Berry Global Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Berry Global Group reveals how political, economic, social, technological, legal, and environmental forces are reshaping the packaging leader’s strategy and risk profile. Gain actionable insights to anticipate regulatory shifts, supply-chain pressures, and sustainability trends. Purchase the full report for the complete, editable breakdown and immediate strategic value.

Political factors

Trade policy and tariffs

Shifts in US–China and EU trade policy, including US Section 301 tariffs that range from 7.5% to 25%, can materially change resin and machinery costs and pressure Berry Global’s margin stability. Tariffs on petrochemicals or packaging inputs effectively raise COGS by the tariff rate and complicate global sourcing and supply-chain planning. Favorable agreements such as USMCA (effective 1 July 2020) can open export markets but increase compliance burdens, so Berry must hedge exposure via diversified suppliers and regional production.

Single-use plastics regulation

Governments are tightening disposable-plastics rules—127 countries have national plastics laws and the EU Single-Use Plastics Directive (in force 2021) plus a 90% plastic-bottle collection target by 2029 are reshaping demand. Bans, taxes and mandates push Berry toward reusable/recyclable/compostable SKUs, raising SKU and formulation complexity; early policy alignment can secure approvals and preferred-vendor status.

EPR and packaging stewardship

Extended Producer Responsibility schemes shift waste-management costs to producers, with national EPR fees (often €100–€500/tonne) directly affecting packaging margins; Berry Global, with ~ $11.2bn revenue in 2024, must absorb or pass these costs. Fees tied to recyclability and material choice incentivize design-for-circularity, while EU PPWR proposals and the UK EPR (launched April 2024) make EPR a strategic pricing lever. Data-reporting obligations require robust traceability systems and capital investment in digital compliance.

Geopolitical supply chain risk

Geopolitical conflicts and sanctions since 2022 have disrupted feedstock flows and logistics lanes, driving resin spot-price swings of up to 50% during peak disruption periods and pressuring Berry Global’s supply costs and margins. Political instability in key resin-producing regions raises price volatility and transport risk, while governments increasingly favor local content rules that can force costly production localization. Scenario planning and inventory buffers are used to mitigate shocks and preserve continuity.

- Supply shocks: resin price swings up to 50%

- Localization risk: rising local-content mandates

- Mitigation: scenario planning, inventory buffers

- Impact: higher input-cost volatility for Berry Global

Public procurement and healthcare policy

Government healthcare spending — public payers account for roughly 50% of health expenditure in OECD countries — drives demand for medical and hygiene packaging, while EU public procurement represents about 14% of GDP, amplifying tender opportunities. Procurement rules increasingly embed sustainability and sterile/tamper-evident specifications, favoring certified suppliers and demanding cost-competitive compliance.

- Public spend ~50% of OECD health expenditure

- EU procurement ~14% of GDP

- Sustainability criteria rising

- Sterile/tamper-evident standards favor qualified suppliers

- Tenders require compliance + price competitiveness

Tariffs, geopolitics drive swings to 50%, squeezing $11.2bn

Trade tariffs (US Section 301 7.5–25%) and geopolitics drive resin cost volatility (spot swings up to 50%), pressuring Berry Global’s 2024 revenue base of ~$11.2bn. Plastic bans, EU SUPD and 127 national laws plus UK EPR (Apr 2024) and EPR fees (€100–€500/t) force circular-design and cost pass-through. Public healthcare procurement (~50% OECD; EU public spend ~14% GDP) increases demand but raises compliance burdens.

