Bio-Techne PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

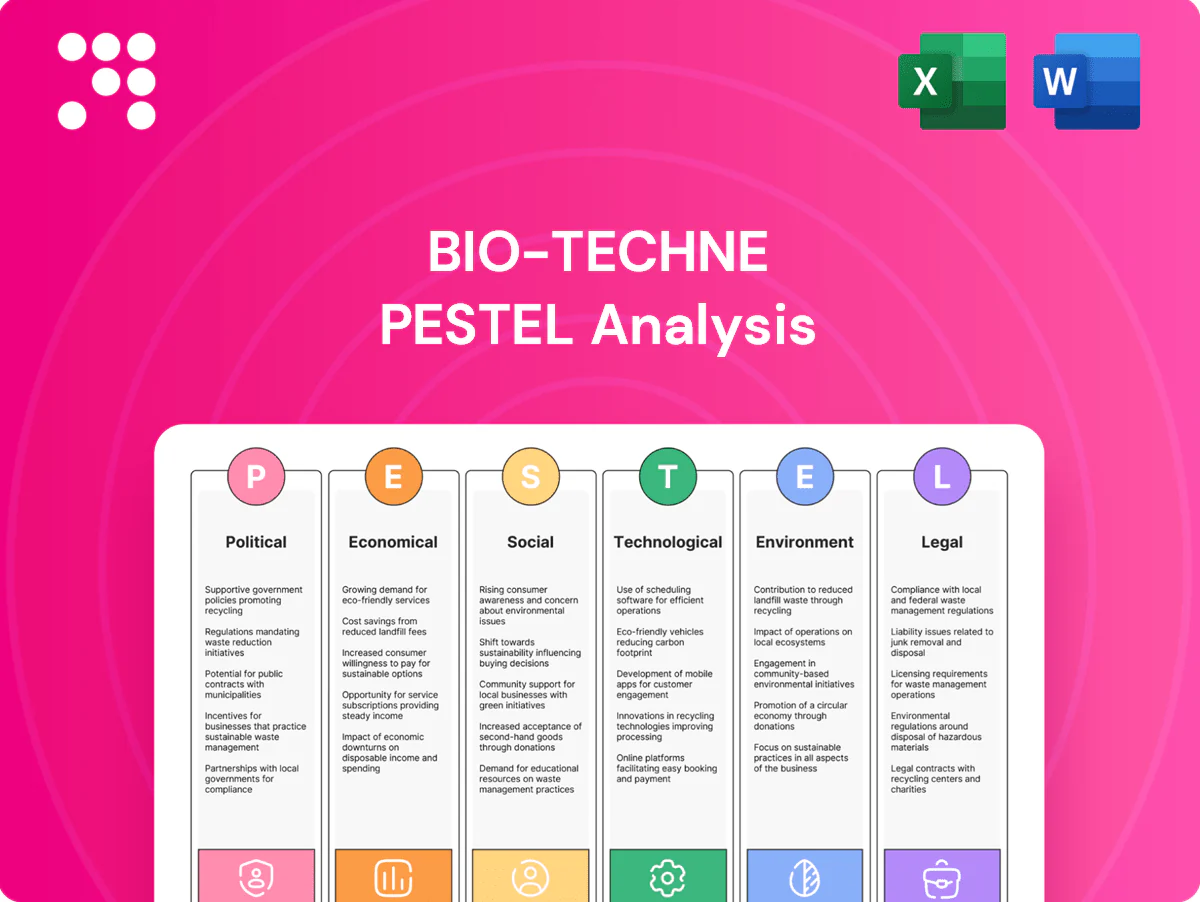

Unlock strategic clarity with our PESTLE Analysis of Bio‑Techne—three to five expert lenses on political, economic, social, technological, legal, and environmental forces shaping its future. Use these insights to anticipate risks and spot growth opportunities for investment or strategy. Purchase the full, editable report now for the complete, actionable deep dive.

