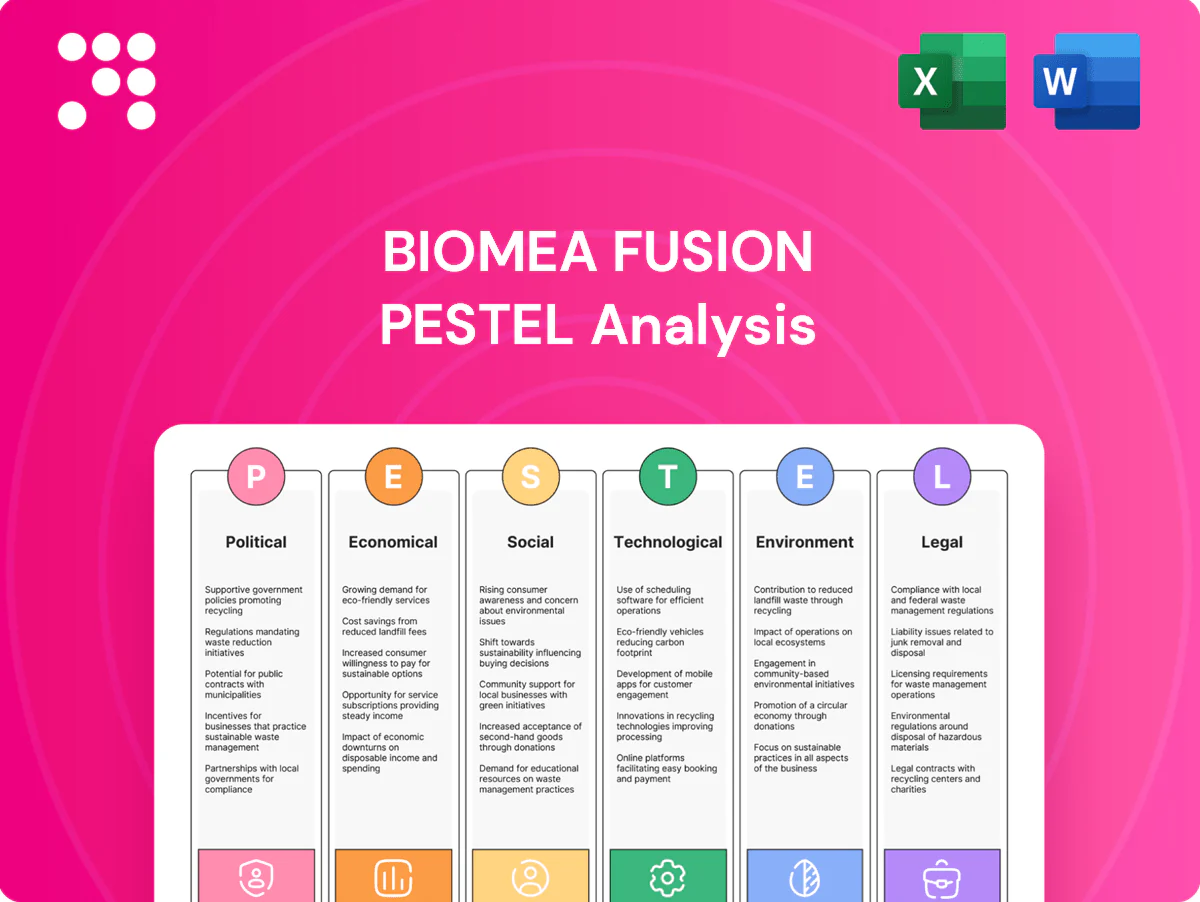

Biomea Fusion PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our focused PESTLE Analysis of Biomea Fusion — revealing how regulatory shifts, biotech funding cycles, and emerging technologies will shape its trajectory. Ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report to download the complete, editable analysis and make data-driven decisions.

Political factors

Regulatory climate and FDA/EMA priorities

Regulators prioritize safety, first-in-class mechanisms, and explicit biomarker strategies, driving trial designs for irreversible covalent inhibitors like BMF-219 and raising the bar on off-target profiling. Oncology and metabolic pathways remain eligible for expedited pathways (Breakthrough, Fast Track), yet evidentiary standards and rigorous safety datasets are enforced. Ongoing, documented engagement with FDA/EMA on covalent binding risks and selectivity is critical. Growing FDA/EMA emphasis on real-world evidence may allow post-approval commitments for BMF-219.