| Metric | Value |

|---|---|

| Revenue (2024) | $11.2bn |

| Tariff range | 7.5–25% |

| Resin volatility | Up to 50% |

| EPR fees | €100–€500/tonne |

What is included in the product

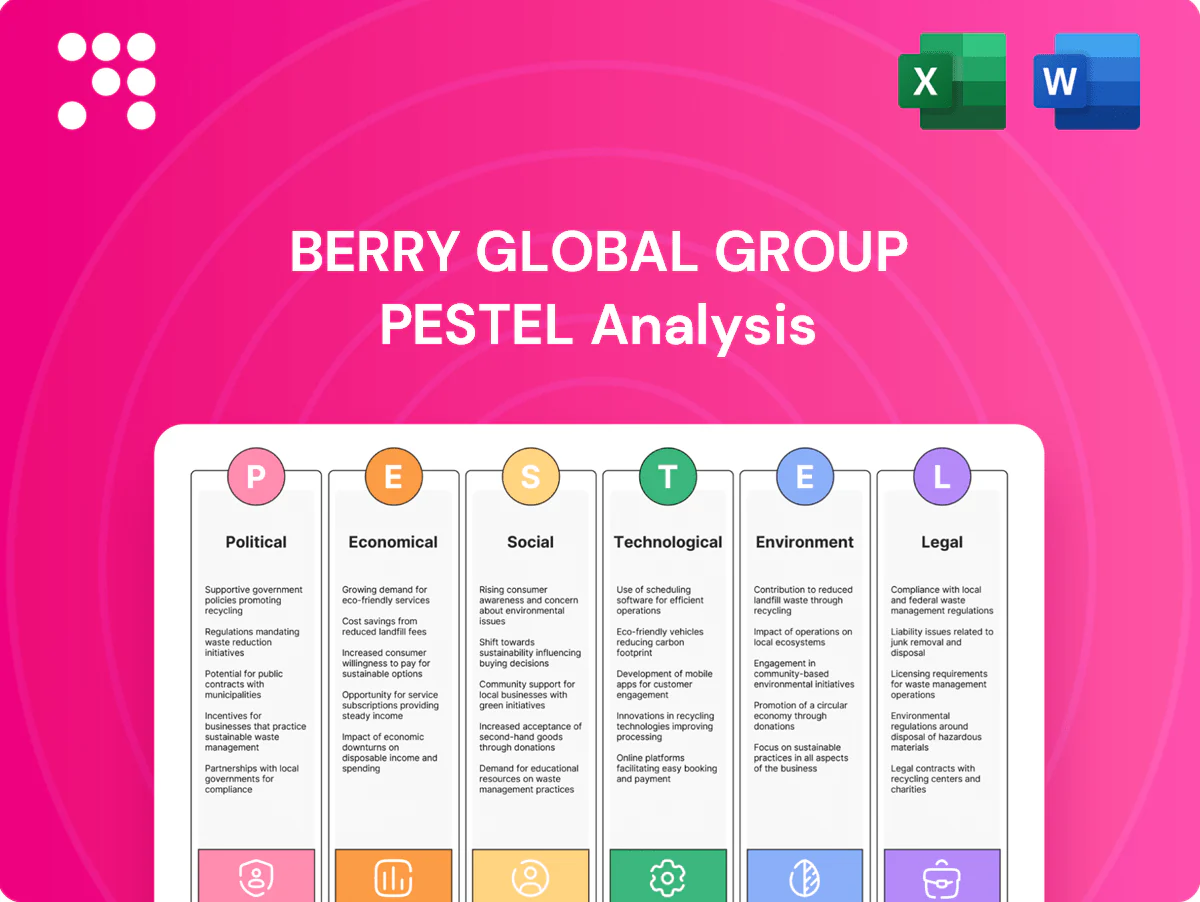

Explores how macro-environmental forces uniquely affect Berry Global Group across Political, Economic, Social, Technological, Environmental and Legal dimensions; data-backed, region- and industry-specific insights designed for executives and investors, with detailed sub-points and forward-looking scenarios to inform strategy and reporting.

A clean, summarized Berry Global Group PESTLE analysis, visually segmented by PESTEL categories for quick interpretation, that can be dropped into presentations or shared across teams to streamline discussions on external risk, market positioning, and strategic planning.

Economic factors

Resin and energy price volatility

Polyethylene, polypropylene and PET resin costs closely follow oil, gas and naphtha cycles; Brent averaged about $86/bl in 2024 and US Henry Hub near $3/MMBtu, driving feedstock-linked resin volatility. Input swings compress or expand Berry Global margins depending on how quickly price increases are passed through to customers. Energy costs materially affect extrusion and molding unit economics, raising variable costs during high energy periods. Hedging programs and formula pricing help stabilize cash flow and reduce margin volatility.

Consumer demand cycles

Packaging volumes track FMCG, e-commerce and personal care growth — global e-commerce sales reached about $6.3 trillion in 2023, supporting demand for transit and retail formats. Downturns shift buyers to value SKUs and lightweighting to cut cost and material use. Defensive end-markets such as healthcare (roughly 20% of some converters’ mixes) partially offset cyclicity. Accurate forecasts are vital for capacity utilization and working capital management.

