Hubei Biocause Pharmaceutical Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

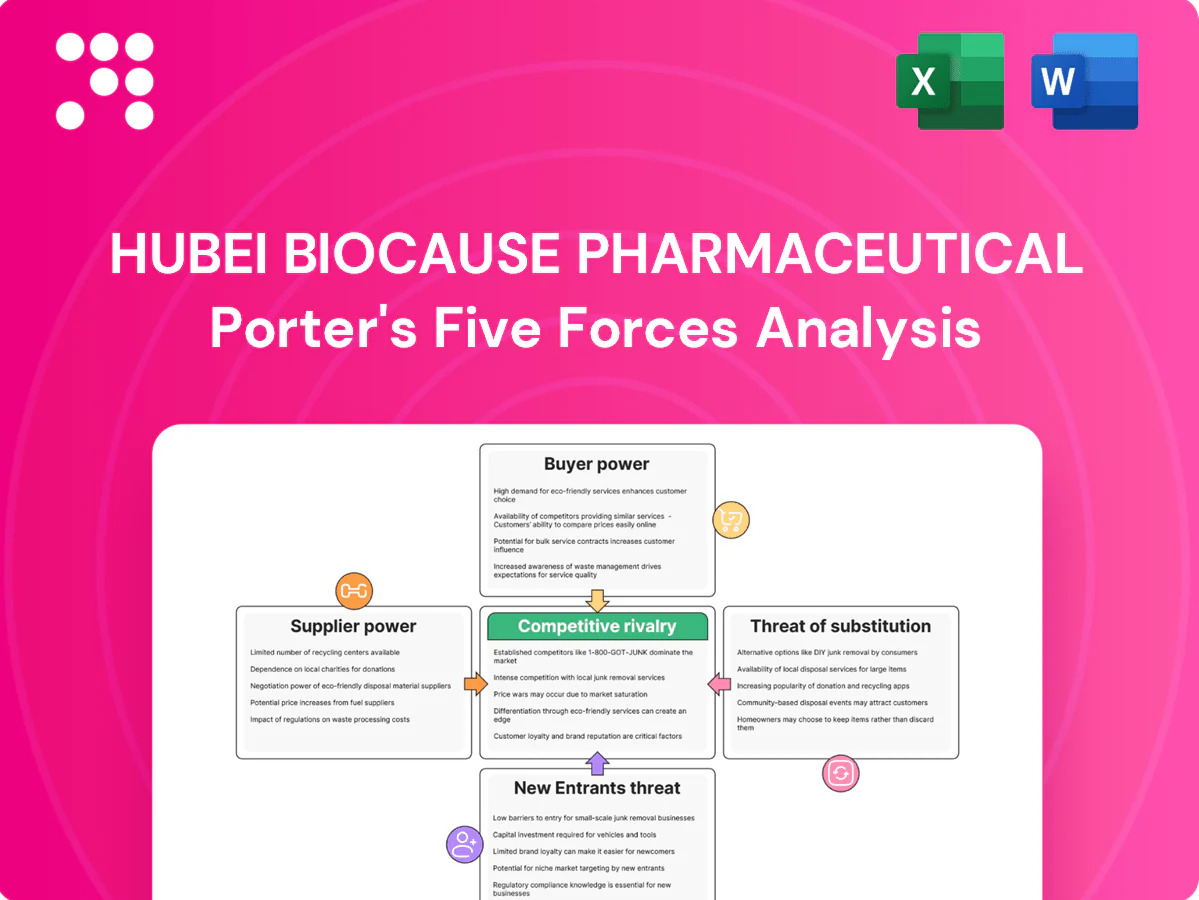

Hubei Biocause faces moderate supplier power, strong buyer scrutiny on drug quality and pricing, and intense rivalry in generics and biosimilars. Regulatory hurdles and capital intensity raise barriers to entry, yet substitutes and international players increase competitive pressure. Patent expiries and distribution partnerships will shape near-term margins and strategic moves. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hubei Biocause Pharmaceutical’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated key intermediates

Several critical API intermediates and specialty excipients are sourced from a limited set of qualified chemical suppliers, concentrating leverage over pricing and contract terms. NMPA/GMP revalidation plus technical transfers and stability work commonly extend supplier changes by 6–18 months, raising switching costs and regulatory risk. This concentration materially lengthens time-to-qualify and operational flexibility.

