Big 5 SWOT Analysis

Make Insightful Decisions Backed by Expert Research

The Big 5 SWOT Analysis distills five critical dimensions shaping the company’s competitive edge, vulnerabilities, market opportunities, and external threats in clear, actionable terms. This concise preview highlights key takeaways for investors and strategists, but the full report delivers in-depth evidence, expert commentary, and editable Word and Excel deliverables. Purchase the complete SWOT to strategize, present, and invest with confidence.

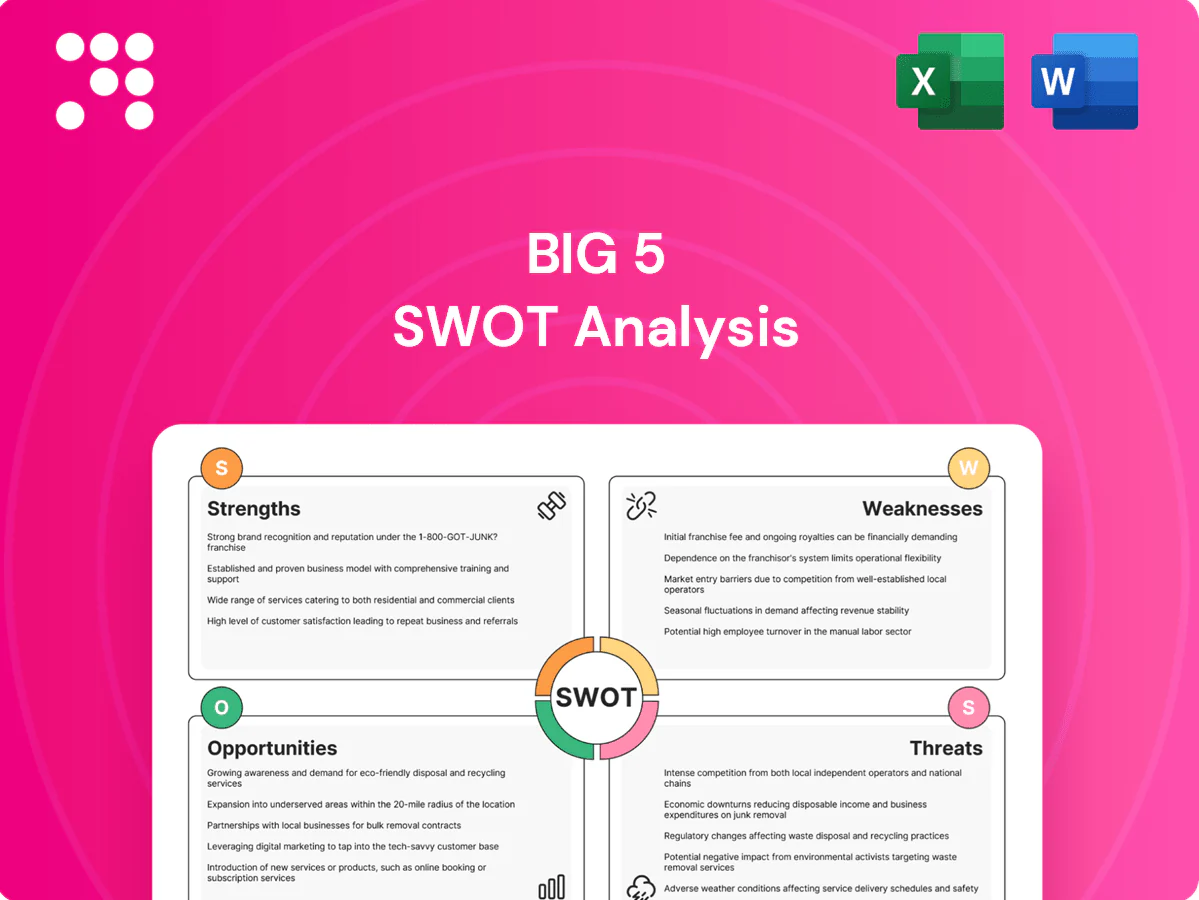

Strengths

Value-focused positioning

Big 5 targets price-sensitive shoppers with everyday value and frequent promotions, aligning assortment to budget-conscious families and teams and operating ≈400 stores as of 2024; this core focus drives repeat trips. The value positioning supports steady traffic during slowdowns, with value-led retailers showing roughly 5–8% resilience in visits in 2023–24. Clear price ladders and good-better-best widen appeal without alienating core buyers and enable quick competitive responses to discounters.