Drug pricing reforms and payer policy influence

US drug negotiation under the IRA begins in 2026, creating downward pressure on net prices while EU reference pricing often cuts list prices by up to ~30%; oncology typically sustains higher willingness-to-pay (NICE thresholds £20–30k/QALY) whereas metabolic indications face stricter cost-effectiveness bars (€20–40k/QALY). Early HEOR is essential to defend value, and government-dominant payers (public funding >80% in many EU diabetes markets) will shape launch sequencing.

Public funding and translational research support

NIH funding (~$52B FY2024) and EU Horizon Europe (€95.5B 2021–27) drive preclinical collaborations and target validation for covalent chemistries, while US Cancer Moonshot (goal: 50% reduction in cancer deaths over 25 years) fuels trial networks; shifting budget cycles and grant priorities constrain access to shared infrastructure/biomarker platforms, making deep academia partnerships a hedge against political funding volatility.

Geopolitical supply chain stability

Export controls and trade tensions constrain sourcing of reagents, APIs and specialized CDMO capacity, raising lead times and costs for Biomea Fusion’s R&D and GMP production. Political instability can delay GMP batch releases and global-trial logistics, disrupting timelines and patient enrollment. Localizing critical steps or dual-sourcing and pursuing harmonized standards ease cross-border sample and data transfers and reduce operational risk.

- Export controls: restrict access to certain reagents and technologies

- Trade tensions: increase lead times and supplier risk

- Localize/dual-source: mitigates single-point failures

- Harmonized standards: facilitate cross-border trials and data flow

Healthcare system capacity and national strategies

National cancer incidence (19.3 million new cases in 2020) and diabetes prevalence (537 million adults in 2021) drive screening and eligible patient pools, shaping Biomea Fusion trial feasibility and market size. Political support for precision medicine and reimbursement is raising genomic testing uptake, expanding genetically defined cancer cohorts. Centralized ethics boards and accredited trial sites can cut start-up timelines by weeks, while regional care disparities demand tailored access programs.

- Policy impact: national cancer/diabetes plans define patient pools

- Precision support: increases genomic testing and eligible cohorts

- Regulatory: accreditation/centralized review speeds trial initiation

- Access: regional disparities require targeted programs

Safety-focused regulators raise trial bar for covalent inhibitors; IRA pricing pressure starts 2026

Regulatory focus on safety/biomarkers raises trial evidentiary bars for covalent inhibitors; expedited pathways remain but require robust safety data. IRA price negotiations begin 2026, pressuring net prices; NICE thresholds ~£20–30k/QALY for oncology. NIH FY2024 ~$52B and Horizon Europe €95.5B sustain translational partnerships; export controls add sourcing risk.

| Metric | Value |

|---|---|

| NIH FY2024 | $52B |

| Horizon Europe | €95.5B (2021–27) |

| Cancer incidence | 19.3M (2020) |

What is included in the product

Provides a data-backed PESTLE review of Biomea Fusion—assessing Political, Economic, Social, Technological, Environmental and Legal factors tied to its industry and regional dynamics to identify risks and opportunities. Designed for executives and investors, it includes detailed subpoints, forward-looking scenario insights and clean formatting ready for reports, decks or funding materials.

Biomea Fusion PESTLE Analysis delivers a clean, visually segmented summary for quick interpretation and meeting-ready insertion into presentations, while allowing users to add contextual notes and share concise insights across teams to streamline external risk assessment and strategic planning.

Economic factors

Capital market conditions and financing runway

Clinical-stage biotechs like Biomea Fusion depend on equity raises and partnering; higher rates and lower risk appetite — with the 10-year U.S. Treasury near 4.1% in July 2025 — increase dilution pressure and slow fundraising cadence. Volatile public markets can defer follow-on raises, constraining BMF-219 trial size and timelines. Milestone-rich collaborations offset cash burn but cede future upside. Prudent cash management preserves pivotal-study optionality.

