Bioventus Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Bioventus faces moderate buyer power, evolving supplier dynamics, and growing substitute threats as innovation and M&A reshape orthobiologics; regulatory pressure and scale advantages further influence competitiveness. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to access detailed, actionable insights for strategy or investment decisions.

Suppliers Bargaining Power

Concentrated tissue and biomaterial sources

Orthobiologics depend on a concentrated set of allograft tissue banks and specialized HA/collagen suppliers, giving suppliers significant leverage over pricing and availability. Donor screening and accreditation further narrow eligible sources and increase dependency. Recalls or supply shortages can cascade across Bioventus product lines, so the company must pursue multi-source procurement and strict quality oversight to mitigate risk.

Specialized sterilization and manufacturing

ETO/gamma sterilization and cleanroom processing remain capacity-constrained and tightly regulated; as of 2024 regulators enforce ISO 11135/11137 and FDA 21 CFR Part 820 standards for validated sterilization and quality systems. Contract manufacturers with ISO 13485/FDA certifications wield bargaining power because switching triggers costly validations, line qualifications and tech transfers that are lengthy and resource-intensive. These frictions elevate supplier leverage over lead times and pricing.

Regulatory and quality switching costs

Supplier changes trigger re-validation and updated technical files, often imposing six-figure requalification costs and regulatory notification processes that can take months, deterring rapid switching and strengthening incumbent suppliers. Ongoing audits and QA monitoring create recurrent administrative burdens that lock in relationships. Under time pressure suppliers can negotiate premium terms, compressing buyer margins and reducing bargaining power.

Proprietary components and IP

- IP-protected components limit supplier alternatives

- Proprietary chemistries increase switching costs

- Licensing/exclusivity raises COGS

- Access often needs volume or co-development

Logistics and geopolitical exposures

In 2024 global supply chains for reagents, resins and packaging continued to face transport, customs and geopolitical disruptions that raised lead times and spot costs; cold-chain and sterile handling added handling layers and premiums, pressuring Bioventus margins as suppliers increasingly passed surcharges through amid currency volatility.

- 2024: heightened transport/customs risk

- Cold-chain/sterility = higher OPEX

- FX swings enable supplier surcharges

Supplier leverage, ISO/FDA sterilization & 2024 shocks drive >$100k revalidation, 3-6mo

Concentrated allograft/HA suppliers and IP‑protected components give suppliers strong leverage; supplier switches trigger revalidation costs often >$100,000 and 3–6 months of delay. 2024 enforcement of ISO 11135/11137 and FDA 21 CFR Part 820 keeps sterilization/CMO capacity tight, raising lead times and premiums. Geopolitical, customs and cold‑chain disruptions in 2024 pushed spot input costs and enabled supplier surcharges.

| Metric | 2024 Value/Impact | Notes |

|---|---|---|

| Requalification cost | >$100,000 | Typical validation/tech transfer |

| Revalidation time | 3–6 months | Regulatory notifications |

| Regulatory standards | ISO 11135/11137, FDA 21 CFR Part 820 | Sterilization/quality |

