Bharat Electronics Limited Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

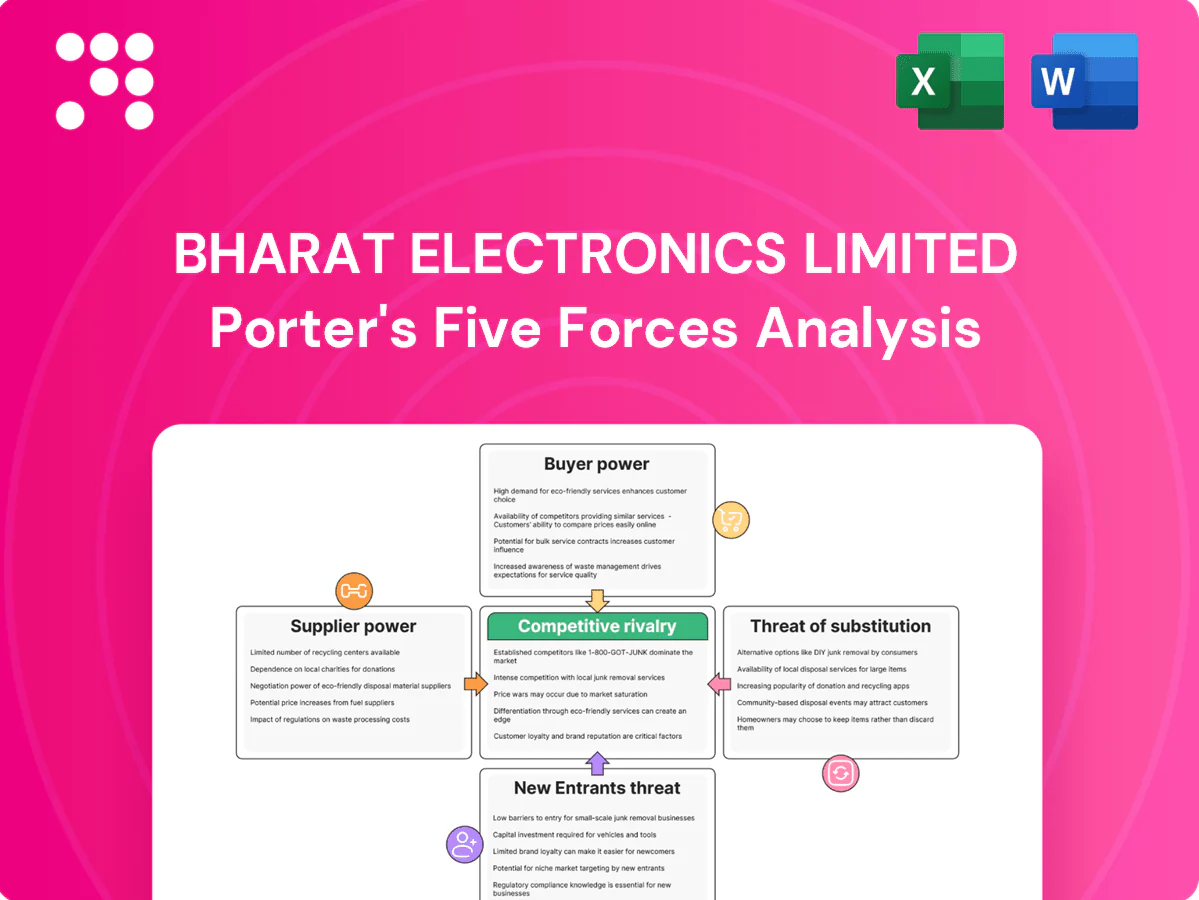

Bharat Electronics Limited navigates intense supplier and government influence, high entry barriers from defense contracts, moderate buyer power, and limited substitutes in specialized electronics, shaping a defensible yet regulation-sensitive position. This snapshot highlights strategic levers and risks. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated critical components

High-end RF, GaN, optronics and radiation‑hardened parts originate from a concentrated global pool (fewer than 10 qualified suppliers for many niche devices), creating single‑source dependencies and exposure to ITAR-like export controls and recent tightened US restrictions. BEL mitigates via multi‑vendor qualification and indigenization drives—reporting indigenization coverage of roughly 55% in key subsystems in 2024—yet niche component scarcity sustains moderate supplier leverage.

