Black Angus Steakhouse Porter's Five Forces Analysis

Don't Miss the Bigger Picture

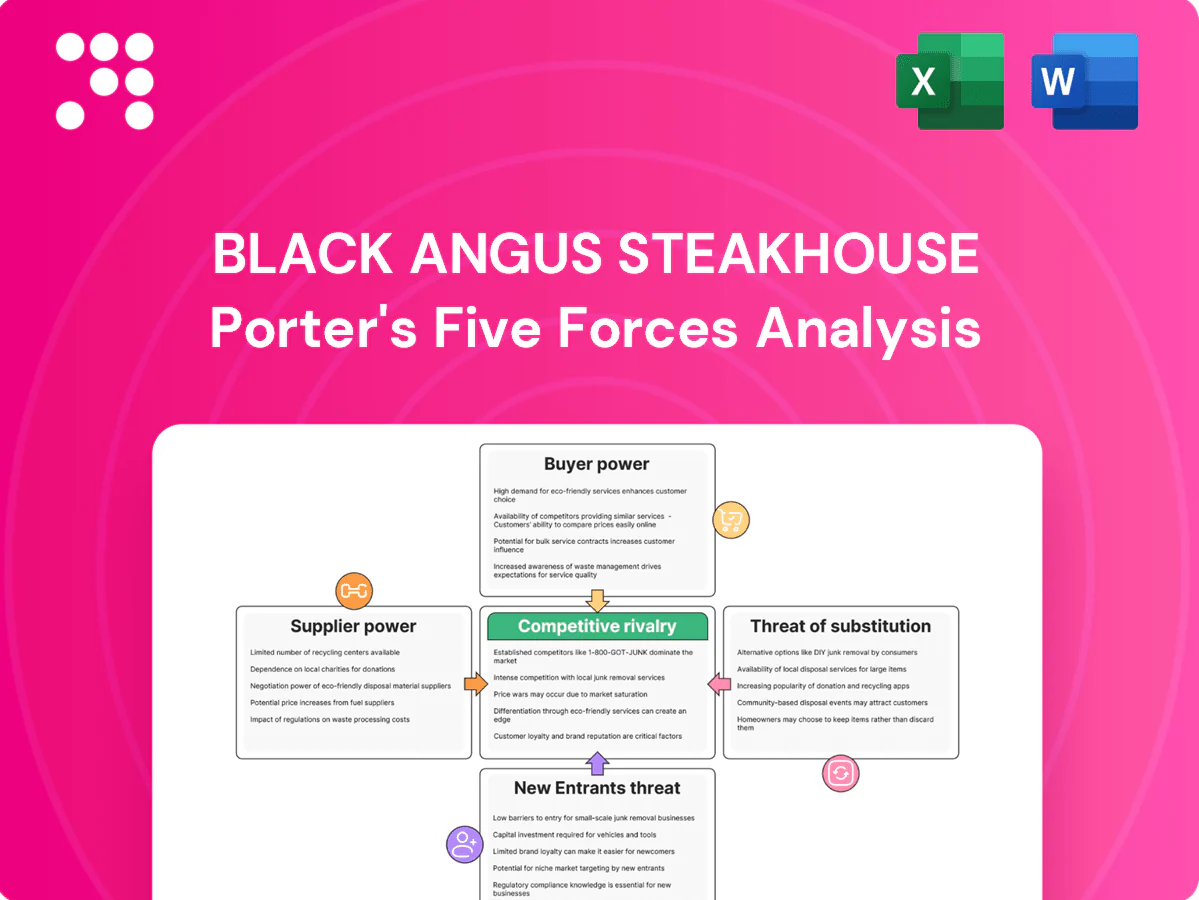

Black Angus Steakhouse faces moderate rivalry, supplier leverage on beef costs, shifting buyer preferences, potential local entrants, and growing substitute competition from fast-casual concepts; this snapshot highlights strategic pressure points. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable recommendations to inform investment or strategy decisions.

Suppliers Bargaining Power

Beef supplier concentration

The U.S. beef packing sector is highly concentrated: JBS, Tyson, Cargill and National Beef accounted for roughly 85% of steer and heifer slaughter capacity in 2024, concentrating upstream bargaining power. Black Angus depends on steady access to specific cuts, making it vulnerable to packer pricing and allocations. During tight supply cycles consolidation can compress restaurant margins. Multi-year or volume contracts can partially offset packer leverage.

