Biomea Fusion Porter's Five Forces Analysis

From Overview to Strategy Blueprint

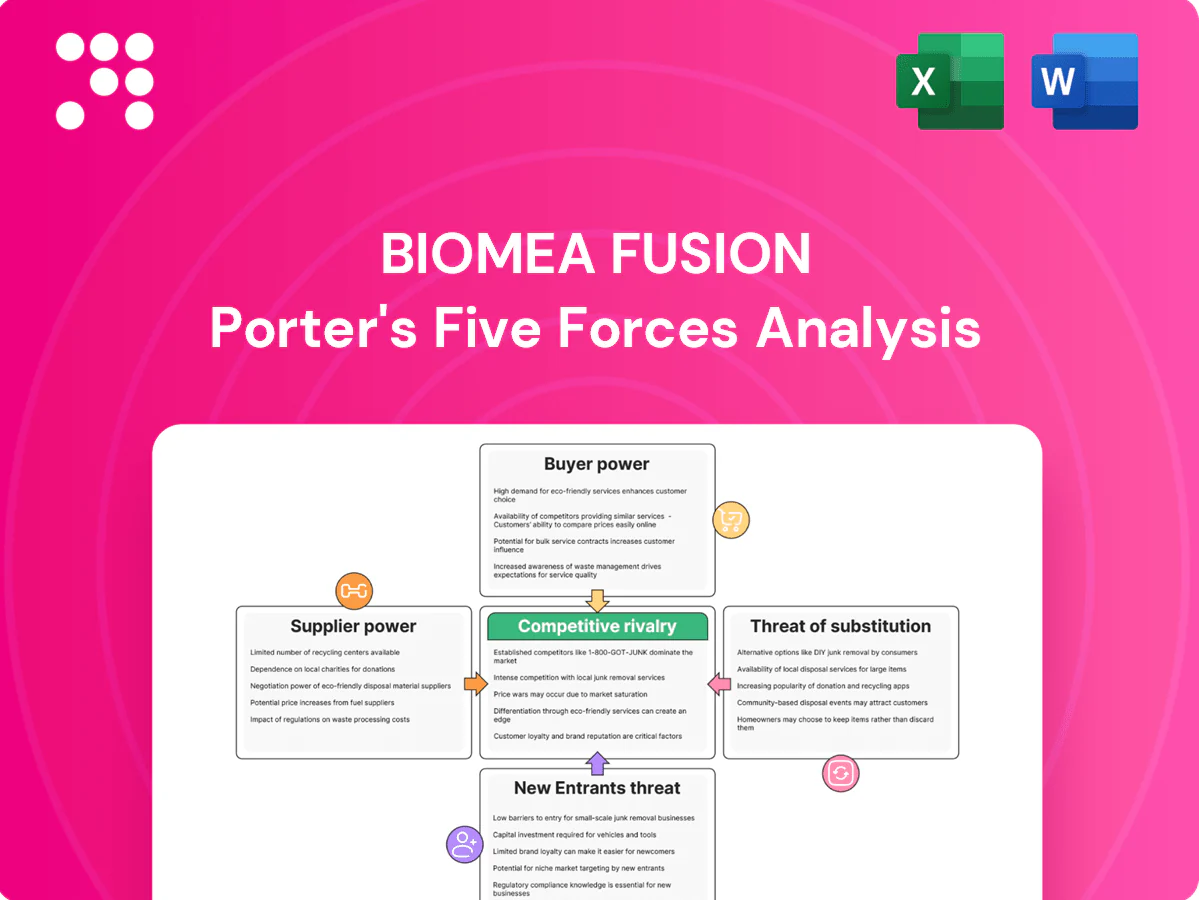

Biomea Fusion faces intense rivalry from established biotech peers, high supplier specialization, and moderate buyer power amid niche oncology pipelines; regulatory hurdles and costly R&D amplify threat levels while novel therapies pose substitute risks. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Specialty reagents and APIs

Biomea Fusion relies on niche chemical intermediates and high-purity APIs sourced from a small pool of specialized vendors, giving suppliers significant leverage. Supply disruptions or quality deviations can halt clinical trials and materially increase development costs. Long lead times and extensive validation requirements further strengthen supplier bargaining power. Dual-sourcing arrangements and inventory buffers partially mitigate but do not eliminate this risk.