What is included in the product

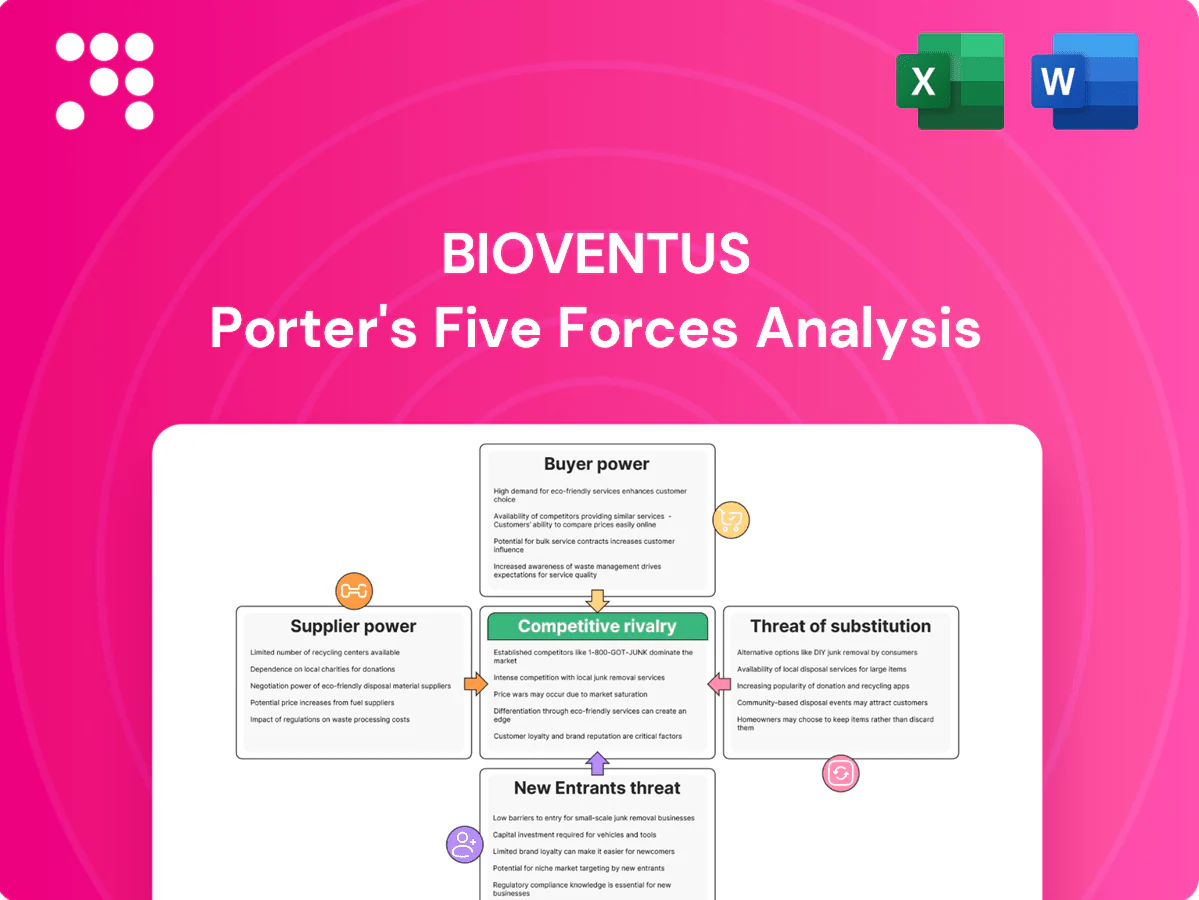

Concise Porter's Five Forces analysis of Bioventus identifying competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities with actionable insights for defense and growth.

One-sheet Porter’s Five Forces for Bioventus—clear, customizable pressure levels with an instant spider chart and clean layout ready for pitch decks or boardrooms; no macros, swap in your own data, and integrate seamlessly with Excel dashboards or the paired Word deep-dive report.

Customers Bargaining Power

GPO/IDN contracting pressure

Hospitals and IDNs aggregate volume via GPOs that negotiate contracts covering more than 90% of US hospitals, enforcing tiered pricing and rebate structures. Competitive tenders from GPO/IDNs compress margins across portfolios, while preferred-vendor status depends on price, service, and clinical data. Losing formulary position can quickly erode market share.

Surgeon preference but rising stewardship

Orthopedic surgeons remain key influencers in product selection, but in 2024 Bioventus's commercial results (~$700M revenue) show surgeon preference no longer guarantees adoption as hospital value analysis and stewardship increasingly scrutinize clinical evidence and cost.

