BioNTech PESTLE Analysis

Your Shortcut to Market Insight Starts Here

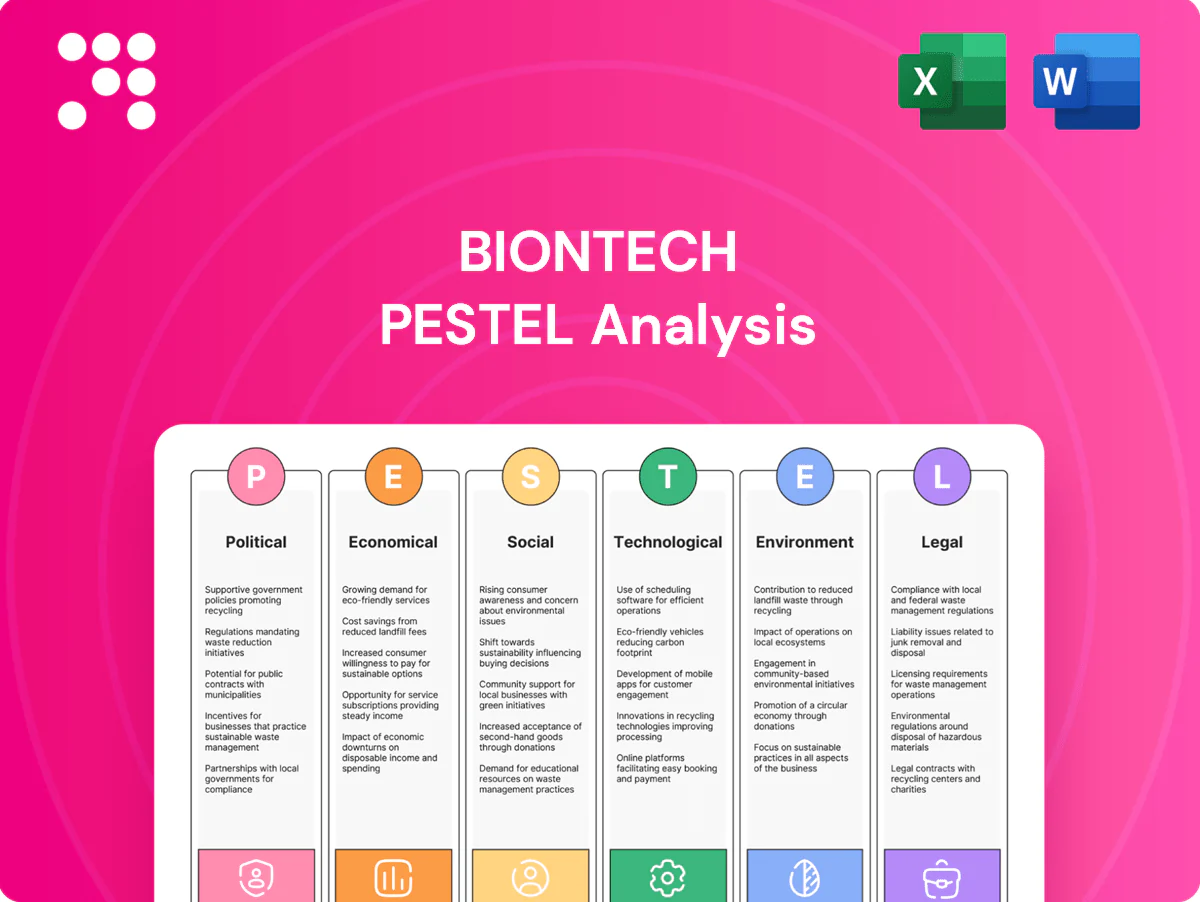

Our PESTLE analysis of BioNTech reveals how political regulation, economic cycles, social demand, technological innovation, legal risks, and environmental trends converge to shape the company’s trajectory. Actionable insights highlight regulatory threats and growth levers for investors and strategists. Purchase the full report to access the complete, editable breakdown and tactical recommendations.

Political factors

Regulatory priorities and funding

Shifts in EU and US health policy can speed or stall approvals and public procurement for vaccines and oncology therapies, affecting BioNTech revenue timing and market access. EU HERA’s preparedness envelope of about €6 billion for 2022–27 and continued BARDA grant programs influence availability of advance purchase commitments and R&D grants. Changes in leadership or health agendas can reallocate funds between infectious disease and oncology, so BioNTech must align pipelines to these priorities.

