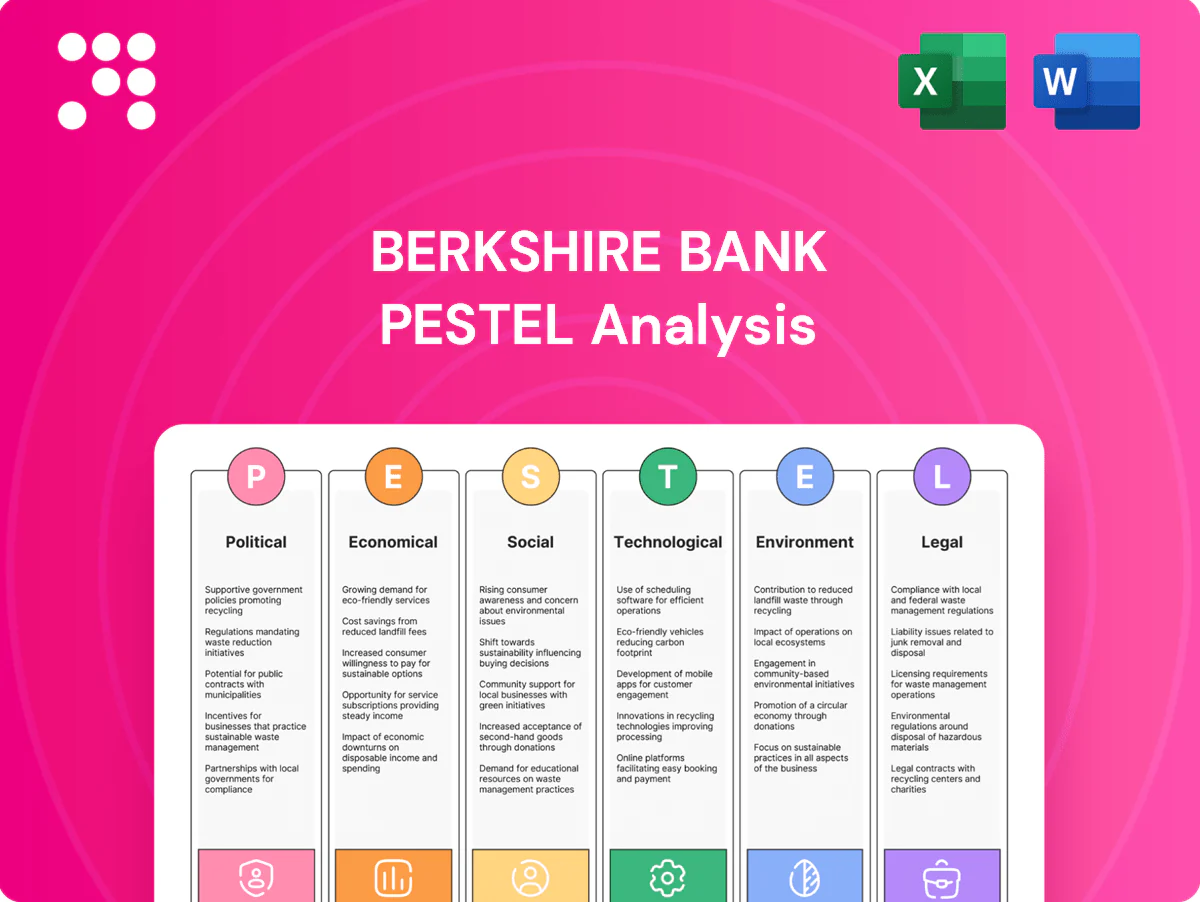

Berkshire Bank PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal and environmental forces shape Berkshire Bank’s future with our concise PESTLE snapshot—ideal for investors and strategists. Each trend is tied to practical implications and action points. Buy the full PESTLE to access the complete, editable analysis and make decisions with confidence.

Political factors

US banking policy direction

Shifts in federal priorities since 2023 (White House and Congress) have altered supervisory tone, capital emphasis and consumer protection focus, raising compliance burdens for regional banks like Berkshire Bank; pro‑growth agendas in 2024 spurred small‑business lending initiatives while tighter oversight in 2025 increased operating costs, and the 2024 election cycle introduced multi‑year planning uncertainty.