Political factors

Public R&D funding and health policy

Government priorities for biomedical research directly shape demand for reagents and instruments, driven by major funding pools such as NIH (roughly $49.9B in FY2024) and EU Horizon Europe (€95.5B 2021–27). Shifts toward pandemic preparedness, oncology or rare-disease grants reallocate procurement and can change Bio-Techne product mix. Health policy favoring diagnostics and precision medicine increases clinical instrument uptake, so Bio-Techne must align portfolio and grant support to these policy themes.

Regulatory harmonization and international standards

Divergent rules across the US, EU and China — e.g., FDA 180-day PMA target, EU IVDR effective May 26, 2022, and NMPA local testing/registration requirements — affect product registration, labeling and QC standards. Fragmentation raises compliance costs and time-to-market; harmonization can shorten approvals versus fragmented pathways in large IVD market ~$90–95B in 2024. Active participation in ISO/IEC and regulatory bodies helps shape assay validation norms; strategic localization meets country-specific mandates and reduces launch delays.

Geopolitical trade and supply chain resilience

Tariffs and Section 301 measures on roughly $370B of goods (rates 7.5–25%) and tightening US export controls since 2022 can raise costs for enzymes, antibodies and electronics and limit access to advanced chips. Geopolitical tensions risk supply of rare reagents and semiconductor components; dual‑use controls (expanded 2022–24) constrain genomic/advanced instruments. Multi‑sourcing and regional manufacturing reduce exposure.

Government incentives for biomanufacturing

Industrial policies promoting domestic bioproduction and advanced therapeutics manufacturing unlock subsidies and tax credits, with governments committing over $10 billion globally to biomanufacturing scale-up since 2020, raising procurement-backed demand for suppliers like Bio-Techne.

Cluster investments in GMP plants expand need for QC assays and analytics; public–private partnerships (e.g., co-funded centers) accelerate adoption and de‑risk capital deployment.

Bio-Techne can co-invest or offer financing to secure anchor customers and long-term supply contracts, strengthening revenue visibility.

- subsidies & tax credits: >$10B global since 2020

- GMP clusters: higher QC assay demand

- PPP: faster tech adoption

- co-investment: secures anchor customers

Public health emergencies and preparedness agendas

Public health emergency pathways and stockpiling agendas drive sharp, short-term spikes in demand for diagnostic reagents, as seen when BARDA-supported procurement scaled during COVID-19 response.

Post-crisis normalization frequently produces inventory overhang and pricing pressure; readiness programs demand validated, scalable platforms and manufacturing capacity.

Scenario planning must balance surge capability with stable baseline demand to protect margins and cash flow.

- Tag: surge demand

- Tag: inventory risk

- Tag: scalable platforms

- Tag: balanced scenarios

R&D funding, diagnostics policy and trade measures reshape life‑science markets

Government R&D funding (NIH $49.9B FY2024; Horizon Europe €95.5B 2021–27) and health policy toward diagnostics/precision medicine drive Bio‑Techne demand and product alignment. Regulatory divergence (FDA, EU IVDR, NMPA) and IVD market size ~$90–95B (2024) raise compliance costs and time‑to‑market. Trade measures (Section 301 on ~$370B; tariffs 7.5–25%) and >$10B biomanufacturing subsidies since 2020 shape supply/security and localization strategies.

| Factor | Key Data (2024/25) |

|---|---|

| Funding | NIH $49.9B; Horizon €95.5B |

| Regulation | IVD market $90–95B; IVDR effective 2022 |

| Trade/Supply | $370B goods; tariffs 7.5–25% |

| Industrial policy | >$10B biomanufacturing support since 2020 |

What is included in the product

Explores how macro-environmental factors uniquely affect Bio-Techne across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to reflect real market and regulatory dynamics; designed to support executives, consultants, and investors with forward-looking insights for scenario planning and strategy.

