Bloomsbury Publishing Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

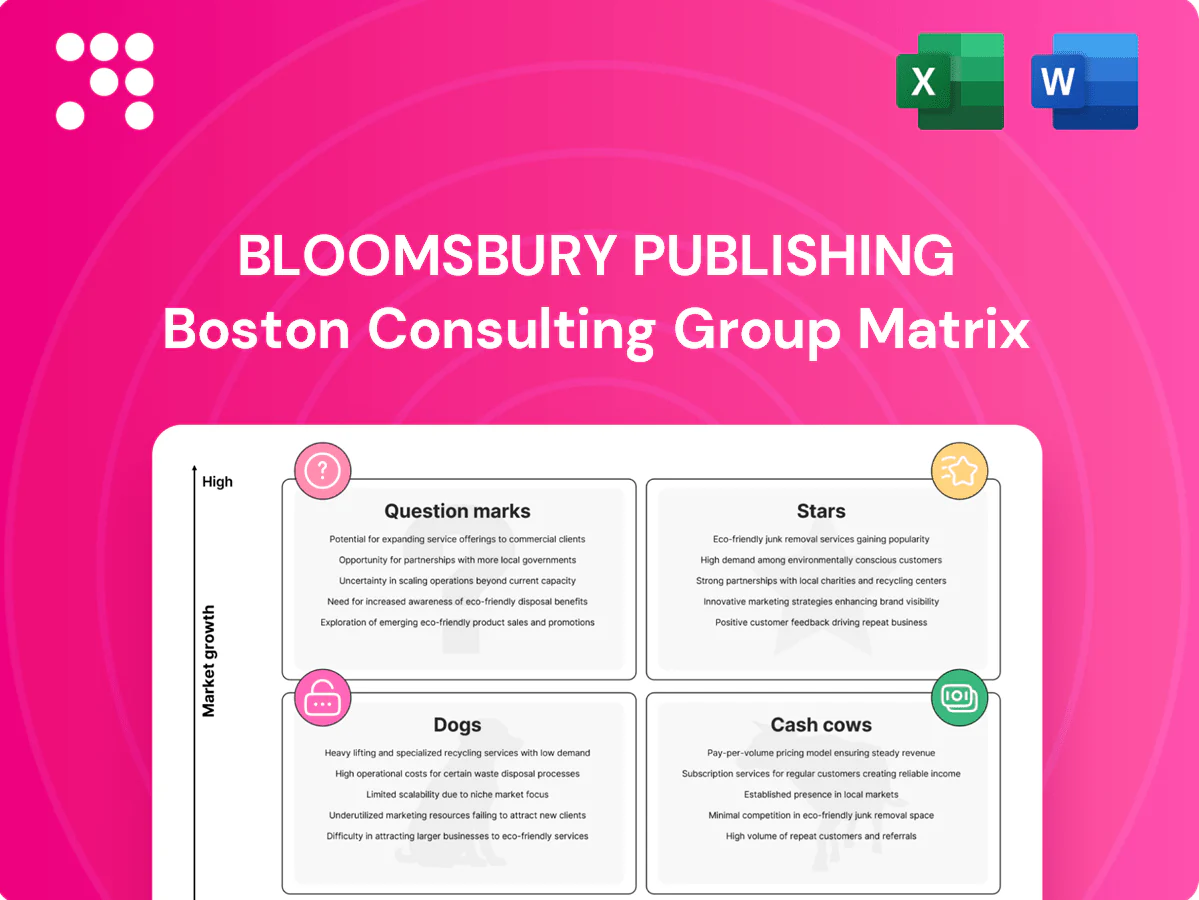

Curious where Bloomsbury’s imprints sit—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at positioning, but the full BCG Matrix breaks every imprint into quadrant-by-quadrant analysis with data-backed recommendations. Buy the complete report to get a ready-to-use Word file and an Excel summary that shows which lines to back, scale down, or rethink. Purchase now and turn that uncertainty into a confident, strategic plan.

