Berkshire Bank SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Berkshire Bank's conservative lending, strong regional brand, and digital investments position it well, but exposure to commercial real estate and competition pose risks. Want the full story on strengths, weaknesses, opportunities and threats? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel pack with strategic takeaways. Move from insight to action with investor-ready deliverables.

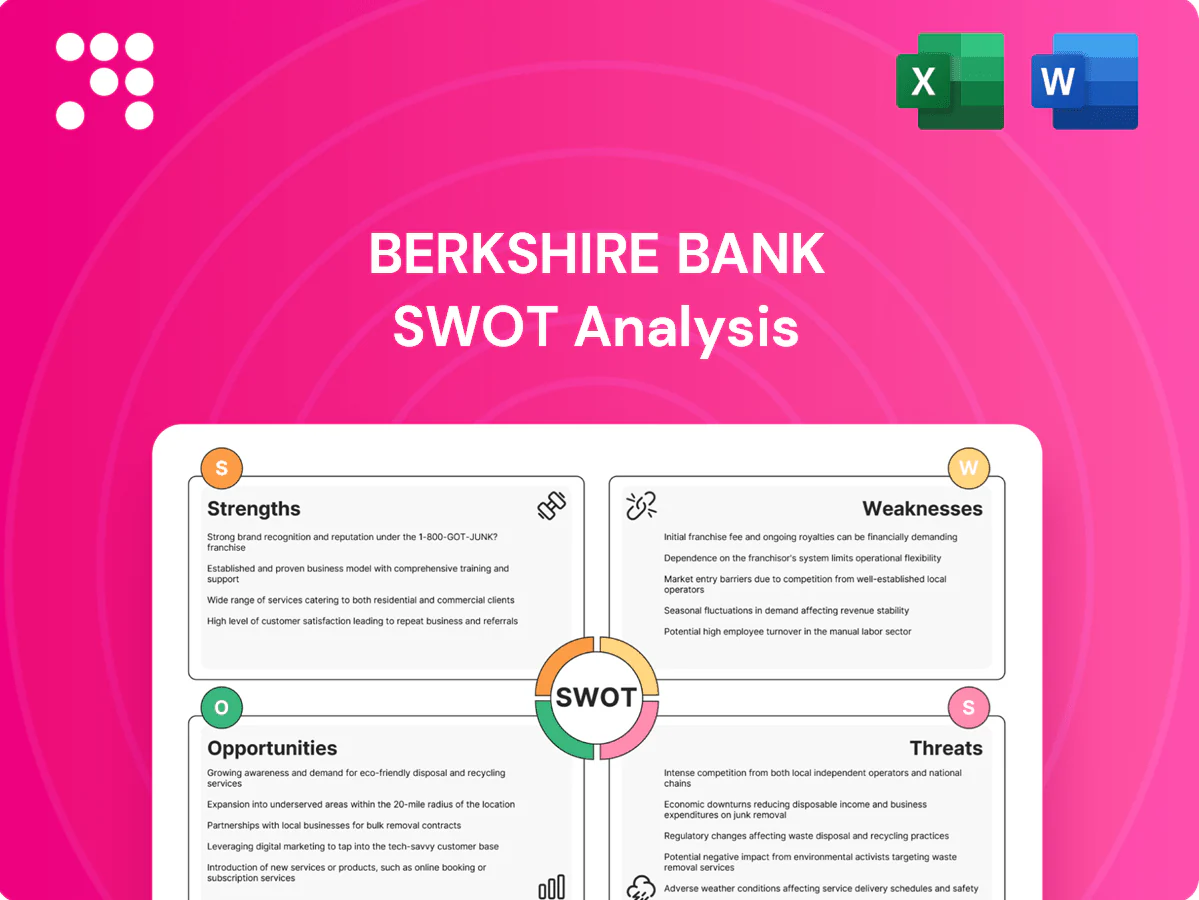

Strengths

Diversified financial services

Berkshire Bank combines retail and commercial banking, wealth management, investment advisory and insurance, producing multiple revenue streams that supported about $20 billion in assets and noninterest income roughly one-third of total revenue in recent reporting; this mix lowers dependence on net interest margin, boosts cross-selling to raise wallet share and enhances resilience across rate and credit cycles.