Payer reimbursement gatekeeping

As of 2024, payer coverage remains variable for OA injections and bone-healing therapies, with prior authorizations and step therapy commonly required, increasing time-to-treatment and price sensitivity; rising real-world evidence expectations push Bioventus to fund registries and outcomes studies, while coding changes or claim denials have materially reduced utilization in multiple markets.

International tender dynamics

International tenders in EMEA/APAC impose price ceilings and prioritize the lowest compliant bids, often compressing margins by 20–40% in 2024; local content rules and reference pricing further intensify buyer leverage. Contract cycles can abruptly reallocate market share—wins/losses of 30–50% within a single cycle are common—so compliance and service KPIs (SLAs, uptime, training) become key differentiators beyond unit price.

- Price pressure: tenders cut prices 20–40% (2024)

- Local content: raises entry barriers, favors incumbents

- Share volatility: 30–50% reallocation per cycle

- Differentiators: SLAs, regulatory compliance, service KPIs

Availability of lower-cost alternatives

Commoditized graft substitutes and legacy therapies offer cheaper options, letting buyers trade down when Bioventus differentiation is unclear; bundled orthopedic deals from large rivals and IDNs further amplify leverage—orthobiologics market estimated at $4.2B in 2024, pressuring premium pricing.

- Commoditization: cheaper grafts erode premium share

- Trade-down risk: unclear differentiation boosts switching

- Bundling: IDN contracts increase buyer power

- Defense: demonstrable clinical/economic value required

Buyers wield leverage: tenders cut prices 20-40%; $700M firm faces a $4.2B orthobiologics market

Buyers wield strong leverage: GPOs/IDNs drive tiered contracts and tenders that cut prices 20–40% and can reallocate 30–50% share per cycle. Surgeon preference matters but hospital value analysis, payer prior auth and step therapy increase price sensitivity; Bioventus revenue ~700M in 2024 faces a $4.2B orthobiologics market with high trade-down risk.

| Metric | 2024 |

|---|---|

| Bioventus revenue | $700M |

| Price cuts via tenders | 20–40% |

| Share reallocation | 30–50% |

| Market size (orthobiologics) | $4.2B |

Full Version Awaits

Bioventus Porter's Five Forces Analysis

This preview displays the complete Bioventus Porter's Five Forces analysis—the same professionally researched and formatted document you’ll receive immediately after purchase. It includes competitive rivalry, supplier and buyer power, threat of entry and substitutes, ready for download and use without alterations.

Go Beyond the Preview—Access the Full Strategic Report

Bioventus faces moderate buyer power, evolving supplier dynamics, and growing substitute threats as innovation and M&A reshape orthobiologics; regulatory pressure and scale advantages further influence competitiveness. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to access detailed, actionable insights for strategy or investment decisions.

Suppliers Bargaining Power

Concentrated tissue and biomaterial sources

Orthobiologics depend on a concentrated set of allograft tissue banks and specialized HA/collagen suppliers, giving suppliers significant leverage over pricing and availability. Donor screening and accreditation further narrow eligible sources and increase dependency. Recalls or supply shortages can cascade across Bioventus product lines, so the company must pursue multi-source procurement and strict quality oversight to mitigate risk.

Specialized sterilization and manufacturing

ETO/gamma sterilization and cleanroom processing remain capacity-constrained and tightly regulated; as of 2024 regulators enforce ISO 11135/11137 and FDA 21 CFR Part 820 standards for validated sterilization and quality systems. Contract manufacturers with ISO 13485/FDA certifications wield bargaining power because switching triggers costly validations, line qualifications and tech transfers that are lengthy and resource-intensive. These frictions elevate supplier leverage over lead times and pricing.

Regulatory and quality switching costs

Supplier changes trigger re-validation and updated technical files, often imposing six-figure requalification costs and regulatory notification processes that can take months, deterring rapid switching and strengthening incumbent suppliers. Ongoing audits and QA monitoring create recurrent administrative burdens that lock in relationships. Under time pressure suppliers can negotiate premium terms, compressing buyer margins and reducing bargaining power.

