Bharat Petroleum SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Bharat Petroleum leverages an extensive downstream network, strong brand recognition, and integrated operations, yet faces margin pressure from volatile crude prices and regulatory constraints. Rising demand for cleaner fuels and retail expansion offer growth levers, while competition and energy transition risks require strategic agility. Purchase the full SWOT analysis for a detailed, editable Word and Excel report to guide investment, strategy, and stakeholder presentations.

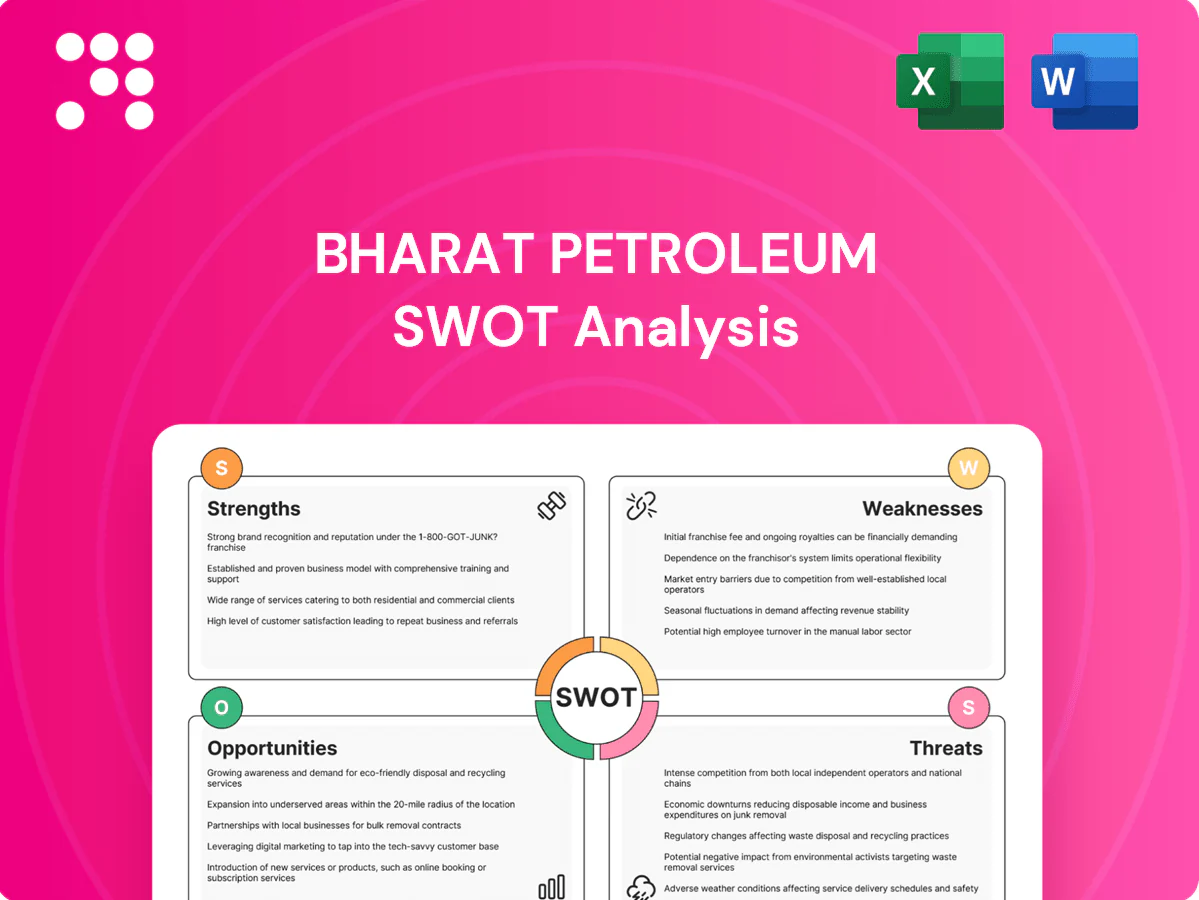

Strengths

Integrated refining-to-marketing footprint

Bharat Petroleum’s integrated refining-to-marketing footprint—two refineries at Mumbai and Kochi plus a nationwide retail network of over 16,000 outlets—enables end-to-end control from crude to pump, driving operational synergies and lower per‑unit costs. Integration cushions margins across cycles by optimizing crude sourcing and product slate adjustments at refinery level. Scale improves procurement bargaining, logistics efficiencies and resilient sales throughput.