A concise, visually segmented PESTLE summary for Bio-Techne that’s easily shared and dropped into presentations, enabling quick alignment across teams and focused discussion on external risks and market positioning.

Economic factors

R&D spending cycles and capital availability

Academic grants (NIH ~$48B FY2024), biotech VC flows (~$28B worldwide in 2024) and pharma R&D (~$220B global in 2024) directly drive instrument and consumable sales, with funding downturns cutting new instrument placements while sustaining consumable demand in core labs. Higher interest rates (Fed funds ~5.25–5.50% in 2024) raise capex costs and favor leasing; flexible pricing and service contracts smooth revenue volatility.

Healthcare reimbursement and diagnostics economics

Coverage decisions and CPT coding drive adoption of clinical assays and IVD instruments, with the global IVD market valued at about $95B in 2024 and US payers relying on CPT-linked reimbursement to set utilization. Value-based care, tying roughly 30% of US payments to outcomes by 2023, favors tests that demonstrably change outcomes or cut total cost of care. Pricing power hinges on robust clinical-utility evidence and HTA assessments, so market-access teams must generate economic models and real-world cost-effectiveness data early in development.

Input costs, FX, and inflation

Protein reagents, specialty chemicals and precision components face persistent inflation and volatility—US CPI slowed to about 3.4% in 2024, keeping input cost pressure on bioprocess supplies. With roughly half of Bio-Techne revenue generated outside the US, margins remain exposed to currency swings. Active hedging and localized pricing helped protect FY2024 margins, while lean inventory and supplier SLAs cut cost-shock exposure.

Customer consolidation and procurement dynamics

Pharma M&A and CRO/CDMO consolidation concentrate buying power, intensifying price negotiations and favoring suppliers that win network standardization; the global CRO/CDMO market was about $70B in 2023, raising stakes for scale wins. Tiered offerings and enterprise agreements lock share while strong technical support sustains premium pricing and defends margins.

- Pharma mergers amplify buyer leverage

- Network standardization locks winners

- Tiered/enterprise deals secure share

- Technical support protects premium

Emerging market growth

Rapid life‑sciences investment in China (~1.4B people) and India (~1.4B) expands Bio‑Techne’s addressable market as R&D intensity rises (China R&D ≈2.5% of GDP 2023; India ≈0.8% 2023); Gulf states increased health‑tech allocations, boosting regional demand. Local tendering and price sensitivity force tailored portfolios and distributor partnerships; variable IP and compliance regimes raise project risk‑reward tradeoffs.

- China: large R&D spend, high volume but price‑sensitive

- India: fast market growth, cost‑driven tenders

- Middle East: increasing capex, regional hubs

- Risk: uneven IP/procurement rules

R&D funding, diagnostics policy and trade measures reshape life‑science markets

Funding flows (NIH $48B FY2024, biotech VC ~$28B 2024, pharma R&D ~$220B 2024) drive instrument and consumable demand while interest rates (Fed 5.25–5.50% 2024) raise capex costs and favor leasing. Reimbursement and HTA (IVD market ~$95B 2024) determine clinical adoption and pricing power. Supply inflation, FX exposure and CRO/CDMO consolidation (~$70B 2023) pressure margins and favor scale.

| Metric | Value |

|---|---|

| NIH FY2024 | $48B |

| Biotech VC 2024 | $28B |

| Pharma R&D 2024 | $220B |

| IVD 2024 | $95B |

| CRO/CDMO 2023 | $70B |

| Fed funds 2024 | 5.25–5.50% |

Same Document Delivered

Bio-Techne PESTLE Analysis

The preview shown here is the exact Bio-Techne PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product, delivered exactly as shown with no placeholders or surprises. After checkout you’ll be able to download this same finished file immediately.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Bio‑Techne—three to five expert lenses on political, economic, social, technological, legal, and environmental forces shaping its future. Use these insights to anticipate risks and spot growth opportunities for investment or strategy. Purchase the full, editable report now for the complete, actionable deep dive.

