BlueLinx Porter's Five Forces Analysis

Don't Miss the Bigger Picture

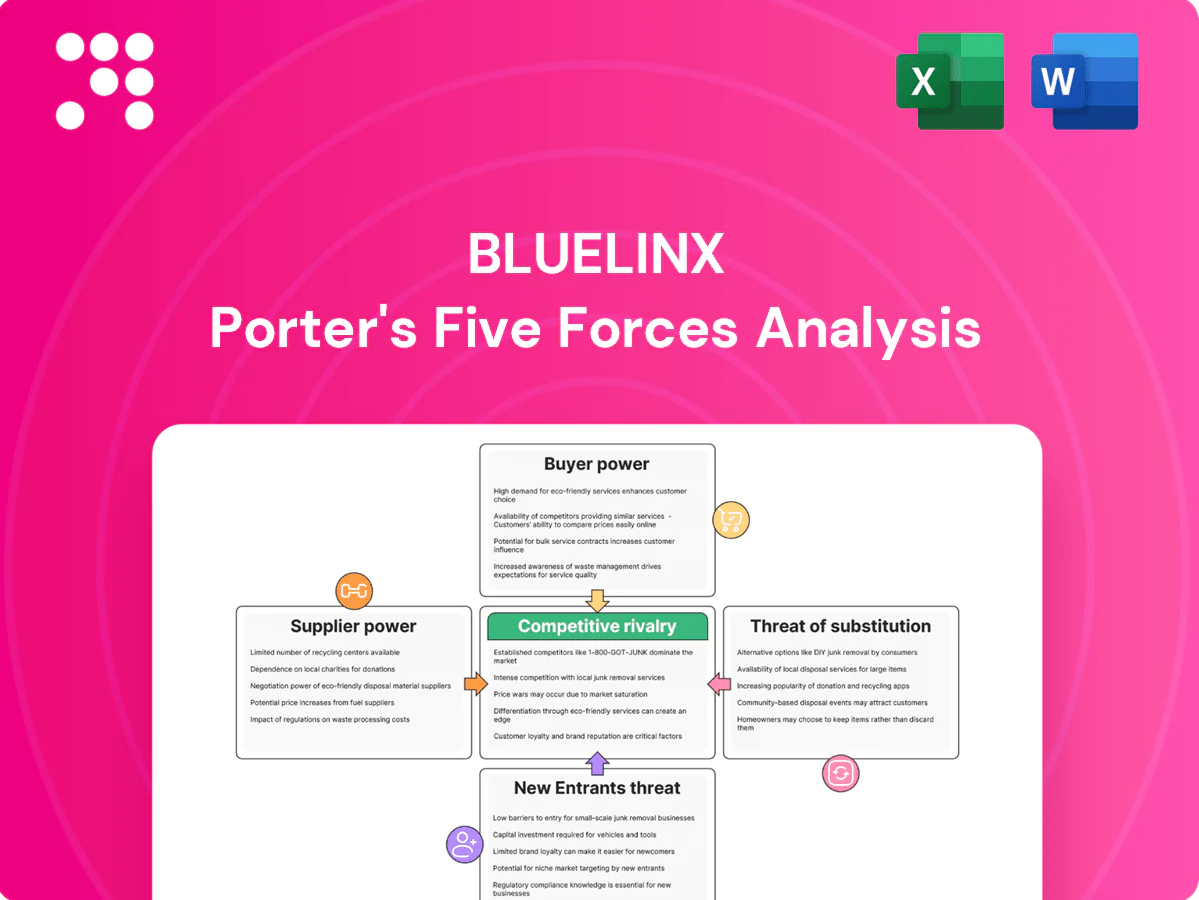

Our Porter's Five Forces snapshot highlights BlueLinx’s competitive pressures—from supplier leverage and buyer power to substitute risks—and outlines immediate strategic considerations for management and investors. This brief overview teases deeper insights into market dynamics and profitability drivers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to BlueLinx.

Suppliers Bargaining Power

Concentrated brand OEMs

Many core categories such as engineered wood, roofing and insulation are dominated by a small set of nationally recognized OEMs, creating strong supplier leverage through brand preference and code approvals that drive buyer pull toward specific manufacturers. Preferred or exclusive lines often carry volume and pricing commitments that limit BlueLinxs negotiating flexibility. BlueLinx must balance offering broad brand breadth with dependency risk on key suppliers and manage inventory and contract exposure accordingly.

Input price volatility

In 2024 commodity swings in lumber, plywood, OSB, resins and steel—with intra-year moves exceeding 40% in past cycles—heightened supplier leverage during tight markets.