Vast retail and distribution network

Bharat Petroleum’s vast retail and distribution network spans urban centers and remote rural locations through an extensive chain of fuel stations, LPG distributors, and lubricants outlets, driving high volumes and pervasive brand visibility. This reach increases customer stickiness via convenience and frequent touchpoints, reinforced by strong dealer relationships and efficient last-mile logistics. Data-driven pricing and loyalty schemes tie purchases to throughput improvements, optimizing margins and retention.

Strong brand and PSU credibility

Bharat Petroleum, a central public sector enterprise since 1976 and listed on NSE/BSE, has built long-term customer trust through decades of PSU stewardship and an established safety‑compliance record. Its government links boost access to institutional and government segment contracts and LPG distribution channels. The company’s operational coordination in emergencies underlines supply security and rapid response. This reputational strength aids retail fuel trust and LPG adoption.

Access to sovereign support and financing

Government majority stake (~53%) gives Bharat Petroleum sovereign support that lowers perceived credit risk and borrowing spreads, enabling access to low-cost capital for large refinery/upstream capex and strategic projects. State backing aids policy coordination and stabilises cashflow during crude-price shocks versus smaller peers.

- SoV stake ~53%

- Better borrowing terms vs smaller peers

- Access to capital for large capex

- Stabilises during price shocks

Diversifying into E&P and new energies

Bharat Petroleum, via its E&P arm Bharat PetroResources Limited, holds an international exploration and production portfolio that provides a direct hedge against upstream crude sourcing risk while securing feedstock optionality.

BPCL has initiated gas, biofuels, EV charging and green hydrogen pilots across refineries to position for the energy transition and to create feedstock and margin optionality for petrochemicals and specialty products.

- Hedge: direct E&P ownership

- New energies: gas, biofuels, EV charging, green H2 pilots

- Strategic goal: long-term transition positioning

- Optionality: petrochemicals and specialty products

State-backed refiner-marketer with 2 refineries, >16,000 outlets and green-energy optionality

Bharat Petroleum’s integrated refining-to-marketing model (2 refineries) plus a nationwide retail network (>16,000 outlets) drives scale, procurement leverage and margin resilience. Government majority stake (~53%) lowers borrowing costs and supports large capex. E&P arm Bharat PetroResources Ltd provides upstream feedstock optionality while new‑energy pilots (biofuels, EV charging, green H2) add transition optionality.

| Metric | Value |

|---|---|

| Retail outlets | >16,000 |

| Refineries | 2 (Mumbai, Kochi) |

| Government stake | ~53% |

| E&P arm | Bharat PetroResources Ltd |

What is included in the product

Delivers a strategic overview of Bharat Petroleum’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, operational resilience, and growth prospects in domestic and global energy markets.

Provides a concise SWOT matrix for Bharat Petroleum to quickly align strategy against market volatility, regulatory shifts, and operational bottlenecks.

Weaknesses

High dependence on imported crude

High import reliance exposes Bharat Petroleum to global supply disruptions, freight cost swings and currency volatility as India imports about 85% of its crude; INR averaged near ₹83/USD in 2023–24 increasing import bills. Sensitivity to crude-grade differentials (often $5–10/bbl between Brent/Dubai/heavy grades) squeezes refinery margins. Price spikes (Brent ~ $120/bbl in 2022) strain working capital and funding. Limited domestic crude (~15% of demand) limits feedstock flexibility.

Regulatory and pricing constraints

BPCL remains highly exposed to government pricing interventions and taxes, facing under-recovery risks during politically sensitive periods that can force below-market retail prices; LPG and auto-fuel margins have in recent cycles been compressed by policy caps and subsidy adjustments, reducing retail GRMs versus private refiners. Compliance complexity and slower commercial agility versus private peers impair rapid margin-restoration, weakening near-term profitability visibility.