FX and interest rates

Berry Global’s global revenues and costs expose it to currency translation and transaction risk, with a strong dollar in 2024–25 pressuring reported sales while often lowering imported resin and additive costs. Fed funds near 5.25–5.50% in mid-2025 raise financing costs for capex and inventory, tightening cash flow. Prudent leverage targets and active FX hedges help preserve strategic flexibility and borrowing capacity.

Emerging market growth

Rising middle classes in emerging markets are expanding packaged‑goods consumption as IMF projects EM and developing economy growth of about 4.3% in 2024 and 4.6% in 2025, supporting FMCG demand; infrastructure gaps and large informal retail sectors push demand toward smaller pack formats and lower price points. Resin availability and logistics volatility in 2024 raised polymer spot prices and freight costs, increasing cost‑to‑serve, while tailored product design and localized packs offer clear share‑gain opportunities for Berry.

- EM growth: IMF 4.3% (2024), 4.6% (2025)

- Pack formats: informal retail → smaller, low‑price packs

- Cost drivers: 2024 resin/transport volatility → higher cost‑to‑serve

- Strategy: localized design unlocks market share

Consolidation and buyer power

Large CPGs and retailers exert pricing pressure and push sustainability claims, squeezing margins even as Berry Global reported fiscal 2024 net sales of $13.8 billion; industry consolidation improves scale but attracts regulatory scrutiny. Long-term, indexed contracts stabilize volumes and resin-cost pass-through; product innovation and differentiated sustainable solutions support margin resilience.

Tariffs, geopolitics drive swings to 50%, squeezing $11.2bn

Feedstock-linked resin volatility (Brent ~$86/bl in 2024; Henry Hub ~$3/MMBtu) drives margin swings; hedging and formula pricing mitigate impact. Demand tied to FMCG/e‑commerce (global e‑commerce ~$6.3T in 2023) and EM growth (IMF 2024/25: 4.3%/4.6%), supporting volumes. Strong dollar and Fed funds ~5.25–5.50% (mid‑2025) raise financing costs; Berry fiscal 2024 net sales $13.8B.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bl |

| Henry Hub | $3/MMBtu |

| e‑commerce 2023 | $6.3T |

| Berry FY2024 sales | $13.8B |

Preview the Actual Deliverable

Berry Global Group PESTLE Analysis

The preview shown here is the exact Berry Global Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file contains the complete, professionally structured assessment of political, economic, social, technological, legal, and environmental factors affecting Berry Global. No placeholders or teasers—what you see is the final document available for immediate download.

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Berry Global Group reveals how political, economic, social, technological, legal, and environmental forces are reshaping the packaging leader’s strategy and risk profile. Gain actionable insights to anticipate regulatory shifts, supply-chain pressures, and sustainability trends. Purchase the full report for the complete, editable breakdown and immediate strategic value.

Political factors

Trade policy and tariffs

Shifts in US–China and EU trade policy, including US Section 301 tariffs that range from 7.5% to 25%, can materially change resin and machinery costs and pressure Berry Global’s margin stability. Tariffs on petrochemicals or packaging inputs effectively raise COGS by the tariff rate and complicate global sourcing and supply-chain planning. Favorable agreements such as USMCA (effective 1 July 2020) can open export markets but increase compliance burdens, so Berry must hedge exposure via diversified suppliers and regional production.

Single-use plastics regulation

Governments are tightening disposable-plastics rules—127 countries have national plastics laws and the EU Single-Use Plastics Directive (in force 2021) plus a 90% plastic-bottle collection target by 2029 are reshaping demand. Bans, taxes and mandates push Berry toward reusable/recyclable/compostable SKUs, raising SKU and formulation complexity; early policy alignment can secure approvals and preferred-vendor status.

EPR and packaging stewardship

Extended Producer Responsibility schemes shift waste-management costs to producers, with national EPR fees (often €100–€500/tonne) directly affecting packaging margins; Berry Global, with ~ $11.2bn revenue in 2024, must absorb or pass these costs. Fees tied to recyclability and material choice incentivize design-for-circularity, while EU PPWR proposals and the UK EPR (launched April 2024) make EPR a strategic pricing lever. Data-reporting obligations require robust traceability systems and capital investment in digital compliance.

Geopolitical supply chain risk

Geopolitical conflicts and sanctions since 2022 have disrupted feedstock flows and logistics lanes, driving resin spot-price swings of up to 50% during peak disruption periods and pressuring Berry Global’s supply costs and margins. Political instability in key resin-producing regions raises price volatility and transport risk, while governments increasingly favor local content rules that can force costly production localization. Scenario planning and inventory buffers are used to mitigate shocks and preserve continuity.