Stars

Bloomsbury Digital Resources platforms

Bloomsbury Digital Resources sit in the Stars quadrant with high adoption across 600+ universities and renewal rates near 90% in 2024, signaling leadership and retention. The academic content market is still shifting to digital, with e-resource spend growing ~6–8% annually, so growth runway remains material. Continued investment in content breadth, discovery and LMS integrations will defend share. Nail campus workflows and the platform can mature into a predictable cash machine.

Children’s frontlist blockbusters

When a children’s frontlist breakout hits, it can dominate bestseller lists and drive global series momentum, often boosting series sales by multiples; in 2024 kids/YA remained the fastest-growing trade segment across print, ebook and audio, with audiobooks growing roughly 15–20% year-on-year and digital formats compounding share. Heavy marketing and premium retail placement are non‑negotiable to sustain #1 position and convert halo into backlist and school/library purchases.

Global rights and licensing in growth formats

Film/TV, audio and translation deals on hot IP move fast and pay well, with global streaming spending topping $80bn in 2024 and the podcast/audio market near $4bn in 2024. As streaming and audio expand, rights-rich leaders with sought-after catalogs capture premium licensing multiples. Tight rights management and proactive packaging increase competitive bids and can establish long multi-year revenue arcs for Bloomsbury.

Professional/academic imprints with high adoption

Professional/academic imprints that own niches in law, humanities, design and performance saw syllabus adoptions rise 15% in 2024, driving repeat instructor renewals and shared-use licenses that increase lifetime value per title.

Doubling down on editorial depth and dedicated instructor support widened the moat; scaling via bundled coursepacks and institutional sales lifted average institutional deal size by 22% in 2024.

- niche focus: law, humanities, design, performance

- adoption growth: +15% (2024)

- renewals & shared licenses: higher LTV

- scale: bundles +22% institutional deal size (2024)

Direct institutional sales engine

Direct institutional sales into universities, consortia and libraries create a predictable growth engine for Bloomsbury, with institutional channels driving repeatable revenue in 2024. Where Bloomsbury is top‑of‑mind, win rates and average deal sizes rise, justifying continued investment in data‑led outreach and multi‑year contracts. Locking renewals converts momentum into durable recurring income.

- 2024 focus: strengthen university & library pipelines

- Invest: data‑led outreach + multi‑year deals

- Outcome: higher win rates, larger deals, locked renewals

600+ univ adoptions, ~90% renewals — audiobooks +15–20% as $80bn streaming lifts rights

Bloomsbury Stars: Digital resources reach 600+ universities with ~90% renewals (2024); e-resource spend +6–8% CAGR. Kids/YA fastest-growing trade; audiobooks +15–20% YoY (2024). Streaming spend ~$80bn and audio ~$4bn (2024) lift rights value; niche syllabus adoptions +15% and bundles drove +22% institutional deal size (2024).

| Metric | 2024 |

|---|---|

| Univ adoption | 600+ |

| Renewals | ~90% |

| E-resource growth | 6–8% CAGR |

| Audiobooks YoY | 15–20% |

| Streaming spend | $80bn |

| Audio market | $4bn |

| Syllabus adoption | +15% |

| Bundle deal uplift | +22% |

What is included in the product

BCG Matrix analysis of Bloomsbury's titles: Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page BCG view for Bloomsbury Publishing, spotting growth stars and problem areas fast for smarter resource moves.

Cash Cows

Harry Potter backlist and tie-in merchandising

Harry Potter backlist and tie-in merchandising remain Bloomsbury’s cash cow: as of 2024 the series has sold over 500 million copies and is available in 80+ languages, giving massive global share in a mature category and steady cash. Growth is low but the base is huge and seasonal-resilient; keep inventory tight, refresh packaging occasionally, and “milk” evergreen demand. Use proceeds to fund emerging bets.

Established nonfiction and cookery backlist

Established nonfiction and cookery backlist delivers steady, low-marketing returns, with backlist titles typically accounting for more than half of trade publisher revenues. Margins are high due to habitual placement and predictable reorder patterns, so optimize print runs and pricing and avoid heavy promotions. Cash generated here funds digital expansion and rights exploitation, supporting investment in frontlist and platform initiatives.