Capex-intensive, aging assets

Capex-intensive operations demand major spending to upgrade refineries, improve energy efficiency and meet emissions norms; BPCL’s combined refining capacity of about 38.7 MMTPA concentrates these upgrade needs. Periodic turnarounds every 2–3 years cause utilization dips and revenue disruption. Legacy process configurations limit shift to higher-margin petrochemicals, while large-scale projects face execution and time-overrun risks.

Lower upstream scale vs. majors

Bharat Petroleum’s E&P portfolio is relatively small versus global majors, limiting natural hedges and leaving the company more exposed to product-margin swings; BPCL has lower influence over crude availability and quality, relying on market purchases. The company depends on partners for exploration learning curves and risk-sharing, constraining control and upside, and earnings remain concentrated in refining and marketing rather than upstream diversification.

- Limited E&P scale — weaker natural hedge

- Lower influence on crude supply/quality

- Dependence on partners for exploration/risks

- Earnings concentrated in refining & marketing

ESG and emissions intensity

Bharat Petroleum's refining and fuels business carries a high Scope 1–3 footprint, with Scope 3 generally accounting for over 90% of lifecycle emissions for liquid fuels, raising investor ESG screening and potential higher financing costs.

Significant capital expenditure is required for decarbonization and energy-efficiency retrofits; delays increase regulatory and reputational risks amid rising climate scrutiny.

- Scope 3 >90%

- Higher ESG screening/financing risk

- Large decarbonization CAPEX need

- Elevated reputational exposure

Import-reliant refiner faces margin squeeze and elevated ESG financing risk

Bharat Petroleum is heavily import-dependent (~85% crude imports; INR ~83/USD in 2023–24), squeezing margins via freight, FX and crude-grade differentials. Refining capacity ~38.7 MMTPA but limited E&P scale restricts natural hedge and upstream influence. High Scope 1–3 emissions (Scope 3 >90%) and large decarbonization CAPEX raise ESG and financing risk.

| Metric | Value |

|---|---|

| Crude import share | ~85% |

| Refining capacity | 38.7 MMTPA |

| INR avg 2023–24 | ~₹83/USD |

| Scope 3 emissions | >90% |

Full Version Awaits

Bharat Petroleum SWOT Analysis

This is a real excerpt from the complete Bharat Petroleum SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structure, findings, and editable format included in the download. Buy now to unlock the entire, detailed analysis for immediate use.

Dive Deeper Into the Company’s Strategic Blueprint

Bharat Petroleum leverages an extensive downstream network, strong brand recognition, and integrated operations, yet faces margin pressure from volatile crude prices and regulatory constraints. Rising demand for cleaner fuels and retail expansion offer growth levers, while competition and energy transition risks require strategic agility. Purchase the full SWOT analysis for a detailed, editable Word and Excel report to guide investment, strategy, and stakeholder presentations.

Strengths

Integrated refining-to-marketing footprint

Bharat Petroleum’s integrated refining-to-marketing footprint—two refineries at Mumbai and Kochi plus a nationwide retail network of over 16,000 outlets—enables end-to-end control from crude to pump, driving operational synergies and lower per‑unit costs. Integration cushions margins across cycles by optimizing crude sourcing and product slate adjustments at refinery level. Scale improves procurement bargaining, logistics efficiencies and resilient sales throughput.

Vast retail and distribution network

Bharat Petroleum’s vast retail and distribution network spans urban centers and remote rural locations through an extensive chain of fuel stations, LPG distributors, and lubricants outlets, driving high volumes and pervasive brand visibility. This reach increases customer stickiness via convenience and frequent touchpoints, reinforced by strong dealer relationships and efficient last-mile logistics. Data-driven pricing and loyalty schemes tie purchases to throughput improvements, optimizing margins and retention.

Strong brand and PSU credibility

Bharat Petroleum, a central public sector enterprise since 1976 and listed on NSE/BSE, has built long-term customer trust through decades of PSU stewardship and an established safety‑compliance record. Its government links boost access to institutional and government segment contracts and LPG distribution channels. The company’s operational coordination in emergencies underlines supply security and rapid response. This reputational strength aids retail fuel trust and LPG adoption.

