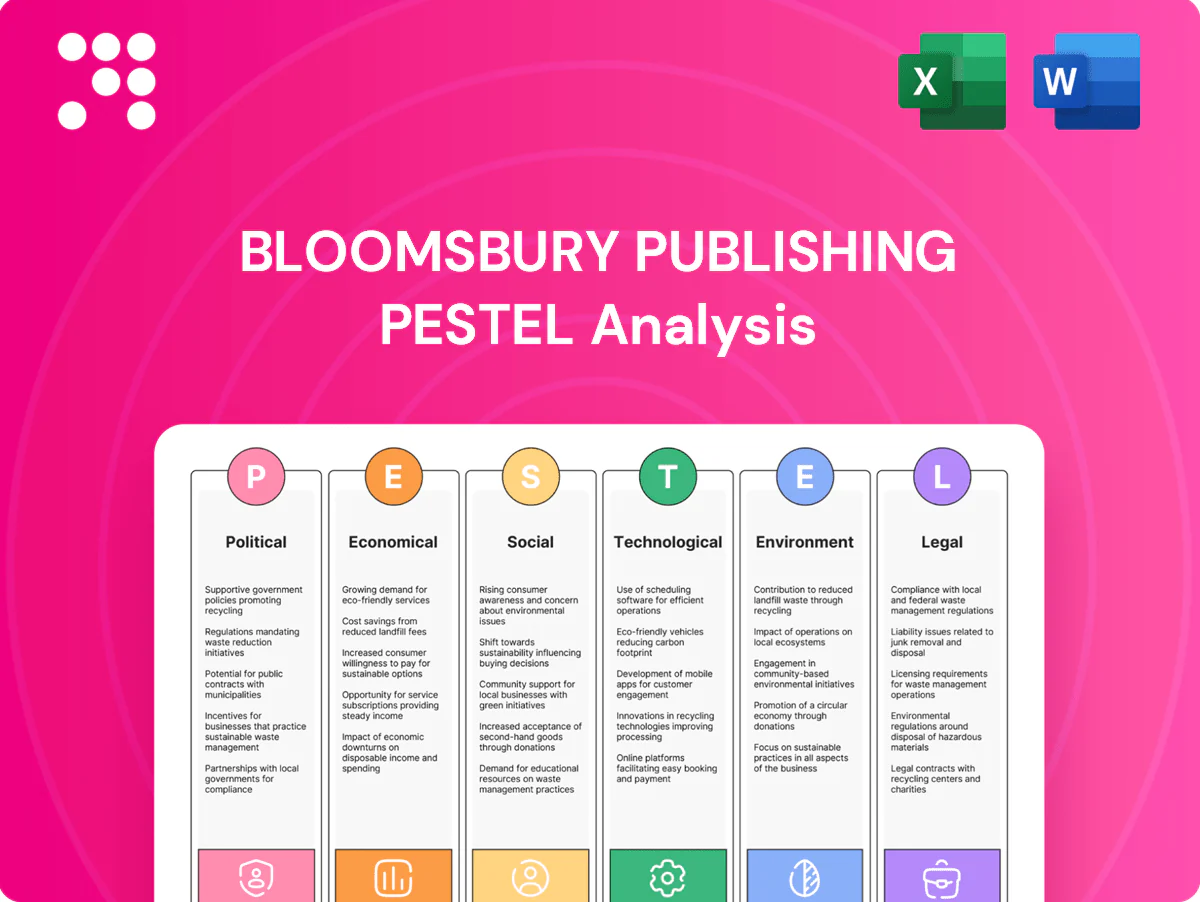

Bloomsbury Publishing PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, digital disruption, and changing reader demographics are reshaping Bloomsbury Publishing in our concise PESTLE overview—perfect for investors and strategists. Gain the full, actionable analysis to quantify risks, spot growth levers, and inform decisions. Purchase the complete PESTLE now for instant, editable insights.

Political factors

Education and arts funding

Public funding for schools, universities and libraries—UK education spending exceeded £100 billion in 2024—directly shapes demand for academic and children’s titles. Shifts in government priorities can expand or contract institutional orders for print and digital resources. Bloomsbury’s academic platforms benefit when education budgets rise; austerity or reallocations pressure renewals and course adoption.