Import dependence and FX exposure

Selective import reliance exposes BEL to currency swings and logistics shocks; semiconductor lead times of 20–40 weeks amplify input-cost risk. Hedging and long-term framework contracts reduce volatility but do not eliminate FX or supply disruptions. When demand spikes outpace wafer capacity (industry utilization often >90%), suppliers gain pricing and delivery leverage, increasing BEL’s bargaining pressure.

Qualification and switching frictions

Defense-grade qualification, EMI/EMC compliance and rigorous reliability testing make supplier switching for BEL slow and costly, often stretching procurement cycles and raising replacement costs. Once a vendor passes qualification, the resulting lock-in increases its bargaining power despite BEL’s approved vendor lists that limit exposure but also narrow options. Long-term lifecycle sustainment and spares requirements keep incumbents entrenched, sustaining supplier leverage.

Government-backed vendor development

Government pushes since Make in India (launched 2014) and 2024 refinements to indigenous defence procurement (IDDM/Buy-Indian preferences) plus QMS-driven vendor development have expanded MSME participation, slowly lowering dependence on foreign suppliers; BEL’s long-term offtake commitments and tech handholding further dilute supplier leverage, though impact remains uneven across deep-tech nodes.

- Policy: Make in India (2014) and 2024 IDDM updates

- Effect: rising MSME supplier base, gradual import substitution

- BEL: long-term offtake + tech support reduces supplier bargaining

- Limit: uneven progress in deep-tech segments

Vertical integration scope

Bharat Electronics Limited’s in-house design, PCB assemblies and subsystem manufacturing temper supplier power at higher tiers, while upstream wafer fabs and advanced sensor stacks remain external. Selective backward integration into commoditised assemblies has improved procurement terms and cost control. Bottlenecks persist for frontier components, keeping supplier leverage on critical items.

- 16 manufacturing units (2024)

- In-house PCB/subsystem production reduces tier-1 supplier power

- Frontier sensors and wafer fabs remain external

Moderate supplier leverage despite 55% indigenization and 20-40 wk semiconductor lead times

BEL faces moderate supplier bargaining:

niche RF/GaN/optronics scarcity and export controls create single‑source risk, despite 55% indigenization in key subsystems (2024). Lead times of 20–40 weeks and wafer utilization >90% amplify supplier leverage; 16 manufacturing units and vendor development reduce but do not remove supplier power.

| Metric | Value | Note |

|---|---|---|

| Indigenization | ~55% | key subsystems (2024) |

| Units | 16 | manufacturing (2024) |

| Lead times | 20–40 wks | semiconductors |

| Wafer utilization | >90% | industry |

What is included in the product

Tailored Porter’s Five Forces analysis of Bharat Electronics Limited uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and highlighting industry dynamics and strategic levers that sustain BEL’s market position and profitability.

A clear, one-sheet summary of Bharat Electronics Limited's five forces—perfect for quick decision-making and ready to copy into pitch decks or boardroom slides. Swap in your own data and customize pressure levels to reflect defense contracts, tech shifts, or regulation changes for instant strategic clarity.

Customers Bargaining Power

Monopsony of Indian MoD

The Ministry of Defence and Services concentrate buyer power over BEL, steering procurement within India’s defence budget of ₹5.94 lakh crore for 2024–25; MoD-led tendering, benchmarking and nomination policies tightly shape pricing and volumes. BEL gains strategic alignment and steady orderflow but faces hard negotiations on margins and delivery timelines. Stringent delivery and quality KPIs further amplify MoD’s leverage.

Competitive tender mechanisms

Competitive tender mechanisms such as L1, QCBS and multi-vendor trials impose strict price discipline on Bharat Electronics Limited, compressing bid premiums and driving down award prices. Detailed technical evaluations and life-cycle cost models used in 2024 reduce scope for premium pricing and squeeze through-life margins. Framework agreements that cap escalation further reinforce buyer clout; BEL reported FY2023-24 revenue above INR 20,000 crore, underscoring the scale affected by these procurement dynamics.