Broad multi-category assortment

Big 5’s broad assortment—team sports, fitness, camping, hunting, fishing, recreation plus footwear and apparel—across over 250 stores diversifies demand across seasons and participation trends. This mix promotes basket-building and cross-selling, lifting average transaction value and offsetting category-specific downturns. It reduces reliance on any single sport or vendor, smoothing revenue volatility in a US sporting goods market that exceeded $50 billion in 2023.

Neighborhood store footprint

Neighborhood footprint of Big 5, with about 434 stores, enables convenient mid-sized formats for quick trips and BOPIS, supporting last-minute purchases for practices or trips; proximity drives event-driven sales and higher basket conversion. Local staff tailor recommendations to regional activities, improving service metrics and loyalty versus pure-play online rivals. This accessibility complements omnichannel revenue streams and reduces last-mile frictions.

Private-label and value brands

Private-label and value brands deliver clear price advantages and typically boost gross margins by about 5–15 percentage points; in 2024 industry averages private-label penetration for value-focused chains was roughly 15–25%, reducing direct comparability with Amazon and big-box rivals. They plug assortment gaps when branded allocations tighten and distinctive value SKUs helped defend traffic during 2024 promotional peaks.

- Higher gross margins: +5–15 ppt

- Share: ~15–25% (2024)

- Defends traffic in promo periods

Outdoor and recreation expertise

Deep expertise in camping, hunting and fishing differentiates the Big 5 chain from generalist retailers, driving category-specific loyalty and higher basket sizes.

Knowledgeable associates and compliant processes for regulated categories build trust and reduce risk; store training hours rose industrywide through 2024.

Assortment matches rising outdoor participation and technical accessories plus consumables (ammo, tackle, fuel) produce frequent repeat visits and steady margin contribution.

- Category expertise

- Regulatory compliance

- Assortment fit with participation trends

- Repeat-purchase consumables

Local sports retailer - ≈434 stores; private-label 15–25%

Big 5’s value positioning and frequent promotions drive repeat trips across ≈434 stores (2024), with private-label penetration ~15–25% and gross-margin uplift of +5–15 ppt. Broad assortment across team sports, outdoor and consumables leverages a >$50B US market (2023) and 5–8% visit resilience in 2023–24. Local footprint and category expertise boost conversion and BOPIS-led convenience.

| Metric | 2023–24 |

|---|---|

| Stores | ≈434 (2024) |

| Private-label | 15–25% |

| Gross-margin uplift | +5–15 ppt |

| Market size | >$50B (2023) |

| Visit resilience | 5–8% |

What is included in the product

Provides a concise SWOT analysis of Big 5, highlighting internal strengths and weaknesses along with external opportunities and threats that shape its competitive position and growth prospects.

Provides a focused Big 5 SWOT summary to cut through analysis paralysis and prioritize the top strategic levers; compact, visual layout speeds stakeholder alignment and decision-making.

Weaknesses

Regional concentration

Concentration in Western U.S. markets heightens exposure to severe weather, wildfires and localized economic downturns, amplifying sales volatility and insurance costs. Limited national scale weakens vendor negotiating power and pricing flexibility. Pronounced regional seasonality increases inventory swings and markdown risk. Scaling beyond the region likely demands substantial capital to replicate local supply chains and customer knowledge.