Trade policy and Brexit spillovers

Tariffs are minimal for printed books, but customs frictions and differing VAT rules (EU VAT on books ranges 0–27%, Hungary 27%) raise cross-border distribution costs and compliance time for Bloomsbury. Post-Brexit regulatory divergence has added paperwork and can extend EU logistics lead times by several days, increasing inventory and freight spend. GBP/EUR volatility (c.1.10–1.20 in 2022–24) affects reported revenues and royalty payouts. Efficient EU warehousing and localized print-on-demand reduce tariff exposure, VAT complexity and FX risk.

Censorship and content controls

Regional restrictions on sensitive topics shape Bloomsbury’s title availability and marketing, forcing removal or limited distribution in certain jurisdictions and affecting sales mix; FY 2024 group revenue was £517.9m, highlighting exposure to market-specific curbs. Compliance with country-specific content rules can block market access or require edited editions, raising production and legal costs. Bloomsbury must balance editorial independence with local laws while diversifying markets to reduce concentration risk from regulatory crackdowns.

Public procurement and library policies

National and municipal acquisition frameworks determine library eligibility and pricing, influencing Bloomsbury’s institutional sales; public procurement—about 14% of EU GDP—can accelerate catalog penetration when standards favor value. eLending policies and one-copy/one-user models (widely used by major platforms) shape digital circulation economics and revenue timing, while shifts to open procurement may intensify competition.

- UK population 67 million (2024) — market scale

- Procurement ~14% of EU GDP — buying power

- One-copy/one-user dominates eLending — limits simultaneous revenue

- Open procurement raises price/value competition

Geopolitics and supply chain resilience

Conflicts and sanctions disrupt paper supply, printing hubs and shipping routes, forcing delays and cost pass-throughs. Political instability raised insurance and logistics costs for physical books, with cargo insurance up over 20% on high-risk routes in 2024. Diversified suppliers and regional print partners reduce exposure, while scenario planning supports continuity for academic cycles and trade seasons.

- Disruptions: paper, printing, shipping

- Cost impact: insurance +20% (2024)

- Mitigation: regional printers, multiple suppliers

- Preparedness: scenario planning for term and peak seasons

Public education >£100bn fuels academic publishing; regional print-on-demand reduces VAT/FX risk

Public education spend >£100bn (2024) drives academic and children’s demand; Bloomsbury revenue £517.9m (FY2024) ties to institutional budgets.

Post-Brexit VAT divergence (EU 0–27%), GBP/EUR 1.10–1.20 (2022–24) and customs frictions raise distribution costs; regional print-on-demand mitigates FX and VAT exposure.

Political instability and sanctions lifted insurance and logistics costs (cargo insurance +20% in 2024); diversified suppliers and regional printers reduce disruption risk.

| Metric | 2024 |

|---|---|

| UK pop | 67m |

| Education spend | £>100bn |

| Group revenue | £517.9m |

| Cargo insurance | +20% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect Bloomsbury Publishing, with data-backed trends, forward-looking insights and specific sub-points to help executives, investors and strategists mitigate risks, capture opportunities and prepare investor-ready plans.

A concise, visually segmented PESTLE summary of Bloomsbury Publishing that’s easy to drop into presentations, editable for local context, and shareable across teams to streamline external risk discussions and strategic planning.

Economic factors

Consumer spending cycles

Discretionary household budgets strongly influence Bloomsbury’s trade fiction and non-fiction, with the UK book market around £6.9bn in 2023 (Nielsen/Statista), making price-sensitive categories vulnerable. Downturns push buyers to lower-priced formats, backlist and libraries, lifting backlist share. High-profile bestsellers and media tie-ins can offset cyclical weakness. Pricing and promotions must track real income trends and inflation to protect margins.

Institutional budgets and renewals

Academic subscriptions for Bloomsbury hinge on university and consortia funding, with renewal rates tied to enrollment trends and research spending; global R&D investment exceeded $2.6tn in 2023, supporting demand for scholarly content. Multi-year agreements (typically 3–5 years) stabilize cash flow but are vulnerable to budget cuts. Value-added analytics and broad content breadth drive retention and upsell opportunities.