Basel III Endgame debates

Proposed Basel III Endgame recalibrations could raise risk-weighted assets by an industry-estimated 5–15% and effectively increase CET1 requirements by ~0.5–1.5 percentage points, potentially constraining Berkshire Bank’s balance-sheet growth. Even if thresholds target global systemics, trickle-down enforcement and higher supervisory buffers often tighten regional standards and underwriting. A 1 ppt capital uplift could cut ROE by roughly 50–150 bps and lower lending capacity, so scenario planning on credit mix and pricing is essential.

State-level priorities in Northeast

Massachusetts 201 CMR 17.00, New York DFS 23 NYCRR 500, Connecticut Public Act 23-3 and recent Vermont privacy/consumer measures create cybersecurity and consumer protections above federal baselines. Divergent state rules drive complex, multi-state compliance for Berkshire Bank. Local tax and grant incentives in the region support CRA-aligned lending. State political support for affordable housing influences mortgage product strategy and capital allocation.

Public funding and infrastructure

Federal and state infrastructure programs, notably the Bipartisan Infrastructure Law (1.2 trillion total, ~550 billion in new spending), create lending and treasury opportunities with municipalities and contractors across Berkshire Bank's New England and New York markets.

Timing of appropriations and multiyear allocations through 2026 shapes commercial loan pipelines; delays compress deal flow and credit production in quarters when funds are paused.

Partnerships on public projects can boost noninterest fee income via cash management and bond services, while budget cuts or payment delays can stall regional activity and slow deposit and fee growth.

- Federal BIL: 1.2 trillion total, ~550 billion new

- Multiyear appropriations affect loan origination timing

- Partnerships drive cash-management fee income

- Budget delays risk regional loan and deposit growth

Trade and geopolitical spillovers

Global tensions disrupt supply chains and regional manufacturers served by Berkshire Bank, increasing order volatility for export-dependent clients and driving short-term working capital needs; manufacturing and trade shocks raised global supply-chain lead times by roughly 20% during 2022–24.

Expanded sanctions regimes elevate BSA/AML monitoring requirements and compliance costs for the bank, while macro uncertainty has weighed on deposit behavior and credit appetite, with business loan demand fluctuating quarter-to-quarter.

- Trade disruptions: higher lead times ~20%

- Export volatility: increased working-capital demand

- Sanctions: tighter BSA/AML controls

- Macro: variable deposits and credit appetite

Regulatory and trade shocks hit regional banks, Basel RWA 5-15% cuts ROE

Federal/state regulatory shifts since 2023 raised compliance and capital costs for regional banks; proposed Basel III Endgame could boost RWA 5–15% (CET1 +0.5–1.5 ppt), cutting ROE ~50–150 bps. State cybersecurity/consumer laws and election-cycle uncertainty increase multi‑year planning risk. Infrastructure spending and trade shocks (supply‑lead times +~20% 2022–24) create lending and fee opportunities but add volatility.

| Metric | Value |

|---|---|

| Basel RWA uplift | 5–15% |

| CET1 impact | +0.5–1.5 ppt |

| BIL new spending | $550B |

| Supply lead times | +~20% (2022–24) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Berkshire Bank, with data-driven, region- and industry-specific analysis highlighting risks, opportunities and regulatory dynamics. Designed for executives and investors, the forward-looking assessment is ready for inclusion in plans, decks or reports.

A concise, visually segmented Berkshire Bank PESTLE summary that relieves briefing pain points by enabling quick interpretation across political, economic, social, technological, legal and environmental factors. Easily editable and shareable, it fits presentations and planning sessions for fast team alignment.

Economic factors

Interest rate volatility

NIM for Berkshire Bank remains sensitive to the Fed funds rate (5.25–5.50% through 2024) and deposit betas (industry averages rose toward ~30%), since asset repricing lags; a flatter or 2/10 inverted curve (roughly -100 bps at peak inversion in 2023) compresses margins, while rate cuts can lower yields faster than funding costs fall. Active hedging, balance-sheet mix and disciplined pricing are critical to preserve retention and growth.

Regional growth dynamics

Northeast real GDP expanded about 1.6% in 2024 (BEA), while regional home prices rose roughly 3% YoY (S&P CoreLogic Case‑Shiller, 2024), supporting mortgage and HELOC demand; small‑business loan inquiries climbed near 4% (2024 Small Business Credit Survey), with urban metros showing resilience as legacy industrial counties lag. Seasonal tourism and college cycles drive deposit swings, and geographic diversification across metros cushions localized shocks.

Credit quality and CRE exposure

Office and retail CRE face valuation pressure as cap rates have widened and U.S. office vacancy stayed above 16% in 2024 amid persistent hybrid work and higher financing costs (policy rate near 5.25–5.50% in 2024). Berkshire Bank’s proactive stress testing and borrower engagement help limit losses. Concentration limits and collateral strategies are critical. Softening consumer credit would impair cards, autos and HELOCs.