Commodity price volatility

Beef, seafood and dairy costs are volatile—USDA reports 2024 fed cattle averaged about $170 per cwt, NOAA logged roughly 12% wholesale seafood price gains in 2024, and US milk prices climbed near $20 per cwt—driven by feed, weather, disease and trade shifts. Sudden spikes are difficult to pass to guests without reducing traffic, raising supplier leverage in up-cycles. Hedging and menu engineering can dampen but not remove this risk.

Quality and spec requirements

Black Angus positioning requires USDA Choice/Prime equivalents (Prime ~2% of carcasses, Choice ~50–55% in 2024) and consistent marbling, which tightens specs and narrows the vendor pool. Higher specs and traceability/animal welfare demands combined with an industry where the top four packers control ~80–85% of processing increase supplier leverage. Standardized specs, however, improve yield consistency and can cut waste and rejects at the restaurant level.

Regional distribution dependence

Operating primarily in the Western U.S. concentrates logistics with regional distributors, increasing exposure to carrier capacity constraints and fuel surcharges in 2024.

Weather events and port congestion in 2024 have intermittently disrupted seafood and other imported inputs, amplifying distributor leverage.

Dual-sourcing and DC bypass where feasible reduce risk by lowering single-distributor dependency.

- Regional concentration: higher distributor leverage

- Carrier capacity & fuel surcharges: elevated in 2024

- Weather/ports: intermittent seafood/import disruption

- Mitigation: dual-sourcing, DC bypass

Switching costs and alternatives

Swapping core protein suppliers requires testing, staff retraining and risks to guest perception, keeping supplier power elevated; US fed-beef processing is highly concentrated, with the top four packers handling about 85% of slaughter (USDA 2023), limiting alternatives. Non-core items (produce, pantry, beverages) are easier to switch, lowering supplier leverage. Private-label programs and multiple SKUs expand negotiating room; volume-based strategic partnerships can secure better pricing and terms.

- core-protein: high switching cost, limited alternatives (top4 ≈85%)

- non-core: low switching cost, lowers supplier power

- private-label/SKUs: increases leverage

- strategic partnerships: trade volume for better terms

Packers' 85% control and $170/cwt cattle reshape sourcing strategies

Top-four U.S. packers controlled ~85% slaughter capacity in 2024, concentrating upstream leverage. Fed-cattle averaged ~$170 per cwt in 2024 and Prime carcasses ≈2% (Choice ≈50–55%), driving cost volatility. Mitigants: multi-year volume contracts, dual-sourcing and private-label programs lower supplier risk.

| Metric | 2024 Value | Impact |

|---|---|---|

| Top4 packer share | ≈85% | High supplier power |

| Fed cattle price | $170 per cwt | Cost volatility |

| Prime/Choice | Prime ~2% / Choice 50–55% | Spec constraints |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Black Angus Steakhouse that uncovers competitive rivalry, buyer and supplier power, threat of substitutes, and entry barriers, highlighting disruptive trends and strategic risks to pricing and market share.

A clear, one-sheet Porter's Five Forces summary for Black Angus Steakhouse—perfect for quick decision-making and slide-ready presentations.

Customers Bargaining Power

Abundant dining choices

Guests choose among steak chains, casual dining, independents and fast-casual, and in 2024 the multi-billion-dollar U.S. dining market still features thousands of outlets, lowering switching costs and strengthening buyer power. High choice forces Black Angus to compete on value, taste and in-restaurant experience to protect visit frequency. Dense trade areas with numerous local competitors further amplify this pressure.

Price sensitivity and value cues

Middle-income diners at Black Angus are highly price-sensitive, reacting to price points, portion sizes and bundle deals when median household income was about 74,580 in 2023 (US Census). Inflation—CPI for all items ~3.4% in 2024 and food away from home up roughly 5.6% (BLS)—heightens deal-seeking and check management. Strong value menus and promotions boost traffic but compress industry margins; clear price-to-portion signaling reduces churn to cheaper options.