Proprietary components and IP

- IP-protected components limit supplier alternatives

- Proprietary chemistries increase switching costs

- Licensing/exclusivity raises COGS

- Access often needs volume or co-development

Logistics and geopolitical exposures

In 2024 global supply chains for reagents, resins and packaging continued to face transport, customs and geopolitical disruptions that raised lead times and spot costs; cold-chain and sterile handling added handling layers and premiums, pressuring Bioventus margins as suppliers increasingly passed surcharges through amid currency volatility.

- 2024: heightened transport/customs risk

- Cold-chain/sterility = higher OPEX

- FX swings enable supplier surcharges

Supplier leverage, ISO/FDA sterilization & 2024 shocks drive >$100k revalidation, 3-6mo

Concentrated allograft/HA suppliers and IP‑protected components give suppliers strong leverage; supplier switches trigger revalidation costs often >$100,000 and 3–6 months of delay. 2024 enforcement of ISO 11135/11137 and FDA 21 CFR Part 820 keeps sterilization/CMO capacity tight, raising lead times and premiums. Geopolitical, customs and cold‑chain disruptions in 2024 pushed spot input costs and enabled supplier surcharges.

| Metric | 2024 Value/Impact | Notes |

|---|---|---|

| Requalification cost | >$100,000 | Typical validation/tech transfer |

| Revalidation time | 3–6 months | Regulatory notifications |

| Regulatory standards | ISO 11135/11137, FDA 21 CFR Part 820 | Sterilization/quality |

What is included in the product

Concise Porter's Five Forces analysis of Bioventus identifying competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities with actionable insights for defense and growth.

One-sheet Porter’s Five Forces for Bioventus—clear, customizable pressure levels with an instant spider chart and clean layout ready for pitch decks or boardrooms; no macros, swap in your own data, and integrate seamlessly with Excel dashboards or the paired Word deep-dive report.

Customers Bargaining Power

GPO/IDN contracting pressure

Hospitals and IDNs aggregate volume via GPOs that negotiate contracts covering more than 90% of US hospitals, enforcing tiered pricing and rebate structures. Competitive tenders from GPO/IDNs compress margins across portfolios, while preferred-vendor status depends on price, service, and clinical data. Losing formulary position can quickly erode market share.

Surgeon preference but rising stewardship

Orthopedic surgeons remain key influencers in product selection, but in 2024 Bioventus's commercial results (~$700M revenue) show surgeon preference no longer guarantees adoption as hospital value analysis and stewardship increasingly scrutinize clinical evidence and cost.

Payer reimbursement gatekeeping

As of 2024, payer coverage remains variable for OA injections and bone-healing therapies, with prior authorizations and step therapy commonly required, increasing time-to-treatment and price sensitivity; rising real-world evidence expectations push Bioventus to fund registries and outcomes studies, while coding changes or claim denials have materially reduced utilization in multiple markets.

International tender dynamics

International tenders in EMEA/APAC impose price ceilings and prioritize the lowest compliant bids, often compressing margins by 20–40% in 2024; local content rules and reference pricing further intensify buyer leverage. Contract cycles can abruptly reallocate market share—wins/losses of 30–50% within a single cycle are common—so compliance and service KPIs (SLAs, uptime, training) become key differentiators beyond unit price.

- Price pressure: tenders cut prices 20–40% (2024)

- Local content: raises entry barriers, favors incumbents

- Share volatility: 30–50% reallocation per cycle

- Differentiators: SLAs, regulatory compliance, service KPIs

Availability of lower-cost alternatives

Commoditized graft substitutes and legacy therapies offer cheaper options, letting buyers trade down when Bioventus differentiation is unclear; bundled orthopedic deals from large rivals and IDNs further amplify leverage—orthobiologics market estimated at $4.2B in 2024, pressuring premium pricing.