Geopolitical supply chain exposure

Export controls on lipids, biologics inputs and specialized equipment have disrupted mRNA supply chains, forcing BioNTech to adapt as regionalization doubled some site-capacity targets and raised operating costs by an estimated ~20% in 2023–24; geopolitical tensions and sanctions complicated trial site selection and enrollment across Asia and Russia/Ukraine-affected regions, so diversifying suppliers and sites—targeting >1bn annual dose capacity by 2024—became vital for resilience.

Vaccine nationalism and allocation

Vaccine nationalism can delay global demand timing and push up prices as governments prioritize domestic access; by end-2024 Pfizer-BioNTech had delivered over 3 billion doses, highlighting uneven early distribution. Advance market commitments secure volumes but include delivery penalties and intense political scrutiny, raising reputational risk. Public procurement often favors local manufacturing footprints, and coordinating multiple government stakeholders adds operational complexity and contractual risk.

Public–private partnerships

Collaborations with national institutes and defense health agencies can de-risk early R&D for BioNTech, offering earlier validation and non-dilutive funding; public-sector support during the COVID-19 response contributed to global vaccine R&D funding totals exceeding $10 billion. Such deals often impose pricing, access, and tech-transfer obligations and add transparency and reporting burdens. The trade-off is earlier market validation versus administrative and contractual constraints.

- Non-dilutive funding: public R&D support >$10bn (global COVID-era)

- Obligations: pricing, access, tech-transfer

- Cost: higher administrative/reporting load

- Benefit: earlier validation, de-risking

Trade, IP, and localization policies

Debates over a TRIPS waiver, supported by more than 100 WTO members since 2021, keep perceived IP security for mRNA platforms under scrutiny; South Africa and India have been leading proponents. Many governments tie public tenders to local fill–finish or tech transfer agreements, complicating supply logistics. Regulatory harmonization (ICH, EMA–FDA cooperation) eases filings, yet divergence across LMICs persists, forcing BioNTech to balance IP protection with market entry and local partnerships.

- 100+ WTO members backed TRIPS waiver talks since 2021

- Governments increasingly require local fill–finish/tech transfer for tenders

- Harmonization exists (ICH, EMA–FDA) but regulatory divergence remains

- BioNTech must hedge IP protection against access via partnerships

EU HERA €6bn and BARDA grants steer procurements; export controls raised costs ~20%

Shifts in EU/US policy affect approvals and procurement; EU HERA ~€6bn (2022–27) and BARDA grants shape advance commitments. Export controls and regionalization raised operating costs ~20% in 2023–24; Pfizer‑BioNTech delivered >3bn doses by end‑2024. Over 100 WTO members backed TRIPS waiver talks; many governments require local fill–finish/tech transfer for tenders.

| Indicator | Value | Political Impact |

|---|---|---|

| EU HERA | €6bn (2022–27) | Advance purchase support |

| BARDA | Ongoing grants | Non‑dilutive R&D funding |

| Deliveries | >3bn doses (end‑2024) | Uneven global access |

| Cost rise | ~20% (2023–24) | Supply‑chain regionalization |

| TRIPS support | 100+ members | IP scrutiny |

What is included in the product

Explores how external macro-environmental factors uniquely affect BioNTech across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors and strategists; formatted for direct use in plans, decks and reports.

A concise, visually segmented BioNTech PESTLE summary that eases stakeholder alignment by distilling regulatory, economic, and technological risks into slide-ready, editable notes for meetings or consultant reports.

Economic factors

Post-pandemic revenue normalization

Post-pandemic Comirnaty sales, which contributed to Pfizer-BioNTech’s roughly $36.8bn vaccine revenue peak in 2021–22, have shifted from mass campaigns to seasonal, high-risk cohorts, compressing volumes and raising demand variability. This variability makes inventory management and capacity utilization central to margin stability. Diversifying into oncology is economically critical to offset cyclical vaccine cashflows.

Payer pressure and HTA outcomes

Payer decisions hinge on cost-effectiveness: NICE typically applies £20,000–30,000/QALY and Germany’s AMNOG triggers early price negotiations after launch, pressuring BioNTech to price precision oncology to reflect survival and QALY gains. Outcomes‑based contracts, which covered roughly 15% of European oncology deals by 2024, are expanding to limit budget impact, while increasing HTA demands—about 70% of assessments now request robust real‑world evidence to support sustainable pricing.