Suppliers passed price increases through within weeks while distributors faced customer repricing lags of 60–90 days, compressing distributor margins.

Volatility complicated inventory risk-sharing and financing terms; strong supplier contracts protected OEM margins at distributors expense.

Logistics and allocation control

In 2024 suppliers retained tight logistics and mill-allocation control, steering limited freight and capacity to higher-margin or strategic channels, which reduced BlueLinx’s fill rates and weakened its negotiating leverage. Carload and minimum order quantity requirements increased switching frictions and inventory risk. Vendor-managed replenishment programs further shift working-capital control toward OEMs, compressing distributor margins and service flexibility.

Switching and qualification costs

Product approvals, warranties and building-code compliance create months-long switching delays for BlueLinx customers, with contractors and inspectors often specifying brands or standards that entrench OEM leverage; re-qualifying alternates requires dedicated sales effort and documentation. Suppliers exploit these frictions in price and rebate negotiations, preserving margin and contract share.

- Brand-specification risk

- Re-qualification time and cost

- Warranty/code lock-in

- Supplier rebate leverage

Counterweights: scale and multi-sourcing

BlueLinx’s national scale — operating over 100 branches and reporting roughly $3.1B in 2023 net sales — plus centralized purchasing and enhanced data visibility let it secure allocations and rebates, and multi-supplier line cards and private-label offerings blunt OEM pricing power; however, during constrained cycles supplier leverage often prevails.

Supplier concentration, 40% commodity swings and 60-90 day repricing lag squeeze distributors

Supplier concentration in engineered wood, roofing and insulation gives OEMs strong leverage via brand/code lock-in; 2024 commodity swings (intra-year moves >40%) and rapid pass-through compressed distributor margins amid 60–90 day repricing lags. BlueLinx scale and centralized purchasing (≈100 branches; $3.1B 2023 sales) mitigate but do not eliminate supplier power in constrained cycles.

| Metric | Value |

|---|---|

| 2023 Net Sales | $3.1B |

| Branches | >100 |

| 2024 commodity swings | >40% intra-year |

| Customer repricing lag | 60–90 days |

What is included in the product

Tailored Porter's Five Forces analysis for BlueLinx that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats, with strategic commentary and industry data to assess pricing leverage and long-term profitability.

A concise one-sheet Porter's Five Forces for BlueLinx that pinpoints competitive pressures and strategic levers—ready to drop into decks; customizable, macro-free, and integrates with Excel dashboards for fast, board-ready decision-making.

Customers Bargaining Power

Large national buyers

Home centers and large pro dealers like Home Depot and Lowe's together account for roughly half of U.S. home improvement sales, buying volumes that force sharp pricing and thin distributor margins. Their scale enables multi-sourcing, vendor scorecards and strict SLAs, and they routinely extract rebates, extended payment terms (often 60–90 days) and logistics concessions. This consolidated buyer power compresses margins for distributors such as BlueLinx.

Price transparency and commoditization

Commodity building products at BlueLinx are highly price-comparable across distributors and regions; daily market quotes (e.g., Random Lengths) let buyers switch on differences of pennies per unit, and spot bids now drive a large share of project purchases—industry estimates show spot/short-term purchases exceeding 40% in 2024—amplifying buyer leverage in routine replenishment.

Service differentiation as a lever

Service differentiation—time-definite delivery, cut-to-length, and JIT programs—raises switching costs and embeds BlueLinx in customer supply chains, reducing buyer power; US construction spending reached about $1.8 trillion in 2024, increasing demand for these logistics services. Sophisticated buyers still monetize value-added services in negotiations, so the net effect hinges on BlueLinx’s execution and local capacity utilization.

Demand cyclicality and credit terms

In 2024 construction-cycle softness shifted bargaining power to BlueLinx customers, who pressed for extended credit and consignment-like terms, increasing distributor working-capital strain and bad-debt risk. Buyers leveraged volume uncertainty to demand order flexibility without price premiums, compressing margins and elevating receivables days. Distributors faced higher financing needs and tighter liquidity as payment terms lengthened.