High switching costs and installed base

High switching costs from platform integration, operator training and ILS tie customers to BEL, whose deep footprint in radars, comms and EW increases stickiness; India’s 2024 defence budget of ₹6.11 lakh crore and continuing modernization mean BEL captures long-term upgrade and MRO revenues that shift bargaining power toward BEL, though new procurements periodically reset competitive dynamics.

Offsets and indigenization mandates

Offsets and indigenization mandates steer system configurations and sourcing, enabling buyers to insist on local content that shapes BEL’s vendor selection and pricing levers, increasing customer bargaining power.

Compliance raises execution complexity and costs but often benefits BEL versus import‑heavy rivals due to its domestic supply chain; policy levers therefore both constrain and enable buyer bargaining.

- Buyers demand local content, altering vendor mix

- Compliance adds program complexity and cost

- BEL gains advantage versus import-dependent competitors

Civil and export diversification

Civil initiatives like smart cities, cyber-security projects and rising exports have broadened BELs customer mix, modestly diluting MoD dependence (MoD ~60% of revenue). These commercial markets offer many alternatives, constraining pricing power despite reference wins that boost credibility rather than market dominance. Net effect: a mild reduction in overall buyer-power concentration.

- MoD share ~60%

- Smart cities/cyber increase customer diversity

- Exports improve credibility, not pricing leverage

- Overall buyer power mildly reduced

MoD-driven procurement compresses margins; platform ties and ILS protect aftermarket revenue

MoD-centric procurement (MoD ~60% of BEL revenue) concentrates buyer power, enforcing strict L1/QCBS pricing, KPIs and local-content mandates that compress margins. Long-term platform ties and ILS create switching costs that protect BEL’s aftermarket revenue, while FY2023-24 revenue > INR 20,000 crore and India defence budget ₹5.94 lakh crore (2024–25) sustain orderflow. Commercial markets and exports modestly dilute MoD leverage.

| Metric | Value |

|---|---|

| MoD share of revenue | ~60% |

| BEL revenue FY2023-24 | INR 20,000+ crore |

| India defence budget 2024–25 | ₹5.94 lakh crore |

Full Version Awaits

Bharat Electronics Limited Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Bharat Electronics Limited you'll receive immediately after purchase—no placeholders or samples. The document is the fully formatted, professionally written file ready for download and immediate use. What you see here is precisely the deliverable you’ll get upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Bharat Electronics Limited navigates intense supplier and government influence, high entry barriers from defense contracts, moderate buyer power, and limited substitutes in specialized electronics, shaping a defensible yet regulation-sensitive position. This snapshot highlights strategic levers and risks. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated critical components

High-end RF, GaN, optronics and radiation‑hardened parts originate from a concentrated global pool (fewer than 10 qualified suppliers for many niche devices), creating single‑source dependencies and exposure to ITAR-like export controls and recent tightened US restrictions. BEL mitigates via multi‑vendor qualification and indigenization drives—reporting indigenization coverage of roughly 55% in key subsystems in 2024—yet niche component scarcity sustains moderate supplier leverage.

Import dependence and FX exposure

Selective import reliance exposes BEL to currency swings and logistics shocks; semiconductor lead times of 20–40 weeks amplify input-cost risk. Hedging and long-term framework contracts reduce volatility but do not eliminate FX or supply disruptions. When demand spikes outpace wafer capacity (industry utilization often >90%), suppliers gain pricing and delivery leverage, increasing BEL’s bargaining pressure.

Qualification and switching frictions

Defense-grade qualification, EMI/EMC compliance and rigorous reliability testing make supplier switching for BEL slow and costly, often stretching procurement cycles and raising replacement costs. Once a vendor passes qualification, the resulting lock-in increases its bargaining power despite BEL’s approved vendor lists that limit exposure but also narrow options. Long-term lifecycle sustainment and spares requirements keep incumbents entrenched, sustaining supplier leverage.

Government-backed vendor development

Government pushes since Make in India (launched 2014) and 2024 refinements to indigenous defence procurement (IDDM/Buy-Indian preferences) plus QMS-driven vendor development have expanded MSME participation, slowly lowering dependence on foreign suppliers; BEL’s long-term offtake commitments and tech handholding further dilute supplier leverage, though impact remains uneven across deep-tech nodes.

