inflation from resin, technical textile and steel price volatility compresses margins across Bekaert Handling Group, forcing tighter cost pass-through. Indexed pricing and forward-hedging programs have smoothed reported COGS swings. Dual-sourcing strategies limit single-supplier disruptions. Strict inventory discipline lowers holding losses when input deflation occurs.

FX exposure

Multi-currency sales and imports create translation and transaction risk for Bekaert Handling Group A/S, with global FX markets averaging about USD 7.5 trillion daily turnover (BIS Apr 2022) increasing exposure. Natural hedging by matching costs and revenues reduces net risk, while forwards and options lock quote validity. Sudden FX swings can reprice export competitiveness overnight.

Freight and energy

- Ocean rates: -70% from 2021 peak (to 2023)

- Energy tariff trigger: >0.15–0.20 USD/kWh for faster payback

- Nearshoring: reduces transit uncertainty and demurrage exposure

- Customer tolerance: surcharges acceptable if SLAs intact

Rates and credit

Higher interest rates (ECB deposit ~4%, US Fed funds 5.25–5.50% in 2024–2025) raise WACC and leasing costs for automation, prompting customers to defer upgrades and stretch sales cycles. Vendor financing and service-based models have protected order intake, while strong balance sheets secure better terms with lenders.

- Higher rates: WACC up

- Leasing cost rise

- Deferred upgrades

- Vendor finance shields orders

- Strong balance sheet = better lender terms

EU market €1.0tn; funds lower capex; Red Sea risk > 200%

Industrial cycles and IMF 2024–25 growth (3.2% / 3.0%) drive demand; backlog cushions upswings while flexible cost bases limit downside. Input volatility (resin/steel) and ocean rate swings (‑70% from 2021 peak to 2023) compress margins; indexed pricing and hedges mitigate. Higher rates (US Fed 5.25–5.50%, ECB dep ~4%) raise WACC, slowing capex; vendor finance and strong balance sheets support orders.

| Metric | Value |

|---|---|

| Global GDP growth 2024/25 (IMF) | 3.2% / 3.0% |

| US Fed funds | 5.25–5.50% |

| ECB deposit | ~4% |

| Ocean rates change (peak→2023) | ‑70% |

| FX daily turnover (BIS Apr 2022) | USD 7.5tn |

Full Version Awaits

Bekaert Handling Group A/S PESTLE Analysis

The preview shown here is the exact Bekaert Handling Group A/S PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure and layout you see are the final version with no placeholders or teasers. After payment you’ll instantly download this exact file, complete and professionally structured for immediate use.

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of Bekaert Handling Group A/S reveals how political shifts, macroeconomic cycles, and rapid tech innovation shape its strategic risks and opportunities. Packed with actionable insights, this briefing helps investors and strategists anticipate regulatory, social, and environmental impacts. Purchase the full analysis to access the complete, fully editable report and make smarter decisions today.

Political factors

EU trade policy

EU Single Market of 27 states guarantees tariff-free movement across the bloc, shaping sourcing and cross-border exports for Bekaert Handling Group A/S. EU–US two‑way trade in goods and services was roughly €1 trillion in 2023, while goods trade with China was around €760 billion, meaning shifts in relations alter landed polymer, fabric and component costs. Monitoring anti-dumping measures in industrial textiles and steel remains essential, and active engagement with trade bodies helps anticipate rule changes.

Industrial subsidies

National and EU incentives — notably Horizon Europe (€95.5bn 2021–27) and the Recovery and Resilience Facility (RRF, €723.8bn) — can materially reduce Bekaert Handling Group A/S capex for automation and green tech projects. Competing jurisdictions offering local subsidies may alter plant-location economics and ROI. Timely applications unlock grants for energy-efficiency upgrades and R&D, while policy reversals can disrupt long-term investment plans.

Geopolitical logistics

Conflicts and sanctions have disrupted sea lanes, driving war-risk premiums in hotspots like the Red Sea up over 200% in 2023–24 and lengthening lead times by several days. Routing via stable corridors can cut disruption risk for containerized shipments. Diversified suppliers in friendly jurisdictions improve resilience. Expanded US/EU export controls since 2023 restrict certain dual-use technologies, affecting transfers.