Regulatory-driven switching costs

Requalifying suppliers demands audits, process validations and dossier updates that typically add regulatory lead time of months, and post-approval changes for marketed preparations generally trigger supplemental filings with review windows often spanning 3–12 months. These regulatory hurdles materially raise switching costs, weakening buyer leverage versus compliant suppliers. Suppliers with cGMP certification and an established track record can therefore extract firmer pricing and contract terms.

Volatile input costs

Solvents, reagents and energy‑intensive intermediates face price swings—often exceeding 20–30% during China’s recent environmental and power-policy cycles—forcing suppliers to pass costs through rapidly and compressing API margins at Biocause.

Hedging instruments are limited for many chemical inputs; Biocause must secure long‑term supply contracts and multi‑sourcing to buffer volatility and preserve gross margin stability.

Acute cost spikes have in past cycles disrupted small‑to‑mid cap Chinese API makers’ competitiveness, risking order losses and margin erosion for Biocause without active procurement strategies.

Equipment and device components

Specialized processing equipment, single‑use filters and device components are concentrated among a few global suppliers (Sartorius, Cytiva, Merck Millipore, Pall), creating supplier power; reported lead times of 6–12 months in 2023–24 and reliance on vendor after‑sales service increase dependency. Custom specifications limit interchangeability, delaying scale‑up and raising capex and opex.

- Few global vendors → supply concentration

- Lead times 6–12 months (2023–24)

- After‑sales dependency raises operational risk

- Custom specs hinder interchangeability, increase capex/opex

Potential to backward integrate

Biocause can insource certain chemical steps or develop alternate synthetic routes, tempering supplier power by reducing dependence on third‑party intermediates. Speed is constrained: capex and environmental permits typically take 12–36 months, with 2024 project capex commonly in the US$15–50m range and significant specialized know‑how required. Back‑integration remains selective and project‑specific, serving mainly as a negotiation lever rather than a blanket strategy.

- Selective back‑integration for high‑value steps

- 2024 capex per project: US$15–50m; timelines 12–36 months

- Limits: permits, environmental compliance, technical know‑how

- Primary role: bargaining leverage vs. suppliers

Supplier power: 6–12 month lead times and 20–30% input swings compress margins

Supplier power is high: qualified API/excipient vendors concentrate supply with 6–12 month lead times (2023–24) and pass through input price swings of ~20–30%, compressing Biocause margins. Regulatory requalification (3–12 months) and specialized equipment dependency increase switching costs. Selective back‑integration (2024 capex US$15–50m; 12–36 months) is used mainly as leverage, not full replacement.

| Metric | 2023–24/2024 |

|---|---|

| Lead times | 6–12 months |

| Input price volatility | 20–30% |

| Requalification lag | 3–12 months |

| Back‑integration capex | US$15–50m |

What is included in the product

Tailored Porter’s Five Forces for Hubei Biocause Pharmaceutical, uncovering competitive intensity, supplier and buyer power, and barriers to entry that shape margins. Identifies substitutes, disruptive threats, and strategic levers to defend market share and pricing.

One-sheet Porter’s Five Forces for Hubei Biocause—clear, slide-ready view that instantly highlights competitive pressures and strategic pain points with a customizable radar chart for rapid boardroom decisions.

Customers Bargaining Power

Centralized procurement pressure

China’s volume-based procurement (VBP) has compressed generics prices—the 2019 national pilot recorded average price cuts of about 52%—giving hospitals and payers strong leverage over suppliers. Winning bids typically secure the bulk of hospital volume, often exceeding 50% market share, but at steep discounts that compress margins for preparations. API buyers benchmark globally as China supplies roughly 60% of the world’s APIs, amplifying buyer power across the value chain.

Large institutional buyers

Hospitals, GPOs and distributors place bulk orders for Hubei Biocause products and demand strict quality and supply assurances, leveraging scale to extract rebates, penalties and tight contract terms. China's centralized procurement experience — the 4+7 pilot cut average drug prices by about 52% — shows buyers' pricing power. Feasible switching among generic suppliers when registrations and quality align keeps margins under pressure.