Digital reviews and visibility

Aggregators and social platforms amplify guest voice: BrightLocal 2024 reports 87% of consumers read online reviews for local businesses, and Harvard Business School (2017) found a one-star change on Yelp correlates with a 5–9% revenue swing. Ratings now rapidly affect traffic and pricing tolerance, while poor sentiment enables quick defection. Active reputation management and prompt responses can rebalance customer leverage.

Loyalty and switching costs

Restaurant loyalty is typically shallow for brands like Black Angus without rewards or distinctive offerings; the National Restaurant Association 2024 notes operators rank loyalty programs among top retention tools.

Effective loyalty programs and limited-time offers can modestly raise switching costs by increasing visit frequency and wallet share, while consistent service and signature items foster habitual behavior; absent those, buyers shift easily to rivals.

- Shallow base loyalty without rewards

- Loyalty programs/LTOs raise switching costs modestly

- Consistent service/signature items build habits

- Otherwise customers shift to competitors

Occasion-driven demand

Steak occasions such as celebrations and weekend dinners are highly planned and comparable across brands, with reservation platforms reporting about 60% of steakhouse bookings on weekends in 2024, driving guests to benchmark experience and perceived quality across competitors. Large parties (6+) routinely negotiate prix fixe menus and perks, and group demand extracts concessions in off-peak windows.

- Occasion-driven benchmarking raises quality expectations

- 60% weekend bookings (2024)

- Groups (6+) negotiate prix fixe/perks

- Off-peak concessions common for large parties

Buyers dominate: 87% check reviews; 60% steak bookings

Buyers have strong power: low switching costs across thousands of 2024 U.S. dining outlets, 60% of steak bookings occur on weekends, 87% consult online reviews, food-away-from-home inflation ~+5.6% (2024), and brand loyalty is shallow without rewards—loyalty programs and LTOs modestly raise switching costs.

| Metric | 2024 / source |

|---|---|

| Online review use | 87% (BrightLocal 2024) |

| Weekend steak bookings | 60% (2024) |

| Food away from home CPI | +5.6% (BLS 2024) |

| Median HH income | $74,580 (2023, US Census) |

What You See Is What You Get

Black Angus Steakhouse Porter's Five Forces Analysis

This preview shows the exact Black Angus Steakhouse Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The report is fully formatted and ready for download the moment you buy, covering threat of new entrants, buyer power, supplier power, substitutes, and competitive rivalry. You're viewing the final deliverable ready for immediate use.

Don't Miss the Bigger Picture

Black Angus Steakhouse faces moderate rivalry, supplier leverage on beef costs, shifting buyer preferences, potential local entrants, and growing substitute competition from fast-casual concepts; this snapshot highlights strategic pressure points. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable recommendations to inform investment or strategy decisions.

Suppliers Bargaining Power

Beef supplier concentration

The U.S. beef packing sector is highly concentrated: JBS, Tyson, Cargill and National Beef accounted for roughly 85% of steer and heifer slaughter capacity in 2024, concentrating upstream bargaining power. Black Angus depends on steady access to specific cuts, making it vulnerable to packer pricing and allocations. During tight supply cycles consolidation can compress restaurant margins. Multi-year or volume contracts can partially offset packer leverage.

Commodity price volatility

Beef, seafood and dairy costs are volatile—USDA reports 2024 fed cattle averaged about $170 per cwt, NOAA logged roughly 12% wholesale seafood price gains in 2024, and US milk prices climbed near $20 per cwt—driven by feed, weather, disease and trade shifts. Sudden spikes are difficult to pass to guests without reducing traffic, raising supplier leverage in up-cycles. Hedging and menu engineering can dampen but not remove this risk.

Quality and spec requirements

Black Angus positioning requires USDA Choice/Prime equivalents (Prime ~2% of carcasses, Choice ~50–55% in 2024) and consistent marbling, which tightens specs and narrows the vendor pool. Higher specs and traceability/animal welfare demands combined with an industry where the top four packers control ~80–85% of processing increase supplier leverage. Standardized specs, however, improve yield consistency and can cut waste and rejects at the restaurant level.

Regional distribution dependence

Operating primarily in the Western U.S. concentrates logistics with regional distributors, increasing exposure to carrier capacity constraints and fuel surcharges in 2024.