Political factors

Public R&D funding and health policy

Government priorities for biomedical research directly shape demand for reagents and instruments, driven by major funding pools such as NIH (roughly $49.9B in FY2024) and EU Horizon Europe (€95.5B 2021–27). Shifts toward pandemic preparedness, oncology or rare-disease grants reallocate procurement and can change Bio-Techne product mix. Health policy favoring diagnostics and precision medicine increases clinical instrument uptake, so Bio-Techne must align portfolio and grant support to these policy themes.

Regulatory harmonization and international standards

Divergent rules across the US, EU and China — e.g., FDA 180-day PMA target, EU IVDR effective May 26, 2022, and NMPA local testing/registration requirements — affect product registration, labeling and QC standards. Fragmentation raises compliance costs and time-to-market; harmonization can shorten approvals versus fragmented pathways in large IVD market ~$90–95B in 2024. Active participation in ISO/IEC and regulatory bodies helps shape assay validation norms; strategic localization meets country-specific mandates and reduces launch delays.

Geopolitical trade and supply chain resilience

Tariffs and Section 301 measures on roughly $370B of goods (rates 7.5–25%) and tightening US export controls since 2022 can raise costs for enzymes, antibodies and electronics and limit access to advanced chips. Geopolitical tensions risk supply of rare reagents and semiconductor components; dual‑use controls (expanded 2022–24) constrain genomic/advanced instruments. Multi‑sourcing and regional manufacturing reduce exposure.

Government incentives for biomanufacturing

Industrial policies promoting domestic bioproduction and advanced therapeutics manufacturing unlock subsidies and tax credits, with governments committing over $10 billion globally to biomanufacturing scale-up since 2020, raising procurement-backed demand for suppliers like Bio-Techne.

Cluster investments in GMP plants expand need for QC assays and analytics; public–private partnerships (e.g., co-funded centers) accelerate adoption and de‑risk capital deployment.

Bio-Techne can co-invest or offer financing to secure anchor customers and long-term supply contracts, strengthening revenue visibility.

- subsidies & tax credits: >$10B global since 2020

- GMP clusters: higher QC assay demand

- PPP: faster tech adoption

- co-investment: secures anchor customers

Public health emergencies and preparedness agendas

Public health emergency pathways and stockpiling agendas drive sharp, short-term spikes in demand for diagnostic reagents, as seen when BARDA-supported procurement scaled during COVID-19 response.

Post-crisis normalization frequently produces inventory overhang and pricing pressure; readiness programs demand validated, scalable platforms and manufacturing capacity.

Scenario planning must balance surge capability with stable baseline demand to protect margins and cash flow.

- Tag: surge demand

- Tag: inventory risk

- Tag: scalable platforms

- Tag: balanced scenarios

R&D funding, diagnostics policy and trade measures reshape life‑science markets

Government R&D funding (NIH $49.9B FY2024; Horizon Europe €95.5B 2021–27) and health policy toward diagnostics/precision medicine drive Bio‑Techne demand and product alignment. Regulatory divergence (FDA, EU IVDR, NMPA) and IVD market size ~$90–95B (2024) raise compliance costs and time‑to‑market. Trade measures (Section 301 on ~$370B; tariffs 7.5–25%) and >$10B biomanufacturing subsidies since 2020 shape supply/security and localization strategies.

| Factor | Key Data (2024/25) |

|---|---|

| Funding | NIH $49.9B; Horizon €95.5B |

| Regulation | IVD market $90–95B; IVDR effective 2022 |

| Trade/Supply | $370B goods; tariffs 7.5–25% |

| Industrial policy | >$10B biomanufacturing support since 2020 |

What is included in the product

Explores how macro-environmental factors uniquely affect Bio-Techne across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to reflect real market and regulatory dynamics; designed to support executives, consultants, and investors with forward-looking insights for scenario planning and strategy.