R&D intensity and capital allocation

mRNA, cell therapies and combination regimens demand sustained high R&D spend; BioNTech reported R&D expenses of about €1.9bn in 2023, underlining ongoing capital intensity. Milestone and royalty receipts from partners like Pfizer help smooth cash burn and supported liquidity of roughly €4.3bn at end-2023. Prioritizing late-stage assets raises risk-adjusted returns, while portfolio pruning limits dilution and redundant trials.

FX and input cost volatility

BioNTech earns most revenue in USD/EUR while key inputs—synthetic lipids, specialized enzymes and energy—are sourced globally, so currency swings directly affect reported results and COGS; hedging programs reduce but do not eliminate translation and transaction risk, and long‑term supply contracts help stabilize input pricing.

- Revenue currency: USD/EUR

- Inputs: lipids, enzymes, energy (global procurement)

- Hedging: mitigates but residual risk

- Long‑term contracts: stabilize costs

Manufacturing scale and utilization

BioNTech retains the large mRNA manufacturing footprint built for COVID-19, capable of producing billions of doses, but reduced vaccine demand has left facilities underutilized, pressuring gross margins and elevating fixed-cost absorption per unit. Modular, multi-product lines and ongoing tech transfers to regional sites aim to boost throughput, enable tender participation, and capture scale efficiencies across oncology and seasonal vaccines.

- Capacity: billions of doses built

- Risk: underutilization reduces gross margins

- Benefit: modular lines raise throughput

- Strategy: tech transfer unlocks regional tenders and scale

EU HERA €6bn and BARDA grants steer procurements; export controls raised costs ~20%

Post‑COVID vaccine sales fell from a peak Pfizer‑BioNTech vaccine revenue of about $36.8bn (2021–22) to seasonal/high‑risk cohorts, increasing demand volatility and stressing capacity utilization. R&D remains capital‑intensive (BioNTech R&D ~€1.9bn in 2023) while liquidity (~€4.3bn end‑2023) and partner milestones smooth cashflow. Payers press pricing via QALY thresholds and outcomes contracts; ~70% of HTAs now seek robust RWE.

| Metric | Value |

|---|---|

| Vaccine peak revenue (2021–22) | $36.8bn |

| R&D (2023) | €1.9bn |

| Liquidity (end‑2023) | €4.3bn |

| HTAs requesting RWE | ~70% |

Preview the Actual Deliverable

BioNTech PESTLE Analysis

The preview shown here is the exact BioNTech PESTLE analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors with concise insights and implications for strategy and investment. No placeholders or teasers—this is the final downloadable file delivered exactly as displayed.

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of BioNTech reveals how political regulation, economic cycles, social demand, technological innovation, legal risks, and environmental trends converge to shape the company’s trajectory. Actionable insights highlight regulatory threats and growth levers for investors and strategists. Purchase the full report to access the complete, editable breakdown and tactical recommendations.

Political factors

Regulatory priorities and funding

Shifts in EU and US health policy can speed or stall approvals and public procurement for vaccines and oncology therapies, affecting BioNTech revenue timing and market access. EU HERA’s preparedness envelope of about €6 billion for 2022–27 and continued BARDA grant programs influence availability of advance purchase commitments and R&D grants. Changes in leadership or health agendas can reallocate funds between infectious disease and oncology, so BioNTech must align pipelines to these priorities.

Geopolitical supply chain exposure

Export controls on lipids, biologics inputs and specialized equipment have disrupted mRNA supply chains, forcing BioNTech to adapt as regionalization doubled some site-capacity targets and raised operating costs by an estimated ~20% in 2023–24; geopolitical tensions and sanctions complicated trial site selection and enrollment across Asia and Russia/Ukraine-affected regions, so diversifying suppliers and sites—targeting >1bn annual dose capacity by 2024—became vital for resilience.

Vaccine nationalism and allocation

Vaccine nationalism can delay global demand timing and push up prices as governments prioritize domestic access; by end-2024 Pfizer-BioNTech had delivered over 3 billion doses, highlighting uneven early distribution. Advance market commitments secure volumes but include delivery penalties and intense political scrutiny, raising reputational risk. Public procurement often favors local manufacturing footprints, and coordinating multiple government stakeholders adds operational complexity and contractual risk.

Public–private partnerships

Collaborations with national institutes and defense health agencies can de-risk early R&D for BioNTech, offering earlier validation and non-dilutive funding; public-sector support during the COVID-19 response contributed to global vaccine R&D funding totals exceeding $10 billion. Such deals often impose pricing, access, and tech-transfer obligations and add transparency and reporting burdens. The trade-off is earlier market validation versus administrative and contractual constraints.