CRO/CDMO capacity constraints

Clinical and manufacturing partners with proven small-molecule covalent chemistry expertise are finite, with CDMO lead times commonly stretching 6–12 months in 2024, driving slot premiums of 15–30% during demand spikes. Switching providers incurs costly tech transfer and regulatory re-validation, often adding months and multimillion-dollar expenses. Strategic multi-year agreements in 2024 reduced price and schedule volatility by roughly 10–20%.

Proprietary assays and platforms

Specialized screening, biomarker and companion diagnostic platforms are concentrated: the top three NGS and assay vendors hold over 70% of instrument market share (2023–24), giving suppliers leverage on pricing and data terms. Access fees and restrictive data-rights can add material cost and delay; the global companion diagnostics market was about $8.5B in 2024. Dependence on external platforms shapes trial design and timelines, though building in-house assay capabilities reduces supplier lock-in over time.

Key talent and consultants

Experienced medicinal chemists, CMC, and regulatory specialists are scarce, giving suppliers of talent strong bargaining power that elevates hiring and retention costs for Biomea Fusion.

High compensation and consultant scarcity during critical milestones create schedule risk and cost overruns; equity incentives align interests but increase shareholder dilution.

- Talent scarcity raises recruiting leverage

- Consultant bottlenecks at milestones

- Higher comp packages increase OPEX

- Equity incentives mitigate risk but dilute

Academic IP licensors

Foundational patents and know-how for Biomea Fusion-class programs often stem from universities; typical academic license deals (2024 AUTM trends) feature upfronts from low five-figures to >$1M, milestone tranches and royalties (1–5%) that raise COGS and impose revenue dilution and deal rigidity. Field-of-use and improvement-right clauses can limit downstream indications and partnering optionality. Proactive IP strategy and patent stacking materially improve negotiating posture and licensing leverage.

- Upfronts: range low five-figures–>$1M

- Royalties: ~1–5%

- Milestones: staged payments increase COGS

- Mitigation: patent stacking, defensive filings

Supplier power: CDMO 6-12mo lead times, 15-30% premiums

Suppliers (APIs, CDMOs, assays, talent, university licenses) exert high bargaining power: CDMO lead times 6–12 months (2024) with 15–30% slot premiums; top-three NGS/assay vendors >70% market share (2023–24); companion diagnostics market ~$8.5B (2024); academic license royalties ~1–5% and upfronts low five-figures–>$1M (AUTM 2024).

| Category | 2023–24 Metric |

|---|---|

| CDMO lead time | 6–12 months |

| Slot premium | 15–30% |

| NGS/assay top3 share | >70% |

| Companion Dx market | $8.5B (2024) |

| Academic royalties | 1–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Biomea Fusion uncovering competitive drivers, supplier and buyer power, entry barriers, and substitute threats; highlights disruptive forces and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Biomea Fusion—clarify competitive pressures, regulatory risk, supplier and buyer bargaining, and substitute threats to speed strategic decisions and investor pitches.

Customers Bargaining Power

Payers and HTA bodies

Reimbursement will depend on clear clinical benefit and cost-effectiveness versus SOC, with ICER thresholds commonly $100,000–$150,000/QALY and NICE £20,000–30,000/QALY. Consolidated payers (top US insurers cover ~70–80% of lives) can demand steep discounts or restrict access. RWE and outcomes-based contracts, while <1% of spend today, are rising and can ease uptake. Early HEOR planning is critical to meet HTA evidence requirements.

Oncologists and endocrinologists

Prescribers weigh efficacy, safety and ease-of-use against entrenched therapies in a oncology market ~200B in 2024, with ASCO attendance >30,000 and AACE membership ~7,000 reflecting concentrated influence. KOL endorsements can accelerate uptake but hinge on robust head-to-head data. Complex monitoring requirements lower clinician willingness to switch, while strong label, guideline inclusion and targeted education materially improve pull-through.