High price sensitivity in generics

In cardiovascular and endocrine lines many molecules are commoditized, so Chinese hospitals and tenders prioritize unit cost; centralized procurement by 2024 had delivered price cuts exceeding 50% on awarded generics, strengthening buyer leverage. Unless Hubei Biocause differentiates via formulation, delivery or service, buyers will drive negotiations toward lowest-cost suppliers, eroding margins.

Export and DMF customers

Export and DMF customers routinely compare Chinese and Indian API offers, insist on DMFs, CoAs and on-site or remote audits, and in 2024 increased regulatory scrutiny raised DMF demand across markets.

Dual-sourcing is common, boosting buyer leverage; long qualification cycles (months) modestly reduce switching but framework agreements typically load terms onto suppliers while payment and credit expectations add finance pressure.

- DMF/CoA/audits: mandatory

- Dual-sourcing: increases buyer leverage

- Qualification: multi-month friction

- Contracts: buyer-favouring terms

- Payments: credit pressure on suppliers

Quality and supply reliability demands

Buyers demand OTIF performance typically of 98–99% and pharmacovigilance reporting within 24 hours, with any deviation risking delisting from tenders or loss of preferred status; this asymmetry lets purchasers enforce strict service levels and penalties. Vendors often must reinvest 3–5% of revenue into quality, supply-chain and PV systems to retain accounts.

- OTIF target: 98–99%

- PV reporting: ≤24 hours

- Compliance spend: 3–5% of revenue

VBP and tenders cut prices >50%, China supplies ~60% of APIs, OTIF targets 98-99%

Centralized VBP and hospital tenders give buyers strong leverage—2019 pilot cut prices ~52% and by 2024 awarded generics still show >50% cuts, squeezing margins. China supplies ~60% of global APIs, enabling global benchmarking. OTIF targets 98–99% and vendors spend 3–5% revenue on compliance, with dual-sourcing common.

| Metric | Value |

|---|---|

| VBP price cut (2019) | ~52% |

| Generic cuts (2024) | >50% |

| China API share | ~60% |

| OTIF | 98–99% |

| Compliance spend | 3–5% rev |

Preview the Actual Deliverable

Hubei Biocause Pharmaceutical Porter's Five Forces Analysis

This preview shows the exact Hubei Biocause Pharmaceutical Porter’s Five Forces analysis you'll receive after purchase—comprehensive, professionally formatted, and ready to use. It covers rivalry, supplier and buyer power, barriers to entry, and substitution risks. No placeholders or samples; the file available immediately upon payment is this same document.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hubei Biocause faces moderate supplier power, strong buyer scrutiny on drug quality and pricing, and intense rivalry in generics and biosimilars. Regulatory hurdles and capital intensity raise barriers to entry, yet substitutes and international players increase competitive pressure. Patent expiries and distribution partnerships will shape near-term margins and strategic moves. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hubei Biocause Pharmaceutical’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated key intermediates

Several critical API intermediates and specialty excipients are sourced from a limited set of qualified chemical suppliers, concentrating leverage over pricing and contract terms. NMPA/GMP revalidation plus technical transfers and stability work commonly extend supplier changes by 6–18 months, raising switching costs and regulatory risk. This concentration materially lengthens time-to-qualify and operational flexibility.

Regulatory-driven switching costs

Requalifying suppliers demands audits, process validations and dossier updates that typically add regulatory lead time of months, and post-approval changes for marketed preparations generally trigger supplemental filings with review windows often spanning 3–12 months. These regulatory hurdles materially raise switching costs, weakening buyer leverage versus compliant suppliers. Suppliers with cGMP certification and an established track record can therefore extract firmer pricing and contract terms.

Volatile input costs

Solvents, reagents and energy‑intensive intermediates face price swings—often exceeding 20–30% during China’s recent environmental and power-policy cycles—forcing suppliers to pass costs through rapidly and compressing API margins at Biocause.

Hedging instruments are limited for many chemical inputs; Biocause must secure long‑term supply contracts and multi‑sourcing to buffer volatility and preserve gross margin stability.

Acute cost spikes have in past cycles disrupted small‑to‑mid cap Chinese API makers’ competitiveness, risking order losses and margin erosion for Biocause without active procurement strategies.