- Commoditization: cheaper grafts erode premium share

- Trade-down risk: unclear differentiation boosts switching

- Bundling: IDN contracts increase buyer power

- Defense: demonstrable clinical/economic value required

Buyers wield leverage: tenders cut prices 20-40%; $700M firm faces a $4.2B orthobiologics market

Buyers wield strong leverage: GPOs/IDNs drive tiered contracts and tenders that cut prices 20–40% and can reallocate 30–50% share per cycle. Surgeon preference matters but hospital value analysis, payer prior auth and step therapy increase price sensitivity; Bioventus revenue ~700M in 2024 faces a $4.2B orthobiologics market with high trade-down risk.

| Metric | 2024 |

|---|---|

| Bioventus revenue | $700M |

| Price cuts via tenders | 20–40% |

| Share reallocation | 30–50% |

| Market size (orthobiologics) | $4.2B |

Full Version Awaits

Bioventus Porter's Five Forces Analysis

This preview displays the complete Bioventus Porter's Five Forces analysis—the same professionally researched and formatted document you’ll receive immediately after purchase. It includes competitive rivalry, supplier and buyer power, threat of entry and substitutes, ready for download and use without alterations.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Bioventus faces moderate buyer power, evolving supplier dynamics, and growing substitute threats as innovation and M&A reshape orthobiologics; regulatory pressure and scale advantages further influence competitiveness. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to access detailed, actionable insights for strategy or investment decisions.

Suppliers Bargaining Power

Concentrated tissue and biomaterial sources

Orthobiologics depend on a concentrated set of allograft tissue banks and specialized HA/collagen suppliers, giving suppliers significant leverage over pricing and availability. Donor screening and accreditation further narrow eligible sources and increase dependency. Recalls or supply shortages can cascade across Bioventus product lines, so the company must pursue multi-source procurement and strict quality oversight to mitigate risk.

Specialized sterilization and manufacturing

ETO/gamma sterilization and cleanroom processing remain capacity-constrained and tightly regulated; as of 2024 regulators enforce ISO 11135/11137 and FDA 21 CFR Part 820 standards for validated sterilization and quality systems. Contract manufacturers with ISO 13485/FDA certifications wield bargaining power because switching triggers costly validations, line qualifications and tech transfers that are lengthy and resource-intensive. These frictions elevate supplier leverage over lead times and pricing.

Regulatory and quality switching costs

Supplier changes trigger re-validation and updated technical files, often imposing six-figure requalification costs and regulatory notification processes that can take months, deterring rapid switching and strengthening incumbent suppliers. Ongoing audits and QA monitoring create recurrent administrative burdens that lock in relationships. Under time pressure suppliers can negotiate premium terms, compressing buyer margins and reducing bargaining power.

Proprietary components and IP

- IP-protected components limit supplier alternatives

- Proprietary chemistries increase switching costs

- Licensing/exclusivity raises COGS

- Access often needs volume or co-development

Logistics and geopolitical exposures

In 2024 global supply chains for reagents, resins and packaging continued to face transport, customs and geopolitical disruptions that raised lead times and spot costs; cold-chain and sterile handling added handling layers and premiums, pressuring Bioventus margins as suppliers increasingly passed surcharges through amid currency volatility.

- 2024: heightened transport/customs risk

- Cold-chain/sterility = higher OPEX

- FX swings enable supplier surcharges

Supplier leverage, ISO/FDA sterilization & 2024 shocks drive >$100k revalidation, 3-6mo

Concentrated allograft/HA suppliers and IP‑protected components give suppliers strong leverage; supplier switches trigger revalidation costs often >$100,000 and 3–6 months of delay. 2024 enforcement of ISO 11135/11137 and FDA 21 CFR Part 820 keeps sterilization/CMO capacity tight, raising lead times and premiums. Geopolitical, customs and cold‑chain disruptions in 2024 pushed spot input costs and enabled supplier surcharges.

| Metric | 2024 Value/Impact | Notes |

|---|---|---|

| Requalification cost | >$100,000 | Typical validation/tech transfer |

| Revalidation time | 3–6 months | Regulatory notifications |

| Regulatory standards | ISO 11135/11137, FDA 21 CFR Part 820 | Sterilization/quality |

What is included in the product

Concise Porter's Five Forces analysis of Bioventus identifying competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities with actionable insights for defense and growth.