Access to sovereign support and financing

Government majority stake (~53%) gives Bharat Petroleum sovereign support that lowers perceived credit risk and borrowing spreads, enabling access to low-cost capital for large refinery/upstream capex and strategic projects. State backing aids policy coordination and stabilises cashflow during crude-price shocks versus smaller peers.

- SoV stake ~53%

- Better borrowing terms vs smaller peers

- Access to capital for large capex

- Stabilises during price shocks

Diversifying into E&P and new energies

Bharat Petroleum, via its E&P arm Bharat PetroResources Limited, holds an international exploration and production portfolio that provides a direct hedge against upstream crude sourcing risk while securing feedstock optionality.

BPCL has initiated gas, biofuels, EV charging and green hydrogen pilots across refineries to position for the energy transition and to create feedstock and margin optionality for petrochemicals and specialty products.

- Hedge: direct E&P ownership

- New energies: gas, biofuels, EV charging, green H2 pilots

- Strategic goal: long-term transition positioning

- Optionality: petrochemicals and specialty products

State-backed refiner-marketer with 2 refineries, >16,000 outlets and green-energy optionality

Bharat Petroleum’s integrated refining-to-marketing model (2 refineries) plus a nationwide retail network (>16,000 outlets) drives scale, procurement leverage and margin resilience. Government majority stake (~53%) lowers borrowing costs and supports large capex. E&P arm Bharat PetroResources Ltd provides upstream feedstock optionality while new‑energy pilots (biofuels, EV charging, green H2) add transition optionality.

| Metric | Value |

|---|---|

| Retail outlets | >16,000 |

| Refineries | 2 (Mumbai, Kochi) |

| Government stake | ~53% |

| E&P arm | Bharat PetroResources Ltd |

What is included in the product

Delivers a strategic overview of Bharat Petroleum’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, operational resilience, and growth prospects in domestic and global energy markets.

Provides a concise SWOT matrix for Bharat Petroleum to quickly align strategy against market volatility, regulatory shifts, and operational bottlenecks.

Weaknesses

High dependence on imported crude

High import reliance exposes Bharat Petroleum to global supply disruptions, freight cost swings and currency volatility as India imports about 85% of its crude; INR averaged near ₹83/USD in 2023–24 increasing import bills. Sensitivity to crude-grade differentials (often $5–10/bbl between Brent/Dubai/heavy grades) squeezes refinery margins. Price spikes (Brent ~ $120/bbl in 2022) strain working capital and funding. Limited domestic crude (~15% of demand) limits feedstock flexibility.

Regulatory and pricing constraints

BPCL remains highly exposed to government pricing interventions and taxes, facing under-recovery risks during politically sensitive periods that can force below-market retail prices; LPG and auto-fuel margins have in recent cycles been compressed by policy caps and subsidy adjustments, reducing retail GRMs versus private refiners. Compliance complexity and slower commercial agility versus private peers impair rapid margin-restoration, weakening near-term profitability visibility.

Capex-intensive, aging assets

Capex-intensive operations demand major spending to upgrade refineries, improve energy efficiency and meet emissions norms; BPCL’s combined refining capacity of about 38.7 MMTPA concentrates these upgrade needs. Periodic turnarounds every 2–3 years cause utilization dips and revenue disruption. Legacy process configurations limit shift to higher-margin petrochemicals, while large-scale projects face execution and time-overrun risks.

Lower upstream scale vs. majors

Bharat Petroleum’s E&P portfolio is relatively small versus global majors, limiting natural hedges and leaving the company more exposed to product-margin swings; BPCL has lower influence over crude availability and quality, relying on market purchases. The company depends on partners for exploration learning curves and risk-sharing, constraining control and upside, and earnings remain concentrated in refining and marketing rather than upstream diversification.

- Limited E&P scale — weaker natural hedge

- Lower influence on crude supply/quality

- Dependence on partners for exploration/risks

- Earnings concentrated in refining & marketing

ESG and emissions intensity

Bharat Petroleum's refining and fuels business carries a high Scope 1–3 footprint, with Scope 3 generally accounting for over 90% of lifecycle emissions for liquid fuels, raising investor ESG screening and potential higher financing costs.