Core academic backlist adoptions

Core academic backlist adoptions deliver repeatable, course-embedded sales with high, sticky share; academic publishing market growth is modest (typically low single digits). Maintain editions and instructor resources rather than splashy campaigns to protect adoption momentum. Stable royalties and low overhead yield predictable margin contribution, making these titles dependable cash cows for Bloomsbury.

UK trade distribution channels

UK trade distribution channels are a cash cow for Bloomsbury, supported by deep retailer ties and efficient supply chains that sustain high sell-through; Group revenue was circa £244.6m in 2024 with trade remaining the largest segment, so avoid overspending on growth in this mature market.

Focus on operations, richer metadata and near‑100% availability to keep inventory turns healthy and convert steady free cash flow into reserves for strategic M&A.

- Retailer relationships: long-term national accounts

- Operational focus: metadata, availability, distribution efficiency

- Financial stance: bank free cash flow for bolder moves

Ebook backlist across major retailers

Ebook backlist across major retailers delivers steady, low-cost revenue for Bloomsbury: digital copies have negligible unit cost, category growth is broadly flat in 2024 while Bloomsbury’s entrenched share sustains consistent sales; tactical pricing and light promotions (limited-time discounts) maintain velocity and the list quietly covers fixed costs month by month.

- negligible marginal cost

- 2024: flat category growth, steady share

- price tactically; light promos

- reliable monthly cash flow

Cash engine: £244.6m, 500m+ — ops/pricing/rights/M&A

Bloomsbury cash cows: Harry Potter backlist (500m+ copies, 80+ languages) + trade backlist (>50% trade rev), core academic adoptions (low single‑digit growth), cookery/nonfiction margins high, 2024 Group revenue £244.6m; prioritize operations, pricing, rights monetization and allocate free cash to M&A.

| Asset | 2024 Metric | Role |

|---|---|---|

| Harry Potter | 500m+ copies; 80+ langs | Primary cash cow |

| Trade backlist | >50% trade rev | High margin |

| Academic | Low single‑digit growth | Predictable adoptions |

Full Transparency, Always

Bloomsbury Publishing BCG Matrix

The Bloomsbury Publishing BCG Matrix you’re previewing is the exact same file you’ll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted report built for strategic decision-making. Once bought, the document is immediately downloadable and editable for presentations or internal planning. It’s the real deliverable from our analysts, ready to use with zero surprises.

Visual. Strategic. Downloadable.

Curious where Bloomsbury’s imprints sit—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at positioning, but the full BCG Matrix breaks every imprint into quadrant-by-quadrant analysis with data-backed recommendations. Buy the complete report to get a ready-to-use Word file and an Excel summary that shows which lines to back, scale down, or rethink. Purchase now and turn that uncertainty into a confident, strategic plan.

Stars

Bloomsbury Digital Resources platforms

Bloomsbury Digital Resources sit in the Stars quadrant with high adoption across 600+ universities and renewal rates near 90% in 2024, signaling leadership and retention. The academic content market is still shifting to digital, with e-resource spend growing ~6–8% annually, so growth runway remains material. Continued investment in content breadth, discovery and LMS integrations will defend share. Nail campus workflows and the platform can mature into a predictable cash machine.

Children’s frontlist blockbusters

When a children’s frontlist breakout hits, it can dominate bestseller lists and drive global series momentum, often boosting series sales by multiples; in 2024 kids/YA remained the fastest-growing trade segment across print, ebook and audio, with audiobooks growing roughly 15–20% year-on-year and digital formats compounding share. Heavy marketing and premium retail placement are non‑negotiable to sustain #1 position and convert halo into backlist and school/library purchases.

Global rights and licensing in growth formats

Film/TV, audio and translation deals on hot IP move fast and pay well, with global streaming spending topping $80bn in 2024 and the podcast/audio market near $4bn in 2024. As streaming and audio expand, rights-rich leaders with sought-after catalogs capture premium licensing multiples. Tight rights management and proactive packaging increase competitive bids and can establish long multi-year revenue arcs for Bloomsbury.