- 2024: customer leverage rose

- Extended credit and consignment risk

- Higher bad-debt and WC pressure

- Volume uncertainty → no price premium

Fragmented tail vs. concentrated head

Home centers 50%; spot > 40%; 60-90d terms squeeze WC

Large buyers like Home Depot and Lowe's account for roughly half of U.S. home improvement sales, using scale to extract rebates, 60–90 day payment terms and logistics concessions that compress distributor margins. Spot/short-term purchases exceeded 40% in 2024, increasing price sensitivity; service differentiation (JIT, cut-to-length) mitigates but does not eliminate buyer leverage. 2024 construction spending was about $1.8 trillion, yet softened demand shifted bargaining power to customers, raising working-capital and bad-debt risks for BlueLinx.

| Metric | 2024 Value | Implication |

|---|---|---|

| Share by home centers | ~50% | High concentrated buyer power |

| Spot/short-term purchases | >40% | Price-driven switching |

| Payment terms | 60–90 days | WC strain on distributors |

| US construction spending | $1.8T | Demand for logistics services |

Full Version Awaits

BlueLinx Porter's Five Forces Analysis

This preview shows the exact BlueLinx Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The content covers industry rivalry, supplier and buyer power, and threats of new entrants and substitutes with actionable insights. What you see is what you get.

Don't Miss the Bigger Picture

Our Porter's Five Forces snapshot highlights BlueLinx’s competitive pressures—from supplier leverage and buyer power to substitute risks—and outlines immediate strategic considerations for management and investors. This brief overview teases deeper insights into market dynamics and profitability drivers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to BlueLinx.

Suppliers Bargaining Power

Concentrated brand OEMs

Many core categories such as engineered wood, roofing and insulation are dominated by a small set of nationally recognized OEMs, creating strong supplier leverage through brand preference and code approvals that drive buyer pull toward specific manufacturers. Preferred or exclusive lines often carry volume and pricing commitments that limit BlueLinxs negotiating flexibility. BlueLinx must balance offering broad brand breadth with dependency risk on key suppliers and manage inventory and contract exposure accordingly.

Input price volatility

In 2024 commodity swings in lumber, plywood, OSB, resins and steel—with intra-year moves exceeding 40% in past cycles—heightened supplier leverage during tight markets.

Suppliers passed price increases through within weeks while distributors faced customer repricing lags of 60–90 days, compressing distributor margins.

Volatility complicated inventory risk-sharing and financing terms; strong supplier contracts protected OEM margins at distributors expense.

Logistics and allocation control

In 2024 suppliers retained tight logistics and mill-allocation control, steering limited freight and capacity to higher-margin or strategic channels, which reduced BlueLinx’s fill rates and weakened its negotiating leverage. Carload and minimum order quantity requirements increased switching frictions and inventory risk. Vendor-managed replenishment programs further shift working-capital control toward OEMs, compressing distributor margins and service flexibility.

Switching and qualification costs

Product approvals, warranties and building-code compliance create months-long switching delays for BlueLinx customers, with contractors and inspectors often specifying brands or standards that entrench OEM leverage; re-qualifying alternates requires dedicated sales effort and documentation. Suppliers exploit these frictions in price and rebate negotiations, preserving margin and contract share.

- Brand-specification risk

- Re-qualification time and cost

- Warranty/code lock-in

- Supplier rebate leverage

Counterweights: scale and multi-sourcing

BlueLinx’s national scale — operating over 100 branches and reporting roughly $3.1B in 2023 net sales — plus centralized purchasing and enhanced data visibility let it secure allocations and rebates, and multi-supplier line cards and private-label offerings blunt OEM pricing power; however, during constrained cycles supplier leverage often prevails.

Supplier concentration, 40% commodity swings and 60-90 day repricing lag squeeze distributors

Supplier concentration in engineered wood, roofing and insulation gives OEMs strong leverage via brand/code lock-in; 2024 commodity swings (intra-year moves >40%) and rapid pass-through compressed distributor margins amid 60–90 day repricing lags. BlueLinx scale and centralized purchasing (≈100 branches; $3.1B 2023 sales) mitigate but do not eliminate supplier power in constrained cycles.

| Metric | Value |

|---|---|

| 2023 Net Sales | $3.1B |

| Branches | >100 |

| 2024 commodity swings | >40% intra-year |

| Customer repricing lag | 60–90 days |

What is included in the product

Tailored Porter's Five Forces analysis for BlueLinx that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats, with strategic commentary and industry data to assess pricing leverage and long-term profitability.

A concise one-sheet Porter's Five Forces for BlueLinx that pinpoints competitive pressures and strategic levers—ready to drop into decks; customizable, macro-free, and integrates with Excel dashboards for fast, board-ready decision-making.