A concise, visually segmented PESTLE summary for Bio-Techne that’s easily shared and dropped into presentations, enabling quick alignment across teams and focused discussion on external risks and market positioning.

Economic factors

R&D spending cycles and capital availability

Academic grants (NIH ~$48B FY2024), biotech VC flows (~$28B worldwide in 2024) and pharma R&D (~$220B global in 2024) directly drive instrument and consumable sales, with funding downturns cutting new instrument placements while sustaining consumable demand in core labs. Higher interest rates (Fed funds ~5.25–5.50% in 2024) raise capex costs and favor leasing; flexible pricing and service contracts smooth revenue volatility.

Healthcare reimbursement and diagnostics economics

Coverage decisions and CPT coding drive adoption of clinical assays and IVD instruments, with the global IVD market valued at about $95B in 2024 and US payers relying on CPT-linked reimbursement to set utilization. Value-based care, tying roughly 30% of US payments to outcomes by 2023, favors tests that demonstrably change outcomes or cut total cost of care. Pricing power hinges on robust clinical-utility evidence and HTA assessments, so market-access teams must generate economic models and real-world cost-effectiveness data early in development.

Input costs, FX, and inflation

Protein reagents, specialty chemicals and precision components face persistent inflation and volatility—US CPI slowed to about 3.4% in 2024, keeping input cost pressure on bioprocess supplies. With roughly half of Bio-Techne revenue generated outside the US, margins remain exposed to currency swings. Active hedging and localized pricing helped protect FY2024 margins, while lean inventory and supplier SLAs cut cost-shock exposure.

Customer consolidation and procurement dynamics

Pharma M&A and CRO/CDMO consolidation concentrate buying power, intensifying price negotiations and favoring suppliers that win network standardization; the global CRO/CDMO market was about $70B in 2023, raising stakes for scale wins. Tiered offerings and enterprise agreements lock share while strong technical support sustains premium pricing and defends margins.

- Pharma mergers amplify buyer leverage

- Network standardization locks winners

- Tiered/enterprise deals secure share

- Technical support protects premium

Emerging market growth

Rapid life‑sciences investment in China (~1.4B people) and India (~1.4B) expands Bio‑Techne’s addressable market as R&D intensity rises (China R&D ≈2.5% of GDP 2023; India ≈0.8% 2023); Gulf states increased health‑tech allocations, boosting regional demand. Local tendering and price sensitivity force tailored portfolios and distributor partnerships; variable IP and compliance regimes raise project risk‑reward tradeoffs.

- China: large R&D spend, high volume but price‑sensitive

- India: fast market growth, cost‑driven tenders

- Middle East: increasing capex, regional hubs

- Risk: uneven IP/procurement rules

R&D funding, diagnostics policy and trade measures reshape life‑science markets

Funding flows (NIH $48B FY2024, biotech VC ~$28B 2024, pharma R&D ~$220B 2024) drive instrument and consumable demand while interest rates (Fed 5.25–5.50% 2024) raise capex costs and favor leasing. Reimbursement and HTA (IVD market ~$95B 2024) determine clinical adoption and pricing power. Supply inflation, FX exposure and CRO/CDMO consolidation (~$70B 2023) pressure margins and favor scale.

| Metric | Value |

|---|---|

| NIH FY2024 | $48B |

| Biotech VC 2024 | $28B |

| Pharma R&D 2024 | $220B |

| IVD 2024 | $95B |

| CRO/CDMO 2023 | $70B |

| Fed funds 2024 | 5.25–5.50% |

Same Document Delivered

Bio-Techne PESTLE Analysis

The preview shown here is the exact Bio-Techne PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product, delivered exactly as shown with no placeholders or surprises. After checkout you’ll be able to download this same finished file immediately.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Bio‑Techne—three to five expert lenses on political, economic, social, technological, legal, and environmental forces shaping its future. Use these insights to anticipate risks and spot growth opportunities for investment or strategy. Purchase the full, editable report now for the complete, actionable deep dive.

