Basler Kantonalbank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

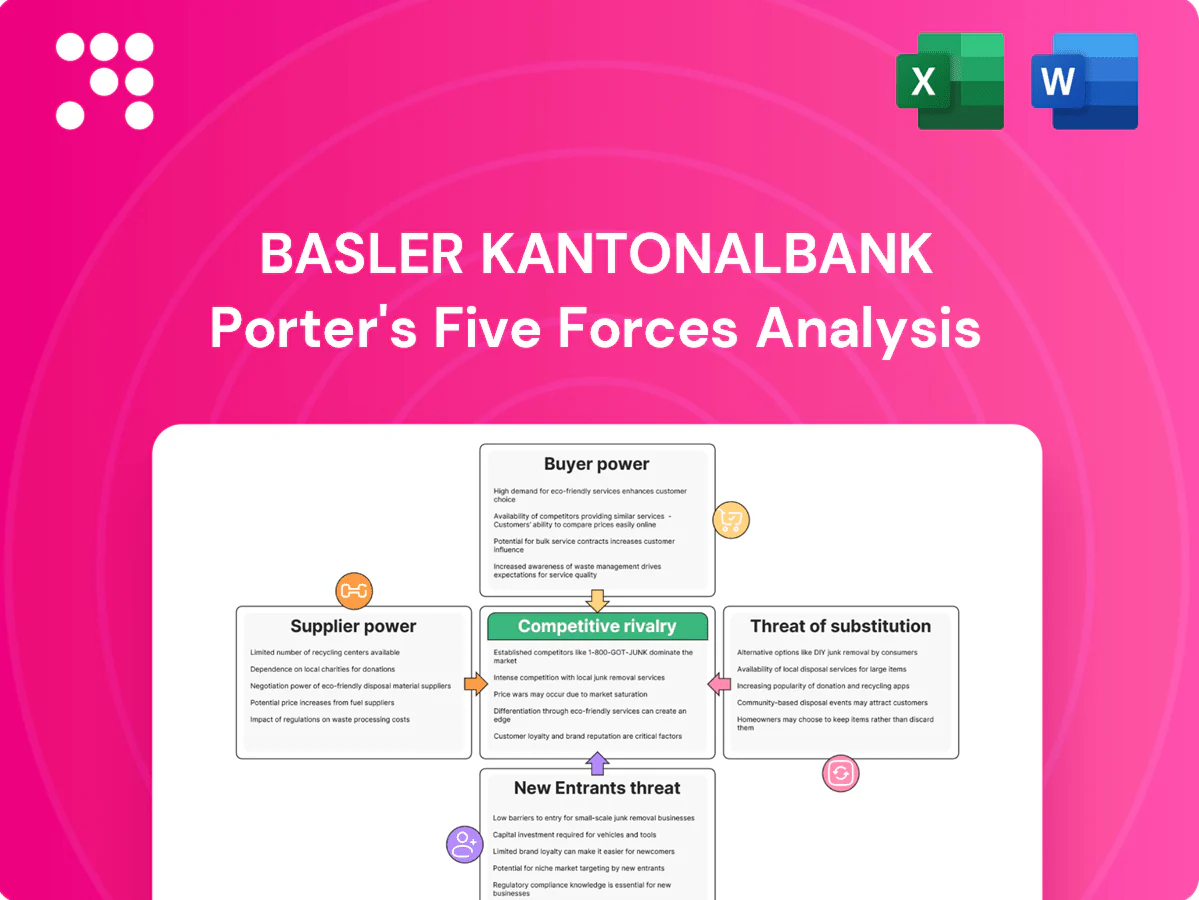

Basler Kantonalbank faces moderate rivalry with regional peers, strong regulatory constraints, and mixed bargaining power from corporate clients and retail depositors.

Supplier and technology pressures are rising as fintech and interbank platforms shift cost and service dynamics, while barriers to entry remain relatively high due to cantonal backing.

Our snapshot highlights strategic strengths and vulnerabilities that matter for investors and managers seeking clarity on market positioning.

This preview is just the beginning. The full Porter's Five Forces Analysis provides force-by-force ratings, visuals, and tailored implications to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentrated core IT vendors

Basler Kantonalbank relies on a concentrated set of core banking platform and cloud partners (commonly 2–4 providers), creating meaningful switching costs and integration risk. Vendor concentration can push up pricing and limit customization leverage, especially under long-term commitments. Multi-year contracts (typically 5–7 years) and Swiss compliance requirements provide negotiation touchpoints. Co-development arrangements and long vendor tenures partially mitigate opportunism.