Patients and advocacy groups

Patients demand clear efficacy and tolerability, strongly shaping trial enrollment and commercial uptake; poor tolerability drives dropout and limits market adoption. Advocacy groups in 2024 amplified unmet-need narratives and payer pressure, raising access scrutiny. For metabolic disease, convenience and weight effects are decisive treatment attributes. Robust patient-support programs reduce out-of-pocket barriers and improve adherence.

Large pharma partners

Large pharma partners exert strong bargaining power when Biomea seeks out-licensing or co-development, as concentrated counterparties can demand favorable terms. Deal economics in 2024 depended heavily on data maturity and competitive landscape; many biotech deals showed median upfronts ~$25–30M and total potential values often >$1B. Milestone-heavy structures shift development and commercial risk to Biomea. Competitive bidding can materially improve upfronts and royalty rates.

- 2024 median upfront ~25–30M; total deal value often >1B

- Data maturity and competitors drive term leverage

- Milestone-heavy = lower upfront, greater contingent risk to Biomea

- Competitive bids increase economics and negotiating leverage

Clinical trial sites

High-performing clinical trial sites can demand premium budgets and favorable terms, with the top 20% of sites delivering roughly 60% of enrollments; site capacity and competing studies therefore materially affect enrollment speed. Protocol burden (visits, procedures) reduces willingness to participate, while strong sponsor-site relationships and 2024-era decentralized elements (used by ~50% of sponsors) cut friction.

- Top sites: ~20% yield ~60% enrollments

- Activation time: ~3–6 months

- Decentralized adoption: ~50% (2024)

- High protocol burden lowers site acceptance

Payer leverage: ICER $100–150k/QALY, DCT adoption ~50%

Payers and consolidated insurers (top US insurers cover ~70–80% of lives) wield strong leverage, enforcing ICER-like thresholds ($100–150k/QALY) and discounting. Prescribers require clear head-to-head efficacy and manageable monitoring to switch from entrenched oncology SOC. Patients and advocacy groups drive access and adherence; decentralized trials (~50% adoption in 2024) and robust patient support reduce barriers.

| Stakeholder | Key metric (2024) |

|---|---|

| Payers | Cover ~70–80% lives; ICER $100–150k/QALY |

| Deals | Median upfront $25–30M; total >$1B |

| Trials | Decentralized use ~50% |

Same Document Delivered

Biomea Fusion Porter's Five Forces Analysis

This preview shows the exact Biomea Fusion Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is professionally formatted, comprehensive, and ready for download and use the moment you buy. You're looking at the final deliverable: the same file available for instant access after payment.

From Overview to Strategy Blueprint

Biomea Fusion faces intense rivalry from established biotech peers, high supplier specialization, and moderate buyer power amid niche oncology pipelines; regulatory hurdles and costly R&D amplify threat levels while novel therapies pose substitute risks. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Specialty reagents and APIs

Biomea Fusion relies on niche chemical intermediates and high-purity APIs sourced from a small pool of specialized vendors, giving suppliers significant leverage. Supply disruptions or quality deviations can halt clinical trials and materially increase development costs. Long lead times and extensive validation requirements further strengthen supplier bargaining power. Dual-sourcing arrangements and inventory buffers partially mitigate but do not eliminate this risk.

CRO/CDMO capacity constraints

Clinical and manufacturing partners with proven small-molecule covalent chemistry expertise are finite, with CDMO lead times commonly stretching 6–12 months in 2024, driving slot premiums of 15–30% during demand spikes. Switching providers incurs costly tech transfer and regulatory re-validation, often adding months and multimillion-dollar expenses. Strategic multi-year agreements in 2024 reduced price and schedule volatility by roughly 10–20%.

Proprietary assays and platforms

Specialized screening, biomarker and companion diagnostic platforms are concentrated: the top three NGS and assay vendors hold over 70% of instrument market share (2023–24), giving suppliers leverage on pricing and data terms. Access fees and restrictive data-rights can add material cost and delay; the global companion diagnostics market was about $8.5B in 2024. Dependence on external platforms shapes trial design and timelines, though building in-house assay capabilities reduces supplier lock-in over time.

Key talent and consultants

Experienced medicinal chemists, CMC, and regulatory specialists are scarce, giving suppliers of talent strong bargaining power that elevates hiring and retention costs for Biomea Fusion.