Scale disadvantages vs. national chains

Scale disadvantages vs national chains squeeze Big 5: larger rivals like Amazon (net sales >$500B in 2024) negotiate lower COGS, secure exclusive allocations and wider media reach, compressing gross margins and forcing deeper promotions. Advertising efficiency and fulfillment density at national peers lower customer acquisition and shipping costs, harming omnichannel economics. Slower delivery speed and higher per-order shipping expense limit competitiveness on e-commerce and same-day fulfillment.

High promotion dependency

Value positioning often leans on coupons and weekly deals to drive footfall, training customers to wait for promotions and eroding pricing power. Promotional cadence typically cuts gross margins 200–400 basis points in peak periods and complicates demand forecasting and inventory turns. Price transparency online accelerates promo frequency, increasing stockouts and markdowns. This dependency inflates marketing spend and short-term sales volatility.

Seasonality and weather sensitivity

Sales for camping, team sports, and winter gear swing with school calendars and climate, concentrating revenue in spring/summer and late fall/winter and increasing markdown risk when weather is unseasonable; carryover inventory and promotional discounts compress gross margins and raise holding costs. Working capital requirements surge ahead of peak seasons, while fluctuating demand complicates store labor scheduling and reduces workforce productivity.

- Seasonal revenue concentration

- Unseasonable weather → markdowns/carryover inventory

- Pre-peak spike in working capital needs

- Harder to optimize store labor

Regulated categories complexity

- Compliance intensity: mandatory background checks and recordkeeping

- Transaction friction: slower sales, higher abandonment risk

- Cost exposure: higher overhead vs non-regulated SKUs

- Regulatory risk: profitability can change quickly with rule shifts

Western concentration and wildfire exposure squeeze margins; promos cut 200–400 bps

Concentration in Western U.S. markets increases weather and wildfire exposure, raising insurance and sales volatility. Scale gap vs national peers (Amazon net sales >500B in 2024) compresses margins and raises fulfillment costs. Promotional cadence cuts gross margin ~200–400 bps and heightens inventory risk. Regulated SKUs face friction and cost pressure (20M NICS checks in 2023).

| Metric | Value |

|---|---|

| Promo margin drag | 200–400 bps |

| Amazon net sales (2024) | >500B |

| NICS checks (2023) | 20M |

Preview Before You Purchase

Big 5 SWOT Analysis

This Big 5 SWOT Analysis preview is the actual document you’ll receive upon purchase—no surprises, just professional quality. The content shown is pulled directly from the full report. Buy now to unlock the complete, editable version.

Make Insightful Decisions Backed by Expert Research

The Big 5 SWOT Analysis distills five critical dimensions shaping the company’s competitive edge, vulnerabilities, market opportunities, and external threats in clear, actionable terms. This concise preview highlights key takeaways for investors and strategists, but the full report delivers in-depth evidence, expert commentary, and editable Word and Excel deliverables. Purchase the complete SWOT to strategize, present, and invest with confidence.

Strengths

Value-focused positioning

Big 5 targets price-sensitive shoppers with everyday value and frequent promotions, aligning assortment to budget-conscious families and teams and operating ≈400 stores as of 2024; this core focus drives repeat trips. The value positioning supports steady traffic during slowdowns, with value-led retailers showing roughly 5–8% resilience in visits in 2023–24. Clear price ladders and good-better-best widen appeal without alienating core buyers and enable quick competitive responses to discounters.

Broad multi-category assortment

Big 5’s broad assortment—team sports, fitness, camping, hunting, fishing, recreation plus footwear and apparel—across over 250 stores diversifies demand across seasons and participation trends. This mix promotes basket-building and cross-selling, lifting average transaction value and offsetting category-specific downturns. It reduces reliance on any single sport or vendor, smoothing revenue volatility in a US sporting goods market that exceeded $50 billion in 2023.

Neighborhood store footprint

Neighborhood footprint of Big 5, with about 434 stores, enables convenient mid-sized formats for quick trips and BOPIS, supporting last-minute purchases for practices or trips; proximity drives event-driven sales and higher basket conversion. Local staff tailor recommendations to regional activities, improving service metrics and loyalty versus pure-play online rivals. This accessibility complements omnichannel revenue streams and reduces last-mile frictions.