Wholesale funding and capital markets

Although deposit funding remains strong for Basler Kantonalbank, supplemental wholesale funding exposes the bank to market spreads and rating-sensitive costs, and in stressed markets liquidity suppliers can gain pricing power. Cantonal backing and a solid credit profile help temper spread volatility. Access to diversified maturities and covered bond markets supports balanced term funding and reduces rollover risk.

Payment networks and data utilities

Card schemes, Swiss payment rails (SIC/SWITCH) and data bureaus set largely standardized fees — interchange and scheme fees typically range from 0.2–1.3% per transaction — leaving little room for bilateral negotiation. Interoperability requirements and technical standards constrain switching and lock-in. Scale across transaction volumes and consortium governance (bank members of schemes) provide some negotiating leverage. FINMA and SNB oversight limits extreme fee increases.

Specialist talent and advisory partners

Competition for tech, risk and wealth advisors gives suppliers clear leverage on wages and terms; in 2024 Basler Kantonalbank, a canton-owned lender, faces hiring pressure from larger Swiss banks and Basel's pharma sector. Basel's deep talent pipeline (University of Basel, founded 1460) and cantonal stability aid retention, while internal training and nearshoring reduce reliance on scarce specialist profiles.

- High supplier leverage: competing employers

- Defensive strengths: cantonal ownership, local universities

- Mitigants: reskilling programs, nearshoring

Regulatory and compliance infrastructure

Compliance-tech, audit and reg‑reporting vendors are mission‑critical for Basler Kantonalbank, increasing supplier dependency; the global regtech market exceeded USD 10bn in 2024, underscoring vendor concentration and investment pressure. Frequent FINMA and industry rule updates raise switching and upgrade costs, while active participation in the Swiss Bankers Association helps shape standards. A modular IT architecture reduces single‑vendor lock‑in and migration costs.

- Vendor dependency: mission‑critical systems

- Market size: regtech > USD 10bn (2024)

- Regulatory churn: FINMA/industry updates increase upgrade costs

- Industry influence: Swiss Bankers Association participation

- Mitigation: modular architecture limits lock‑in

Swiss cantonal bank: moderate supplier power - regtech >USD 10bn, 5-7yr contracts

Basler Kantonalbank faces moderate supplier power: concentrated core-platform and regtech vendors (regtech > USD 10bn in 2024) and multi-year contracts (5–7 years) create switching costs, while cantonal backing and modular IT reduce leverage. Payment schemes (interchange 0.2–1.3%) and liquidity markets can push costs under stress, but scale and Swiss oversight limit extremes.

| Metric | Value (2024) |

|---|---|

| Regtech market | USD >10bn |

| Contract length | 5–7 years |

| Interchange fees | 0.2–1.3% |

| Vendor count (core) | 2–4 |

What is included in the product

Uncovers competitive drivers, customer bargaining power, supplier influence, threat of new entrants and substitutes, and regulatory barriers shaping Basler Kantonalbank's profitability and market position; includes strategic implications and tailored recommendations.

A concise one-sheet Porter's Five Forces for Basler Kantonalbank—clarifies competitive pressures, regulatory risks and deposit/credit threats for rapid board and investor decisions.

Customers Bargaining Power

Sticky regional retail deposits

Local households value trust, proximity and the cantonal link, which reduces price sensitivity and supports sticky retail deposits. Digital rate comparison raises elasticity in a rising-rate cycle, but Swiss household deposits remained around CHF 1.1 trillion in 2024, underscoring overall deposit stickiness. Bundled products and relationship pricing preserve margins, while service quality and branch access remain clear differentiators in Basel.

SMEs with multi-banking

According to the Swiss Bankers Association 2024 survey, about 60% of Swiss SMEs maintain relationships with two or more banks, increasing bidding pressure on loans and fees. Tendering for mortgages, leasing and cash management pushed average competitive discounts to roughly 10–15% in 2024 industry benchmarks. BKB’s regional knowledge and sub‑48‑hour credit decisions counterbalance price demands, while cross‑sell and advisory embedment—lifting share of wallet by ~30–40% for advised clients—raise switching costs.