Liquidity competition

Money market funds (about $5.8 trillion of assets in 2024) and high‑yield online savings (top rates ~4.5–5.0% in 2024) lift wholesale funding costs, narrowing net interest margin for regional banks like Berkshire Bank. Core deposit franchise strength provides stability and pricing power, while use of brokered deposits and roughly $1.05 trillion of FHLB advances nationally in 2024 gives liquidity flexibility but compresses earnings; deposit mix management remains a priority.

- MMF assets: ~5.8T (2024)

- Top online savings rates: ~4.5–5.0% (2024)

- FHLB advances outstanding: ~1.05T (2024)

- Priority: active deposit mix management

Scale and efficiency pressures

Industry consolidation raises the bar on technology spend and unit costs, forcing Berkshire Bank to scale digital investments to remain competitive while managing higher per-branch economics. Operating leverage now hinges on branch optimization and customer digital adoption to lower cost-to-income ratios. Fee income from wealth management and insurance increasingly diversifies revenue, while M&A opportunities require careful balance of integration risk and capital allocation.

- Tech-driven unit cost pressure

- Branch optimization critical

- Wealth/insurance fee diversification

- M&A: growth vs integration risk

Regulatory and trade shocks hit regional banks, Basel RWA 5-15% cuts ROE

NIM sensitivity remains high as fed funds held at 5.25–5.50% in 2024 with deposit betas near 30%, compressing margins until asset repricing catches up. Northeast GDP grew ~1.6% in 2024 and home prices +3% YoY, supporting mortgages and HELOCs, while CRE office vacancy >16% raises stress. MMF flows (~5.8T) and FHLB advances (~1.05T) tighten funding costs, forcing deposit mix and digital scale actions.

| Metric | Value (2024) |

|---|---|

| Fed funds | 5.25–5.50% |

| Northeast GDP | ~1.6% |

| Home prices (NE) | +3% YoY |

| MMF assets | ~5.8T |

| FHLB advances | ~1.05T |

Same Document Delivered

Berkshire Bank PESTLE Analysis

The preview shown here is the exact Berkshire Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors affecting Berkshire Bank, with concise implications for risk and strategy. No placeholders or surprises—this is the final, downloadable file you’ll own after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal and environmental forces shape Berkshire Bank’s future with our concise PESTLE snapshot—ideal for investors and strategists. Each trend is tied to practical implications and action points. Buy the full PESTLE to access the complete, editable analysis and make decisions with confidence.

Political factors

US banking policy direction

Shifts in federal priorities since 2023 (White House and Congress) have altered supervisory tone, capital emphasis and consumer protection focus, raising compliance burdens for regional banks like Berkshire Bank; pro‑growth agendas in 2024 spurred small‑business lending initiatives while tighter oversight in 2025 increased operating costs, and the 2024 election cycle introduced multi‑year planning uncertainty.

Basel III Endgame debates

Proposed Basel III Endgame recalibrations could raise risk-weighted assets by an industry-estimated 5–15% and effectively increase CET1 requirements by ~0.5–1.5 percentage points, potentially constraining Berkshire Bank’s balance-sheet growth. Even if thresholds target global systemics, trickle-down enforcement and higher supervisory buffers often tighten regional standards and underwriting. A 1 ppt capital uplift could cut ROE by roughly 50–150 bps and lower lending capacity, so scenario planning on credit mix and pricing is essential.

State-level priorities in Northeast

Massachusetts 201 CMR 17.00, New York DFS 23 NYCRR 500, Connecticut Public Act 23-3 and recent Vermont privacy/consumer measures create cybersecurity and consumer protections above federal baselines. Divergent state rules drive complex, multi-state compliance for Berkshire Bank. Local tax and grant incentives in the region support CRA-aligned lending. State political support for affordable housing influences mortgage product strategy and capital allocation.

Public funding and infrastructure

Federal and state infrastructure programs, notably the Bipartisan Infrastructure Law (1.2 trillion total, ~550 billion in new spending), create lending and treasury opportunities with municipalities and contractors across Berkshire Bank's New England and New York markets.

Timing of appropriations and multiyear allocations through 2026 shapes commercial loan pipelines; delays compress deal flow and credit production in quarters when funds are paused.

Partnerships on public projects can boost noninterest fee income via cash management and bond services, while budget cuts or payment delays can stall regional activity and slow deposit and fee growth.