- Supply shocks: resin price swings up to 50%

- Localization risk: rising local-content mandates

- Mitigation: scenario planning, inventory buffers

- Impact: higher input-cost volatility for Berry Global

Public procurement and healthcare policy

Government healthcare spending — public payers account for roughly 50% of health expenditure in OECD countries — drives demand for medical and hygiene packaging, while EU public procurement represents about 14% of GDP, amplifying tender opportunities. Procurement rules increasingly embed sustainability and sterile/tamper-evident specifications, favoring certified suppliers and demanding cost-competitive compliance.

- Public spend ~50% of OECD health expenditure

- EU procurement ~14% of GDP

- Sustainability criteria rising

- Sterile/tamper-evident standards favor qualified suppliers

- Tenders require compliance + price competitiveness

Tariffs, geopolitics drive swings to 50%, squeezing $11.2bn

Trade tariffs (US Section 301 7.5–25%) and geopolitics drive resin cost volatility (spot swings up to 50%), pressuring Berry Global’s 2024 revenue base of ~$11.2bn. Plastic bans, EU SUPD and 127 national laws plus UK EPR (Apr 2024) and EPR fees (€100–€500/t) force circular-design and cost pass-through. Public healthcare procurement (~50% OECD; EU public spend ~14% GDP) increases demand but raises compliance burdens.

| Metric | Value |

|---|---|

| Revenue (2024) | $11.2bn |

| Tariff range | 7.5–25% |

| Resin volatility | Up to 50% |

| EPR fees | €100–€500/tonne |

What is included in the product

Explores how macro-environmental forces uniquely affect Berry Global Group across Political, Economic, Social, Technological, Environmental and Legal dimensions; data-backed, region- and industry-specific insights designed for executives and investors, with detailed sub-points and forward-looking scenarios to inform strategy and reporting.

A clean, summarized Berry Global Group PESTLE analysis, visually segmented by PESTEL categories for quick interpretation, that can be dropped into presentations or shared across teams to streamline discussions on external risk, market positioning, and strategic planning.

Economic factors

Resin and energy price volatility

Polyethylene, polypropylene and PET resin costs closely follow oil, gas and naphtha cycles; Brent averaged about $86/bl in 2024 and US Henry Hub near $3/MMBtu, driving feedstock-linked resin volatility. Input swings compress or expand Berry Global margins depending on how quickly price increases are passed through to customers. Energy costs materially affect extrusion and molding unit economics, raising variable costs during high energy periods. Hedging programs and formula pricing help stabilize cash flow and reduce margin volatility.

Consumer demand cycles

Packaging volumes track FMCG, e-commerce and personal care growth — global e-commerce sales reached about $6.3 trillion in 2023, supporting demand for transit and retail formats. Downturns shift buyers to value SKUs and lightweighting to cut cost and material use. Defensive end-markets such as healthcare (roughly 20% of some converters’ mixes) partially offset cyclicity. Accurate forecasts are vital for capacity utilization and working capital management.

FX and interest rates

Berry Global’s global revenues and costs expose it to currency translation and transaction risk, with a strong dollar in 2024–25 pressuring reported sales while often lowering imported resin and additive costs. Fed funds near 5.25–5.50% in mid-2025 raise financing costs for capex and inventory, tightening cash flow. Prudent leverage targets and active FX hedges help preserve strategic flexibility and borrowing capacity.

Emerging market growth

Rising middle classes in emerging markets are expanding packaged‑goods consumption as IMF projects EM and developing economy growth of about 4.3% in 2024 and 4.6% in 2025, supporting FMCG demand; infrastructure gaps and large informal retail sectors push demand toward smaller pack formats and lower price points. Resin availability and logistics volatility in 2024 raised polymer spot prices and freight costs, increasing cost‑to‑serve, while tailored product design and localized packs offer clear share‑gain opportunities for Berry.

- EM growth: IMF 4.3% (2024), 4.6% (2025)

- Pack formats: informal retail → smaller, low‑price packs

- Cost drivers: 2024 resin/transport volatility → higher cost‑to‑serve

- Strategy: localized design unlocks market share

Consolidation and buyer power

Large CPGs and retailers exert pricing pressure and push sustainability claims, squeezing margins even as Berry Global reported fiscal 2024 net sales of $13.8 billion; industry consolidation improves scale but attracts regulatory scrutiny. Long-term, indexed contracts stabilize volumes and resin-cost pass-through; product innovation and differentiated sustainable solutions support margin resilience.