- Policy: Make in India (2014) and 2024 IDDM updates

- Effect: rising MSME supplier base, gradual import substitution

- BEL: long-term offtake + tech support reduces supplier bargaining

- Limit: uneven progress in deep-tech segments

Vertical integration scope

Bharat Electronics Limited’s in-house design, PCB assemblies and subsystem manufacturing temper supplier power at higher tiers, while upstream wafer fabs and advanced sensor stacks remain external. Selective backward integration into commoditised assemblies has improved procurement terms and cost control. Bottlenecks persist for frontier components, keeping supplier leverage on critical items.

- 16 manufacturing units (2024)

- In-house PCB/subsystem production reduces tier-1 supplier power

- Frontier sensors and wafer fabs remain external

Moderate supplier leverage despite 55% indigenization and 20-40 wk semiconductor lead times

BEL faces moderate supplier bargaining:

niche RF/GaN/optronics scarcity and export controls create single‑source risk, despite 55% indigenization in key subsystems (2024). Lead times of 20–40 weeks and wafer utilization >90% amplify supplier leverage; 16 manufacturing units and vendor development reduce but do not remove supplier power.

| Metric | Value | Note |

|---|---|---|

| Indigenization | ~55% | key subsystems (2024) |

| Units | 16 | manufacturing (2024) |

| Lead times | 20–40 wks | semiconductors |

| Wafer utilization | >90% | industry |

What is included in the product

Tailored Porter’s Five Forces analysis of Bharat Electronics Limited uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and highlighting industry dynamics and strategic levers that sustain BEL’s market position and profitability.

A clear, one-sheet summary of Bharat Electronics Limited's five forces—perfect for quick decision-making and ready to copy into pitch decks or boardroom slides. Swap in your own data and customize pressure levels to reflect defense contracts, tech shifts, or regulation changes for instant strategic clarity.

Customers Bargaining Power

Monopsony of Indian MoD

The Ministry of Defence and Services concentrate buyer power over BEL, steering procurement within India’s defence budget of ₹5.94 lakh crore for 2024–25; MoD-led tendering, benchmarking and nomination policies tightly shape pricing and volumes. BEL gains strategic alignment and steady orderflow but faces hard negotiations on margins and delivery timelines. Stringent delivery and quality KPIs further amplify MoD’s leverage.

Competitive tender mechanisms

Competitive tender mechanisms such as L1, QCBS and multi-vendor trials impose strict price discipline on Bharat Electronics Limited, compressing bid premiums and driving down award prices. Detailed technical evaluations and life-cycle cost models used in 2024 reduce scope for premium pricing and squeeze through-life margins. Framework agreements that cap escalation further reinforce buyer clout; BEL reported FY2023-24 revenue above INR 20,000 crore, underscoring the scale affected by these procurement dynamics.

High switching costs and installed base

High switching costs from platform integration, operator training and ILS tie customers to BEL, whose deep footprint in radars, comms and EW increases stickiness; India’s 2024 defence budget of ₹6.11 lakh crore and continuing modernization mean BEL captures long-term upgrade and MRO revenues that shift bargaining power toward BEL, though new procurements periodically reset competitive dynamics.

Offsets and indigenization mandates

Offsets and indigenization mandates steer system configurations and sourcing, enabling buyers to insist on local content that shapes BEL’s vendor selection and pricing levers, increasing customer bargaining power.

Compliance raises execution complexity and costs but often benefits BEL versus import‑heavy rivals due to its domestic supply chain; policy levers therefore both constrain and enable buyer bargaining.

- Buyers demand local content, altering vendor mix

- Compliance adds program complexity and cost

- BEL gains advantage versus import-dependent competitors

Civil and export diversification

Civil initiatives like smart cities, cyber-security projects and rising exports have broadened BELs customer mix, modestly diluting MoD dependence (MoD ~60% of revenue). These commercial markets offer many alternatives, constraining pricing power despite reference wins that boost credibility rather than market dominance. Net effect: a mild reduction in overall buyer-power concentration.