Equipment and device components

Specialized processing equipment, single‑use filters and device components are concentrated among a few global suppliers (Sartorius, Cytiva, Merck Millipore, Pall), creating supplier power; reported lead times of 6–12 months in 2023–24 and reliance on vendor after‑sales service increase dependency. Custom specifications limit interchangeability, delaying scale‑up and raising capex and opex.

- Few global vendors → supply concentration

- Lead times 6–12 months (2023–24)

- After‑sales dependency raises operational risk

- Custom specs hinder interchangeability, increase capex/opex

Potential to backward integrate

Biocause can insource certain chemical steps or develop alternate synthetic routes, tempering supplier power by reducing dependence on third‑party intermediates. Speed is constrained: capex and environmental permits typically take 12–36 months, with 2024 project capex commonly in the US$15–50m range and significant specialized know‑how required. Back‑integration remains selective and project‑specific, serving mainly as a negotiation lever rather than a blanket strategy.

- Selective back‑integration for high‑value steps

- 2024 capex per project: US$15–50m; timelines 12–36 months

- Limits: permits, environmental compliance, technical know‑how

- Primary role: bargaining leverage vs. suppliers

Supplier power: 6–12 month lead times and 20–30% input swings compress margins

Supplier power is high: qualified API/excipient vendors concentrate supply with 6–12 month lead times (2023–24) and pass through input price swings of ~20–30%, compressing Biocause margins. Regulatory requalification (3–12 months) and specialized equipment dependency increase switching costs. Selective back‑integration (2024 capex US$15–50m; 12–36 months) is used mainly as leverage, not full replacement.

| Metric | 2023–24/2024 |

|---|---|

| Lead times | 6–12 months |

| Input price volatility | 20–30% |

| Requalification lag | 3–12 months |

| Back‑integration capex | US$15–50m |

What is included in the product

Tailored Porter’s Five Forces for Hubei Biocause Pharmaceutical, uncovering competitive intensity, supplier and buyer power, and barriers to entry that shape margins. Identifies substitutes, disruptive threats, and strategic levers to defend market share and pricing.

One-sheet Porter’s Five Forces for Hubei Biocause—clear, slide-ready view that instantly highlights competitive pressures and strategic pain points with a customizable radar chart for rapid boardroom decisions.

Customers Bargaining Power

Centralized procurement pressure

China’s volume-based procurement (VBP) has compressed generics prices—the 2019 national pilot recorded average price cuts of about 52%—giving hospitals and payers strong leverage over suppliers. Winning bids typically secure the bulk of hospital volume, often exceeding 50% market share, but at steep discounts that compress margins for preparations. API buyers benchmark globally as China supplies roughly 60% of the world’s APIs, amplifying buyer power across the value chain.

Large institutional buyers

Hospitals, GPOs and distributors place bulk orders for Hubei Biocause products and demand strict quality and supply assurances, leveraging scale to extract rebates, penalties and tight contract terms. China's centralized procurement experience — the 4+7 pilot cut average drug prices by about 52% — shows buyers' pricing power. Feasible switching among generic suppliers when registrations and quality align keeps margins under pressure.

High price sensitivity in generics

In cardiovascular and endocrine lines many molecules are commoditized, so Chinese hospitals and tenders prioritize unit cost; centralized procurement by 2024 had delivered price cuts exceeding 50% on awarded generics, strengthening buyer leverage. Unless Hubei Biocause differentiates via formulation, delivery or service, buyers will drive negotiations toward lowest-cost suppliers, eroding margins.

Export and DMF customers

Export and DMF customers routinely compare Chinese and Indian API offers, insist on DMFs, CoAs and on-site or remote audits, and in 2024 increased regulatory scrutiny raised DMF demand across markets.

Dual-sourcing is common, boosting buyer leverage; long qualification cycles (months) modestly reduce switching but framework agreements typically load terms onto suppliers while payment and credit expectations add finance pressure.

- DMF/CoA/audits: mandatory

- Dual-sourcing: increases buyer leverage

- Qualification: multi-month friction

- Contracts: buyer-favouring terms

- Payments: credit pressure on suppliers

Quality and supply reliability demands

Buyers demand OTIF performance typically of 98–99% and pharmacovigilance reporting within 24 hours, with any deviation risking delisting from tenders or loss of preferred status; this asymmetry lets purchasers enforce strict service levels and penalties. Vendors often must reinvest 3–5% of revenue into quality, supply-chain and PV systems to retain accounts.