Private-label and value brands

Private-label and value brands deliver clear price advantages and typically boost gross margins by about 5–15 percentage points; in 2024 industry averages private-label penetration for value-focused chains was roughly 15–25%, reducing direct comparability with Amazon and big-box rivals. They plug assortment gaps when branded allocations tighten and distinctive value SKUs helped defend traffic during 2024 promotional peaks.

- Higher gross margins: +5–15 ppt

- Share: ~15–25% (2024)

- Defends traffic in promo periods

Outdoor and recreation expertise

Deep expertise in camping, hunting and fishing differentiates the Big 5 chain from generalist retailers, driving category-specific loyalty and higher basket sizes.

Knowledgeable associates and compliant processes for regulated categories build trust and reduce risk; store training hours rose industrywide through 2024.

Assortment matches rising outdoor participation and technical accessories plus consumables (ammo, tackle, fuel) produce frequent repeat visits and steady margin contribution.

- Category expertise

- Regulatory compliance

- Assortment fit with participation trends

- Repeat-purchase consumables

Local sports retailer - ≈434 stores; private-label 15–25%

Big 5’s value positioning and frequent promotions drive repeat trips across ≈434 stores (2024), with private-label penetration ~15–25% and gross-margin uplift of +5–15 ppt. Broad assortment across team sports, outdoor and consumables leverages a >$50B US market (2023) and 5–8% visit resilience in 2023–24. Local footprint and category expertise boost conversion and BOPIS-led convenience.

| Metric | 2023–24 |

|---|---|

| Stores | ≈434 (2024) |

| Private-label | 15–25% |

| Gross-margin uplift | +5–15 ppt |

| Market size | >$50B (2023) |

| Visit resilience | 5–8% |

What is included in the product

Provides a concise SWOT analysis of Big 5, highlighting internal strengths and weaknesses along with external opportunities and threats that shape its competitive position and growth prospects.

Provides a focused Big 5 SWOT summary to cut through analysis paralysis and prioritize the top strategic levers; compact, visual layout speeds stakeholder alignment and decision-making.

Weaknesses

Regional concentration

Concentration in Western U.S. markets heightens exposure to severe weather, wildfires and localized economic downturns, amplifying sales volatility and insurance costs. Limited national scale weakens vendor negotiating power and pricing flexibility. Pronounced regional seasonality increases inventory swings and markdown risk. Scaling beyond the region likely demands substantial capital to replicate local supply chains and customer knowledge.

Scale disadvantages vs. national chains

Scale disadvantages vs national chains squeeze Big 5: larger rivals like Amazon (net sales >$500B in 2024) negotiate lower COGS, secure exclusive allocations and wider media reach, compressing gross margins and forcing deeper promotions. Advertising efficiency and fulfillment density at national peers lower customer acquisition and shipping costs, harming omnichannel economics. Slower delivery speed and higher per-order shipping expense limit competitiveness on e-commerce and same-day fulfillment.

High promotion dependency

Value positioning often leans on coupons and weekly deals to drive footfall, training customers to wait for promotions and eroding pricing power. Promotional cadence typically cuts gross margins 200–400 basis points in peak periods and complicates demand forecasting and inventory turns. Price transparency online accelerates promo frequency, increasing stockouts and markdowns. This dependency inflates marketing spend and short-term sales volatility.

Seasonality and weather sensitivity

Sales for camping, team sports, and winter gear swing with school calendars and climate, concentrating revenue in spring/summer and late fall/winter and increasing markdown risk when weather is unseasonable; carryover inventory and promotional discounts compress gross margins and raise holding costs. Working capital requirements surge ahead of peak seasons, while fluctuating demand complicates store labor scheduling and reduces workforce productivity.