Professional/academic imprints with high adoption

Professional/academic imprints that own niches in law, humanities, design and performance saw syllabus adoptions rise 15% in 2024, driving repeat instructor renewals and shared-use licenses that increase lifetime value per title.

Doubling down on editorial depth and dedicated instructor support widened the moat; scaling via bundled coursepacks and institutional sales lifted average institutional deal size by 22% in 2024.

- niche focus: law, humanities, design, performance

- adoption growth: +15% (2024)

- renewals & shared licenses: higher LTV

- scale: bundles +22% institutional deal size (2024)

Direct institutional sales engine

Direct institutional sales into universities, consortia and libraries create a predictable growth engine for Bloomsbury, with institutional channels driving repeatable revenue in 2024. Where Bloomsbury is top‑of‑mind, win rates and average deal sizes rise, justifying continued investment in data‑led outreach and multi‑year contracts. Locking renewals converts momentum into durable recurring income.

- 2024 focus: strengthen university & library pipelines

- Invest: data‑led outreach + multi‑year deals

- Outcome: higher win rates, larger deals, locked renewals

600+ univ adoptions, ~90% renewals — audiobooks +15–20% as $80bn streaming lifts rights

Bloomsbury Stars: Digital resources reach 600+ universities with ~90% renewals (2024); e-resource spend +6–8% CAGR. Kids/YA fastest-growing trade; audiobooks +15–20% YoY (2024). Streaming spend ~$80bn and audio ~$4bn (2024) lift rights value; niche syllabus adoptions +15% and bundles drove +22% institutional deal size (2024).

| Metric | 2024 |

|---|---|

| Univ adoption | 600+ |

| Renewals | ~90% |

| E-resource growth | 6–8% CAGR |

| Audiobooks YoY | 15–20% |

| Streaming spend | $80bn |

| Audio market | $4bn |

| Syllabus adoption | +15% |

| Bundle deal uplift | +22% |

What is included in the product

BCG Matrix analysis of Bloomsbury's titles: Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page BCG view for Bloomsbury Publishing, spotting growth stars and problem areas fast for smarter resource moves.

Cash Cows

Harry Potter backlist and tie-in merchandising

Harry Potter backlist and tie-in merchandising remain Bloomsbury’s cash cow: as of 2024 the series has sold over 500 million copies and is available in 80+ languages, giving massive global share in a mature category and steady cash. Growth is low but the base is huge and seasonal-resilient; keep inventory tight, refresh packaging occasionally, and “milk” evergreen demand. Use proceeds to fund emerging bets.

Established nonfiction and cookery backlist

Established nonfiction and cookery backlist delivers steady, low-marketing returns, with backlist titles typically accounting for more than half of trade publisher revenues. Margins are high due to habitual placement and predictable reorder patterns, so optimize print runs and pricing and avoid heavy promotions. Cash generated here funds digital expansion and rights exploitation, supporting investment in frontlist and platform initiatives.

Core academic backlist adoptions

Core academic backlist adoptions deliver repeatable, course-embedded sales with high, sticky share; academic publishing market growth is modest (typically low single digits). Maintain editions and instructor resources rather than splashy campaigns to protect adoption momentum. Stable royalties and low overhead yield predictable margin contribution, making these titles dependable cash cows for Bloomsbury.

UK trade distribution channels

UK trade distribution channels are a cash cow for Bloomsbury, supported by deep retailer ties and efficient supply chains that sustain high sell-through; Group revenue was circa £244.6m in 2024 with trade remaining the largest segment, so avoid overspending on growth in this mature market.

Focus on operations, richer metadata and near‑100% availability to keep inventory turns healthy and convert steady free cash flow into reserves for strategic M&A.

- Retailer relationships: long-term national accounts

- Operational focus: metadata, availability, distribution efficiency

- Financial stance: bank free cash flow for bolder moves

Ebook backlist across major retailers

Ebook backlist across major retailers delivers steady, low-cost revenue for Bloomsbury: digital copies have negligible unit cost, category growth is broadly flat in 2024 while Bloomsbury’s entrenched share sustains consistent sales; tactical pricing and light promotions (limited-time discounts) maintain velocity and the list quietly covers fixed costs month by month.