Strong regional footprint

Berkshire Bank concentrates its operations across five Northeastern states (Massachusetts, New York, Connecticut, Vermont, New Hampshire), building strong brand familiarity and deep local market knowledge. Local decisioning enables faster lending and service turnaround at branch level. A visible community presence supports relationship banking and stable core deposits. Proximity to customers enhances granular credit insight and risk assessment.

Omnichannel delivery

Berkshire Bank’s network of branches paired with digital channels widens access and convenience, enabling in-branch and remote services across regions. Customers can transact, apply, and manage finances seamlessly across platforms, supporting acquisition and retention across ages and income levels. With U.S. mobile banking adoption over 80% in 2024, growing digital usage helps lower cost-to-serve as more customers shift online.

Relationship banking with SMBs

Relationship banking with SMBs lets Berkshire Bank deliver tailored lending and treasury solutions, enabling relationship managers to price for value rather than compete solely on rate; stable operating accounts drive low-cost deposits and long-term ties produce referrals and cross-sell opportunities.

- SMB-focused lending

- Value-based pricing

- Low-cost deposit base

- Referral and cross-sell pipeline

Cross-sell capabilities

Cross-sell capabilities enable Berkshire Bank to bundle wealth, advisory and insurance around life events and business milestones, boosting fee income and reducing churn; Berkshire Hills Bancorp reported about $16 billion in assets in 2024 supporting scale for such offers.

Integrated advice differentiates the bank from product-only competitors and leverages data across lines for better personalization and risk insight.

Diversified retail, commercial, wealth and insurance mix boosts fee resilience, local deposits

Berkshire Bank’s diversified mix—retail, commercial, wealth, advisory and insurance—supports about $20 billion in assets and noninterest income ~one-third of revenue, reducing NIM dependence and boosting fee resilience.

Concentrated five-state New England footprint and branch+digital network deliver strong local deposits, SMB relationships and fast decisioning.

Wealth/insurance bundling and cross-sell raise fee income and lower churn.

| Metric | Value |

|---|---|

| Total assets | ~$20B |

| Berkshire Hills Bancorp assets (2024) | $16B |

| Noninterest income share | ~33% |

| Mobile banking adoption (US, 2024) | >80% |

What is included in the product

Provides a concise SWOT overview of Berkshire Bank, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and strategic outlook.

Provides a concise Berkshire Bank SWOT matrix for fast, visual strategy alignment and quick identification of competitive risks and opportunities.

Weaknesses

Geographic concentration

Operations concentrated in the Northeast — with over 100 branches clustered in New England and upstate New York — expose Berkshire Bank to regional economic shocks. Localized downturns can elevate credit losses and compress loan and deposit growth, as seen in prior regional recessions. Severe weather, dominant local industries, and state policy shifts can disproportionately impact performance. Limited geographic diversification reduces smoothing across markets.

Scale disadvantages

As a mid-sized bank with approximately $14.6 billion in assets at 12/31/2023, Berkshire Bank lacks the cost advantages of national banks that manage trillions in assets (eg JPMorgan ~3.5 trillion in 2024). Technology, marketing and compliance costs therefore consume a larger share of revenue, weakening pricing power versus mega-banks with broader product sets. Vendor terms and talent attraction often prove less favorable for regional firms.

Legacy technology burden

Berkshire Bank's legacy technology creates costly modernization needs for core systems and integrations, slowing digital feature rollouts and keeping change cycles longer than peers; this is stark given the bank's roughly $18.5 billion in assets and ~130-branch footprint (2024). Fragmented data hampers advanced analytics and personalization, raising operational risk and customer experience gaps that can erode retention and fee income.

Interest rate sensitivity

Berkshire Bank's net interest margin is tightly tied to asset-liability management and deposit betas; with the federal funds rate near 5.25–5.50% in 2024–2025, rapid rate shifts can quickly compress spreads or damp loan demand. Fixed-rate loan portfolios and slow-to-reprice deposits expose earnings when funding costs lag, and while hedging reduces volatility it increases funding costs and operational complexity.

- Deposit beta sensitivity

- Fixed-rate asset repricing lag

- Hedging cost and complexity

- Exposure to rate-driven loan demand shocks

Limited national brand

Outside its New England and New York core, Berkshire Bank's national brand recognition and trust lag larger national peers, constraining low-cost customer acquisition and forcing more targeted, higher-cost marketing to build awareness. Commercial clients with multi-state operations often prefer national banks offering uniform services and broader footprints, creating lost opportunity for larger commercial relationships.