- Federal BIL: 1.2 trillion total, ~550 billion new

- Multiyear appropriations affect loan origination timing

- Partnerships drive cash-management fee income

- Budget delays risk regional loan and deposit growth

Trade and geopolitical spillovers

Global tensions disrupt supply chains and regional manufacturers served by Berkshire Bank, increasing order volatility for export-dependent clients and driving short-term working capital needs; manufacturing and trade shocks raised global supply-chain lead times by roughly 20% during 2022–24.

Expanded sanctions regimes elevate BSA/AML monitoring requirements and compliance costs for the bank, while macro uncertainty has weighed on deposit behavior and credit appetite, with business loan demand fluctuating quarter-to-quarter.

- Trade disruptions: higher lead times ~20%

- Export volatility: increased working-capital demand

- Sanctions: tighter BSA/AML controls

- Macro: variable deposits and credit appetite

Regulatory and trade shocks hit regional banks, Basel RWA 5-15% cuts ROE

Federal/state regulatory shifts since 2023 raised compliance and capital costs for regional banks; proposed Basel III Endgame could boost RWA 5–15% (CET1 +0.5–1.5 ppt), cutting ROE ~50–150 bps. State cybersecurity/consumer laws and election-cycle uncertainty increase multi‑year planning risk. Infrastructure spending and trade shocks (supply‑lead times +~20% 2022–24) create lending and fee opportunities but add volatility.

| Metric | Value |

|---|---|

| Basel RWA uplift | 5–15% |

| CET1 impact | +0.5–1.5 ppt |

| BIL new spending | $550B |

| Supply lead times | +~20% (2022–24) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Berkshire Bank, with data-driven, region- and industry-specific analysis highlighting risks, opportunities and regulatory dynamics. Designed for executives and investors, the forward-looking assessment is ready for inclusion in plans, decks or reports.

A concise, visually segmented Berkshire Bank PESTLE summary that relieves briefing pain points by enabling quick interpretation across political, economic, social, technological, legal and environmental factors. Easily editable and shareable, it fits presentations and planning sessions for fast team alignment.

Economic factors

Interest rate volatility

NIM for Berkshire Bank remains sensitive to the Fed funds rate (5.25–5.50% through 2024) and deposit betas (industry averages rose toward ~30%), since asset repricing lags; a flatter or 2/10 inverted curve (roughly -100 bps at peak inversion in 2023) compresses margins, while rate cuts can lower yields faster than funding costs fall. Active hedging, balance-sheet mix and disciplined pricing are critical to preserve retention and growth.

Regional growth dynamics

Northeast real GDP expanded about 1.6% in 2024 (BEA), while regional home prices rose roughly 3% YoY (S&P CoreLogic Case‑Shiller, 2024), supporting mortgage and HELOC demand; small‑business loan inquiries climbed near 4% (2024 Small Business Credit Survey), with urban metros showing resilience as legacy industrial counties lag. Seasonal tourism and college cycles drive deposit swings, and geographic diversification across metros cushions localized shocks.

Credit quality and CRE exposure

Office and retail CRE face valuation pressure as cap rates have widened and U.S. office vacancy stayed above 16% in 2024 amid persistent hybrid work and higher financing costs (policy rate near 5.25–5.50% in 2024). Berkshire Bank’s proactive stress testing and borrower engagement help limit losses. Concentration limits and collateral strategies are critical. Softening consumer credit would impair cards, autos and HELOCs.

Liquidity competition

Money market funds (about $5.8 trillion of assets in 2024) and high‑yield online savings (top rates ~4.5–5.0% in 2024) lift wholesale funding costs, narrowing net interest margin for regional banks like Berkshire Bank. Core deposit franchise strength provides stability and pricing power, while use of brokered deposits and roughly $1.05 trillion of FHLB advances nationally in 2024 gives liquidity flexibility but compresses earnings; deposit mix management remains a priority.

- MMF assets: ~5.8T (2024)

- Top online savings rates: ~4.5–5.0% (2024)

- FHLB advances outstanding: ~1.05T (2024)

- Priority: active deposit mix management

Scale and efficiency pressures

Industry consolidation raises the bar on technology spend and unit costs, forcing Berkshire Bank to scale digital investments to remain competitive while managing higher per-branch economics. Operating leverage now hinges on branch optimization and customer digital adoption to lower cost-to-income ratios. Fee income from wealth management and insurance increasingly diversifies revenue, while M&A opportunities require careful balance of integration risk and capital allocation.