Cost inflation in print

Paper, energy and freight inflation have compressed print margins for Bloomsbury, with global container rates falling from SCFI highs near 5,000 USD/FEU in 2021 to c.1,500 USD/FEU by 2024, but paper and energy unit costs remaining elevated versus pre‑pandemic levels; longer lead times and smaller, more frequent runs lift per‑unit costs, while print‑on‑demand cuts obsolescence and working capital; strategic pricing and a larger digital/format mix help preserve gross margin.

FX exposure and royalties

Global sales expose Bloomsbury to GBP, USD and EUR translation effects that materially impact reported results; over half of group revenue comes from overseas markets, amplifying FX swings on margins. Currency moves feed through to author royalties and co-edition income, while hedging programmes smooth but add cost. Localised pricing and regional editions are used to reduce FX-driven volatility.

- FX translation: GBP/USD/EUR mix

- Royalties: exposed to exchange swings

- Hedging: reduces volatility, increases hedging cost

- Pricing: localised to mitigate FX risk

Retail channel concentration

Dependence on large online retailers, notably Amazon, concentrates negotiating power and makes discoverability a key commercial risk for Bloomsbury, while independent bookstores and direct-to-consumer channels deliver higher margins and richer customer data that support backlist value and marketing.

- Concentration: online retailers dominate discoverability and terms

- Independents/DTC: better margins and customer data

- Wholesaler consolidation: tighter bargaining power

- Balanced mix: lowers revenue volatility

Public education >£100bn fuels academic publishing; regional print-on-demand reduces VAT/FX risk

Household discretionary spend and UK book market (~£6.9bn in 2023) drive trade sales; inflation and real-income trends pressure pricing and format mix. Academic demand ties to university funding and global R&D (~$2.6tn in 2023), stabilised by 3–5 year subscriptions. Input cost inflation (paper, energy) and FX (c.50% revenue overseas) compress margins; hedging and digital mix mitigate risk.

| Metric | 2023/24 | Impact |

|---|---|---|

| UK market | £6.9bn (2023) | Trade sensitivity |

| Global R&D | $2.6tn (2023) | Academic demand |

| Container rates | ~$1,500/FEU (2024) | Print costs |

| Overseas rev | ~50% of group | FX exposure |

Full Version Awaits

Bloomsbury Publishing PESTLE Analysis

The Bloomsbury Publishing PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides the full political, economic, social, technological, legal and environmental assessment with no placeholders. The layout, content, and structure visible are exactly what you’ll download immediately after buying.

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, digital disruption, and changing reader demographics are reshaping Bloomsbury Publishing in our concise PESTLE overview—perfect for investors and strategists. Gain the full, actionable analysis to quantify risks, spot growth levers, and inform decisions. Purchase the complete PESTLE now for instant, editable insights.

Political factors

Education and arts funding

Public funding for schools, universities and libraries—UK education spending exceeded £100 billion in 2024—directly shapes demand for academic and children’s titles. Shifts in government priorities can expand or contract institutional orders for print and digital resources. Bloomsbury’s academic platforms benefit when education budgets rise; austerity or reallocations pressure renewals and course adoption.

Trade policy and Brexit spillovers

Tariffs are minimal for printed books, but customs frictions and differing VAT rules (EU VAT on books ranges 0–27%, Hungary 27%) raise cross-border distribution costs and compliance time for Bloomsbury. Post-Brexit regulatory divergence has added paperwork and can extend EU logistics lead times by several days, increasing inventory and freight spend. GBP/EUR volatility (c.1.10–1.20 in 2022–24) affects reported revenues and royalty payouts. Efficient EU warehousing and localized print-on-demand reduce tariff exposure, VAT complexity and FX risk.

Censorship and content controls

Regional restrictions on sensitive topics shape Bloomsbury’s title availability and marketing, forcing removal or limited distribution in certain jurisdictions and affecting sales mix; FY 2024 group revenue was £517.9m, highlighting exposure to market-specific curbs. Compliance with country-specific content rules can block market access or require edited editions, raising production and legal costs. Bloomsbury must balance editorial independence with local laws while diversifying markets to reduce concentration risk from regulatory crackdowns.