- Limited national awareness

- Higher cost-per-acquisition

- Weak appeal to multi-state commercial clients

Concentrated Northeast (~130 branches) with $18.5B assets; rate exposure at 5.25–5.50%

Concentrated Northeast footprint (~130 branches) raises regional shock risk. Mid-size scale (~$18.5B assets, 2024) limits cost efficiency versus national banks. Legacy core tech slows digital rollout and raises modernization costs. Earnings sensitive to rate shifts with fed funds ~5.25–5.50% (2024–25), creating deposit beta and repricing exposure.

| Metric | Value |

|---|---|

| Total assets | $18.5B (2024) |

| Branches | ~130 |

| Fed funds | 5.25–5.50% (2024–25) |

Full Version Awaits

Berkshire Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download after payment.

Dive Deeper Into the Company’s Strategic Blueprint

Berkshire Bank's conservative lending, strong regional brand, and digital investments position it well, but exposure to commercial real estate and competition pose risks. Want the full story on strengths, weaknesses, opportunities and threats? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel pack with strategic takeaways. Move from insight to action with investor-ready deliverables.

Strengths

Diversified financial services

Berkshire Bank combines retail and commercial banking, wealth management, investment advisory and insurance, producing multiple revenue streams that supported about $20 billion in assets and noninterest income roughly one-third of total revenue in recent reporting; this mix lowers dependence on net interest margin, boosts cross-selling to raise wallet share and enhances resilience across rate and credit cycles.

Strong regional footprint

Berkshire Bank concentrates its operations across five Northeastern states (Massachusetts, New York, Connecticut, Vermont, New Hampshire), building strong brand familiarity and deep local market knowledge. Local decisioning enables faster lending and service turnaround at branch level. A visible community presence supports relationship banking and stable core deposits. Proximity to customers enhances granular credit insight and risk assessment.

Omnichannel delivery

Berkshire Bank’s network of branches paired with digital channels widens access and convenience, enabling in-branch and remote services across regions. Customers can transact, apply, and manage finances seamlessly across platforms, supporting acquisition and retention across ages and income levels. With U.S. mobile banking adoption over 80% in 2024, growing digital usage helps lower cost-to-serve as more customers shift online.

Relationship banking with SMBs

Relationship banking with SMBs lets Berkshire Bank deliver tailored lending and treasury solutions, enabling relationship managers to price for value rather than compete solely on rate; stable operating accounts drive low-cost deposits and long-term ties produce referrals and cross-sell opportunities.

- SMB-focused lending

- Value-based pricing

- Low-cost deposit base

- Referral and cross-sell pipeline

Cross-sell capabilities

Cross-sell capabilities enable Berkshire Bank to bundle wealth, advisory and insurance around life events and business milestones, boosting fee income and reducing churn; Berkshire Hills Bancorp reported about $16 billion in assets in 2024 supporting scale for such offers.

Integrated advice differentiates the bank from product-only competitors and leverages data across lines for better personalization and risk insight.

Diversified retail, commercial, wealth and insurance mix boosts fee resilience, local deposits

Berkshire Bank’s diversified mix—retail, commercial, wealth, advisory and insurance—supports about $20 billion in assets and noninterest income ~one-third of revenue, reducing NIM dependence and boosting fee resilience.

Concentrated five-state New England footprint and branch+digital network deliver strong local deposits, SMB relationships and fast decisioning.

Wealth/insurance bundling and cross-sell raise fee income and lower churn.

| Metric | Value |

|---|---|

| Total assets | ~$20B |

| Berkshire Hills Bancorp assets (2024) | $16B |

| Noninterest income share | ~33% |

| Mobile banking adoption (US, 2024) | >80% |

What is included in the product

Provides a concise SWOT overview of Berkshire Bank, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and strategic outlook.

Provides a concise Berkshire Bank SWOT matrix for fast, visual strategy alignment and quick identification of competitive risks and opportunities.

Weaknesses

Geographic concentration

Operations concentrated in the Northeast — with over 100 branches clustered in New England and upstate New York — expose Berkshire Bank to regional economic shocks. Localized downturns can elevate credit losses and compress loan and deposit growth, as seen in prior regional recessions. Severe weather, dominant local industries, and state policy shifts can disproportionately impact performance. Limited geographic diversification reduces smoothing across markets.