Political factors

Public R&D funding and health policy

Government priorities for biomedical research directly shape demand for reagents and instruments, driven by major funding pools such as NIH (roughly $49.9B in FY2024) and EU Horizon Europe (€95.5B 2021–27). Shifts toward pandemic preparedness, oncology or rare-disease grants reallocate procurement and can change Bio-Techne product mix. Health policy favoring diagnostics and precision medicine increases clinical instrument uptake, so Bio-Techne must align portfolio and grant support to these policy themes.

Regulatory harmonization and international standards

Divergent rules across the US, EU and China — e.g., FDA 180-day PMA target, EU IVDR effective May 26, 2022, and NMPA local testing/registration requirements — affect product registration, labeling and QC standards. Fragmentation raises compliance costs and time-to-market; harmonization can shorten approvals versus fragmented pathways in large IVD market ~$90–95B in 2024. Active participation in ISO/IEC and regulatory bodies helps shape assay validation norms; strategic localization meets country-specific mandates and reduces launch delays.

Geopolitical trade and supply chain resilience

Tariffs and Section 301 measures on roughly $370B of goods (rates 7.5–25%) and tightening US export controls since 2022 can raise costs for enzymes, antibodies and electronics and limit access to advanced chips. Geopolitical tensions risk supply of rare reagents and semiconductor components; dual‑use controls (expanded 2022–24) constrain genomic/advanced instruments. Multi‑sourcing and regional manufacturing reduce exposure.

Government incentives for biomanufacturing

Industrial policies promoting domestic bioproduction and advanced therapeutics manufacturing unlock subsidies and tax credits, with governments committing over $10 billion globally to biomanufacturing scale-up since 2020, raising procurement-backed demand for suppliers like Bio-Techne.

Cluster investments in GMP plants expand need for QC assays and analytics; public–private partnerships (e.g., co-funded centers) accelerate adoption and de‑risk capital deployment.

Bio-Techne can co-invest or offer financing to secure anchor customers and long-term supply contracts, strengthening revenue visibility.

- subsidies & tax credits: >$10B global since 2020

- GMP clusters: higher QC assay demand

- PPP: faster tech adoption

- co-investment: secures anchor customers

Public health emergencies and preparedness agendas

Public health emergency pathways and stockpiling agendas drive sharp, short-term spikes in demand for diagnostic reagents, as seen when BARDA-supported procurement scaled during COVID-19 response.

Post-crisis normalization frequently produces inventory overhang and pricing pressure; readiness programs demand validated, scalable platforms and manufacturing capacity.

Scenario planning must balance surge capability with stable baseline demand to protect margins and cash flow.

- Tag: surge demand

- Tag: inventory risk

- Tag: scalable platforms

- Tag: balanced scenarios

R&D funding, diagnostics policy and trade measures reshape life‑science markets

Government R&D funding (NIH $49.9B FY2024; Horizon Europe €95.5B 2021–27) and health policy toward diagnostics/precision medicine drive Bio‑Techne demand and product alignment. Regulatory divergence (FDA, EU IVDR, NMPA) and IVD market size ~$90–95B (2024) raise compliance costs and time‑to‑market. Trade measures (Section 301 on ~$370B; tariffs 7.5–25%) and >$10B biomanufacturing subsidies since 2020 shape supply/security and localization strategies.

| Factor | Key Data (2024/25) |

|---|---|

| Funding | NIH $49.9B; Horizon €95.5B |

| Regulation | IVD market $90–95B; IVDR effective 2022 |

| Trade/Supply | $370B goods; tariffs 7.5–25% |

| Industrial policy | >$10B biomanufacturing support since 2020 |

What is included in the product

Explores how macro-environmental factors uniquely affect Bio-Techne across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to reflect real market and regulatory dynamics; designed to support executives, consultants, and investors with forward-looking insights for scenario planning and strategy.