- OTIF target: 98–99%

- PV reporting: ≤24 hours

- Compliance spend: 3–5% of revenue

VBP and tenders cut prices >50%, China supplies ~60% of APIs, OTIF targets 98-99%

Centralized VBP and hospital tenders give buyers strong leverage—2019 pilot cut prices ~52% and by 2024 awarded generics still show >50% cuts, squeezing margins. China supplies ~60% of global APIs, enabling global benchmarking. OTIF targets 98–99% and vendors spend 3–5% revenue on compliance, with dual-sourcing common.

| Metric | Value |

|---|---|

| VBP price cut (2019) | ~52% |

| Generic cuts (2024) | >50% |

| China API share | ~60% |

| OTIF | 98–99% |

| Compliance spend | 3–5% rev |

Preview the Actual Deliverable

Hubei Biocause Pharmaceutical Porter's Five Forces Analysis

This preview shows the exact Hubei Biocause Pharmaceutical Porter’s Five Forces analysis you'll receive after purchase—comprehensive, professionally formatted, and ready to use. It covers rivalry, supplier and buyer power, barriers to entry, and substitution risks. No placeholders or samples; the file available immediately upon payment is this same document.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hubei Biocause faces moderate supplier power, strong buyer scrutiny on drug quality and pricing, and intense rivalry in generics and biosimilars. Regulatory hurdles and capital intensity raise barriers to entry, yet substitutes and international players increase competitive pressure. Patent expiries and distribution partnerships will shape near-term margins and strategic moves. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hubei Biocause Pharmaceutical’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated key intermediates

Several critical API intermediates and specialty excipients are sourced from a limited set of qualified chemical suppliers, concentrating leverage over pricing and contract terms. NMPA/GMP revalidation plus technical transfers and stability work commonly extend supplier changes by 6–18 months, raising switching costs and regulatory risk. This concentration materially lengthens time-to-qualify and operational flexibility.

Regulatory-driven switching costs

Requalifying suppliers demands audits, process validations and dossier updates that typically add regulatory lead time of months, and post-approval changes for marketed preparations generally trigger supplemental filings with review windows often spanning 3–12 months. These regulatory hurdles materially raise switching costs, weakening buyer leverage versus compliant suppliers. Suppliers with cGMP certification and an established track record can therefore extract firmer pricing and contract terms.

Volatile input costs

Solvents, reagents and energy‑intensive intermediates face price swings—often exceeding 20–30% during China’s recent environmental and power-policy cycles—forcing suppliers to pass costs through rapidly and compressing API margins at Biocause.

Hedging instruments are limited for many chemical inputs; Biocause must secure long‑term supply contracts and multi‑sourcing to buffer volatility and preserve gross margin stability.

Acute cost spikes have in past cycles disrupted small‑to‑mid cap Chinese API makers’ competitiveness, risking order losses and margin erosion for Biocause without active procurement strategies.

Equipment and device components

Specialized processing equipment, single‑use filters and device components are concentrated among a few global suppliers (Sartorius, Cytiva, Merck Millipore, Pall), creating supplier power; reported lead times of 6–12 months in 2023–24 and reliance on vendor after‑sales service increase dependency. Custom specifications limit interchangeability, delaying scale‑up and raising capex and opex.

- Few global vendors → supply concentration

- Lead times 6–12 months (2023–24)

- After‑sales dependency raises operational risk

- Custom specs hinder interchangeability, increase capex/opex

Potential to backward integrate

Biocause can insource certain chemical steps or develop alternate synthetic routes, tempering supplier power by reducing dependence on third‑party intermediates. Speed is constrained: capex and environmental permits typically take 12–36 months, with 2024 project capex commonly in the US$15–50m range and significant specialized know‑how required. Back‑integration remains selective and project‑specific, serving mainly as a negotiation lever rather than a blanket strategy.