Weather events and port congestion in 2024 have intermittently disrupted seafood and other imported inputs, amplifying distributor leverage.

Dual-sourcing and DC bypass where feasible reduce risk by lowering single-distributor dependency.

- Regional concentration: higher distributor leverage

- Carrier capacity & fuel surcharges: elevated in 2024

- Weather/ports: intermittent seafood/import disruption

- Mitigation: dual-sourcing, DC bypass

Switching costs and alternatives

Swapping core protein suppliers requires testing, staff retraining and risks to guest perception, keeping supplier power elevated; US fed-beef processing is highly concentrated, with the top four packers handling about 85% of slaughter (USDA 2023), limiting alternatives. Non-core items (produce, pantry, beverages) are easier to switch, lowering supplier leverage. Private-label programs and multiple SKUs expand negotiating room; volume-based strategic partnerships can secure better pricing and terms.

- core-protein: high switching cost, limited alternatives (top4 ≈85%)

- non-core: low switching cost, lowers supplier power

- private-label/SKUs: increases leverage

- strategic partnerships: trade volume for better terms

Packers' 85% control and $170/cwt cattle reshape sourcing strategies

Top-four U.S. packers controlled ~85% slaughter capacity in 2024, concentrating upstream leverage. Fed-cattle averaged ~$170 per cwt in 2024 and Prime carcasses ≈2% (Choice ≈50–55%), driving cost volatility. Mitigants: multi-year volume contracts, dual-sourcing and private-label programs lower supplier risk.

| Metric | 2024 Value | Impact |

|---|---|---|

| Top4 packer share | ≈85% | High supplier power |

| Fed cattle price | $170 per cwt | Cost volatility |

| Prime/Choice | Prime ~2% / Choice 50–55% | Spec constraints |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Black Angus Steakhouse that uncovers competitive rivalry, buyer and supplier power, threat of substitutes, and entry barriers, highlighting disruptive trends and strategic risks to pricing and market share.

A clear, one-sheet Porter's Five Forces summary for Black Angus Steakhouse—perfect for quick decision-making and slide-ready presentations.

Customers Bargaining Power

Abundant dining choices

Guests choose among steak chains, casual dining, independents and fast-casual, and in 2024 the multi-billion-dollar U.S. dining market still features thousands of outlets, lowering switching costs and strengthening buyer power. High choice forces Black Angus to compete on value, taste and in-restaurant experience to protect visit frequency. Dense trade areas with numerous local competitors further amplify this pressure.

Price sensitivity and value cues

Middle-income diners at Black Angus are highly price-sensitive, reacting to price points, portion sizes and bundle deals when median household income was about 74,580 in 2023 (US Census). Inflation—CPI for all items ~3.4% in 2024 and food away from home up roughly 5.6% (BLS)—heightens deal-seeking and check management. Strong value menus and promotions boost traffic but compress industry margins; clear price-to-portion signaling reduces churn to cheaper options.

Digital reviews and visibility

Aggregators and social platforms amplify guest voice: BrightLocal 2024 reports 87% of consumers read online reviews for local businesses, and Harvard Business School (2017) found a one-star change on Yelp correlates with a 5–9% revenue swing. Ratings now rapidly affect traffic and pricing tolerance, while poor sentiment enables quick defection. Active reputation management and prompt responses can rebalance customer leverage.

Loyalty and switching costs

Restaurant loyalty is typically shallow for brands like Black Angus without rewards or distinctive offerings; the National Restaurant Association 2024 notes operators rank loyalty programs among top retention tools.

Effective loyalty programs and limited-time offers can modestly raise switching costs by increasing visit frequency and wallet share, while consistent service and signature items foster habitual behavior; absent those, buyers shift easily to rivals.

- Shallow base loyalty without rewards

- Loyalty programs/LTOs raise switching costs modestly

- Consistent service/signature items build habits

- Otherwise customers shift to competitors

Occasion-driven demand

Steak occasions such as celebrations and weekend dinners are highly planned and comparable across brands, with reservation platforms reporting about 60% of steakhouse bookings on weekends in 2024, driving guests to benchmark experience and perceived quality across competitors. Large parties (6+) routinely negotiate prix fixe menus and perks, and group demand extracts concessions in off-peak windows.