Affluent and private banking clients

Affluent clients increasingly compare performance, fees and platform features, exercising high bargaining power in 2024 as global ETF assets exceeded USD 10 trillion, compressing advisory margins through low-cost passive options. Fee transparency and ETF adoption push prices down, but BKB's personalized mandates and local discretion justify premium fees for bespoke solutions. Open architecture expands product choice while maintaining advisor control through curated offerings.

Public sector and institutions

Public sector and institutional clients prioritize safety, cost efficiency and policy alignment, using scale to extract favorable terms; Basel-Stadt had about 203,000 residents in 2024, underpinning sizeable municipal balance sheets and procurement volumes.

Formal procurement rules intensify price competition, but Basler Kantonalbank’s cantonal mandate and capital stability offer a service-and-trust advantage beyond lowest price; established, multi-year mandates lower churn risk.

- Negotiation leverage: high via aggregated mandates

- Procurement effect: formalized price pressure

- Bank edge: cantonal backing and stability

- Client stickiness: long-term institutional relationships

Digital-first customers

Digital-first customers raise bargaining power as neobanks set low-fee, instant-UX benchmarks—2024 data shows neobanks captured about 18% of new retail accounts in Europe while mobile banking adoption in Switzerland reached roughly 70% in 2024; easy switching via digital onboarding and APIs reduces friction, forcing Basler Kantonalbank to match app speed and fee transparency. Continuous app improvements and bundled value-added services help retain users, and clear pricing plus loyalty benefits materially curb churn.

Customers pressure banks: CHF 1.1tn, SMEs 60% multibank

Customers wield moderate-to-high bargaining power: households stick (CHF 1.1tn deposits in 2024) but rate comparison raises elasticity; 60% of SMEs multi-bank relationships drive 10–15% loan/fee discounts; affluent clients pressure fees as global ETF assets >USD 10tn; institutions use procurement rules but cantonal backing limits churn.

| Metric | 2024 |

|---|---|

| Household deposits | CHF 1.1tn |

| SMEs multi-bank | ~60% |

| Loan/fee discounts | 10–15% |

| Global ETF assets | >USD 10tn |

| Neobank new accounts (EU) | ~18% |

Preview Before You Purchase

Basler Kantonalbank Porter's Five Forces Analysis

This preview shows the exact Basler Kantonalbank Porter’s Five Forces analysis you’ll receive—fully formatted and ready to use. It contains the complete competitive assessment, threat and supplier analyses, and strategic implications as presented in the finished file. No placeholders or samples: once you purchase, you’ll get instant access to this identical document.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Basler Kantonalbank faces moderate rivalry with regional peers, strong regulatory constraints, and mixed bargaining power from corporate clients and retail depositors.

Supplier and technology pressures are rising as fintech and interbank platforms shift cost and service dynamics, while barriers to entry remain relatively high due to cantonal backing.

Our snapshot highlights strategic strengths and vulnerabilities that matter for investors and managers seeking clarity on market positioning.

This preview is just the beginning. The full Porter's Five Forces Analysis provides force-by-force ratings, visuals, and tailored implications to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentrated core IT vendors

Basler Kantonalbank relies on a concentrated set of core banking platform and cloud partners (commonly 2–4 providers), creating meaningful switching costs and integration risk. Vendor concentration can push up pricing and limit customization leverage, especially under long-term commitments. Multi-year contracts (typically 5–7 years) and Swiss compliance requirements provide negotiation touchpoints. Co-development arrangements and long vendor tenures partially mitigate opportunism.

Wholesale funding and capital markets

Although deposit funding remains strong for Basler Kantonalbank, supplemental wholesale funding exposes the bank to market spreads and rating-sensitive costs, and in stressed markets liquidity suppliers can gain pricing power. Cantonal backing and a solid credit profile help temper spread volatility. Access to diversified maturities and covered bond markets supports balanced term funding and reduces rollover risk.

Payment networks and data utilities

Card schemes, Swiss payment rails (SIC/SWITCH) and data bureaus set largely standardized fees — interchange and scheme fees typically range from 0.2–1.3% per transaction — leaving little room for bilateral negotiation. Interoperability requirements and technical standards constrain switching and lock-in. Scale across transaction volumes and consortium governance (bank members of schemes) provide some negotiating leverage. FINMA and SNB oversight limits extreme fee increases.

Specialist talent and advisory partners

Competition for tech, risk and wealth advisors gives suppliers clear leverage on wages and terms; in 2024 Basler Kantonalbank, a canton-owned lender, faces hiring pressure from larger Swiss banks and Basel's pharma sector. Basel's deep talent pipeline (University of Basel, founded 1460) and cantonal stability aid retention, while internal training and nearshoring reduce reliance on scarce specialist profiles.