Customers Bargaining Power

Large national buyers

Home centers and large pro dealers like Home Depot and Lowe's together account for roughly half of U.S. home improvement sales, buying volumes that force sharp pricing and thin distributor margins. Their scale enables multi-sourcing, vendor scorecards and strict SLAs, and they routinely extract rebates, extended payment terms (often 60–90 days) and logistics concessions. This consolidated buyer power compresses margins for distributors such as BlueLinx.

Price transparency and commoditization

Commodity building products at BlueLinx are highly price-comparable across distributors and regions; daily market quotes (e.g., Random Lengths) let buyers switch on differences of pennies per unit, and spot bids now drive a large share of project purchases—industry estimates show spot/short-term purchases exceeding 40% in 2024—amplifying buyer leverage in routine replenishment.

Service differentiation as a lever

Service differentiation—time-definite delivery, cut-to-length, and JIT programs—raises switching costs and embeds BlueLinx in customer supply chains, reducing buyer power; US construction spending reached about $1.8 trillion in 2024, increasing demand for these logistics services. Sophisticated buyers still monetize value-added services in negotiations, so the net effect hinges on BlueLinx’s execution and local capacity utilization.

Demand cyclicality and credit terms

In 2024 construction-cycle softness shifted bargaining power to BlueLinx customers, who pressed for extended credit and consignment-like terms, increasing distributor working-capital strain and bad-debt risk. Buyers leveraged volume uncertainty to demand order flexibility without price premiums, compressing margins and elevating receivables days. Distributors faced higher financing needs and tighter liquidity as payment terms lengthened.

- 2024: customer leverage rose

- Extended credit and consignment risk

- Higher bad-debt and WC pressure

- Volume uncertainty → no price premium

Fragmented tail vs. concentrated head

Home centers 50%; spot > 40%; 60-90d terms squeeze WC

Large buyers like Home Depot and Lowe's account for roughly half of U.S. home improvement sales, using scale to extract rebates, 60–90 day payment terms and logistics concessions that compress distributor margins. Spot/short-term purchases exceeded 40% in 2024, increasing price sensitivity; service differentiation (JIT, cut-to-length) mitigates but does not eliminate buyer leverage. 2024 construction spending was about $1.8 trillion, yet softened demand shifted bargaining power to customers, raising working-capital and bad-debt risks for BlueLinx.

| Metric | 2024 Value | Implication |

|---|---|---|

| Share by home centers | ~50% | High concentrated buyer power |

| Spot/short-term purchases | >40% | Price-driven switching |

| Payment terms | 60–90 days | WC strain on distributors |

| US construction spending | $1.8T | Demand for logistics services |

Full Version Awaits

BlueLinx Porter's Five Forces Analysis

This preview shows the exact BlueLinx Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The content covers industry rivalry, supplier and buyer power, and threats of new entrants and substitutes with actionable insights. What you see is what you get.

Description

Don't Miss the Bigger Picture

Our Porter's Five Forces snapshot highlights BlueLinx’s competitive pressures—from supplier leverage and buyer power to substitute risks—and outlines immediate strategic considerations for management and investors. This brief overview teases deeper insights into market dynamics and profitability drivers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to BlueLinx.

Suppliers Bargaining Power

Concentrated brand OEMs

Many core categories such as engineered wood, roofing and insulation are dominated by a small set of nationally recognized OEMs, creating strong supplier leverage through brand preference and code approvals that drive buyer pull toward specific manufacturers. Preferred or exclusive lines often carry volume and pricing commitments that limit BlueLinxs negotiating flexibility. BlueLinx must balance offering broad brand breadth with dependency risk on key suppliers and manage inventory and contract exposure accordingly.

Input price volatility

In 2024 commodity swings in lumber, plywood, OSB, resins and steel—with intra-year moves exceeding 40% in past cycles—heightened supplier leverage during tight markets.

Suppliers passed price increases through within weeks while distributors faced customer repricing lags of 60–90 days, compressing distributor margins.

Volatility complicated inventory risk-sharing and financing terms; strong supplier contracts protected OEM margins at distributors expense.

Logistics and allocation control

In 2024 suppliers retained tight logistics and mill-allocation control, steering limited freight and capacity to higher-margin or strategic channels, which reduced BlueLinx’s fill rates and weakened its negotiating leverage. Carload and minimum order quantity requirements increased switching frictions and inventory risk. Vendor-managed replenishment programs further shift working-capital control toward OEMs, compressing distributor margins and service flexibility.

Switching and qualification costs

Product approvals, warranties and building-code compliance create months-long switching delays for BlueLinx customers, with contractors and inspectors often specifying brands or standards that entrench OEM leverage; re-qualifying alternates requires dedicated sales effort and documentation. Suppliers exploit these frictions in price and rebate negotiations, preserving margin and contract share.