Standards harmonization

Alignment of packaging and handling standards across the 27‑country European Single Market lowers compliance friction and cross‑border testing; ISO reports over 24,000 International Standards (2024), reducing multiplicity of national specs. Divergent national rules raise testing and certification costs and time to market. Participation in standards committees lets Bekaert Handling influence practical requirements, while early compliance signals stronger tender competitiveness.

- Standards scale: ISO >24,000 (2024)

- EU market: 27 countries—reduces cross‑border friction

- Committee participation: shapes requirements

- Early compliance: competitive tender signal

Public procurement

Public procurement cycles drive demand for handling equipment—EU public procurement represented about 14% of GDP in recent years and global public tendering often tracks government capex, so SOE and infrastructure tenders materially affect order timing and volume. Local content rules (eg India/local preference policies) can force higher domestic sourcing or assembly, altering margins and supply chains. Transparent, audited bidding favors certified, safety-led suppliers and political shifts can quickly reallocate budgets across transport, energy or industrial projects.

- Procurement share: EU ~14% of GDP

- Local content: procurement preferences (eg India) reshape sourcing

- Compliance edge: certification and safety improve tender win-rate

- Political risk: sector reprioritization alters capex flows

EU market €1.0tn; funds lower capex; Red Sea risk > 200%

EU Single Market (27 states) eases cross‑border trade; EU–US goods/services two‑way ≈€1.0tn (2023) and EU–China goods ≈€760bn (2023), so geopolitical shifts affect component costs. Horizon Europe (€95.5bn 2021–27) and RRF (€723.8bn) cut capex for automation/green projects; EU public procurement ≈14% GDP. Red Sea war‑risk premiums rose >200% in 2023–24, extending lead times.

| Indicator | Value |

|---|---|

| EU states | 27 |

| Horizon Europe | €95.5bn (2021–27) |

| RRF | €723.8bn |

| EU–US trade (2023) | €1.0tn |

| War‑risk premium Red Sea | +>200% (2023–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bekaert Handling Group A/S across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking implications to help executives, consultants and investors identify risks, opportunities and strategic responses.

A clean, summarized PESTLE of Bekaert Handling Group A/S, visually segmented and editable, streamlines meetings and presentations, supports external risk and market-positioning discussions, and is easily shareable or dropped into slides for quick team alignment.

Economic factors

Industrial cycle

Industrial cycles drive Bekaert Handling demand: capital goods sales closely follow S&P Global manufacturing PMI, which hovered around 50 in 2024, and corporate capex trends; IMF projected global GDP growth of 3.2% in 2024 and 3.0% in 2025, shifting volumes in chemicals, agriculture and e-commerce. Backlog accumulation in upswings stabilizes utilization, while flexible cost structures (variable labor, outsourced logistics) have cushioned recent downturns.

Input inflation

Input inflation from resin, technical textile and steel price volatility compresses margins across Bekaert Handling Group, forcing tighter cost pass-through. Indexed pricing and forward-hedging programs have smoothed reported COGS swings. Dual-sourcing strategies limit single-supplier disruptions. Strict inventory discipline lowers holding losses when input deflation occurs.

FX exposure

Multi-currency sales and imports create translation and transaction risk for Bekaert Handling Group A/S, with global FX markets averaging about USD 7.5 trillion daily turnover (BIS Apr 2022) increasing exposure. Natural hedging by matching costs and revenues reduces net risk, while forwards and options lock quote validity. Sudden FX swings can reprice export competitiveness overnight.

Freight and energy

- Ocean rates: -70% from 2021 peak (to 2023)

- Energy tariff trigger: >0.15–0.20 USD/kWh for faster payback

- Nearshoring: reduces transit uncertainty and demurrage exposure

- Customer tolerance: surcharges acceptable if SLAs intact

Rates and credit

Higher interest rates (ECB deposit ~4%, US Fed funds 5.25–5.50% in 2024–2025) raise WACC and leasing costs for automation, prompting customers to defer upgrades and stretch sales cycles. Vendor financing and service-based models have protected order intake, while strong balance sheets secure better terms with lenders.