- High supplier leverage: competing employers

- Defensive strengths: cantonal ownership, local universities

- Mitigants: reskilling programs, nearshoring

Regulatory and compliance infrastructure

Compliance-tech, audit and reg‑reporting vendors are mission‑critical for Basler Kantonalbank, increasing supplier dependency; the global regtech market exceeded USD 10bn in 2024, underscoring vendor concentration and investment pressure. Frequent FINMA and industry rule updates raise switching and upgrade costs, while active participation in the Swiss Bankers Association helps shape standards. A modular IT architecture reduces single‑vendor lock‑in and migration costs.

- Vendor dependency: mission‑critical systems

- Market size: regtech > USD 10bn (2024)

- Regulatory churn: FINMA/industry updates increase upgrade costs

- Industry influence: Swiss Bankers Association participation

- Mitigation: modular architecture limits lock‑in

Swiss cantonal bank: moderate supplier power - regtech >USD 10bn, 5-7yr contracts

Basler Kantonalbank faces moderate supplier power: concentrated core-platform and regtech vendors (regtech > USD 10bn in 2024) and multi-year contracts (5–7 years) create switching costs, while cantonal backing and modular IT reduce leverage. Payment schemes (interchange 0.2–1.3%) and liquidity markets can push costs under stress, but scale and Swiss oversight limit extremes.

| Metric | Value (2024) |

|---|---|

| Regtech market | USD >10bn |

| Contract length | 5–7 years |

| Interchange fees | 0.2–1.3% |

| Vendor count (core) | 2–4 |

What is included in the product

Uncovers competitive drivers, customer bargaining power, supplier influence, threat of new entrants and substitutes, and regulatory barriers shaping Basler Kantonalbank's profitability and market position; includes strategic implications and tailored recommendations.

A concise one-sheet Porter's Five Forces for Basler Kantonalbank—clarifies competitive pressures, regulatory risks and deposit/credit threats for rapid board and investor decisions.

Customers Bargaining Power

Sticky regional retail deposits

Local households value trust, proximity and the cantonal link, which reduces price sensitivity and supports sticky retail deposits. Digital rate comparison raises elasticity in a rising-rate cycle, but Swiss household deposits remained around CHF 1.1 trillion in 2024, underscoring overall deposit stickiness. Bundled products and relationship pricing preserve margins, while service quality and branch access remain clear differentiators in Basel.

SMEs with multi-banking

According to the Swiss Bankers Association 2024 survey, about 60% of Swiss SMEs maintain relationships with two or more banks, increasing bidding pressure on loans and fees. Tendering for mortgages, leasing and cash management pushed average competitive discounts to roughly 10–15% in 2024 industry benchmarks. BKB’s regional knowledge and sub‑48‑hour credit decisions counterbalance price demands, while cross‑sell and advisory embedment—lifting share of wallet by ~30–40% for advised clients—raise switching costs.

Affluent and private banking clients

Affluent clients increasingly compare performance, fees and platform features, exercising high bargaining power in 2024 as global ETF assets exceeded USD 10 trillion, compressing advisory margins through low-cost passive options. Fee transparency and ETF adoption push prices down, but BKB's personalized mandates and local discretion justify premium fees for bespoke solutions. Open architecture expands product choice while maintaining advisor control through curated offerings.

Public sector and institutions

Public sector and institutional clients prioritize safety, cost efficiency and policy alignment, using scale to extract favorable terms; Basel-Stadt had about 203,000 residents in 2024, underpinning sizeable municipal balance sheets and procurement volumes.

Formal procurement rules intensify price competition, but Basler Kantonalbank’s cantonal mandate and capital stability offer a service-and-trust advantage beyond lowest price; established, multi-year mandates lower churn risk.

- Negotiation leverage: high via aggregated mandates

- Procurement effect: formalized price pressure

- Bank edge: cantonal backing and stability

- Client stickiness: long-term institutional relationships

Digital-first customers

Digital-first customers raise bargaining power as neobanks set low-fee, instant-UX benchmarks—2024 data shows neobanks captured about 18% of new retail accounts in Europe while mobile banking adoption in Switzerland reached roughly 70% in 2024; easy switching via digital onboarding and APIs reduces friction, forcing Basler Kantonalbank to match app speed and fee transparency. Continuous app improvements and bundled value-added services help retain users, and clear pricing plus loyalty benefits materially curb churn.