- Brand-specification risk

- Re-qualification time and cost

- Warranty/code lock-in

- Supplier rebate leverage

Counterweights: scale and multi-sourcing

BlueLinx’s national scale — operating over 100 branches and reporting roughly $3.1B in 2023 net sales — plus centralized purchasing and enhanced data visibility let it secure allocations and rebates, and multi-supplier line cards and private-label offerings blunt OEM pricing power; however, during constrained cycles supplier leverage often prevails.

Supplier concentration, 40% commodity swings and 60-90 day repricing lag squeeze distributors

Supplier concentration in engineered wood, roofing and insulation gives OEMs strong leverage via brand/code lock-in; 2024 commodity swings (intra-year moves >40%) and rapid pass-through compressed distributor margins amid 60–90 day repricing lags. BlueLinx scale and centralized purchasing (≈100 branches; $3.1B 2023 sales) mitigate but do not eliminate supplier power in constrained cycles.

| Metric | Value |

|---|---|

| 2023 Net Sales | $3.1B |

| Branches | >100 |

| 2024 commodity swings | >40% intra-year |

| Customer repricing lag | 60–90 days |

What is included in the product

Tailored Porter's Five Forces analysis for BlueLinx that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats, with strategic commentary and industry data to assess pricing leverage and long-term profitability.

A concise one-sheet Porter's Five Forces for BlueLinx that pinpoints competitive pressures and strategic levers—ready to drop into decks; customizable, macro-free, and integrates with Excel dashboards for fast, board-ready decision-making.

Customers Bargaining Power

Large national buyers

Home centers and large pro dealers like Home Depot and Lowe's together account for roughly half of U.S. home improvement sales, buying volumes that force sharp pricing and thin distributor margins. Their scale enables multi-sourcing, vendor scorecards and strict SLAs, and they routinely extract rebates, extended payment terms (often 60–90 days) and logistics concessions. This consolidated buyer power compresses margins for distributors such as BlueLinx.

Price transparency and commoditization

Commodity building products at BlueLinx are highly price-comparable across distributors and regions; daily market quotes (e.g., Random Lengths) let buyers switch on differences of pennies per unit, and spot bids now drive a large share of project purchases—industry estimates show spot/short-term purchases exceeding 40% in 2024—amplifying buyer leverage in routine replenishment.

Service differentiation as a lever

Service differentiation—time-definite delivery, cut-to-length, and JIT programs—raises switching costs and embeds BlueLinx in customer supply chains, reducing buyer power; US construction spending reached about $1.8 trillion in 2024, increasing demand for these logistics services. Sophisticated buyers still monetize value-added services in negotiations, so the net effect hinges on BlueLinx’s execution and local capacity utilization.

Demand cyclicality and credit terms

In 2024 construction-cycle softness shifted bargaining power to BlueLinx customers, who pressed for extended credit and consignment-like terms, increasing distributor working-capital strain and bad-debt risk. Buyers leveraged volume uncertainty to demand order flexibility without price premiums, compressing margins and elevating receivables days. Distributors faced higher financing needs and tighter liquidity as payment terms lengthened.

- 2024: customer leverage rose

- Extended credit and consignment risk

- Higher bad-debt and WC pressure

- Volume uncertainty → no price premium

Fragmented tail vs. concentrated head

Home centers 50%; spot > 40%; 60-90d terms squeeze WC

Large buyers like Home Depot and Lowe's account for roughly half of U.S. home improvement sales, using scale to extract rebates, 60–90 day payment terms and logistics concessions that compress distributor margins. Spot/short-term purchases exceeded 40% in 2024, increasing price sensitivity; service differentiation (JIT, cut-to-length) mitigates but does not eliminate buyer leverage. 2024 construction spending was about $1.8 trillion, yet softened demand shifted bargaining power to customers, raising working-capital and bad-debt risks for BlueLinx.

| Metric | 2024 Value | Implication |

|---|---|---|

| Share by home centers | ~50% | High concentrated buyer power |

| Spot/short-term purchases | >40% | Price-driven switching |

| Payment terms | 60–90 days | WC strain on distributors |

| US construction spending | $1.8T | Demand for logistics services |

Full Version Awaits

BlueLinx Porter's Five Forces Analysis

This preview shows the exact BlueLinx Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The content covers industry rivalry, supplier and buyer power, and threats of new entrants and substitutes with actionable insights. What you see is what you get.