Cost of clinical development and CDMO inflation

CMC scale-up for irreversible inhibitors requires specialized analytics and process development, often adding 20–40% to early manufacturing budgets. Competition for CDMO slots has pushed lead times to 12–24 months and spot pricing up roughly 10–15% Y/Y in 2023–24. Investing in process robustness early can cut rework and batch-failure rates by over 30%. Geographic arbitrage and multi-year framework agreements commonly cap unit costs by 10–25%.

Market size in oncology and metabolic diseases

Oncology offers premium pricing with the global oncology drug market ~USD 200–230B in 2024 but patient populations are segmented by mutations, limiting addressable share per asset. Metabolic diseases such as diabetes represent larger volumes—global diabetes drug market ~USD 60–80B in 2024—but face tighter payer controls and price pressure. Biomea’s indication mix must weigh peak sales upside in oncology against reimbursement risk in metabolic. Sequencing oncology first can clinically validate MoA and de-risk broader metabolic launches.

Payer mix and affordability dynamics

US payer mix matters: commercial enrollment ~178M, Medicare ~66M and Medicaid ~84M (CMS 2023), driving differential net price realization as commercial plans often secure higher list-to-net spreads while Medicare/Medicaid impose statutory/managed discounts; EU HTA bodies (NICE threshold ~20–30k GBP/QALY) insist on comparative effectiveness and budget impact; co-pay design affects adherence in chronic metabolic care; value-based contracts tie payment to outcomes.

- Payer enrollment: commercial 178M; Medicare 66M; Medicaid 84M (CMS 2023)

- NICE threshold ~20–30k GBP/QALY

- Co-pay levels materially influence adherence in chronic metabolic diseases

- Value-based contracts align economics with outcomes

FX and international launch economics

Safety-focused regulators raise trial bar for covalent inhibitors; IRA pricing pressure starts 2026

Higher rates (US 10y ~4.1% Jul 2025) raise dilution risk and slow equity raises; CDMO lead times 12–24m and +10–15% spot pricing lift early CMC spend; oncology market ~USD 210B (2024) offers high pricing but narrow mutation-defined pools; EUR/USD ~1.08 (2024) and external reference pricing compress net prices across regions.

| Metric | Value |

|---|---|

| US 10y | ~4.1% (Jul 2025) |

| CDMO lead time | 12–24 months |

| Oncology market | ~USD 210B (2024) |

| EUR/USD | ~1.08 (2024) |

Same Document Delivered

Biomea Fusion PESTLE Analysis

The Biomea Fusion PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are the final file with no placeholders or teasers. After payment you’ll instantly download this exact, professionally structured report.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our focused PESTLE Analysis of Biomea Fusion — revealing how regulatory shifts, biotech funding cycles, and emerging technologies will shape its trajectory. Ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report to download the complete, editable analysis and make data-driven decisions.

Political factors

Regulatory climate and FDA/EMA priorities

Regulators prioritize safety, first-in-class mechanisms, and explicit biomarker strategies, driving trial designs for irreversible covalent inhibitors like BMF-219 and raising the bar on off-target profiling. Oncology and metabolic pathways remain eligible for expedited pathways (Breakthrough, Fast Track), yet evidentiary standards and rigorous safety datasets are enforced. Ongoing, documented engagement with FDA/EMA on covalent binding risks and selectivity is critical. Growing FDA/EMA emphasis on real-world evidence may allow post-approval commitments for BMF-219.

Drug pricing reforms and payer policy influence

US drug negotiation under the IRA begins in 2026, creating downward pressure on net prices while EU reference pricing often cuts list prices by up to ~30%; oncology typically sustains higher willingness-to-pay (NICE thresholds £20–30k/QALY) whereas metabolic indications face stricter cost-effectiveness bars (€20–40k/QALY). Early HEOR is essential to defend value, and government-dominant payers (public funding >80% in many EU diabetes markets) will shape launch sequencing.

Public funding and translational research support

NIH funding (~$52B FY2024) and EU Horizon Europe (€95.5B 2021–27) drive preclinical collaborations and target validation for covalent chemistries, while US Cancer Moonshot (goal: 50% reduction in cancer deaths over 25 years) fuels trial networks; shifting budget cycles and grant priorities constrain access to shared infrastructure/biomarker platforms, making deep academia partnerships a hedge against political funding volatility.