Customers pressure banks: CHF 1.1tn, SMEs 60% multibank

Customers wield moderate-to-high bargaining power: households stick (CHF 1.1tn deposits in 2024) but rate comparison raises elasticity; 60% of SMEs multi-bank relationships drive 10–15% loan/fee discounts; affluent clients pressure fees as global ETF assets >USD 10tn; institutions use procurement rules but cantonal backing limits churn.

| Metric | 2024 |

|---|---|

| Household deposits | CHF 1.1tn |

| SMEs multi-bank | ~60% |

| Loan/fee discounts | 10–15% |

| Global ETF assets | >USD 10tn |

| Neobank new accounts (EU) | ~18% |

Preview Before You Purchase

Basler Kantonalbank Porter's Five Forces Analysis

This preview shows the exact Basler Kantonalbank Porter’s Five Forces analysis you’ll receive—fully formatted and ready to use. It contains the complete competitive assessment, threat and supplier analyses, and strategic implications as presented in the finished file. No placeholders or samples: once you purchase, you’ll get instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Basler Kantonalbank faces moderate rivalry with regional peers, strong regulatory constraints, and mixed bargaining power from corporate clients and retail depositors.

Supplier and technology pressures are rising as fintech and interbank platforms shift cost and service dynamics, while barriers to entry remain relatively high due to cantonal backing.

Our snapshot highlights strategic strengths and vulnerabilities that matter for investors and managers seeking clarity on market positioning.

This preview is just the beginning. The full Porter's Five Forces Analysis provides force-by-force ratings, visuals, and tailored implications to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentrated core IT vendors

Basler Kantonalbank relies on a concentrated set of core banking platform and cloud partners (commonly 2–4 providers), creating meaningful switching costs and integration risk. Vendor concentration can push up pricing and limit customization leverage, especially under long-term commitments. Multi-year contracts (typically 5–7 years) and Swiss compliance requirements provide negotiation touchpoints. Co-development arrangements and long vendor tenures partially mitigate opportunism.

Wholesale funding and capital markets

Although deposit funding remains strong for Basler Kantonalbank, supplemental wholesale funding exposes the bank to market spreads and rating-sensitive costs, and in stressed markets liquidity suppliers can gain pricing power. Cantonal backing and a solid credit profile help temper spread volatility. Access to diversified maturities and covered bond markets supports balanced term funding and reduces rollover risk.

Payment networks and data utilities

Card schemes, Swiss payment rails (SIC/SWITCH) and data bureaus set largely standardized fees — interchange and scheme fees typically range from 0.2–1.3% per transaction — leaving little room for bilateral negotiation. Interoperability requirements and technical standards constrain switching and lock-in. Scale across transaction volumes and consortium governance (bank members of schemes) provide some negotiating leverage. FINMA and SNB oversight limits extreme fee increases.

Specialist talent and advisory partners

Competition for tech, risk and wealth advisors gives suppliers clear leverage on wages and terms; in 2024 Basler Kantonalbank, a canton-owned lender, faces hiring pressure from larger Swiss banks and Basel's pharma sector. Basel's deep talent pipeline (University of Basel, founded 1460) and cantonal stability aid retention, while internal training and nearshoring reduce reliance on scarce specialist profiles.

- High supplier leverage: competing employers

- Defensive strengths: cantonal ownership, local universities

- Mitigants: reskilling programs, nearshoring

Regulatory and compliance infrastructure

Compliance-tech, audit and reg‑reporting vendors are mission‑critical for Basler Kantonalbank, increasing supplier dependency; the global regtech market exceeded USD 10bn in 2024, underscoring vendor concentration and investment pressure. Frequent FINMA and industry rule updates raise switching and upgrade costs, while active participation in the Swiss Bankers Association helps shape standards. A modular IT architecture reduces single‑vendor lock‑in and migration costs.