One-sheet Porter’s Five Forces for Bioventus—clear, customizable pressure levels with an instant spider chart and clean layout ready for pitch decks or boardrooms; no macros, swap in your own data, and integrate seamlessly with Excel dashboards or the paired Word deep-dive report.

Customers Bargaining Power

GPO/IDN contracting pressure

Hospitals and IDNs aggregate volume via GPOs that negotiate contracts covering more than 90% of US hospitals, enforcing tiered pricing and rebate structures. Competitive tenders from GPO/IDNs compress margins across portfolios, while preferred-vendor status depends on price, service, and clinical data. Losing formulary position can quickly erode market share.

Surgeon preference but rising stewardship

Orthopedic surgeons remain key influencers in product selection, but in 2024 Bioventus's commercial results (~$700M revenue) show surgeon preference no longer guarantees adoption as hospital value analysis and stewardship increasingly scrutinize clinical evidence and cost.

Payer reimbursement gatekeeping

As of 2024, payer coverage remains variable for OA injections and bone-healing therapies, with prior authorizations and step therapy commonly required, increasing time-to-treatment and price sensitivity; rising real-world evidence expectations push Bioventus to fund registries and outcomes studies, while coding changes or claim denials have materially reduced utilization in multiple markets.

International tender dynamics

International tenders in EMEA/APAC impose price ceilings and prioritize the lowest compliant bids, often compressing margins by 20–40% in 2024; local content rules and reference pricing further intensify buyer leverage. Contract cycles can abruptly reallocate market share—wins/losses of 30–50% within a single cycle are common—so compliance and service KPIs (SLAs, uptime, training) become key differentiators beyond unit price.

- Price pressure: tenders cut prices 20–40% (2024)

- Local content: raises entry barriers, favors incumbents

- Share volatility: 30–50% reallocation per cycle

- Differentiators: SLAs, regulatory compliance, service KPIs

Availability of lower-cost alternatives

Commoditized graft substitutes and legacy therapies offer cheaper options, letting buyers trade down when Bioventus differentiation is unclear; bundled orthopedic deals from large rivals and IDNs further amplify leverage—orthobiologics market estimated at $4.2B in 2024, pressuring premium pricing.

- Commoditization: cheaper grafts erode premium share

- Trade-down risk: unclear differentiation boosts switching

- Bundling: IDN contracts increase buyer power

- Defense: demonstrable clinical/economic value required

Buyers wield leverage: tenders cut prices 20-40%; $700M firm faces a $4.2B orthobiologics market

Buyers wield strong leverage: GPOs/IDNs drive tiered contracts and tenders that cut prices 20–40% and can reallocate 30–50% share per cycle. Surgeon preference matters but hospital value analysis, payer prior auth and step therapy increase price sensitivity; Bioventus revenue ~700M in 2024 faces a $4.2B orthobiologics market with high trade-down risk.

| Metric | 2024 |

|---|---|

| Bioventus revenue | $700M |

| Price cuts via tenders | 20–40% |

| Share reallocation | 30–50% |

| Market size (orthobiologics) | $4.2B |

Full Version Awaits

Bioventus Porter's Five Forces Analysis

This preview displays the complete Bioventus Porter's Five Forces analysis—the same professionally researched and formatted document you’ll receive immediately after purchase. It includes competitive rivalry, supplier and buyer power, threat of entry and substitutes, ready for download and use without alterations.