Geopolitical supply chain stability

Export controls and trade tensions constrain sourcing of reagents, APIs and specialized CDMO capacity, raising lead times and costs for Biomea Fusion’s R&D and GMP production. Political instability can delay GMP batch releases and global-trial logistics, disrupting timelines and patient enrollment. Localizing critical steps or dual-sourcing and pursuing harmonized standards ease cross-border sample and data transfers and reduce operational risk.

- Export controls: restrict access to certain reagents and technologies

- Trade tensions: increase lead times and supplier risk

- Localize/dual-source: mitigates single-point failures

- Harmonized standards: facilitate cross-border trials and data flow

Healthcare system capacity and national strategies

National cancer incidence (19.3 million new cases in 2020) and diabetes prevalence (537 million adults in 2021) drive screening and eligible patient pools, shaping Biomea Fusion trial feasibility and market size. Political support for precision medicine and reimbursement is raising genomic testing uptake, expanding genetically defined cancer cohorts. Centralized ethics boards and accredited trial sites can cut start-up timelines by weeks, while regional care disparities demand tailored access programs.

- Policy impact: national cancer/diabetes plans define patient pools

- Precision support: increases genomic testing and eligible cohorts

- Regulatory: accreditation/centralized review speeds trial initiation

- Access: regional disparities require targeted programs

Safety-focused regulators raise trial bar for covalent inhibitors; IRA pricing pressure starts 2026

Regulatory focus on safety/biomarkers raises trial evidentiary bars for covalent inhibitors; expedited pathways remain but require robust safety data. IRA price negotiations begin 2026, pressuring net prices; NICE thresholds ~£20–30k/QALY for oncology. NIH FY2024 ~$52B and Horizon Europe €95.5B sustain translational partnerships; export controls add sourcing risk.

| Metric | Value |

|---|---|

| NIH FY2024 | $52B |

| Horizon Europe | €95.5B (2021–27) |

| Cancer incidence | 19.3M (2020) |

What is included in the product

Provides a data-backed PESTLE review of Biomea Fusion—assessing Political, Economic, Social, Technological, Environmental and Legal factors tied to its industry and regional dynamics to identify risks and opportunities. Designed for executives and investors, it includes detailed subpoints, forward-looking scenario insights and clean formatting ready for reports, decks or funding materials.

Biomea Fusion PESTLE Analysis delivers a clean, visually segmented summary for quick interpretation and meeting-ready insertion into presentations, while allowing users to add contextual notes and share concise insights across teams to streamline external risk assessment and strategic planning.

Economic factors

Capital market conditions and financing runway

Clinical-stage biotechs like Biomea Fusion depend on equity raises and partnering; higher rates and lower risk appetite — with the 10-year U.S. Treasury near 4.1% in July 2025 — increase dilution pressure and slow fundraising cadence. Volatile public markets can defer follow-on raises, constraining BMF-219 trial size and timelines. Milestone-rich collaborations offset cash burn but cede future upside. Prudent cash management preserves pivotal-study optionality.

Cost of clinical development and CDMO inflation

CMC scale-up for irreversible inhibitors requires specialized analytics and process development, often adding 20–40% to early manufacturing budgets. Competition for CDMO slots has pushed lead times to 12–24 months and spot pricing up roughly 10–15% Y/Y in 2023–24. Investing in process robustness early can cut rework and batch-failure rates by over 30%. Geographic arbitrage and multi-year framework agreements commonly cap unit costs by 10–25%.

Market size in oncology and metabolic diseases

Oncology offers premium pricing with the global oncology drug market ~USD 200–230B in 2024 but patient populations are segmented by mutations, limiting addressable share per asset. Metabolic diseases such as diabetes represent larger volumes—global diabetes drug market ~USD 60–80B in 2024—but face tighter payer controls and price pressure. Biomea’s indication mix must weigh peak sales upside in oncology against reimbursement risk in metabolic. Sequencing oncology first can clinically validate MoA and de-risk broader metabolic launches.

Payer mix and affordability dynamics

US payer mix matters: commercial enrollment ~178M, Medicare ~66M and Medicaid ~84M (CMS 2023), driving differential net price realization as commercial plans often secure higher list-to-net spreads while Medicare/Medicaid impose statutory/managed discounts; EU HTA bodies (NICE threshold ~20–30k GBP/QALY) insist on comparative effectiveness and budget impact; co-pay design affects adherence in chronic metabolic care; value-based contracts tie payment to outcomes.