Tariffs, geopolitics drive swings to 50%, squeezing $11.2bn

Feedstock-linked resin volatility (Brent ~$86/bl in 2024; Henry Hub ~$3/MMBtu) drives margin swings; hedging and formula pricing mitigate impact. Demand tied to FMCG/e‑commerce (global e‑commerce ~$6.3T in 2023) and EM growth (IMF 2024/25: 4.3%/4.6%), supporting volumes. Strong dollar and Fed funds ~5.25–5.50% (mid‑2025) raise financing costs; Berry fiscal 2024 net sales $13.8B.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bl |

| Henry Hub | $3/MMBtu |

| e‑commerce 2023 | $6.3T |

| Berry FY2024 sales | $13.8B |

Preview the Actual Deliverable

Berry Global Group PESTLE Analysis

The preview shown here is the exact Berry Global Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file contains the complete, professionally structured assessment of political, economic, social, technological, legal, and environmental factors affecting Berry Global. No placeholders or teasers—what you see is the final document available for immediate download.

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Berry Global Group reveals how political, economic, social, technological, legal, and environmental forces are reshaping the packaging leader’s strategy and risk profile. Gain actionable insights to anticipate regulatory shifts, supply-chain pressures, and sustainability trends. Purchase the full report for the complete, editable breakdown and immediate strategic value.

Political factors

Trade policy and tariffs

Shifts in US–China and EU trade policy, including US Section 301 tariffs that range from 7.5% to 25%, can materially change resin and machinery costs and pressure Berry Global’s margin stability. Tariffs on petrochemicals or packaging inputs effectively raise COGS by the tariff rate and complicate global sourcing and supply-chain planning. Favorable agreements such as USMCA (effective 1 July 2020) can open export markets but increase compliance burdens, so Berry must hedge exposure via diversified suppliers and regional production.

Single-use plastics regulation

Governments are tightening disposable-plastics rules—127 countries have national plastics laws and the EU Single-Use Plastics Directive (in force 2021) plus a 90% plastic-bottle collection target by 2029 are reshaping demand. Bans, taxes and mandates push Berry toward reusable/recyclable/compostable SKUs, raising SKU and formulation complexity; early policy alignment can secure approvals and preferred-vendor status.

EPR and packaging stewardship

Extended Producer Responsibility schemes shift waste-management costs to producers, with national EPR fees (often €100–€500/tonne) directly affecting packaging margins; Berry Global, with ~ $11.2bn revenue in 2024, must absorb or pass these costs. Fees tied to recyclability and material choice incentivize design-for-circularity, while EU PPWR proposals and the UK EPR (launched April 2024) make EPR a strategic pricing lever. Data-reporting obligations require robust traceability systems and capital investment in digital compliance.

Geopolitical supply chain risk

Geopolitical conflicts and sanctions since 2022 have disrupted feedstock flows and logistics lanes, driving resin spot-price swings of up to 50% during peak disruption periods and pressuring Berry Global’s supply costs and margins. Political instability in key resin-producing regions raises price volatility and transport risk, while governments increasingly favor local content rules that can force costly production localization. Scenario planning and inventory buffers are used to mitigate shocks and preserve continuity.

- Supply shocks: resin price swings up to 50%

- Localization risk: rising local-content mandates

- Mitigation: scenario planning, inventory buffers

- Impact: higher input-cost volatility for Berry Global

Public procurement and healthcare policy

Government healthcare spending — public payers account for roughly 50% of health expenditure in OECD countries — drives demand for medical and hygiene packaging, while EU public procurement represents about 14% of GDP, amplifying tender opportunities. Procurement rules increasingly embed sustainability and sterile/tamper-evident specifications, favoring certified suppliers and demanding cost-competitive compliance.