A concise, visually segmented PESTLE summary for Bio-Techne that’s easily shared and dropped into presentations, enabling quick alignment across teams and focused discussion on external risks and market positioning.

Economic factors

R&D spending cycles and capital availability

Academic grants (NIH ~$48B FY2024), biotech VC flows (~$28B worldwide in 2024) and pharma R&D (~$220B global in 2024) directly drive instrument and consumable sales, with funding downturns cutting new instrument placements while sustaining consumable demand in core labs. Higher interest rates (Fed funds ~5.25–5.50% in 2024) raise capex costs and favor leasing; flexible pricing and service contracts smooth revenue volatility.

Healthcare reimbursement and diagnostics economics

Coverage decisions and CPT coding drive adoption of clinical assays and IVD instruments, with the global IVD market valued at about $95B in 2024 and US payers relying on CPT-linked reimbursement to set utilization. Value-based care, tying roughly 30% of US payments to outcomes by 2023, favors tests that demonstrably change outcomes or cut total cost of care. Pricing power hinges on robust clinical-utility evidence and HTA assessments, so market-access teams must generate economic models and real-world cost-effectiveness data early in development.

Input costs, FX, and inflation

Protein reagents, specialty chemicals and precision components face persistent inflation and volatility—US CPI slowed to about 3.4% in 2024, keeping input cost pressure on bioprocess supplies. With roughly half of Bio-Techne revenue generated outside the US, margins remain exposed to currency swings. Active hedging and localized pricing helped protect FY2024 margins, while lean inventory and supplier SLAs cut cost-shock exposure.

Customer consolidation and procurement dynamics

Pharma M&A and CRO/CDMO consolidation concentrate buying power, intensifying price negotiations and favoring suppliers that win network standardization; the global CRO/CDMO market was about $70B in 2023, raising stakes for scale wins. Tiered offerings and enterprise agreements lock share while strong technical support sustains premium pricing and defends margins.

- Pharma mergers amplify buyer leverage

- Network standardization locks winners

- Tiered/enterprise deals secure share

- Technical support protects premium

Emerging market growth

Rapid life‑sciences investment in China (~1.4B people) and India (~1.4B) expands Bio‑Techne’s addressable market as R&D intensity rises (China R&D ≈2.5% of GDP 2023; India ≈0.8% 2023); Gulf states increased health‑tech allocations, boosting regional demand. Local tendering and price sensitivity force tailored portfolios and distributor partnerships; variable IP and compliance regimes raise project risk‑reward tradeoffs.

- China: large R&D spend, high volume but price‑sensitive

- India: fast market growth, cost‑driven tenders

- Middle East: increasing capex, regional hubs

- Risk: uneven IP/procurement rules

R&D funding, diagnostics policy and trade measures reshape life‑science markets

Funding flows (NIH $48B FY2024, biotech VC ~$28B 2024, pharma R&D ~$220B 2024) drive instrument and consumable demand while interest rates (Fed 5.25–5.50% 2024) raise capex costs and favor leasing. Reimbursement and HTA (IVD market ~$95B 2024) determine clinical adoption and pricing power. Supply inflation, FX exposure and CRO/CDMO consolidation (~$70B 2023) pressure margins and favor scale.

| Metric | Value |

|---|---|

| NIH FY2024 | $48B |

| Biotech VC 2024 | $28B |

| Pharma R&D 2024 | $220B |

| IVD 2024 | $95B |

| CRO/CDMO 2023 | $70B |

| Fed funds 2024 | 5.25–5.50% |

Same Document Delivered

Bio-Techne PESTLE Analysis

The preview shown here is the exact Bio-Techne PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product, delivered exactly as shown with no placeholders or surprises. After checkout you’ll be able to download this same finished file immediately.