- Occasion-driven benchmarking raises quality expectations

- 60% weekend bookings (2024)

- Groups (6+) negotiate prix fixe/perks

- Off-peak concessions common for large parties

Buyers dominate: 87% check reviews; 60% steak bookings

Buyers have strong power: low switching costs across thousands of 2024 U.S. dining outlets, 60% of steak bookings occur on weekends, 87% consult online reviews, food-away-from-home inflation ~+5.6% (2024), and brand loyalty is shallow without rewards—loyalty programs and LTOs modestly raise switching costs.

| Metric | 2024 / source |

|---|---|

| Online review use | 87% (BrightLocal 2024) |

| Weekend steak bookings | 60% (2024) |

| Food away from home CPI | +5.6% (BLS 2024) |

| Median HH income | $74,580 (2023, US Census) |

What You See Is What You Get

Black Angus Steakhouse Porter's Five Forces Analysis

This preview shows the exact Black Angus Steakhouse Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The report is fully formatted and ready for download the moment you buy, covering threat of new entrants, buyer power, supplier power, substitutes, and competitive rivalry. You're viewing the final deliverable ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Black Angus Steakhouse faces moderate rivalry, supplier leverage on beef costs, shifting buyer preferences, potential local entrants, and growing substitute competition from fast-casual concepts; this snapshot highlights strategic pressure points. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable recommendations to inform investment or strategy decisions.

Suppliers Bargaining Power

Beef supplier concentration

The U.S. beef packing sector is highly concentrated: JBS, Tyson, Cargill and National Beef accounted for roughly 85% of steer and heifer slaughter capacity in 2024, concentrating upstream bargaining power. Black Angus depends on steady access to specific cuts, making it vulnerable to packer pricing and allocations. During tight supply cycles consolidation can compress restaurant margins. Multi-year or volume contracts can partially offset packer leverage.

Commodity price volatility

Beef, seafood and dairy costs are volatile—USDA reports 2024 fed cattle averaged about $170 per cwt, NOAA logged roughly 12% wholesale seafood price gains in 2024, and US milk prices climbed near $20 per cwt—driven by feed, weather, disease and trade shifts. Sudden spikes are difficult to pass to guests without reducing traffic, raising supplier leverage in up-cycles. Hedging and menu engineering can dampen but not remove this risk.

Quality and spec requirements

Black Angus positioning requires USDA Choice/Prime equivalents (Prime ~2% of carcasses, Choice ~50–55% in 2024) and consistent marbling, which tightens specs and narrows the vendor pool. Higher specs and traceability/animal welfare demands combined with an industry where the top four packers control ~80–85% of processing increase supplier leverage. Standardized specs, however, improve yield consistency and can cut waste and rejects at the restaurant level.

Regional distribution dependence

Operating primarily in the Western U.S. concentrates logistics with regional distributors, increasing exposure to carrier capacity constraints and fuel surcharges in 2024.

Weather events and port congestion in 2024 have intermittently disrupted seafood and other imported inputs, amplifying distributor leverage.

Dual-sourcing and DC bypass where feasible reduce risk by lowering single-distributor dependency.

- Regional concentration: higher distributor leverage

- Carrier capacity & fuel surcharges: elevated in 2024

- Weather/ports: intermittent seafood/import disruption

- Mitigation: dual-sourcing, DC bypass

Switching costs and alternatives

Swapping core protein suppliers requires testing, staff retraining and risks to guest perception, keeping supplier power elevated; US fed-beef processing is highly concentrated, with the top four packers handling about 85% of slaughter (USDA 2023), limiting alternatives. Non-core items (produce, pantry, beverages) are easier to switch, lowering supplier leverage. Private-label programs and multiple SKUs expand negotiating room; volume-based strategic partnerships can secure better pricing and terms.