- Non-dilutive funding: public R&D support >$10bn (global COVID-era)

- Obligations: pricing, access, tech-transfer

- Cost: higher administrative/reporting load

- Benefit: earlier validation, de-risking

Trade, IP, and localization policies

Debates over a TRIPS waiver, supported by more than 100 WTO members since 2021, keep perceived IP security for mRNA platforms under scrutiny; South Africa and India have been leading proponents. Many governments tie public tenders to local fill–finish or tech transfer agreements, complicating supply logistics. Regulatory harmonization (ICH, EMA–FDA cooperation) eases filings, yet divergence across LMICs persists, forcing BioNTech to balance IP protection with market entry and local partnerships.

- 100+ WTO members backed TRIPS waiver talks since 2021

- Governments increasingly require local fill–finish/tech transfer for tenders

- Harmonization exists (ICH, EMA–FDA) but regulatory divergence remains

- BioNTech must hedge IP protection against access via partnerships

EU HERA €6bn and BARDA grants steer procurements; export controls raised costs ~20%

Shifts in EU/US policy affect approvals and procurement; EU HERA ~€6bn (2022–27) and BARDA grants shape advance commitments. Export controls and regionalization raised operating costs ~20% in 2023–24; Pfizer‑BioNTech delivered >3bn doses by end‑2024. Over 100 WTO members backed TRIPS waiver talks; many governments require local fill–finish/tech transfer for tenders.

| Indicator | Value | Political Impact |

|---|---|---|

| EU HERA | €6bn (2022–27) | Advance purchase support |

| BARDA | Ongoing grants | Non‑dilutive R&D funding |

| Deliveries | >3bn doses (end‑2024) | Uneven global access |

| Cost rise | ~20% (2023–24) | Supply‑chain regionalization |

| TRIPS support | 100+ members | IP scrutiny |

What is included in the product

Explores how external macro-environmental factors uniquely affect BioNTech across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors and strategists; formatted for direct use in plans, decks and reports.

A concise, visually segmented BioNTech PESTLE summary that eases stakeholder alignment by distilling regulatory, economic, and technological risks into slide-ready, editable notes for meetings or consultant reports.

Economic factors

Post-pandemic revenue normalization

Post-pandemic Comirnaty sales, which contributed to Pfizer-BioNTech’s roughly $36.8bn vaccine revenue peak in 2021–22, have shifted from mass campaigns to seasonal, high-risk cohorts, compressing volumes and raising demand variability. This variability makes inventory management and capacity utilization central to margin stability. Diversifying into oncology is economically critical to offset cyclical vaccine cashflows.

Payer pressure and HTA outcomes

Payer decisions hinge on cost-effectiveness: NICE typically applies £20,000–30,000/QALY and Germany’s AMNOG triggers early price negotiations after launch, pressuring BioNTech to price precision oncology to reflect survival and QALY gains. Outcomes‑based contracts, which covered roughly 15% of European oncology deals by 2024, are expanding to limit budget impact, while increasing HTA demands—about 70% of assessments now request robust real‑world evidence to support sustainable pricing.

R&D intensity and capital allocation

mRNA, cell therapies and combination regimens demand sustained high R&D spend; BioNTech reported R&D expenses of about €1.9bn in 2023, underlining ongoing capital intensity. Milestone and royalty receipts from partners like Pfizer help smooth cash burn and supported liquidity of roughly €4.3bn at end-2023. Prioritizing late-stage assets raises risk-adjusted returns, while portfolio pruning limits dilution and redundant trials.

FX and input cost volatility

BioNTech earns most revenue in USD/EUR while key inputs—synthetic lipids, specialized enzymes and energy—are sourced globally, so currency swings directly affect reported results and COGS; hedging programs reduce but do not eliminate translation and transaction risk, and long‑term supply contracts help stabilize input pricing.

- Revenue currency: USD/EUR

- Inputs: lipids, enzymes, energy (global procurement)

- Hedging: mitigates but residual risk

- Long‑term contracts: stabilize costs

Manufacturing scale and utilization

BioNTech retains the large mRNA manufacturing footprint built for COVID-19, capable of producing billions of doses, but reduced vaccine demand has left facilities underutilized, pressuring gross margins and elevating fixed-cost absorption per unit. Modular, multi-product lines and ongoing tech transfers to regional sites aim to boost throughput, enable tender participation, and capture scale efficiencies across oncology and seasonal vaccines.