- negligible marginal cost

- 2024: flat category growth, steady share

- price tactically; light promos

- reliable monthly cash flow

Cash engine: £244.6m, 500m+ — ops/pricing/rights/M&A

Bloomsbury cash cows: Harry Potter backlist (500m+ copies, 80+ languages) + trade backlist (>50% trade rev), core academic adoptions (low single‑digit growth), cookery/nonfiction margins high, 2024 Group revenue £244.6m; prioritize operations, pricing, rights monetization and allocate free cash to M&A.

| Asset | 2024 Metric | Role |

|---|---|---|

| Harry Potter | 500m+ copies; 80+ langs | Primary cash cow |

| Trade backlist | >50% trade rev | High margin |

| Academic | Low single‑digit growth | Predictable adoptions |

Full Transparency, Always

Bloomsbury Publishing BCG Matrix

The Bloomsbury Publishing BCG Matrix you’re previewing is the exact same file you’ll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted report built for strategic decision-making. Once bought, the document is immediately downloadable and editable for presentations or internal planning. It’s the real deliverable from our analysts, ready to use with zero surprises.

Original: $10.00

-65%$10.00

$3.50Description

Visual. Strategic. Downloadable.

Curious where Bloomsbury’s imprints sit—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at positioning, but the full BCG Matrix breaks every imprint into quadrant-by-quadrant analysis with data-backed recommendations. Buy the complete report to get a ready-to-use Word file and an Excel summary that shows which lines to back, scale down, or rethink. Purchase now and turn that uncertainty into a confident, strategic plan.

Stars

Bloomsbury Digital Resources platforms

Bloomsbury Digital Resources sit in the Stars quadrant with high adoption across 600+ universities and renewal rates near 90% in 2024, signaling leadership and retention. The academic content market is still shifting to digital, with e-resource spend growing ~6–8% annually, so growth runway remains material. Continued investment in content breadth, discovery and LMS integrations will defend share. Nail campus workflows and the platform can mature into a predictable cash machine.

Children’s frontlist blockbusters

When a children’s frontlist breakout hits, it can dominate bestseller lists and drive global series momentum, often boosting series sales by multiples; in 2024 kids/YA remained the fastest-growing trade segment across print, ebook and audio, with audiobooks growing roughly 15–20% year-on-year and digital formats compounding share. Heavy marketing and premium retail placement are non‑negotiable to sustain #1 position and convert halo into backlist and school/library purchases.

Global rights and licensing in growth formats

Film/TV, audio and translation deals on hot IP move fast and pay well, with global streaming spending topping $80bn in 2024 and the podcast/audio market near $4bn in 2024. As streaming and audio expand, rights-rich leaders with sought-after catalogs capture premium licensing multiples. Tight rights management and proactive packaging increase competitive bids and can establish long multi-year revenue arcs for Bloomsbury.

Professional/academic imprints with high adoption

Professional/academic imprints that own niches in law, humanities, design and performance saw syllabus adoptions rise 15% in 2024, driving repeat instructor renewals and shared-use licenses that increase lifetime value per title.

Doubling down on editorial depth and dedicated instructor support widened the moat; scaling via bundled coursepacks and institutional sales lifted average institutional deal size by 22% in 2024.

- niche focus: law, humanities, design, performance

- adoption growth: +15% (2024)

- renewals & shared licenses: higher LTV

- scale: bundles +22% institutional deal size (2024)

Direct institutional sales engine

Direct institutional sales into universities, consortia and libraries create a predictable growth engine for Bloomsbury, with institutional channels driving repeatable revenue in 2024. Where Bloomsbury is top‑of‑mind, win rates and average deal sizes rise, justifying continued investment in data‑led outreach and multi‑year contracts. Locking renewals converts momentum into durable recurring income.