Significant capital expenditure is required for decarbonization and energy-efficiency retrofits; delays increase regulatory and reputational risks amid rising climate scrutiny.

- Scope 3 >90%

- Higher ESG screening/financing risk

- Large decarbonization CAPEX need

- Elevated reputational exposure

Import-reliant refiner faces margin squeeze and elevated ESG financing risk

Bharat Petroleum is heavily import-dependent (~85% crude imports; INR ~83/USD in 2023–24), squeezing margins via freight, FX and crude-grade differentials. Refining capacity ~38.7 MMTPA but limited E&P scale restricts natural hedge and upstream influence. High Scope 1–3 emissions (Scope 3 >90%) and large decarbonization CAPEX raise ESG and financing risk.

| Metric | Value |

|---|---|

| Crude import share | ~85% |

| Refining capacity | 38.7 MMTPA |

| INR avg 2023–24 | ~₹83/USD |

| Scope 3 emissions | >90% |

Full Version Awaits

Bharat Petroleum SWOT Analysis

This is a real excerpt from the complete Bharat Petroleum SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structure, findings, and editable format included in the download. Buy now to unlock the entire, detailed analysis for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Bharat Petroleum leverages an extensive downstream network, strong brand recognition, and integrated operations, yet faces margin pressure from volatile crude prices and regulatory constraints. Rising demand for cleaner fuels and retail expansion offer growth levers, while competition and energy transition risks require strategic agility. Purchase the full SWOT analysis for a detailed, editable Word and Excel report to guide investment, strategy, and stakeholder presentations.

Strengths

Integrated refining-to-marketing footprint

Bharat Petroleum’s integrated refining-to-marketing footprint—two refineries at Mumbai and Kochi plus a nationwide retail network of over 16,000 outlets—enables end-to-end control from crude to pump, driving operational synergies and lower per‑unit costs. Integration cushions margins across cycles by optimizing crude sourcing and product slate adjustments at refinery level. Scale improves procurement bargaining, logistics efficiencies and resilient sales throughput.

Vast retail and distribution network

Bharat Petroleum’s vast retail and distribution network spans urban centers and remote rural locations through an extensive chain of fuel stations, LPG distributors, and lubricants outlets, driving high volumes and pervasive brand visibility. This reach increases customer stickiness via convenience and frequent touchpoints, reinforced by strong dealer relationships and efficient last-mile logistics. Data-driven pricing and loyalty schemes tie purchases to throughput improvements, optimizing margins and retention.

Strong brand and PSU credibility

Bharat Petroleum, a central public sector enterprise since 1976 and listed on NSE/BSE, has built long-term customer trust through decades of PSU stewardship and an established safety‑compliance record. Its government links boost access to institutional and government segment contracts and LPG distribution channels. The company’s operational coordination in emergencies underlines supply security and rapid response. This reputational strength aids retail fuel trust and LPG adoption.

Access to sovereign support and financing

Government majority stake (~53%) gives Bharat Petroleum sovereign support that lowers perceived credit risk and borrowing spreads, enabling access to low-cost capital for large refinery/upstream capex and strategic projects. State backing aids policy coordination and stabilises cashflow during crude-price shocks versus smaller peers.

- SoV stake ~53%

- Better borrowing terms vs smaller peers

- Access to capital for large capex

- Stabilises during price shocks

Diversifying into E&P and new energies

Bharat Petroleum, via its E&P arm Bharat PetroResources Limited, holds an international exploration and production portfolio that provides a direct hedge against upstream crude sourcing risk while securing feedstock optionality.

BPCL has initiated gas, biofuels, EV charging and green hydrogen pilots across refineries to position for the energy transition and to create feedstock and margin optionality for petrochemicals and specialty products.