Public procurement and library policies

National and municipal acquisition frameworks determine library eligibility and pricing, influencing Bloomsbury’s institutional sales; public procurement—about 14% of EU GDP—can accelerate catalog penetration when standards favor value. eLending policies and one-copy/one-user models (widely used by major platforms) shape digital circulation economics and revenue timing, while shifts to open procurement may intensify competition.

- UK population 67 million (2024) — market scale

- Procurement ~14% of EU GDP — buying power

- One-copy/one-user dominates eLending — limits simultaneous revenue

- Open procurement raises price/value competition

Geopolitics and supply chain resilience

Conflicts and sanctions disrupt paper supply, printing hubs and shipping routes, forcing delays and cost pass-throughs. Political instability raised insurance and logistics costs for physical books, with cargo insurance up over 20% on high-risk routes in 2024. Diversified suppliers and regional print partners reduce exposure, while scenario planning supports continuity for academic cycles and trade seasons.

- Disruptions: paper, printing, shipping

- Cost impact: insurance +20% (2024)

- Mitigation: regional printers, multiple suppliers

- Preparedness: scenario planning for term and peak seasons

Public education >£100bn fuels academic publishing; regional print-on-demand reduces VAT/FX risk

Public education spend >£100bn (2024) drives academic and children’s demand; Bloomsbury revenue £517.9m (FY2024) ties to institutional budgets.

Post-Brexit VAT divergence (EU 0–27%), GBP/EUR 1.10–1.20 (2022–24) and customs frictions raise distribution costs; regional print-on-demand mitigates FX and VAT exposure.

Political instability and sanctions lifted insurance and logistics costs (cargo insurance +20% in 2024); diversified suppliers and regional printers reduce disruption risk.

| Metric | 2024 |

|---|---|

| UK pop | 67m |

| Education spend | £>100bn |

| Group revenue | £517.9m |

| Cargo insurance | +20% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect Bloomsbury Publishing, with data-backed trends, forward-looking insights and specific sub-points to help executives, investors and strategists mitigate risks, capture opportunities and prepare investor-ready plans.

A concise, visually segmented PESTLE summary of Bloomsbury Publishing that’s easy to drop into presentations, editable for local context, and shareable across teams to streamline external risk discussions and strategic planning.

Economic factors

Consumer spending cycles

Discretionary household budgets strongly influence Bloomsbury’s trade fiction and non-fiction, with the UK book market around £6.9bn in 2023 (Nielsen/Statista), making price-sensitive categories vulnerable. Downturns push buyers to lower-priced formats, backlist and libraries, lifting backlist share. High-profile bestsellers and media tie-ins can offset cyclical weakness. Pricing and promotions must track real income trends and inflation to protect margins.

Institutional budgets and renewals

Academic subscriptions for Bloomsbury hinge on university and consortia funding, with renewal rates tied to enrollment trends and research spending; global R&D investment exceeded $2.6tn in 2023, supporting demand for scholarly content. Multi-year agreements (typically 3–5 years) stabilize cash flow but are vulnerable to budget cuts. Value-added analytics and broad content breadth drive retention and upsell opportunities.

Cost inflation in print

Paper, energy and freight inflation have compressed print margins for Bloomsbury, with global container rates falling from SCFI highs near 5,000 USD/FEU in 2021 to c.1,500 USD/FEU by 2024, but paper and energy unit costs remaining elevated versus pre‑pandemic levels; longer lead times and smaller, more frequent runs lift per‑unit costs, while print‑on‑demand cuts obsolescence and working capital; strategic pricing and a larger digital/format mix help preserve gross margin.

FX exposure and royalties

Global sales expose Bloomsbury to GBP, USD and EUR translation effects that materially impact reported results; over half of group revenue comes from overseas markets, amplifying FX swings on margins. Currency moves feed through to author royalties and co-edition income, while hedging programmes smooth but add cost. Localised pricing and regional editions are used to reduce FX-driven volatility.

- FX translation: GBP/USD/EUR mix

- Royalties: exposed to exchange swings

- Hedging: reduces volatility, increases hedging cost

- Pricing: localised to mitigate FX risk

Retail channel concentration

Dependence on large online retailers, notably Amazon, concentrates negotiating power and makes discoverability a key commercial risk for Bloomsbury, while independent bookstores and direct-to-consumer channels deliver higher margins and richer customer data that support backlist value and marketing.