- Vendor dependency: mission‑critical systems

- Market size: regtech > USD 10bn (2024)

- Regulatory churn: FINMA/industry updates increase upgrade costs

- Industry influence: Swiss Bankers Association participation

- Mitigation: modular architecture limits lock‑in

Swiss cantonal bank: moderate supplier power - regtech >USD 10bn, 5-7yr contracts

Basler Kantonalbank faces moderate supplier power: concentrated core-platform and regtech vendors (regtech > USD 10bn in 2024) and multi-year contracts (5–7 years) create switching costs, while cantonal backing and modular IT reduce leverage. Payment schemes (interchange 0.2–1.3%) and liquidity markets can push costs under stress, but scale and Swiss oversight limit extremes.

| Metric | Value (2024) |

|---|---|

| Regtech market | USD >10bn |

| Contract length | 5–7 years |

| Interchange fees | 0.2–1.3% |

| Vendor count (core) | 2–4 |

What is included in the product

Uncovers competitive drivers, customer bargaining power, supplier influence, threat of new entrants and substitutes, and regulatory barriers shaping Basler Kantonalbank's profitability and market position; includes strategic implications and tailored recommendations.

A concise one-sheet Porter's Five Forces for Basler Kantonalbank—clarifies competitive pressures, regulatory risks and deposit/credit threats for rapid board and investor decisions.

Customers Bargaining Power

Sticky regional retail deposits

Local households value trust, proximity and the cantonal link, which reduces price sensitivity and supports sticky retail deposits. Digital rate comparison raises elasticity in a rising-rate cycle, but Swiss household deposits remained around CHF 1.1 trillion in 2024, underscoring overall deposit stickiness. Bundled products and relationship pricing preserve margins, while service quality and branch access remain clear differentiators in Basel.

SMEs with multi-banking

According to the Swiss Bankers Association 2024 survey, about 60% of Swiss SMEs maintain relationships with two or more banks, increasing bidding pressure on loans and fees. Tendering for mortgages, leasing and cash management pushed average competitive discounts to roughly 10–15% in 2024 industry benchmarks. BKB’s regional knowledge and sub‑48‑hour credit decisions counterbalance price demands, while cross‑sell and advisory embedment—lifting share of wallet by ~30–40% for advised clients—raise switching costs.

Affluent and private banking clients

Affluent clients increasingly compare performance, fees and platform features, exercising high bargaining power in 2024 as global ETF assets exceeded USD 10 trillion, compressing advisory margins through low-cost passive options. Fee transparency and ETF adoption push prices down, but BKB's personalized mandates and local discretion justify premium fees for bespoke solutions. Open architecture expands product choice while maintaining advisor control through curated offerings.

Public sector and institutions

Public sector and institutional clients prioritize safety, cost efficiency and policy alignment, using scale to extract favorable terms; Basel-Stadt had about 203,000 residents in 2024, underpinning sizeable municipal balance sheets and procurement volumes.

Formal procurement rules intensify price competition, but Basler Kantonalbank’s cantonal mandate and capital stability offer a service-and-trust advantage beyond lowest price; established, multi-year mandates lower churn risk.

- Negotiation leverage: high via aggregated mandates

- Procurement effect: formalized price pressure

- Bank edge: cantonal backing and stability

- Client stickiness: long-term institutional relationships

Digital-first customers

Digital-first customers raise bargaining power as neobanks set low-fee, instant-UX benchmarks—2024 data shows neobanks captured about 18% of new retail accounts in Europe while mobile banking adoption in Switzerland reached roughly 70% in 2024; easy switching via digital onboarding and APIs reduces friction, forcing Basler Kantonalbank to match app speed and fee transparency. Continuous app improvements and bundled value-added services help retain users, and clear pricing plus loyalty benefits materially curb churn.

Customers pressure banks: CHF 1.1tn, SMEs 60% multibank

Customers wield moderate-to-high bargaining power: households stick (CHF 1.1tn deposits in 2024) but rate comparison raises elasticity; 60% of SMEs multi-bank relationships drive 10–15% loan/fee discounts; affluent clients pressure fees as global ETF assets >USD 10tn; institutions use procurement rules but cantonal backing limits churn.

| Metric | 2024 |

|---|---|

| Household deposits | CHF 1.1tn |

| SMEs multi-bank | ~60% |

| Loan/fee discounts | 10–15% |

| Global ETF assets | >USD 10tn |

| Neobank new accounts (EU) | ~18% |

Preview Before You Purchase

Basler Kantonalbank Porter's Five Forces Analysis

This preview shows the exact Basler Kantonalbank Porter’s Five Forces analysis you’ll receive—fully formatted and ready to use. It contains the complete competitive assessment, threat and supplier analyses, and strategic implications as presented in the finished file. No placeholders or samples: once you purchase, you’ll get instant access to this identical document.