High compensation and consultant scarcity during critical milestones create schedule risk and cost overruns; equity incentives align interests but increase shareholder dilution.

- Talent scarcity raises recruiting leverage

- Consultant bottlenecks at milestones

- Higher comp packages increase OPEX

- Equity incentives mitigate risk but dilute

Academic IP licensors

Foundational patents and know-how for Biomea Fusion-class programs often stem from universities; typical academic license deals (2024 AUTM trends) feature upfronts from low five-figures to >$1M, milestone tranches and royalties (1–5%) that raise COGS and impose revenue dilution and deal rigidity. Field-of-use and improvement-right clauses can limit downstream indications and partnering optionality. Proactive IP strategy and patent stacking materially improve negotiating posture and licensing leverage.

- Upfronts: range low five-figures–>$1M

- Royalties: ~1–5%

- Milestones: staged payments increase COGS

- Mitigation: patent stacking, defensive filings

Supplier power: CDMO 6-12mo lead times, 15-30% premiums

Suppliers (APIs, CDMOs, assays, talent, university licenses) exert high bargaining power: CDMO lead times 6–12 months (2024) with 15–30% slot premiums; top-three NGS/assay vendors >70% market share (2023–24); companion diagnostics market ~$8.5B (2024); academic license royalties ~1–5% and upfronts low five-figures–>$1M (AUTM 2024).

| Category | 2023–24 Metric |

|---|---|

| CDMO lead time | 6–12 months |

| Slot premium | 15–30% |

| NGS/assay top3 share | >70% |

| Companion Dx market | $8.5B (2024) |

| Academic royalties | 1–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Biomea Fusion uncovering competitive drivers, supplier and buyer power, entry barriers, and substitute threats; highlights disruptive forces and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Biomea Fusion—clarify competitive pressures, regulatory risk, supplier and buyer bargaining, and substitute threats to speed strategic decisions and investor pitches.

Customers Bargaining Power

Payers and HTA bodies

Reimbursement will depend on clear clinical benefit and cost-effectiveness versus SOC, with ICER thresholds commonly $100,000–$150,000/QALY and NICE £20,000–30,000/QALY. Consolidated payers (top US insurers cover ~70–80% of lives) can demand steep discounts or restrict access. RWE and outcomes-based contracts, while <1% of spend today, are rising and can ease uptake. Early HEOR planning is critical to meet HTA evidence requirements.

Oncologists and endocrinologists

Prescribers weigh efficacy, safety and ease-of-use against entrenched therapies in a oncology market ~200B in 2024, with ASCO attendance >30,000 and AACE membership ~7,000 reflecting concentrated influence. KOL endorsements can accelerate uptake but hinge on robust head-to-head data. Complex monitoring requirements lower clinician willingness to switch, while strong label, guideline inclusion and targeted education materially improve pull-through.

Patients and advocacy groups

Patients demand clear efficacy and tolerability, strongly shaping trial enrollment and commercial uptake; poor tolerability drives dropout and limits market adoption. Advocacy groups in 2024 amplified unmet-need narratives and payer pressure, raising access scrutiny. For metabolic disease, convenience and weight effects are decisive treatment attributes. Robust patient-support programs reduce out-of-pocket barriers and improve adherence.

Large pharma partners

Large pharma partners exert strong bargaining power when Biomea seeks out-licensing or co-development, as concentrated counterparties can demand favorable terms. Deal economics in 2024 depended heavily on data maturity and competitive landscape; many biotech deals showed median upfronts ~$25–30M and total potential values often >$1B. Milestone-heavy structures shift development and commercial risk to Biomea. Competitive bidding can materially improve upfronts and royalty rates.

- 2024 median upfront ~25–30M; total deal value often >1B

- Data maturity and competitors drive term leverage

- Milestone-heavy = lower upfront, greater contingent risk to Biomea

- Competitive bids increase economics and negotiating leverage

Clinical trial sites

High-performing clinical trial sites can demand premium budgets and favorable terms, with the top 20% of sites delivering roughly 60% of enrollments; site capacity and competing studies therefore materially affect enrollment speed. Protocol burden (visits, procedures) reduces willingness to participate, while strong sponsor-site relationships and 2024-era decentralized elements (used by ~50% of sponsors) cut friction.