- Seasonal revenue concentration

- Unseasonable weather → markdowns/carryover inventory

- Pre-peak spike in working capital needs

- Harder to optimize store labor

Regulated categories complexity

- Compliance intensity: mandatory background checks and recordkeeping

- Transaction friction: slower sales, higher abandonment risk

- Cost exposure: higher overhead vs non-regulated SKUs

- Regulatory risk: profitability can change quickly with rule shifts

Western concentration and wildfire exposure squeeze margins; promos cut 200–400 bps

Concentration in Western U.S. markets increases weather and wildfire exposure, raising insurance and sales volatility. Scale gap vs national peers (Amazon net sales >500B in 2024) compresses margins and raises fulfillment costs. Promotional cadence cuts gross margin ~200–400 bps and heightens inventory risk. Regulated SKUs face friction and cost pressure (20M NICS checks in 2023).

| Metric | Value |

|---|---|

| Promo margin drag | 200–400 bps |

| Amazon net sales (2024) | >500B |

| NICS checks (2023) | 20M |

Preview Before You Purchase

Big 5 SWOT Analysis

This Big 5 SWOT Analysis preview is the actual document you’ll receive upon purchase—no surprises, just professional quality. The content shown is pulled directly from the full report. Buy now to unlock the complete, editable version.

Description

Make Insightful Decisions Backed by Expert Research

The Big 5 SWOT Analysis distills five critical dimensions shaping the company’s competitive edge, vulnerabilities, market opportunities, and external threats in clear, actionable terms. This concise preview highlights key takeaways for investors and strategists, but the full report delivers in-depth evidence, expert commentary, and editable Word and Excel deliverables. Purchase the complete SWOT to strategize, present, and invest with confidence.

Strengths

Value-focused positioning

Big 5 targets price-sensitive shoppers with everyday value and frequent promotions, aligning assortment to budget-conscious families and teams and operating ≈400 stores as of 2024; this core focus drives repeat trips. The value positioning supports steady traffic during slowdowns, with value-led retailers showing roughly 5–8% resilience in visits in 2023–24. Clear price ladders and good-better-best widen appeal without alienating core buyers and enable quick competitive responses to discounters.

Broad multi-category assortment

Big 5’s broad assortment—team sports, fitness, camping, hunting, fishing, recreation plus footwear and apparel—across over 250 stores diversifies demand across seasons and participation trends. This mix promotes basket-building and cross-selling, lifting average transaction value and offsetting category-specific downturns. It reduces reliance on any single sport or vendor, smoothing revenue volatility in a US sporting goods market that exceeded $50 billion in 2023.

Neighborhood store footprint

Neighborhood footprint of Big 5, with about 434 stores, enables convenient mid-sized formats for quick trips and BOPIS, supporting last-minute purchases for practices or trips; proximity drives event-driven sales and higher basket conversion. Local staff tailor recommendations to regional activities, improving service metrics and loyalty versus pure-play online rivals. This accessibility complements omnichannel revenue streams and reduces last-mile frictions.

Private-label and value brands

Private-label and value brands deliver clear price advantages and typically boost gross margins by about 5–15 percentage points; in 2024 industry averages private-label penetration for value-focused chains was roughly 15–25%, reducing direct comparability with Amazon and big-box rivals. They plug assortment gaps when branded allocations tighten and distinctive value SKUs helped defend traffic during 2024 promotional peaks.

- Higher gross margins: +5–15 ppt

- Share: ~15–25% (2024)

- Defends traffic in promo periods

Outdoor and recreation expertise

Deep expertise in camping, hunting and fishing differentiates the Big 5 chain from generalist retailers, driving category-specific loyalty and higher basket sizes.

Knowledgeable associates and compliant processes for regulated categories build trust and reduce risk; store training hours rose industrywide through 2024.

Assortment matches rising outdoor participation and technical accessories plus consumables (ammo, tackle, fuel) produce frequent repeat visits and steady margin contribution.