- Capacity: billions of doses built

- Risk: underutilization reduces gross margins

- Benefit: modular lines raise throughput

- Strategy: tech transfer unlocks regional tenders and scale

EU HERA €6bn and BARDA grants steer procurements; export controls raised costs ~20%

Post‑COVID vaccine sales fell from a peak Pfizer‑BioNTech vaccine revenue of about $36.8bn (2021–22) to seasonal/high‑risk cohorts, increasing demand volatility and stressing capacity utilization. R&D remains capital‑intensive (BioNTech R&D ~€1.9bn in 2023) while liquidity (~€4.3bn end‑2023) and partner milestones smooth cashflow. Payers press pricing via QALY thresholds and outcomes contracts; ~70% of HTAs now seek robust RWE.

| Metric | Value |

|---|---|

| Vaccine peak revenue (2021–22) | $36.8bn |

| R&D (2023) | €1.9bn |

| Liquidity (end‑2023) | €4.3bn |

| HTAs requesting RWE | ~70% |

Preview the Actual Deliverable

BioNTech PESTLE Analysis

The preview shown here is the exact BioNTech PESTLE analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors with concise insights and implications for strategy and investment. No placeholders or teasers—this is the final downloadable file delivered exactly as displayed.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of BioNTech reveals how political regulation, economic cycles, social demand, technological innovation, legal risks, and environmental trends converge to shape the company’s trajectory. Actionable insights highlight regulatory threats and growth levers for investors and strategists. Purchase the full report to access the complete, editable breakdown and tactical recommendations.

Political factors

Regulatory priorities and funding

Shifts in EU and US health policy can speed or stall approvals and public procurement for vaccines and oncology therapies, affecting BioNTech revenue timing and market access. EU HERA’s preparedness envelope of about €6 billion for 2022–27 and continued BARDA grant programs influence availability of advance purchase commitments and R&D grants. Changes in leadership or health agendas can reallocate funds between infectious disease and oncology, so BioNTech must align pipelines to these priorities.

Geopolitical supply chain exposure

Export controls on lipids, biologics inputs and specialized equipment have disrupted mRNA supply chains, forcing BioNTech to adapt as regionalization doubled some site-capacity targets and raised operating costs by an estimated ~20% in 2023–24; geopolitical tensions and sanctions complicated trial site selection and enrollment across Asia and Russia/Ukraine-affected regions, so diversifying suppliers and sites—targeting >1bn annual dose capacity by 2024—became vital for resilience.

Vaccine nationalism and allocation

Vaccine nationalism can delay global demand timing and push up prices as governments prioritize domestic access; by end-2024 Pfizer-BioNTech had delivered over 3 billion doses, highlighting uneven early distribution. Advance market commitments secure volumes but include delivery penalties and intense political scrutiny, raising reputational risk. Public procurement often favors local manufacturing footprints, and coordinating multiple government stakeholders adds operational complexity and contractual risk.

Public–private partnerships

Collaborations with national institutes and defense health agencies can de-risk early R&D for BioNTech, offering earlier validation and non-dilutive funding; public-sector support during the COVID-19 response contributed to global vaccine R&D funding totals exceeding $10 billion. Such deals often impose pricing, access, and tech-transfer obligations and add transparency and reporting burdens. The trade-off is earlier market validation versus administrative and contractual constraints.

- Non-dilutive funding: public R&D support >$10bn (global COVID-era)

- Obligations: pricing, access, tech-transfer

- Cost: higher administrative/reporting load

- Benefit: earlier validation, de-risking

Trade, IP, and localization policies

Debates over a TRIPS waiver, supported by more than 100 WTO members since 2021, keep perceived IP security for mRNA platforms under scrutiny; South Africa and India have been leading proponents. Many governments tie public tenders to local fill–finish or tech transfer agreements, complicating supply logistics. Regulatory harmonization (ICH, EMA–FDA cooperation) eases filings, yet divergence across LMICs persists, forcing BioNTech to balance IP protection with market entry and local partnerships.