- Top sites: ~20% yield ~60% enrollments

- Activation time: ~3–6 months

- Decentralized adoption: ~50% (2024)

- High protocol burden lowers site acceptance

Payer leverage: ICER $100–150k/QALY, DCT adoption ~50%

Payers and consolidated insurers (top US insurers cover ~70–80% of lives) wield strong leverage, enforcing ICER-like thresholds ($100–150k/QALY) and discounting. Prescribers require clear head-to-head efficacy and manageable monitoring to switch from entrenched oncology SOC. Patients and advocacy groups drive access and adherence; decentralized trials (~50% adoption in 2024) and robust patient support reduce barriers.

| Stakeholder | Key metric (2024) |

|---|---|

| Payers | Cover ~70–80% lives; ICER $100–150k/QALY |

| Deals | Median upfront $25–30M; total >$1B |

| Trials | Decentralized use ~50% |

Same Document Delivered

Biomea Fusion Porter's Five Forces Analysis

This preview shows the exact Biomea Fusion Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is professionally formatted, comprehensive, and ready for download and use the moment you buy. You're looking at the final deliverable: the same file available for instant access after payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Biomea Fusion faces intense rivalry from established biotech peers, high supplier specialization, and moderate buyer power amid niche oncology pipelines; regulatory hurdles and costly R&D amplify threat levels while novel therapies pose substitute risks. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Specialty reagents and APIs

Biomea Fusion relies on niche chemical intermediates and high-purity APIs sourced from a small pool of specialized vendors, giving suppliers significant leverage. Supply disruptions or quality deviations can halt clinical trials and materially increase development costs. Long lead times and extensive validation requirements further strengthen supplier bargaining power. Dual-sourcing arrangements and inventory buffers partially mitigate but do not eliminate this risk.

CRO/CDMO capacity constraints

Clinical and manufacturing partners with proven small-molecule covalent chemistry expertise are finite, with CDMO lead times commonly stretching 6–12 months in 2024, driving slot premiums of 15–30% during demand spikes. Switching providers incurs costly tech transfer and regulatory re-validation, often adding months and multimillion-dollar expenses. Strategic multi-year agreements in 2024 reduced price and schedule volatility by roughly 10–20%.

Proprietary assays and platforms

Specialized screening, biomarker and companion diagnostic platforms are concentrated: the top three NGS and assay vendors hold over 70% of instrument market share (2023–24), giving suppliers leverage on pricing and data terms. Access fees and restrictive data-rights can add material cost and delay; the global companion diagnostics market was about $8.5B in 2024. Dependence on external platforms shapes trial design and timelines, though building in-house assay capabilities reduces supplier lock-in over time.

Key talent and consultants

Experienced medicinal chemists, CMC, and regulatory specialists are scarce, giving suppliers of talent strong bargaining power that elevates hiring and retention costs for Biomea Fusion.

High compensation and consultant scarcity during critical milestones create schedule risk and cost overruns; equity incentives align interests but increase shareholder dilution.

- Talent scarcity raises recruiting leverage

- Consultant bottlenecks at milestones

- Higher comp packages increase OPEX

- Equity incentives mitigate risk but dilute

Academic IP licensors

Foundational patents and know-how for Biomea Fusion-class programs often stem from universities; typical academic license deals (2024 AUTM trends) feature upfronts from low five-figures to >$1M, milestone tranches and royalties (1–5%) that raise COGS and impose revenue dilution and deal rigidity. Field-of-use and improvement-right clauses can limit downstream indications and partnering optionality. Proactive IP strategy and patent stacking materially improve negotiating posture and licensing leverage.