- Concentration: online retailers dominate discoverability and terms

- Independents/DTC: better margins and customer data

- Wholesaler consolidation: tighter bargaining power

- Balanced mix: lowers revenue volatility

Public education >£100bn fuels academic publishing; regional print-on-demand reduces VAT/FX risk

Household discretionary spend and UK book market (~£6.9bn in 2023) drive trade sales; inflation and real-income trends pressure pricing and format mix. Academic demand ties to university funding and global R&D (~$2.6tn in 2023), stabilised by 3–5 year subscriptions. Input cost inflation (paper, energy) and FX (c.50% revenue overseas) compress margins; hedging and digital mix mitigate risk.

| Metric | 2023/24 | Impact |

|---|---|---|

| UK market | £6.9bn (2023) | Trade sensitivity |

| Global R&D | $2.6tn (2023) | Academic demand |

| Container rates | ~$1,500/FEU (2024) | Print costs |

| Overseas rev | ~50% of group | FX exposure |

Full Version Awaits

Bloomsbury Publishing PESTLE Analysis

The Bloomsbury Publishing PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides the full political, economic, social, technological, legal and environmental assessment with no placeholders. The layout, content, and structure visible are exactly what you’ll download immediately after buying.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, digital disruption, and changing reader demographics are reshaping Bloomsbury Publishing in our concise PESTLE overview—perfect for investors and strategists. Gain the full, actionable analysis to quantify risks, spot growth levers, and inform decisions. Purchase the complete PESTLE now for instant, editable insights.

Political factors

Education and arts funding

Public funding for schools, universities and libraries—UK education spending exceeded £100 billion in 2024—directly shapes demand for academic and children’s titles. Shifts in government priorities can expand or contract institutional orders for print and digital resources. Bloomsbury’s academic platforms benefit when education budgets rise; austerity or reallocations pressure renewals and course adoption.

Trade policy and Brexit spillovers

Tariffs are minimal for printed books, but customs frictions and differing VAT rules (EU VAT on books ranges 0–27%, Hungary 27%) raise cross-border distribution costs and compliance time for Bloomsbury. Post-Brexit regulatory divergence has added paperwork and can extend EU logistics lead times by several days, increasing inventory and freight spend. GBP/EUR volatility (c.1.10–1.20 in 2022–24) affects reported revenues and royalty payouts. Efficient EU warehousing and localized print-on-demand reduce tariff exposure, VAT complexity and FX risk.

Censorship and content controls

Regional restrictions on sensitive topics shape Bloomsbury’s title availability and marketing, forcing removal or limited distribution in certain jurisdictions and affecting sales mix; FY 2024 group revenue was £517.9m, highlighting exposure to market-specific curbs. Compliance with country-specific content rules can block market access or require edited editions, raising production and legal costs. Bloomsbury must balance editorial independence with local laws while diversifying markets to reduce concentration risk from regulatory crackdowns.

Public procurement and library policies

National and municipal acquisition frameworks determine library eligibility and pricing, influencing Bloomsbury’s institutional sales; public procurement—about 14% of EU GDP—can accelerate catalog penetration when standards favor value. eLending policies and one-copy/one-user models (widely used by major platforms) shape digital circulation economics and revenue timing, while shifts to open procurement may intensify competition.

- UK population 67 million (2024) — market scale

- Procurement ~14% of EU GDP — buying power

- One-copy/one-user dominates eLending — limits simultaneous revenue

- Open procurement raises price/value competition

Geopolitics and supply chain resilience

Conflicts and sanctions disrupt paper supply, printing hubs and shipping routes, forcing delays and cost pass-throughs. Political instability raised insurance and logistics costs for physical books, with cargo insurance up over 20% on high-risk routes in 2024. Diversified suppliers and regional print partners reduce exposure, while scenario planning supports continuity for academic cycles and trade seasons.

- Disruptions: paper, printing, shipping

- Cost impact: insurance +20% (2024)

- Mitigation: regional printers, multiple suppliers

- Preparedness: scenario planning for term and peak seasons

Public education >£100bn fuels academic publishing; regional print-on-demand reduces VAT/FX risk

Public education spend >£100bn (2024) drives academic and children’s demand; Bloomsbury revenue £517.9m (FY2024) ties to institutional budgets.