- Tech-driven unit cost pressure

- Branch optimization critical

- Wealth/insurance fee diversification

- M&A: growth vs integration risk

Regulatory and trade shocks hit regional banks, Basel RWA 5-15% cuts ROE

NIM sensitivity remains high as fed funds held at 5.25–5.50% in 2024 with deposit betas near 30%, compressing margins until asset repricing catches up. Northeast GDP grew ~1.6% in 2024 and home prices +3% YoY, supporting mortgages and HELOCs, while CRE office vacancy >16% raises stress. MMF flows (~5.8T) and FHLB advances (~1.05T) tighten funding costs, forcing deposit mix and digital scale actions.

| Metric | Value (2024) |

|---|---|

| Fed funds | 5.25–5.50% |

| Northeast GDP | ~1.6% |

| Home prices (NE) | +3% YoY |

| MMF assets | ~5.8T |

| FHLB advances | ~1.05T |

Same Document Delivered

Berkshire Bank PESTLE Analysis

The preview shown here is the exact Berkshire Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors affecting Berkshire Bank, with concise implications for risk and strategy. No placeholders or surprises—this is the final, downloadable file you’ll own after checkout.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal and environmental forces shape Berkshire Bank’s future with our concise PESTLE snapshot—ideal for investors and strategists. Each trend is tied to practical implications and action points. Buy the full PESTLE to access the complete, editable analysis and make decisions with confidence.

Political factors

US banking policy direction

Shifts in federal priorities since 2023 (White House and Congress) have altered supervisory tone, capital emphasis and consumer protection focus, raising compliance burdens for regional banks like Berkshire Bank; pro‑growth agendas in 2024 spurred small‑business lending initiatives while tighter oversight in 2025 increased operating costs, and the 2024 election cycle introduced multi‑year planning uncertainty.

Basel III Endgame debates

Proposed Basel III Endgame recalibrations could raise risk-weighted assets by an industry-estimated 5–15% and effectively increase CET1 requirements by ~0.5–1.5 percentage points, potentially constraining Berkshire Bank’s balance-sheet growth. Even if thresholds target global systemics, trickle-down enforcement and higher supervisory buffers often tighten regional standards and underwriting. A 1 ppt capital uplift could cut ROE by roughly 50–150 bps and lower lending capacity, so scenario planning on credit mix and pricing is essential.

State-level priorities in Northeast

Massachusetts 201 CMR 17.00, New York DFS 23 NYCRR 500, Connecticut Public Act 23-3 and recent Vermont privacy/consumer measures create cybersecurity and consumer protections above federal baselines. Divergent state rules drive complex, multi-state compliance for Berkshire Bank. Local tax and grant incentives in the region support CRA-aligned lending. State political support for affordable housing influences mortgage product strategy and capital allocation.

Public funding and infrastructure

Federal and state infrastructure programs, notably the Bipartisan Infrastructure Law (1.2 trillion total, ~550 billion in new spending), create lending and treasury opportunities with municipalities and contractors across Berkshire Bank's New England and New York markets.

Timing of appropriations and multiyear allocations through 2026 shapes commercial loan pipelines; delays compress deal flow and credit production in quarters when funds are paused.

Partnerships on public projects can boost noninterest fee income via cash management and bond services, while budget cuts or payment delays can stall regional activity and slow deposit and fee growth.

- Federal BIL: 1.2 trillion total, ~550 billion new

- Multiyear appropriations affect loan origination timing

- Partnerships drive cash-management fee income

- Budget delays risk regional loan and deposit growth

Trade and geopolitical spillovers

Global tensions disrupt supply chains and regional manufacturers served by Berkshire Bank, increasing order volatility for export-dependent clients and driving short-term working capital needs; manufacturing and trade shocks raised global supply-chain lead times by roughly 20% during 2022–24.

Expanded sanctions regimes elevate BSA/AML monitoring requirements and compliance costs for the bank, while macro uncertainty has weighed on deposit behavior and credit appetite, with business loan demand fluctuating quarter-to-quarter.