- Payer enrollment: commercial 178M; Medicare 66M; Medicaid 84M (CMS 2023)

- NICE threshold ~20–30k GBP/QALY

- Co-pay levels materially influence adherence in chronic metabolic diseases

- Value-based contracts align economics with outcomes

FX and international launch economics

Safety-focused regulators raise trial bar for covalent inhibitors; IRA pricing pressure starts 2026

Higher rates (US 10y ~4.1% Jul 2025) raise dilution risk and slow equity raises; CDMO lead times 12–24m and +10–15% spot pricing lift early CMC spend; oncology market ~USD 210B (2024) offers high pricing but narrow mutation-defined pools; EUR/USD ~1.08 (2024) and external reference pricing compress net prices across regions.

| Metric | Value |

|---|---|

| US 10y | ~4.1% (Jul 2025) |

| CDMO lead time | 12–24 months |

| Oncology market | ~USD 210B (2024) |

| EUR/USD | ~1.08 (2024) |

Same Document Delivered

Biomea Fusion PESTLE Analysis

The Biomea Fusion PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are the final file with no placeholders or teasers. After payment you’ll instantly download this exact, professionally structured report.

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our focused PESTLE Analysis of Biomea Fusion — revealing how regulatory shifts, biotech funding cycles, and emerging technologies will shape its trajectory. Ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report to download the complete, editable analysis and make data-driven decisions.

Political factors

Regulatory climate and FDA/EMA priorities

Regulators prioritize safety, first-in-class mechanisms, and explicit biomarker strategies, driving trial designs for irreversible covalent inhibitors like BMF-219 and raising the bar on off-target profiling. Oncology and metabolic pathways remain eligible for expedited pathways (Breakthrough, Fast Track), yet evidentiary standards and rigorous safety datasets are enforced. Ongoing, documented engagement with FDA/EMA on covalent binding risks and selectivity is critical. Growing FDA/EMA emphasis on real-world evidence may allow post-approval commitments for BMF-219.

Drug pricing reforms and payer policy influence

US drug negotiation under the IRA begins in 2026, creating downward pressure on net prices while EU reference pricing often cuts list prices by up to ~30%; oncology typically sustains higher willingness-to-pay (NICE thresholds £20–30k/QALY) whereas metabolic indications face stricter cost-effectiveness bars (€20–40k/QALY). Early HEOR is essential to defend value, and government-dominant payers (public funding >80% in many EU diabetes markets) will shape launch sequencing.

Public funding and translational research support

NIH funding (~$52B FY2024) and EU Horizon Europe (€95.5B 2021–27) drive preclinical collaborations and target validation for covalent chemistries, while US Cancer Moonshot (goal: 50% reduction in cancer deaths over 25 years) fuels trial networks; shifting budget cycles and grant priorities constrain access to shared infrastructure/biomarker platforms, making deep academia partnerships a hedge against political funding volatility.

Geopolitical supply chain stability

Export controls and trade tensions constrain sourcing of reagents, APIs and specialized CDMO capacity, raising lead times and costs for Biomea Fusion’s R&D and GMP production. Political instability can delay GMP batch releases and global-trial logistics, disrupting timelines and patient enrollment. Localizing critical steps or dual-sourcing and pursuing harmonized standards ease cross-border sample and data transfers and reduce operational risk.

- Export controls: restrict access to certain reagents and technologies

- Trade tensions: increase lead times and supplier risk

- Localize/dual-source: mitigates single-point failures

- Harmonized standards: facilitate cross-border trials and data flow

Healthcare system capacity and national strategies

National cancer incidence (19.3 million new cases in 2020) and diabetes prevalence (537 million adults in 2021) drive screening and eligible patient pools, shaping Biomea Fusion trial feasibility and market size. Political support for precision medicine and reimbursement is raising genomic testing uptake, expanding genetically defined cancer cohorts. Centralized ethics boards and accredited trial sites can cut start-up timelines by weeks, while regional care disparities demand tailored access programs.