- 100+ WTO members backed TRIPS waiver talks since 2021

- Governments increasingly require local fill–finish/tech transfer for tenders

- Harmonization exists (ICH, EMA–FDA) but regulatory divergence remains

- BioNTech must hedge IP protection against access via partnerships

EU HERA €6bn and BARDA grants steer procurements; export controls raised costs ~20%

Shifts in EU/US policy affect approvals and procurement; EU HERA ~€6bn (2022–27) and BARDA grants shape advance commitments. Export controls and regionalization raised operating costs ~20% in 2023–24; Pfizer‑BioNTech delivered >3bn doses by end‑2024. Over 100 WTO members backed TRIPS waiver talks; many governments require local fill–finish/tech transfer for tenders.

| Indicator | Value | Political Impact |

|---|---|---|

| EU HERA | €6bn (2022–27) | Advance purchase support |

| BARDA | Ongoing grants | Non‑dilutive R&D funding |

| Deliveries | >3bn doses (end‑2024) | Uneven global access |

| Cost rise | ~20% (2023–24) | Supply‑chain regionalization |

| TRIPS support | 100+ members | IP scrutiny |

What is included in the product

Explores how external macro-environmental factors uniquely affect BioNTech across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors and strategists; formatted for direct use in plans, decks and reports.

A concise, visually segmented BioNTech PESTLE summary that eases stakeholder alignment by distilling regulatory, economic, and technological risks into slide-ready, editable notes for meetings or consultant reports.

Economic factors

Post-pandemic revenue normalization

Post-pandemic Comirnaty sales, which contributed to Pfizer-BioNTech’s roughly $36.8bn vaccine revenue peak in 2021–22, have shifted from mass campaigns to seasonal, high-risk cohorts, compressing volumes and raising demand variability. This variability makes inventory management and capacity utilization central to margin stability. Diversifying into oncology is economically critical to offset cyclical vaccine cashflows.

Payer pressure and HTA outcomes

Payer decisions hinge on cost-effectiveness: NICE typically applies £20,000–30,000/QALY and Germany’s AMNOG triggers early price negotiations after launch, pressuring BioNTech to price precision oncology to reflect survival and QALY gains. Outcomes‑based contracts, which covered roughly 15% of European oncology deals by 2024, are expanding to limit budget impact, while increasing HTA demands—about 70% of assessments now request robust real‑world evidence to support sustainable pricing.

R&D intensity and capital allocation

mRNA, cell therapies and combination regimens demand sustained high R&D spend; BioNTech reported R&D expenses of about €1.9bn in 2023, underlining ongoing capital intensity. Milestone and royalty receipts from partners like Pfizer help smooth cash burn and supported liquidity of roughly €4.3bn at end-2023. Prioritizing late-stage assets raises risk-adjusted returns, while portfolio pruning limits dilution and redundant trials.

FX and input cost volatility

BioNTech earns most revenue in USD/EUR while key inputs—synthetic lipids, specialized enzymes and energy—are sourced globally, so currency swings directly affect reported results and COGS; hedging programs reduce but do not eliminate translation and transaction risk, and long‑term supply contracts help stabilize input pricing.

- Revenue currency: USD/EUR

- Inputs: lipids, enzymes, energy (global procurement)

- Hedging: mitigates but residual risk

- Long‑term contracts: stabilize costs

Manufacturing scale and utilization

BioNTech retains the large mRNA manufacturing footprint built for COVID-19, capable of producing billions of doses, but reduced vaccine demand has left facilities underutilized, pressuring gross margins and elevating fixed-cost absorption per unit. Modular, multi-product lines and ongoing tech transfers to regional sites aim to boost throughput, enable tender participation, and capture scale efficiencies across oncology and seasonal vaccines.

- Capacity: billions of doses built

- Risk: underutilization reduces gross margins

- Benefit: modular lines raise throughput

- Strategy: tech transfer unlocks regional tenders and scale

EU HERA €6bn and BARDA grants steer procurements; export controls raised costs ~20%

Post‑COVID vaccine sales fell from a peak Pfizer‑BioNTech vaccine revenue of about $36.8bn (2021–22) to seasonal/high‑risk cohorts, increasing demand volatility and stressing capacity utilization. R&D remains capital‑intensive (BioNTech R&D ~€1.9bn in 2023) while liquidity (~€4.3bn end‑2023) and partner milestones smooth cashflow. Payers press pricing via QALY thresholds and outcomes contracts; ~70% of HTAs now seek robust RWE.

| Metric | Value |

|---|---|

| Vaccine peak revenue (2021–22) | $36.8bn |

| R&D (2023) | €1.9bn |

| Liquidity (end‑2023) | €4.3bn |

| HTAs requesting RWE | ~70% |

Preview the Actual Deliverable

BioNTech PESTLE Analysis

The preview shown here is the exact BioNTech PESTLE analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors with concise insights and implications for strategy and investment. No placeholders or teasers—this is the final downloadable file delivered exactly as displayed.