- Trade disruptions: higher lead times ~20%

- Export volatility: increased working-capital demand

- Sanctions: tighter BSA/AML controls

- Macro: variable deposits and credit appetite

Regulatory and trade shocks hit regional banks, Basel RWA 5-15% cuts ROE

Federal/state regulatory shifts since 2023 raised compliance and capital costs for regional banks; proposed Basel III Endgame could boost RWA 5–15% (CET1 +0.5–1.5 ppt), cutting ROE ~50–150 bps. State cybersecurity/consumer laws and election-cycle uncertainty increase multi‑year planning risk. Infrastructure spending and trade shocks (supply‑lead times +~20% 2022–24) create lending and fee opportunities but add volatility.

| Metric | Value |

|---|---|

| Basel RWA uplift | 5–15% |

| CET1 impact | +0.5–1.5 ppt |

| BIL new spending | $550B |

| Supply lead times | +~20% (2022–24) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Berkshire Bank, with data-driven, region- and industry-specific analysis highlighting risks, opportunities and regulatory dynamics. Designed for executives and investors, the forward-looking assessment is ready for inclusion in plans, decks or reports.

A concise, visually segmented Berkshire Bank PESTLE summary that relieves briefing pain points by enabling quick interpretation across political, economic, social, technological, legal and environmental factors. Easily editable and shareable, it fits presentations and planning sessions for fast team alignment.

Economic factors

Interest rate volatility

NIM for Berkshire Bank remains sensitive to the Fed funds rate (5.25–5.50% through 2024) and deposit betas (industry averages rose toward ~30%), since asset repricing lags; a flatter or 2/10 inverted curve (roughly -100 bps at peak inversion in 2023) compresses margins, while rate cuts can lower yields faster than funding costs fall. Active hedging, balance-sheet mix and disciplined pricing are critical to preserve retention and growth.

Regional growth dynamics

Northeast real GDP expanded about 1.6% in 2024 (BEA), while regional home prices rose roughly 3% YoY (S&P CoreLogic Case‑Shiller, 2024), supporting mortgage and HELOC demand; small‑business loan inquiries climbed near 4% (2024 Small Business Credit Survey), with urban metros showing resilience as legacy industrial counties lag. Seasonal tourism and college cycles drive deposit swings, and geographic diversification across metros cushions localized shocks.

Credit quality and CRE exposure

Office and retail CRE face valuation pressure as cap rates have widened and U.S. office vacancy stayed above 16% in 2024 amid persistent hybrid work and higher financing costs (policy rate near 5.25–5.50% in 2024). Berkshire Bank’s proactive stress testing and borrower engagement help limit losses. Concentration limits and collateral strategies are critical. Softening consumer credit would impair cards, autos and HELOCs.

Liquidity competition

Money market funds (about $5.8 trillion of assets in 2024) and high‑yield online savings (top rates ~4.5–5.0% in 2024) lift wholesale funding costs, narrowing net interest margin for regional banks like Berkshire Bank. Core deposit franchise strength provides stability and pricing power, while use of brokered deposits and roughly $1.05 trillion of FHLB advances nationally in 2024 gives liquidity flexibility but compresses earnings; deposit mix management remains a priority.

- MMF assets: ~5.8T (2024)

- Top online savings rates: ~4.5–5.0% (2024)

- FHLB advances outstanding: ~1.05T (2024)

- Priority: active deposit mix management

Scale and efficiency pressures

Industry consolidation raises the bar on technology spend and unit costs, forcing Berkshire Bank to scale digital investments to remain competitive while managing higher per-branch economics. Operating leverage now hinges on branch optimization and customer digital adoption to lower cost-to-income ratios. Fee income from wealth management and insurance increasingly diversifies revenue, while M&A opportunities require careful balance of integration risk and capital allocation.

- Tech-driven unit cost pressure

- Branch optimization critical

- Wealth/insurance fee diversification

- M&A: growth vs integration risk

Regulatory and trade shocks hit regional banks, Basel RWA 5-15% cuts ROE

NIM sensitivity remains high as fed funds held at 5.25–5.50% in 2024 with deposit betas near 30%, compressing margins until asset repricing catches up. Northeast GDP grew ~1.6% in 2024 and home prices +3% YoY, supporting mortgages and HELOCs, while CRE office vacancy >16% raises stress. MMF flows (~5.8T) and FHLB advances (~1.05T) tighten funding costs, forcing deposit mix and digital scale actions.

| Metric | Value (2024) |

|---|---|

| Fed funds | 5.25–5.50% |

| Northeast GDP | ~1.6% |

| Home prices (NE) | +3% YoY |

| MMF assets | ~5.8T |

| FHLB advances | ~1.05T |

Same Document Delivered

Berkshire Bank PESTLE Analysis

The preview shown here is the exact Berkshire Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors affecting Berkshire Bank, with concise implications for risk and strategy. No placeholders or surprises—this is the final, downloadable file you’ll own after checkout.