- Policy impact: national cancer/diabetes plans define patient pools

- Precision support: increases genomic testing and eligible cohorts

- Regulatory: accreditation/centralized review speeds trial initiation

- Access: regional disparities require targeted programs

Safety-focused regulators raise trial bar for covalent inhibitors; IRA pricing pressure starts 2026

Regulatory focus on safety/biomarkers raises trial evidentiary bars for covalent inhibitors; expedited pathways remain but require robust safety data. IRA price negotiations begin 2026, pressuring net prices; NICE thresholds ~£20–30k/QALY for oncology. NIH FY2024 ~$52B and Horizon Europe €95.5B sustain translational partnerships; export controls add sourcing risk.

| Metric | Value |

|---|---|

| NIH FY2024 | $52B |

| Horizon Europe | €95.5B (2021–27) |

| Cancer incidence | 19.3M (2020) |

What is included in the product

Provides a data-backed PESTLE review of Biomea Fusion—assessing Political, Economic, Social, Technological, Environmental and Legal factors tied to its industry and regional dynamics to identify risks and opportunities. Designed for executives and investors, it includes detailed subpoints, forward-looking scenario insights and clean formatting ready for reports, decks or funding materials.

Biomea Fusion PESTLE Analysis delivers a clean, visually segmented summary for quick interpretation and meeting-ready insertion into presentations, while allowing users to add contextual notes and share concise insights across teams to streamline external risk assessment and strategic planning.

Economic factors

Capital market conditions and financing runway

Clinical-stage biotechs like Biomea Fusion depend on equity raises and partnering; higher rates and lower risk appetite — with the 10-year U.S. Treasury near 4.1% in July 2025 — increase dilution pressure and slow fundraising cadence. Volatile public markets can defer follow-on raises, constraining BMF-219 trial size and timelines. Milestone-rich collaborations offset cash burn but cede future upside. Prudent cash management preserves pivotal-study optionality.

Cost of clinical development and CDMO inflation

CMC scale-up for irreversible inhibitors requires specialized analytics and process development, often adding 20–40% to early manufacturing budgets. Competition for CDMO slots has pushed lead times to 12–24 months and spot pricing up roughly 10–15% Y/Y in 2023–24. Investing in process robustness early can cut rework and batch-failure rates by over 30%. Geographic arbitrage and multi-year framework agreements commonly cap unit costs by 10–25%.

Market size in oncology and metabolic diseases

Oncology offers premium pricing with the global oncology drug market ~USD 200–230B in 2024 but patient populations are segmented by mutations, limiting addressable share per asset. Metabolic diseases such as diabetes represent larger volumes—global diabetes drug market ~USD 60–80B in 2024—but face tighter payer controls and price pressure. Biomea’s indication mix must weigh peak sales upside in oncology against reimbursement risk in metabolic. Sequencing oncology first can clinically validate MoA and de-risk broader metabolic launches.

Payer mix and affordability dynamics

US payer mix matters: commercial enrollment ~178M, Medicare ~66M and Medicaid ~84M (CMS 2023), driving differential net price realization as commercial plans often secure higher list-to-net spreads while Medicare/Medicaid impose statutory/managed discounts; EU HTA bodies (NICE threshold ~20–30k GBP/QALY) insist on comparative effectiveness and budget impact; co-pay design affects adherence in chronic metabolic care; value-based contracts tie payment to outcomes.

- Payer enrollment: commercial 178M; Medicare 66M; Medicaid 84M (CMS 2023)

- NICE threshold ~20–30k GBP/QALY

- Co-pay levels materially influence adherence in chronic metabolic diseases

- Value-based contracts align economics with outcomes

FX and international launch economics

Safety-focused regulators raise trial bar for covalent inhibitors; IRA pricing pressure starts 2026

Higher rates (US 10y ~4.1% Jul 2025) raise dilution risk and slow equity raises; CDMO lead times 12–24m and +10–15% spot pricing lift early CMC spend; oncology market ~USD 210B (2024) offers high pricing but narrow mutation-defined pools; EUR/USD ~1.08 (2024) and external reference pricing compress net prices across regions.

| Metric | Value |

|---|---|

| US 10y | ~4.1% (Jul 2025) |

| CDMO lead time | 12–24 months |

| Oncology market | ~USD 210B (2024) |

| EUR/USD | ~1.08 (2024) |

Same Document Delivered

Biomea Fusion PESTLE Analysis

The Biomea Fusion PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are the final file with no placeholders or teasers. After payment you’ll instantly download this exact, professionally structured report.