- Public spend ~50% of OECD health expenditure

- EU procurement ~14% of GDP

- Sustainability criteria rising

- Sterile/tamper-evident standards favor qualified suppliers

- Tenders require compliance + price competitiveness

Tariffs, geopolitics drive swings to 50%, squeezing $11.2bn

Trade tariffs (US Section 301 7.5–25%) and geopolitics drive resin cost volatility (spot swings up to 50%), pressuring Berry Global’s 2024 revenue base of ~$11.2bn. Plastic bans, EU SUPD and 127 national laws plus UK EPR (Apr 2024) and EPR fees (€100–€500/t) force circular-design and cost pass-through. Public healthcare procurement (~50% OECD; EU public spend ~14% GDP) increases demand but raises compliance burdens.

| Metric | Value |

|---|---|

| Revenue (2024) | $11.2bn |

| Tariff range | 7.5–25% |

| Resin volatility | Up to 50% |

| EPR fees | €100–€500/tonne |

What is included in the product

Explores how macro-environmental forces uniquely affect Berry Global Group across Political, Economic, Social, Technological, Environmental and Legal dimensions; data-backed, region- and industry-specific insights designed for executives and investors, with detailed sub-points and forward-looking scenarios to inform strategy and reporting.

A clean, summarized Berry Global Group PESTLE analysis, visually segmented by PESTEL categories for quick interpretation, that can be dropped into presentations or shared across teams to streamline discussions on external risk, market positioning, and strategic planning.

Economic factors

Resin and energy price volatility

Polyethylene, polypropylene and PET resin costs closely follow oil, gas and naphtha cycles; Brent averaged about $86/bl in 2024 and US Henry Hub near $3/MMBtu, driving feedstock-linked resin volatility. Input swings compress or expand Berry Global margins depending on how quickly price increases are passed through to customers. Energy costs materially affect extrusion and molding unit economics, raising variable costs during high energy periods. Hedging programs and formula pricing help stabilize cash flow and reduce margin volatility.

Consumer demand cycles

Packaging volumes track FMCG, e-commerce and personal care growth — global e-commerce sales reached about $6.3 trillion in 2023, supporting demand for transit and retail formats. Downturns shift buyers to value SKUs and lightweighting to cut cost and material use. Defensive end-markets such as healthcare (roughly 20% of some converters’ mixes) partially offset cyclicity. Accurate forecasts are vital for capacity utilization and working capital management.

FX and interest rates

Berry Global’s global revenues and costs expose it to currency translation and transaction risk, with a strong dollar in 2024–25 pressuring reported sales while often lowering imported resin and additive costs. Fed funds near 5.25–5.50% in mid-2025 raise financing costs for capex and inventory, tightening cash flow. Prudent leverage targets and active FX hedges help preserve strategic flexibility and borrowing capacity.

Emerging market growth

Rising middle classes in emerging markets are expanding packaged‑goods consumption as IMF projects EM and developing economy growth of about 4.3% in 2024 and 4.6% in 2025, supporting FMCG demand; infrastructure gaps and large informal retail sectors push demand toward smaller pack formats and lower price points. Resin availability and logistics volatility in 2024 raised polymer spot prices and freight costs, increasing cost‑to‑serve, while tailored product design and localized packs offer clear share‑gain opportunities for Berry.

- EM growth: IMF 4.3% (2024), 4.6% (2025)

- Pack formats: informal retail → smaller, low‑price packs

- Cost drivers: 2024 resin/transport volatility → higher cost‑to‑serve

- Strategy: localized design unlocks market share

Consolidation and buyer power

Large CPGs and retailers exert pricing pressure and push sustainability claims, squeezing margins even as Berry Global reported fiscal 2024 net sales of $13.8 billion; industry consolidation improves scale but attracts regulatory scrutiny. Long-term, indexed contracts stabilize volumes and resin-cost pass-through; product innovation and differentiated sustainable solutions support margin resilience.

Tariffs, geopolitics drive swings to 50%, squeezing $11.2bn

Feedstock-linked resin volatility (Brent ~$86/bl in 2024; Henry Hub ~$3/MMBtu) drives margin swings; hedging and formula pricing mitigate impact. Demand tied to FMCG/e‑commerce (global e‑commerce ~$6.3T in 2023) and EM growth (IMF 2024/25: 4.3%/4.6%), supporting volumes. Strong dollar and Fed funds ~5.25–5.50% (mid‑2025) raise financing costs; Berry fiscal 2024 net sales $13.8B.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bl |

| Henry Hub | $3/MMBtu |

| e‑commerce 2023 | $6.3T |

| Berry FY2024 sales | $13.8B |

Preview the Actual Deliverable

Berry Global Group PESTLE Analysis

The preview shown here is the exact Berry Global Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file contains the complete, professionally structured assessment of political, economic, social, technological, legal, and environmental factors affecting Berry Global. No placeholders or teasers—what you see is the final document available for immediate download.