- Category expertise

- Regulatory compliance

- Assortment fit with participation trends

- Repeat-purchase consumables

Local sports retailer - ≈434 stores; private-label 15–25%

Big 5’s value positioning and frequent promotions drive repeat trips across ≈434 stores (2024), with private-label penetration ~15–25% and gross-margin uplift of +5–15 ppt. Broad assortment across team sports, outdoor and consumables leverages a >$50B US market (2023) and 5–8% visit resilience in 2023–24. Local footprint and category expertise boost conversion and BOPIS-led convenience.

| Metric | 2023–24 |

|---|---|

| Stores | ≈434 (2024) |

| Private-label | 15–25% |

| Gross-margin uplift | +5–15 ppt |

| Market size | >$50B (2023) |

| Visit resilience | 5–8% |

What is included in the product

Provides a concise SWOT analysis of Big 5, highlighting internal strengths and weaknesses along with external opportunities and threats that shape its competitive position and growth prospects.

Provides a focused Big 5 SWOT summary to cut through analysis paralysis and prioritize the top strategic levers; compact, visual layout speeds stakeholder alignment and decision-making.

Weaknesses

Regional concentration

Concentration in Western U.S. markets heightens exposure to severe weather, wildfires and localized economic downturns, amplifying sales volatility and insurance costs. Limited national scale weakens vendor negotiating power and pricing flexibility. Pronounced regional seasonality increases inventory swings and markdown risk. Scaling beyond the region likely demands substantial capital to replicate local supply chains and customer knowledge.

Scale disadvantages vs. national chains

Scale disadvantages vs national chains squeeze Big 5: larger rivals like Amazon (net sales >$500B in 2024) negotiate lower COGS, secure exclusive allocations and wider media reach, compressing gross margins and forcing deeper promotions. Advertising efficiency and fulfillment density at national peers lower customer acquisition and shipping costs, harming omnichannel economics. Slower delivery speed and higher per-order shipping expense limit competitiveness on e-commerce and same-day fulfillment.

High promotion dependency

Value positioning often leans on coupons and weekly deals to drive footfall, training customers to wait for promotions and eroding pricing power. Promotional cadence typically cuts gross margins 200–400 basis points in peak periods and complicates demand forecasting and inventory turns. Price transparency online accelerates promo frequency, increasing stockouts and markdowns. This dependency inflates marketing spend and short-term sales volatility.

Seasonality and weather sensitivity

Sales for camping, team sports, and winter gear swing with school calendars and climate, concentrating revenue in spring/summer and late fall/winter and increasing markdown risk when weather is unseasonable; carryover inventory and promotional discounts compress gross margins and raise holding costs. Working capital requirements surge ahead of peak seasons, while fluctuating demand complicates store labor scheduling and reduces workforce productivity.

- Seasonal revenue concentration

- Unseasonable weather → markdowns/carryover inventory

- Pre-peak spike in working capital needs

- Harder to optimize store labor

Regulated categories complexity

- Compliance intensity: mandatory background checks and recordkeeping

- Transaction friction: slower sales, higher abandonment risk

- Cost exposure: higher overhead vs non-regulated SKUs

- Regulatory risk: profitability can change quickly with rule shifts

Western concentration and wildfire exposure squeeze margins; promos cut 200–400 bps

Concentration in Western U.S. markets increases weather and wildfire exposure, raising insurance and sales volatility. Scale gap vs national peers (Amazon net sales >500B in 2024) compresses margins and raises fulfillment costs. Promotional cadence cuts gross margin ~200–400 bps and heightens inventory risk. Regulated SKUs face friction and cost pressure (20M NICS checks in 2023).

| Metric | Value |

|---|---|

| Promo margin drag | 200–400 bps |

| Amazon net sales (2024) | >500B |

| NICS checks (2023) | 20M |

Preview Before You Purchase

Big 5 SWOT Analysis

This Big 5 SWOT Analysis preview is the actual document you’ll receive upon purchase—no surprises, just professional quality. The content shown is pulled directly from the full report. Buy now to unlock the complete, editable version.