- Hedge: direct E&P ownership

- New energies: gas, biofuels, EV charging, green H2 pilots

- Strategic goal: long-term transition positioning

- Optionality: petrochemicals and specialty products

State-backed refiner-marketer with 2 refineries, >16,000 outlets and green-energy optionality

Bharat Petroleum’s integrated refining-to-marketing model (2 refineries) plus a nationwide retail network (>16,000 outlets) drives scale, procurement leverage and margin resilience. Government majority stake (~53%) lowers borrowing costs and supports large capex. E&P arm Bharat PetroResources Ltd provides upstream feedstock optionality while new‑energy pilots (biofuels, EV charging, green H2) add transition optionality.

| Metric | Value |

|---|---|

| Retail outlets | >16,000 |

| Refineries | 2 (Mumbai, Kochi) |

| Government stake | ~53% |

| E&P arm | Bharat PetroResources Ltd |

What is included in the product

Delivers a strategic overview of Bharat Petroleum’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, operational resilience, and growth prospects in domestic and global energy markets.

Provides a concise SWOT matrix for Bharat Petroleum to quickly align strategy against market volatility, regulatory shifts, and operational bottlenecks.

Weaknesses

High dependence on imported crude

High import reliance exposes Bharat Petroleum to global supply disruptions, freight cost swings and currency volatility as India imports about 85% of its crude; INR averaged near ₹83/USD in 2023–24 increasing import bills. Sensitivity to crude-grade differentials (often $5–10/bbl between Brent/Dubai/heavy grades) squeezes refinery margins. Price spikes (Brent ~ $120/bbl in 2022) strain working capital and funding. Limited domestic crude (~15% of demand) limits feedstock flexibility.

Regulatory and pricing constraints

BPCL remains highly exposed to government pricing interventions and taxes, facing under-recovery risks during politically sensitive periods that can force below-market retail prices; LPG and auto-fuel margins have in recent cycles been compressed by policy caps and subsidy adjustments, reducing retail GRMs versus private refiners. Compliance complexity and slower commercial agility versus private peers impair rapid margin-restoration, weakening near-term profitability visibility.

Capex-intensive, aging assets

Capex-intensive operations demand major spending to upgrade refineries, improve energy efficiency and meet emissions norms; BPCL’s combined refining capacity of about 38.7 MMTPA concentrates these upgrade needs. Periodic turnarounds every 2–3 years cause utilization dips and revenue disruption. Legacy process configurations limit shift to higher-margin petrochemicals, while large-scale projects face execution and time-overrun risks.

Lower upstream scale vs. majors

Bharat Petroleum’s E&P portfolio is relatively small versus global majors, limiting natural hedges and leaving the company more exposed to product-margin swings; BPCL has lower influence over crude availability and quality, relying on market purchases. The company depends on partners for exploration learning curves and risk-sharing, constraining control and upside, and earnings remain concentrated in refining and marketing rather than upstream diversification.

- Limited E&P scale — weaker natural hedge

- Lower influence on crude supply/quality

- Dependence on partners for exploration/risks

- Earnings concentrated in refining & marketing

ESG and emissions intensity

Bharat Petroleum's refining and fuels business carries a high Scope 1–3 footprint, with Scope 3 generally accounting for over 90% of lifecycle emissions for liquid fuels, raising investor ESG screening and potential higher financing costs.

Significant capital expenditure is required for decarbonization and energy-efficiency retrofits; delays increase regulatory and reputational risks amid rising climate scrutiny.

- Scope 3 >90%

- Higher ESG screening/financing risk

- Large decarbonization CAPEX need

- Elevated reputational exposure

Import-reliant refiner faces margin squeeze and elevated ESG financing risk

Bharat Petroleum is heavily import-dependent (~85% crude imports; INR ~83/USD in 2023–24), squeezing margins via freight, FX and crude-grade differentials. Refining capacity ~38.7 MMTPA but limited E&P scale restricts natural hedge and upstream influence. High Scope 1–3 emissions (Scope 3 >90%) and large decarbonization CAPEX raise ESG and financing risk.

| Metric | Value |

|---|---|

| Crude import share | ~85% |

| Refining capacity | 38.7 MMTPA |

| INR avg 2023–24 | ~₹83/USD |

| Scope 3 emissions | >90% |

Full Version Awaits

Bharat Petroleum SWOT Analysis

This is a real excerpt from the complete Bharat Petroleum SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structure, findings, and editable format included in the download. Buy now to unlock the entire, detailed analysis for immediate use.