- Selective back‑integration for high‑value steps

- 2024 capex per project: US$15–50m; timelines 12–36 months

- Limits: permits, environmental compliance, technical know‑how

- Primary role: bargaining leverage vs. suppliers

Supplier power: 6–12 month lead times and 20–30% input swings compress margins

Supplier power is high: qualified API/excipient vendors concentrate supply with 6–12 month lead times (2023–24) and pass through input price swings of ~20–30%, compressing Biocause margins. Regulatory requalification (3–12 months) and specialized equipment dependency increase switching costs. Selective back‑integration (2024 capex US$15–50m; 12–36 months) is used mainly as leverage, not full replacement.

| Metric | 2023–24/2024 |

|---|---|

| Lead times | 6–12 months |

| Input price volatility | 20–30% |

| Requalification lag | 3–12 months |

| Back‑integration capex | US$15–50m |

What is included in the product

Tailored Porter’s Five Forces for Hubei Biocause Pharmaceutical, uncovering competitive intensity, supplier and buyer power, and barriers to entry that shape margins. Identifies substitutes, disruptive threats, and strategic levers to defend market share and pricing.

One-sheet Porter’s Five Forces for Hubei Biocause—clear, slide-ready view that instantly highlights competitive pressures and strategic pain points with a customizable radar chart for rapid boardroom decisions.

Customers Bargaining Power

Centralized procurement pressure

China’s volume-based procurement (VBP) has compressed generics prices—the 2019 national pilot recorded average price cuts of about 52%—giving hospitals and payers strong leverage over suppliers. Winning bids typically secure the bulk of hospital volume, often exceeding 50% market share, but at steep discounts that compress margins for preparations. API buyers benchmark globally as China supplies roughly 60% of the world’s APIs, amplifying buyer power across the value chain.

Large institutional buyers

Hospitals, GPOs and distributors place bulk orders for Hubei Biocause products and demand strict quality and supply assurances, leveraging scale to extract rebates, penalties and tight contract terms. China's centralized procurement experience — the 4+7 pilot cut average drug prices by about 52% — shows buyers' pricing power. Feasible switching among generic suppliers when registrations and quality align keeps margins under pressure.

High price sensitivity in generics

In cardiovascular and endocrine lines many molecules are commoditized, so Chinese hospitals and tenders prioritize unit cost; centralized procurement by 2024 had delivered price cuts exceeding 50% on awarded generics, strengthening buyer leverage. Unless Hubei Biocause differentiates via formulation, delivery or service, buyers will drive negotiations toward lowest-cost suppliers, eroding margins.

Export and DMF customers

Export and DMF customers routinely compare Chinese and Indian API offers, insist on DMFs, CoAs and on-site or remote audits, and in 2024 increased regulatory scrutiny raised DMF demand across markets.

Dual-sourcing is common, boosting buyer leverage; long qualification cycles (months) modestly reduce switching but framework agreements typically load terms onto suppliers while payment and credit expectations add finance pressure.

- DMF/CoA/audits: mandatory

- Dual-sourcing: increases buyer leverage

- Qualification: multi-month friction

- Contracts: buyer-favouring terms

- Payments: credit pressure on suppliers

Quality and supply reliability demands

Buyers demand OTIF performance typically of 98–99% and pharmacovigilance reporting within 24 hours, with any deviation risking delisting from tenders or loss of preferred status; this asymmetry lets purchasers enforce strict service levels and penalties. Vendors often must reinvest 3–5% of revenue into quality, supply-chain and PV systems to retain accounts.

- OTIF target: 98–99%

- PV reporting: ≤24 hours

- Compliance spend: 3–5% of revenue

VBP and tenders cut prices >50%, China supplies ~60% of APIs, OTIF targets 98-99%

Centralized VBP and hospital tenders give buyers strong leverage—2019 pilot cut prices ~52% and by 2024 awarded generics still show >50% cuts, squeezing margins. China supplies ~60% of global APIs, enabling global benchmarking. OTIF targets 98–99% and vendors spend 3–5% revenue on compliance, with dual-sourcing common.

| Metric | Value |

|---|---|

| VBP price cut (2019) | ~52% |

| Generic cuts (2024) | >50% |

| China API share | ~60% |

| OTIF | 98–99% |

| Compliance spend | 3–5% rev |

Preview the Actual Deliverable

Hubei Biocause Pharmaceutical Porter's Five Forces Analysis

This preview shows the exact Hubei Biocause Pharmaceutical Porter’s Five Forces analysis you'll receive after purchase—comprehensive, professionally formatted, and ready to use. It covers rivalry, supplier and buyer power, barriers to entry, and substitution risks. No placeholders or samples; the file available immediately upon payment is this same document.