Post-Brexit VAT divergence (EU 0–27%), GBP/EUR 1.10–1.20 (2022–24) and customs frictions raise distribution costs; regional print-on-demand mitigates FX and VAT exposure.

Political instability and sanctions lifted insurance and logistics costs (cargo insurance +20% in 2024); diversified suppliers and regional printers reduce disruption risk.

| Metric | 2024 |

|---|---|

| UK pop | 67m |

| Education spend | £>100bn |

| Group revenue | £517.9m |

| Cargo insurance | +20% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect Bloomsbury Publishing, with data-backed trends, forward-looking insights and specific sub-points to help executives, investors and strategists mitigate risks, capture opportunities and prepare investor-ready plans.

A concise, visually segmented PESTLE summary of Bloomsbury Publishing that’s easy to drop into presentations, editable for local context, and shareable across teams to streamline external risk discussions and strategic planning.

Economic factors

Consumer spending cycles

Discretionary household budgets strongly influence Bloomsbury’s trade fiction and non-fiction, with the UK book market around £6.9bn in 2023 (Nielsen/Statista), making price-sensitive categories vulnerable. Downturns push buyers to lower-priced formats, backlist and libraries, lifting backlist share. High-profile bestsellers and media tie-ins can offset cyclical weakness. Pricing and promotions must track real income trends and inflation to protect margins.

Institutional budgets and renewals

Academic subscriptions for Bloomsbury hinge on university and consortia funding, with renewal rates tied to enrollment trends and research spending; global R&D investment exceeded $2.6tn in 2023, supporting demand for scholarly content. Multi-year agreements (typically 3–5 years) stabilize cash flow but are vulnerable to budget cuts. Value-added analytics and broad content breadth drive retention and upsell opportunities.

Cost inflation in print

Paper, energy and freight inflation have compressed print margins for Bloomsbury, with global container rates falling from SCFI highs near 5,000 USD/FEU in 2021 to c.1,500 USD/FEU by 2024, but paper and energy unit costs remaining elevated versus pre‑pandemic levels; longer lead times and smaller, more frequent runs lift per‑unit costs, while print‑on‑demand cuts obsolescence and working capital; strategic pricing and a larger digital/format mix help preserve gross margin.

FX exposure and royalties

Global sales expose Bloomsbury to GBP, USD and EUR translation effects that materially impact reported results; over half of group revenue comes from overseas markets, amplifying FX swings on margins. Currency moves feed through to author royalties and co-edition income, while hedging programmes smooth but add cost. Localised pricing and regional editions are used to reduce FX-driven volatility.

- FX translation: GBP/USD/EUR mix

- Royalties: exposed to exchange swings

- Hedging: reduces volatility, increases hedging cost

- Pricing: localised to mitigate FX risk

Retail channel concentration

Dependence on large online retailers, notably Amazon, concentrates negotiating power and makes discoverability a key commercial risk for Bloomsbury, while independent bookstores and direct-to-consumer channels deliver higher margins and richer customer data that support backlist value and marketing.

- Concentration: online retailers dominate discoverability and terms

- Independents/DTC: better margins and customer data

- Wholesaler consolidation: tighter bargaining power

- Balanced mix: lowers revenue volatility

Public education >£100bn fuels academic publishing; regional print-on-demand reduces VAT/FX risk

Household discretionary spend and UK book market (~£6.9bn in 2023) drive trade sales; inflation and real-income trends pressure pricing and format mix. Academic demand ties to university funding and global R&D (~$2.6tn in 2023), stabilised by 3–5 year subscriptions. Input cost inflation (paper, energy) and FX (c.50% revenue overseas) compress margins; hedging and digital mix mitigate risk.

| Metric | 2023/24 | Impact |

|---|---|---|

| UK market | £6.9bn (2023) | Trade sensitivity |

| Global R&D | $2.6tn (2023) | Academic demand |

| Container rates | ~$1,500/FEU (2024) | Print costs |

| Overseas rev | ~50% of group | FX exposure |

Full Version Awaits

Bloomsbury Publishing PESTLE Analysis

The Bloomsbury Publishing PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides the full political, economic, social, technological, legal and environmental assessment with no placeholders. The layout, content, and structure visible are exactly what you’ll download immediately after buying.