- MoD share ~60%

- Smart cities/cyber increase customer diversity

- Exports improve credibility, not pricing leverage

- Overall buyer power mildly reduced

MoD-driven procurement compresses margins; platform ties and ILS protect aftermarket revenue

MoD-centric procurement (MoD ~60% of BEL revenue) concentrates buyer power, enforcing strict L1/QCBS pricing, KPIs and local-content mandates that compress margins. Long-term platform ties and ILS create switching costs that protect BEL’s aftermarket revenue, while FY2023-24 revenue > INR 20,000 crore and India defence budget ₹5.94 lakh crore (2024–25) sustain orderflow. Commercial markets and exports modestly dilute MoD leverage.

| Metric | Value |

|---|---|

| MoD share of revenue | ~60% |

| BEL revenue FY2023-24 | INR 20,000+ crore |

| India defence budget 2024–25 | ₹5.94 lakh crore |

Full Version Awaits

Bharat Electronics Limited Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Bharat Electronics Limited you'll receive immediately after purchase—no placeholders or samples. The document is the fully formatted, professionally written file ready for download and immediate use. What you see here is precisely the deliverable you’ll get upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Bharat Electronics Limited navigates intense supplier and government influence, high entry barriers from defense contracts, moderate buyer power, and limited substitutes in specialized electronics, shaping a defensible yet regulation-sensitive position. This snapshot highlights strategic levers and risks. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated critical components

High-end RF, GaN, optronics and radiation‑hardened parts originate from a concentrated global pool (fewer than 10 qualified suppliers for many niche devices), creating single‑source dependencies and exposure to ITAR-like export controls and recent tightened US restrictions. BEL mitigates via multi‑vendor qualification and indigenization drives—reporting indigenization coverage of roughly 55% in key subsystems in 2024—yet niche component scarcity sustains moderate supplier leverage.

Import dependence and FX exposure

Selective import reliance exposes BEL to currency swings and logistics shocks; semiconductor lead times of 20–40 weeks amplify input-cost risk. Hedging and long-term framework contracts reduce volatility but do not eliminate FX or supply disruptions. When demand spikes outpace wafer capacity (industry utilization often >90%), suppliers gain pricing and delivery leverage, increasing BEL’s bargaining pressure.

Qualification and switching frictions

Defense-grade qualification, EMI/EMC compliance and rigorous reliability testing make supplier switching for BEL slow and costly, often stretching procurement cycles and raising replacement costs. Once a vendor passes qualification, the resulting lock-in increases its bargaining power despite BEL’s approved vendor lists that limit exposure but also narrow options. Long-term lifecycle sustainment and spares requirements keep incumbents entrenched, sustaining supplier leverage.

Government-backed vendor development

Government pushes since Make in India (launched 2014) and 2024 refinements to indigenous defence procurement (IDDM/Buy-Indian preferences) plus QMS-driven vendor development have expanded MSME participation, slowly lowering dependence on foreign suppliers; BEL’s long-term offtake commitments and tech handholding further dilute supplier leverage, though impact remains uneven across deep-tech nodes.

- Policy: Make in India (2014) and 2024 IDDM updates

- Effect: rising MSME supplier base, gradual import substitution

- BEL: long-term offtake + tech support reduces supplier bargaining

- Limit: uneven progress in deep-tech segments

Vertical integration scope

Bharat Electronics Limited’s in-house design, PCB assemblies and subsystem manufacturing temper supplier power at higher tiers, while upstream wafer fabs and advanced sensor stacks remain external. Selective backward integration into commoditised assemblies has improved procurement terms and cost control. Bottlenecks persist for frontier components, keeping supplier leverage on critical items.