- Higher rates: WACC up

- Leasing cost rise

- Deferred upgrades

- Vendor finance shields orders

- Strong balance sheet = better lender terms

EU market €1.0tn; funds lower capex; Red Sea risk > 200%

Industrial cycles and IMF 2024–25 growth (3.2% / 3.0%) drive demand; backlog cushions upswings while flexible cost bases limit downside. Input volatility (resin/steel) and ocean rate swings (‑70% from 2021 peak to 2023) compress margins; indexed pricing and hedges mitigate. Higher rates (US Fed 5.25–5.50%, ECB dep ~4%) raise WACC, slowing capex; vendor finance and strong balance sheets support orders.

| Metric | Value |

|---|---|

| Global GDP growth 2024/25 (IMF) | 3.2% / 3.0% |

| US Fed funds | 5.25–5.50% |

| ECB deposit | ~4% |

| Ocean rates change (peak→2023) | ‑70% |

| FX daily turnover (BIS Apr 2022) | USD 7.5tn |

Full Version Awaits

Bekaert Handling Group A/S PESTLE Analysis

The preview shown here is the exact Bekaert Handling Group A/S PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure and layout you see are the final version with no placeholders or teasers. After payment you’ll instantly download this exact file, complete and professionally structured for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of Bekaert Handling Group A/S reveals how political shifts, macroeconomic cycles, and rapid tech innovation shape its strategic risks and opportunities. Packed with actionable insights, this briefing helps investors and strategists anticipate regulatory, social, and environmental impacts. Purchase the full analysis to access the complete, fully editable report and make smarter decisions today.

Political factors

EU trade policy

EU Single Market of 27 states guarantees tariff-free movement across the bloc, shaping sourcing and cross-border exports for Bekaert Handling Group A/S. EU–US two‑way trade in goods and services was roughly €1 trillion in 2023, while goods trade with China was around €760 billion, meaning shifts in relations alter landed polymer, fabric and component costs. Monitoring anti-dumping measures in industrial textiles and steel remains essential, and active engagement with trade bodies helps anticipate rule changes.

Industrial subsidies

National and EU incentives — notably Horizon Europe (€95.5bn 2021–27) and the Recovery and Resilience Facility (RRF, €723.8bn) — can materially reduce Bekaert Handling Group A/S capex for automation and green tech projects. Competing jurisdictions offering local subsidies may alter plant-location economics and ROI. Timely applications unlock grants for energy-efficiency upgrades and R&D, while policy reversals can disrupt long-term investment plans.

Geopolitical logistics

Conflicts and sanctions have disrupted sea lanes, driving war-risk premiums in hotspots like the Red Sea up over 200% in 2023–24 and lengthening lead times by several days. Routing via stable corridors can cut disruption risk for containerized shipments. Diversified suppliers in friendly jurisdictions improve resilience. Expanded US/EU export controls since 2023 restrict certain dual-use technologies, affecting transfers.

Standards harmonization

Alignment of packaging and handling standards across the 27‑country European Single Market lowers compliance friction and cross‑border testing; ISO reports over 24,000 International Standards (2024), reducing multiplicity of national specs. Divergent national rules raise testing and certification costs and time to market. Participation in standards committees lets Bekaert Handling influence practical requirements, while early compliance signals stronger tender competitiveness.

- Standards scale: ISO >24,000 (2024)

- EU market: 27 countries—reduces cross‑border friction

- Committee participation: shapes requirements

- Early compliance: competitive tender signal

Public procurement

Public procurement cycles drive demand for handling equipment—EU public procurement represented about 14% of GDP in recent years and global public tendering often tracks government capex, so SOE and infrastructure tenders materially affect order timing and volume. Local content rules (eg India/local preference policies) can force higher domestic sourcing or assembly, altering margins and supply chains. Transparent, audited bidding favors certified, safety-led suppliers and political shifts can quickly reallocate budgets across transport, energy or industrial projects.