Scale disadvantages

As a mid-sized bank with approximately $14.6 billion in assets at 12/31/2023, Berkshire Bank lacks the cost advantages of national banks that manage trillions in assets (eg JPMorgan ~3.5 trillion in 2024). Technology, marketing and compliance costs therefore consume a larger share of revenue, weakening pricing power versus mega-banks with broader product sets. Vendor terms and talent attraction often prove less favorable for regional firms.

Legacy technology burden

Berkshire Bank's legacy technology creates costly modernization needs for core systems and integrations, slowing digital feature rollouts and keeping change cycles longer than peers; this is stark given the bank's roughly $18.5 billion in assets and ~130-branch footprint (2024). Fragmented data hampers advanced analytics and personalization, raising operational risk and customer experience gaps that can erode retention and fee income.

Interest rate sensitivity

Berkshire Bank's net interest margin is tightly tied to asset-liability management and deposit betas; with the federal funds rate near 5.25–5.50% in 2024–2025, rapid rate shifts can quickly compress spreads or damp loan demand. Fixed-rate loan portfolios and slow-to-reprice deposits expose earnings when funding costs lag, and while hedging reduces volatility it increases funding costs and operational complexity.

- Deposit beta sensitivity

- Fixed-rate asset repricing lag

- Hedging cost and complexity

- Exposure to rate-driven loan demand shocks

Limited national brand

Outside its New England and New York core, Berkshire Bank's national brand recognition and trust lag larger national peers, constraining low-cost customer acquisition and forcing more targeted, higher-cost marketing to build awareness. Commercial clients with multi-state operations often prefer national banks offering uniform services and broader footprints, creating lost opportunity for larger commercial relationships.

- Limited national awareness

- Higher cost-per-acquisition

- Weak appeal to multi-state commercial clients

Concentrated Northeast (~130 branches) with $18.5B assets; rate exposure at 5.25–5.50%

Concentrated Northeast footprint (~130 branches) raises regional shock risk. Mid-size scale (~$18.5B assets, 2024) limits cost efficiency versus national banks. Legacy core tech slows digital rollout and raises modernization costs. Earnings sensitive to rate shifts with fed funds ~5.25–5.50% (2024–25), creating deposit beta and repricing exposure.

| Metric | Value |

|---|---|

| Total assets | $18.5B (2024) |

| Branches | ~130 |

| Fed funds | 5.25–5.50% (2024–25) |

Full Version Awaits

Berkshire Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download after payment.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Berkshire Bank's conservative lending, strong regional brand, and digital investments position it well, but exposure to commercial real estate and competition pose risks. Want the full story on strengths, weaknesses, opportunities and threats? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel pack with strategic takeaways. Move from insight to action with investor-ready deliverables.

Strengths

Diversified financial services

Berkshire Bank combines retail and commercial banking, wealth management, investment advisory and insurance, producing multiple revenue streams that supported about $20 billion in assets and noninterest income roughly one-third of total revenue in recent reporting; this mix lowers dependence on net interest margin, boosts cross-selling to raise wallet share and enhances resilience across rate and credit cycles.

Strong regional footprint

Berkshire Bank concentrates its operations across five Northeastern states (Massachusetts, New York, Connecticut, Vermont, New Hampshire), building strong brand familiarity and deep local market knowledge. Local decisioning enables faster lending and service turnaround at branch level. A visible community presence supports relationship banking and stable core deposits. Proximity to customers enhances granular credit insight and risk assessment.

Omnichannel delivery

Berkshire Bank’s network of branches paired with digital channels widens access and convenience, enabling in-branch and remote services across regions. Customers can transact, apply, and manage finances seamlessly across platforms, supporting acquisition and retention across ages and income levels. With U.S. mobile banking adoption over 80% in 2024, growing digital usage helps lower cost-to-serve as more customers shift online.

Relationship banking with SMBs

Relationship banking with SMBs lets Berkshire Bank deliver tailored lending and treasury solutions, enabling relationship managers to price for value rather than compete solely on rate; stable operating accounts drive low-cost deposits and long-term ties produce referrals and cross-sell opportunities.