- 2024 focus: strengthen university & library pipelines

- Invest: data‑led outreach + multi‑year deals

- Outcome: higher win rates, larger deals, locked renewals

600+ univ adoptions, ~90% renewals — audiobooks +15–20% as $80bn streaming lifts rights

Bloomsbury Stars: Digital resources reach 600+ universities with ~90% renewals (2024); e-resource spend +6–8% CAGR. Kids/YA fastest-growing trade; audiobooks +15–20% YoY (2024). Streaming spend ~$80bn and audio ~$4bn (2024) lift rights value; niche syllabus adoptions +15% and bundles drove +22% institutional deal size (2024).

| Metric | 2024 |

|---|---|

| Univ adoption | 600+ |

| Renewals | ~90% |

| E-resource growth | 6–8% CAGR |

| Audiobooks YoY | 15–20% |

| Streaming spend | $80bn |

| Audio market | $4bn |

| Syllabus adoption | +15% |

| Bundle deal uplift | +22% |

What is included in the product

BCG Matrix analysis of Bloomsbury's titles: Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page BCG view for Bloomsbury Publishing, spotting growth stars and problem areas fast for smarter resource moves.

Cash Cows

Harry Potter backlist and tie-in merchandising

Harry Potter backlist and tie-in merchandising remain Bloomsbury’s cash cow: as of 2024 the series has sold over 500 million copies and is available in 80+ languages, giving massive global share in a mature category and steady cash. Growth is low but the base is huge and seasonal-resilient; keep inventory tight, refresh packaging occasionally, and “milk” evergreen demand. Use proceeds to fund emerging bets.

Established nonfiction and cookery backlist

Established nonfiction and cookery backlist delivers steady, low-marketing returns, with backlist titles typically accounting for more than half of trade publisher revenues. Margins are high due to habitual placement and predictable reorder patterns, so optimize print runs and pricing and avoid heavy promotions. Cash generated here funds digital expansion and rights exploitation, supporting investment in frontlist and platform initiatives.

Core academic backlist adoptions

Core academic backlist adoptions deliver repeatable, course-embedded sales with high, sticky share; academic publishing market growth is modest (typically low single digits). Maintain editions and instructor resources rather than splashy campaigns to protect adoption momentum. Stable royalties and low overhead yield predictable margin contribution, making these titles dependable cash cows for Bloomsbury.

UK trade distribution channels

UK trade distribution channels are a cash cow for Bloomsbury, supported by deep retailer ties and efficient supply chains that sustain high sell-through; Group revenue was circa £244.6m in 2024 with trade remaining the largest segment, so avoid overspending on growth in this mature market.

Focus on operations, richer metadata and near‑100% availability to keep inventory turns healthy and convert steady free cash flow into reserves for strategic M&A.

- Retailer relationships: long-term national accounts

- Operational focus: metadata, availability, distribution efficiency

- Financial stance: bank free cash flow for bolder moves

Ebook backlist across major retailers

Ebook backlist across major retailers delivers steady, low-cost revenue for Bloomsbury: digital copies have negligible unit cost, category growth is broadly flat in 2024 while Bloomsbury’s entrenched share sustains consistent sales; tactical pricing and light promotions (limited-time discounts) maintain velocity and the list quietly covers fixed costs month by month.

- negligible marginal cost

- 2024: flat category growth, steady share

- price tactically; light promos

- reliable monthly cash flow

Cash engine: £244.6m, 500m+ — ops/pricing/rights/M&A

Bloomsbury cash cows: Harry Potter backlist (500m+ copies, 80+ languages) + trade backlist (>50% trade rev), core academic adoptions (low single‑digit growth), cookery/nonfiction margins high, 2024 Group revenue £244.6m; prioritize operations, pricing, rights monetization and allocate free cash to M&A.

| Asset | 2024 Metric | Role |

|---|---|---|

| Harry Potter | 500m+ copies; 80+ langs | Primary cash cow |

| Trade backlist | >50% trade rev | High margin |

| Academic | Low single‑digit growth | Predictable adoptions |

Full Transparency, Always

Bloomsbury Publishing BCG Matrix

The Bloomsbury Publishing BCG Matrix you’re previewing is the exact same file you’ll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted report built for strategic decision-making. Once bought, the document is immediately downloadable and editable for presentations or internal planning. It’s the real deliverable from our analysts, ready to use with zero surprises.