- Procurement share: EU ~14% of GDP

- Local content: procurement preferences (eg India) reshape sourcing

- Compliance edge: certification and safety improve tender win-rate

- Political risk: sector reprioritization alters capex flows

EU market €1.0tn; funds lower capex; Red Sea risk > 200%

EU Single Market (27 states) eases cross‑border trade; EU–US goods/services two‑way ≈€1.0tn (2023) and EU–China goods ≈€760bn (2023), so geopolitical shifts affect component costs. Horizon Europe (€95.5bn 2021–27) and RRF (€723.8bn) cut capex for automation/green projects; EU public procurement ≈14% GDP. Red Sea war‑risk premiums rose >200% in 2023–24, extending lead times.

| Indicator | Value |

|---|---|

| EU states | 27 |

| Horizon Europe | €95.5bn (2021–27) |

| RRF | €723.8bn |

| EU–US trade (2023) | €1.0tn |

| War‑risk premium Red Sea | +>200% (2023–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bekaert Handling Group A/S across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking implications to help executives, consultants and investors identify risks, opportunities and strategic responses.

A clean, summarized PESTLE of Bekaert Handling Group A/S, visually segmented and editable, streamlines meetings and presentations, supports external risk and market-positioning discussions, and is easily shareable or dropped into slides for quick team alignment.

Economic factors

Industrial cycle

Industrial cycles drive Bekaert Handling demand: capital goods sales closely follow S&P Global manufacturing PMI, which hovered around 50 in 2024, and corporate capex trends; IMF projected global GDP growth of 3.2% in 2024 and 3.0% in 2025, shifting volumes in chemicals, agriculture and e-commerce. Backlog accumulation in upswings stabilizes utilization, while flexible cost structures (variable labor, outsourced logistics) have cushioned recent downturns.

Input inflation

Input inflation from resin, technical textile and steel price volatility compresses margins across Bekaert Handling Group, forcing tighter cost pass-through. Indexed pricing and forward-hedging programs have smoothed reported COGS swings. Dual-sourcing strategies limit single-supplier disruptions. Strict inventory discipline lowers holding losses when input deflation occurs.

FX exposure

Multi-currency sales and imports create translation and transaction risk for Bekaert Handling Group A/S, with global FX markets averaging about USD 7.5 trillion daily turnover (BIS Apr 2022) increasing exposure. Natural hedging by matching costs and revenues reduces net risk, while forwards and options lock quote validity. Sudden FX swings can reprice export competitiveness overnight.

Freight and energy

- Ocean rates: -70% from 2021 peak (to 2023)

- Energy tariff trigger: >0.15–0.20 USD/kWh for faster payback

- Nearshoring: reduces transit uncertainty and demurrage exposure

- Customer tolerance: surcharges acceptable if SLAs intact

Rates and credit

Higher interest rates (ECB deposit ~4%, US Fed funds 5.25–5.50% in 2024–2025) raise WACC and leasing costs for automation, prompting customers to defer upgrades and stretch sales cycles. Vendor financing and service-based models have protected order intake, while strong balance sheets secure better terms with lenders.

- Higher rates: WACC up

- Leasing cost rise

- Deferred upgrades

- Vendor finance shields orders

- Strong balance sheet = better lender terms

EU market €1.0tn; funds lower capex; Red Sea risk > 200%

Industrial cycles and IMF 2024–25 growth (3.2% / 3.0%) drive demand; backlog cushions upswings while flexible cost bases limit downside. Input volatility (resin/steel) and ocean rate swings (‑70% from 2021 peak to 2023) compress margins; indexed pricing and hedges mitigate. Higher rates (US Fed 5.25–5.50%, ECB dep ~4%) raise WACC, slowing capex; vendor finance and strong balance sheets support orders.

| Metric | Value |

|---|---|

| Global GDP growth 2024/25 (IMF) | 3.2% / 3.0% |

| US Fed funds | 5.25–5.50% |

| ECB deposit | ~4% |

| Ocean rates change (peak→2023) | ‑70% |

| FX daily turnover (BIS Apr 2022) | USD 7.5tn |

Full Version Awaits

Bekaert Handling Group A/S PESTLE Analysis

The preview shown here is the exact Bekaert Handling Group A/S PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure and layout you see are the final version with no placeholders or teasers. After payment you’ll instantly download this exact file, complete and professionally structured for immediate use.