- Upfronts: range low five-figures–>$1M

- Royalties: ~1–5%

- Milestones: staged payments increase COGS

- Mitigation: patent stacking, defensive filings

Supplier power: CDMO 6-12mo lead times, 15-30% premiums

Suppliers (APIs, CDMOs, assays, talent, university licenses) exert high bargaining power: CDMO lead times 6–12 months (2024) with 15–30% slot premiums; top-three NGS/assay vendors >70% market share (2023–24); companion diagnostics market ~$8.5B (2024); academic license royalties ~1–5% and upfronts low five-figures–>$1M (AUTM 2024).

| Category | 2023–24 Metric |

|---|---|

| CDMO lead time | 6–12 months |

| Slot premium | 15–30% |

| NGS/assay top3 share | >70% |

| Companion Dx market | $8.5B (2024) |

| Academic royalties | 1–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Biomea Fusion uncovering competitive drivers, supplier and buyer power, entry barriers, and substitute threats; highlights disruptive forces and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Biomea Fusion—clarify competitive pressures, regulatory risk, supplier and buyer bargaining, and substitute threats to speed strategic decisions and investor pitches.

Customers Bargaining Power

Payers and HTA bodies

Reimbursement will depend on clear clinical benefit and cost-effectiveness versus SOC, with ICER thresholds commonly $100,000–$150,000/QALY and NICE £20,000–30,000/QALY. Consolidated payers (top US insurers cover ~70–80% of lives) can demand steep discounts or restrict access. RWE and outcomes-based contracts, while <1% of spend today, are rising and can ease uptake. Early HEOR planning is critical to meet HTA evidence requirements.

Oncologists and endocrinologists

Prescribers weigh efficacy, safety and ease-of-use against entrenched therapies in a oncology market ~200B in 2024, with ASCO attendance >30,000 and AACE membership ~7,000 reflecting concentrated influence. KOL endorsements can accelerate uptake but hinge on robust head-to-head data. Complex monitoring requirements lower clinician willingness to switch, while strong label, guideline inclusion and targeted education materially improve pull-through.

Patients and advocacy groups

Patients demand clear efficacy and tolerability, strongly shaping trial enrollment and commercial uptake; poor tolerability drives dropout and limits market adoption. Advocacy groups in 2024 amplified unmet-need narratives and payer pressure, raising access scrutiny. For metabolic disease, convenience and weight effects are decisive treatment attributes. Robust patient-support programs reduce out-of-pocket barriers and improve adherence.

Large pharma partners

Large pharma partners exert strong bargaining power when Biomea seeks out-licensing or co-development, as concentrated counterparties can demand favorable terms. Deal economics in 2024 depended heavily on data maturity and competitive landscape; many biotech deals showed median upfronts ~$25–30M and total potential values often >$1B. Milestone-heavy structures shift development and commercial risk to Biomea. Competitive bidding can materially improve upfronts and royalty rates.

- 2024 median upfront ~25–30M; total deal value often >1B

- Data maturity and competitors drive term leverage

- Milestone-heavy = lower upfront, greater contingent risk to Biomea

- Competitive bids increase economics and negotiating leverage

Clinical trial sites

High-performing clinical trial sites can demand premium budgets and favorable terms, with the top 20% of sites delivering roughly 60% of enrollments; site capacity and competing studies therefore materially affect enrollment speed. Protocol burden (visits, procedures) reduces willingness to participate, while strong sponsor-site relationships and 2024-era decentralized elements (used by ~50% of sponsors) cut friction.

- Top sites: ~20% yield ~60% enrollments

- Activation time: ~3–6 months

- Decentralized adoption: ~50% (2024)

- High protocol burden lowers site acceptance

Payer leverage: ICER $100–150k/QALY, DCT adoption ~50%

Payers and consolidated insurers (top US insurers cover ~70–80% of lives) wield strong leverage, enforcing ICER-like thresholds ($100–150k/QALY) and discounting. Prescribers require clear head-to-head efficacy and manageable monitoring to switch from entrenched oncology SOC. Patients and advocacy groups drive access and adherence; decentralized trials (~50% adoption in 2024) and robust patient support reduce barriers.

| Stakeholder | Key metric (2024) |

|---|---|

| Payers | Cover ~70–80% lives; ICER $100–150k/QALY |

| Deals | Median upfront $25–30M; total >$1B |

| Trials | Decentralized use ~50% |

Same Document Delivered

Biomea Fusion Porter's Five Forces Analysis

This preview shows the exact Biomea Fusion Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is professionally formatted, comprehensive, and ready for download and use the moment you buy. You're looking at the final deliverable: the same file available for instant access after payment.