- SMB-focused lending

- Value-based pricing

- Low-cost deposit base

- Referral and cross-sell pipeline

Cross-sell capabilities

Cross-sell capabilities enable Berkshire Bank to bundle wealth, advisory and insurance around life events and business milestones, boosting fee income and reducing churn; Berkshire Hills Bancorp reported about $16 billion in assets in 2024 supporting scale for such offers.

Integrated advice differentiates the bank from product-only competitors and leverages data across lines for better personalization and risk insight.

Diversified retail, commercial, wealth and insurance mix boosts fee resilience, local deposits

Berkshire Bank’s diversified mix—retail, commercial, wealth, advisory and insurance—supports about $20 billion in assets and noninterest income ~one-third of revenue, reducing NIM dependence and boosting fee resilience.

Concentrated five-state New England footprint and branch+digital network deliver strong local deposits, SMB relationships and fast decisioning.

Wealth/insurance bundling and cross-sell raise fee income and lower churn.

| Metric | Value |

|---|---|

| Total assets | ~$20B |

| Berkshire Hills Bancorp assets (2024) | $16B |

| Noninterest income share | ~33% |

| Mobile banking adoption (US, 2024) | >80% |

What is included in the product

Provides a concise SWOT overview of Berkshire Bank, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and strategic outlook.

Provides a concise Berkshire Bank SWOT matrix for fast, visual strategy alignment and quick identification of competitive risks and opportunities.

Weaknesses

Geographic concentration

Operations concentrated in the Northeast — with over 100 branches clustered in New England and upstate New York — expose Berkshire Bank to regional economic shocks. Localized downturns can elevate credit losses and compress loan and deposit growth, as seen in prior regional recessions. Severe weather, dominant local industries, and state policy shifts can disproportionately impact performance. Limited geographic diversification reduces smoothing across markets.

Scale disadvantages

As a mid-sized bank with approximately $14.6 billion in assets at 12/31/2023, Berkshire Bank lacks the cost advantages of national banks that manage trillions in assets (eg JPMorgan ~3.5 trillion in 2024). Technology, marketing and compliance costs therefore consume a larger share of revenue, weakening pricing power versus mega-banks with broader product sets. Vendor terms and talent attraction often prove less favorable for regional firms.

Legacy technology burden

Berkshire Bank's legacy technology creates costly modernization needs for core systems and integrations, slowing digital feature rollouts and keeping change cycles longer than peers; this is stark given the bank's roughly $18.5 billion in assets and ~130-branch footprint (2024). Fragmented data hampers advanced analytics and personalization, raising operational risk and customer experience gaps that can erode retention and fee income.

Interest rate sensitivity

Berkshire Bank's net interest margin is tightly tied to asset-liability management and deposit betas; with the federal funds rate near 5.25–5.50% in 2024–2025, rapid rate shifts can quickly compress spreads or damp loan demand. Fixed-rate loan portfolios and slow-to-reprice deposits expose earnings when funding costs lag, and while hedging reduces volatility it increases funding costs and operational complexity.

- Deposit beta sensitivity

- Fixed-rate asset repricing lag

- Hedging cost and complexity

- Exposure to rate-driven loan demand shocks

Limited national brand

Outside its New England and New York core, Berkshire Bank's national brand recognition and trust lag larger national peers, constraining low-cost customer acquisition and forcing more targeted, higher-cost marketing to build awareness. Commercial clients with multi-state operations often prefer national banks offering uniform services and broader footprints, creating lost opportunity for larger commercial relationships.

- Limited national awareness

- Higher cost-per-acquisition

- Weak appeal to multi-state commercial clients

Concentrated Northeast (~130 branches) with $18.5B assets; rate exposure at 5.25–5.50%

Concentrated Northeast footprint (~130 branches) raises regional shock risk. Mid-size scale (~$18.5B assets, 2024) limits cost efficiency versus national banks. Legacy core tech slows digital rollout and raises modernization costs. Earnings sensitive to rate shifts with fed funds ~5.25–5.50% (2024–25), creating deposit beta and repricing exposure.

| Metric | Value |

|---|---|

| Total assets | $18.5B (2024) |

| Branches | ~130 |

| Fed funds | 5.25–5.50% (2024–25) |

Full Version Awaits

Berkshire Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download after payment.