- core-protein: high switching cost, limited alternatives (top4 ≈85%)

- non-core: low switching cost, lowers supplier power

- private-label/SKUs: increases leverage

- strategic partnerships: trade volume for better terms

Packers' 85% control and $170/cwt cattle reshape sourcing strategies

Top-four U.S. packers controlled ~85% slaughter capacity in 2024, concentrating upstream leverage. Fed-cattle averaged ~$170 per cwt in 2024 and Prime carcasses ≈2% (Choice ≈50–55%), driving cost volatility. Mitigants: multi-year volume contracts, dual-sourcing and private-label programs lower supplier risk.

| Metric | 2024 Value | Impact |

|---|---|---|

| Top4 packer share | ≈85% | High supplier power |

| Fed cattle price | $170 per cwt | Cost volatility |

| Prime/Choice | Prime ~2% / Choice 50–55% | Spec constraints |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Black Angus Steakhouse that uncovers competitive rivalry, buyer and supplier power, threat of substitutes, and entry barriers, highlighting disruptive trends and strategic risks to pricing and market share.

A clear, one-sheet Porter's Five Forces summary for Black Angus Steakhouse—perfect for quick decision-making and slide-ready presentations.

Customers Bargaining Power

Abundant dining choices

Guests choose among steak chains, casual dining, independents and fast-casual, and in 2024 the multi-billion-dollar U.S. dining market still features thousands of outlets, lowering switching costs and strengthening buyer power. High choice forces Black Angus to compete on value, taste and in-restaurant experience to protect visit frequency. Dense trade areas with numerous local competitors further amplify this pressure.

Price sensitivity and value cues

Middle-income diners at Black Angus are highly price-sensitive, reacting to price points, portion sizes and bundle deals when median household income was about 74,580 in 2023 (US Census). Inflation—CPI for all items ~3.4% in 2024 and food away from home up roughly 5.6% (BLS)—heightens deal-seeking and check management. Strong value menus and promotions boost traffic but compress industry margins; clear price-to-portion signaling reduces churn to cheaper options.

Digital reviews and visibility

Aggregators and social platforms amplify guest voice: BrightLocal 2024 reports 87% of consumers read online reviews for local businesses, and Harvard Business School (2017) found a one-star change on Yelp correlates with a 5–9% revenue swing. Ratings now rapidly affect traffic and pricing tolerance, while poor sentiment enables quick defection. Active reputation management and prompt responses can rebalance customer leverage.

Loyalty and switching costs

Restaurant loyalty is typically shallow for brands like Black Angus without rewards or distinctive offerings; the National Restaurant Association 2024 notes operators rank loyalty programs among top retention tools.

Effective loyalty programs and limited-time offers can modestly raise switching costs by increasing visit frequency and wallet share, while consistent service and signature items foster habitual behavior; absent those, buyers shift easily to rivals.

- Shallow base loyalty without rewards

- Loyalty programs/LTOs raise switching costs modestly

- Consistent service/signature items build habits

- Otherwise customers shift to competitors

Occasion-driven demand

Steak occasions such as celebrations and weekend dinners are highly planned and comparable across brands, with reservation platforms reporting about 60% of steakhouse bookings on weekends in 2024, driving guests to benchmark experience and perceived quality across competitors. Large parties (6+) routinely negotiate prix fixe menus and perks, and group demand extracts concessions in off-peak windows.

- Occasion-driven benchmarking raises quality expectations

- 60% weekend bookings (2024)

- Groups (6+) negotiate prix fixe/perks

- Off-peak concessions common for large parties

Buyers dominate: 87% check reviews; 60% steak bookings

Buyers have strong power: low switching costs across thousands of 2024 U.S. dining outlets, 60% of steak bookings occur on weekends, 87% consult online reviews, food-away-from-home inflation ~+5.6% (2024), and brand loyalty is shallow without rewards—loyalty programs and LTOs modestly raise switching costs.

| Metric | 2024 / source |

|---|---|

| Online review use | 87% (BrightLocal 2024) |

| Weekend steak bookings | 60% (2024) |

| Food away from home CPI | +5.6% (BLS 2024) |

| Median HH income | $74,580 (2023, US Census) |

What You See Is What You Get

Black Angus Steakhouse Porter's Five Forces Analysis

This preview shows the exact Black Angus Steakhouse Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The report is fully formatted and ready for download the moment you buy, covering threat of new entrants, buyer power, supplier power, substitutes, and competitive rivalry. You're viewing the final deliverable ready for immediate use.