- 16 manufacturing units (2024)

- In-house PCB/subsystem production reduces tier-1 supplier power

- Frontier sensors and wafer fabs remain external

Moderate supplier leverage despite 55% indigenization and 20-40 wk semiconductor lead times

BEL faces moderate supplier bargaining:

niche RF/GaN/optronics scarcity and export controls create single‑source risk, despite 55% indigenization in key subsystems (2024). Lead times of 20–40 weeks and wafer utilization >90% amplify supplier leverage; 16 manufacturing units and vendor development reduce but do not remove supplier power.

| Metric | Value | Note |

|---|---|---|

| Indigenization | ~55% | key subsystems (2024) |

| Units | 16 | manufacturing (2024) |

| Lead times | 20–40 wks | semiconductors |

| Wafer utilization | >90% | industry |

What is included in the product

Tailored Porter’s Five Forces analysis of Bharat Electronics Limited uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and highlighting industry dynamics and strategic levers that sustain BEL’s market position and profitability.

A clear, one-sheet summary of Bharat Electronics Limited's five forces—perfect for quick decision-making and ready to copy into pitch decks or boardroom slides. Swap in your own data and customize pressure levels to reflect defense contracts, tech shifts, or regulation changes for instant strategic clarity.

Customers Bargaining Power

Monopsony of Indian MoD

The Ministry of Defence and Services concentrate buyer power over BEL, steering procurement within India’s defence budget of ₹5.94 lakh crore for 2024–25; MoD-led tendering, benchmarking and nomination policies tightly shape pricing and volumes. BEL gains strategic alignment and steady orderflow but faces hard negotiations on margins and delivery timelines. Stringent delivery and quality KPIs further amplify MoD’s leverage.

Competitive tender mechanisms

Competitive tender mechanisms such as L1, QCBS and multi-vendor trials impose strict price discipline on Bharat Electronics Limited, compressing bid premiums and driving down award prices. Detailed technical evaluations and life-cycle cost models used in 2024 reduce scope for premium pricing and squeeze through-life margins. Framework agreements that cap escalation further reinforce buyer clout; BEL reported FY2023-24 revenue above INR 20,000 crore, underscoring the scale affected by these procurement dynamics.

High switching costs and installed base

High switching costs from platform integration, operator training and ILS tie customers to BEL, whose deep footprint in radars, comms and EW increases stickiness; India’s 2024 defence budget of ₹6.11 lakh crore and continuing modernization mean BEL captures long-term upgrade and MRO revenues that shift bargaining power toward BEL, though new procurements periodically reset competitive dynamics.

Offsets and indigenization mandates

Offsets and indigenization mandates steer system configurations and sourcing, enabling buyers to insist on local content that shapes BEL’s vendor selection and pricing levers, increasing customer bargaining power.

Compliance raises execution complexity and costs but often benefits BEL versus import‑heavy rivals due to its domestic supply chain; policy levers therefore both constrain and enable buyer bargaining.

- Buyers demand local content, altering vendor mix

- Compliance adds program complexity and cost

- BEL gains advantage versus import-dependent competitors

Civil and export diversification

Civil initiatives like smart cities, cyber-security projects and rising exports have broadened BELs customer mix, modestly diluting MoD dependence (MoD ~60% of revenue). These commercial markets offer many alternatives, constraining pricing power despite reference wins that boost credibility rather than market dominance. Net effect: a mild reduction in overall buyer-power concentration.

- MoD share ~60%

- Smart cities/cyber increase customer diversity

- Exports improve credibility, not pricing leverage

- Overall buyer power mildly reduced

MoD-driven procurement compresses margins; platform ties and ILS protect aftermarket revenue

MoD-centric procurement (MoD ~60% of BEL revenue) concentrates buyer power, enforcing strict L1/QCBS pricing, KPIs and local-content mandates that compress margins. Long-term platform ties and ILS create switching costs that protect BEL’s aftermarket revenue, while FY2023-24 revenue > INR 20,000 crore and India defence budget ₹5.94 lakh crore (2024–25) sustain orderflow. Commercial markets and exports modestly dilute MoD leverage.

| Metric | Value |

|---|---|

| MoD share of revenue | ~60% |

| BEL revenue FY2023-24 | INR 20,000+ crore |

| India defence budget 2024–25 | ₹5.94 lakh crore |

Full Version Awaits

Bharat Electronics Limited Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Bharat Electronics Limited you'll receive immediately after purchase—no placeholders or samples. The document is the fully formatted, professionally written file ready for download and immediate use. What you see here is precisely the deliverable you’ll get upon payment.