Blue Ridge Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, regional economic trends, and emerging fintech threats are shaping Blue Ridge Bank’s outlook in our concise PESTLE snapshot—essential reading for investors and strategists. This analysis highlights immediate risks and growth levers so you can make faster, smarter decisions. Purchase the full PESTLE report to access detailed evidence, actionable recommendations, and editable charts for boardroom-ready use.

Political factors

Regulatory oversight shifts

Changes in U.S. banking policy under different administrations can tighten or loosen supervision for community banks; in 2024 community banks held about 12% of U.S. banking assets. Blue Ridge Bank must adapt to evolving priorities at the OCC, FDIC, Federal Reserve and CFPB, which shift compliance budgets, product design and risk appetites. Proactive regulatory engagement reduces operational disruption.

Community banking policy support

Federal and state initiatives aim to preserve community banking and small-business credit access by supporting lenders through programs such as SBA guarantees and SSBCI; SBA 7(a) guarantees can cover up to 85% of a loan and SSBCI was funded at about 10 billion dollars. Accessing these programs can boost yield and lower loss severity by shifting credit risk to guarantees and incentives. Political commitment to these supports can wax and wane.

Geopolitical and macro stability

Global tensions raise funding costs and market volatility, with US federal funds at 5.25–5.50% (July 2025) and the 10-year Treasury near 4.3%, elevating term funding and hedging expenses for banks. Regional banks like Blue Ridge feel spillovers via deposit shifts and marked-to-market securities losses. Political stability reduces risk premia and supports lending confidence. Strong contingency planning preserves liquidity resilience.

Local government development priorities

Local government development priorities directly shape Blue Ridge Bank’s loan pipeline: county and municipal incentives, zoning changes, infrastructure spending and 5–20 year tax abatements drive real estate and small-business activity and can accelerate originations; strong local relationships surface early opportunities, while policy reversals or funding cuts elevate project delay risk and credit stress.

- Incentives influence deal flow

- Zoning & infrastructure steer collateral quality

- 5–20 year abatements affect borrower cash flow

- Policy reversals raise credit/default risk

Cannabis and emerging industries stance

Policy shifts, 12% assets, $10B SSBCI and higher rates press community bank compliance

Political shifts reshape supervision and compliance budgets for community banks (they held ~12% of U.S. banking assets in 2024), while federal/state programs (SSBCI ~$10B, SBA 7(a) guarantees up to 85%) and local incentives drive originations; rising rates (fed 5.25–5.50% and 10y ~4.3% in July 2025) raise funding costs and volatility. Cannabis state patchwork (20+ adult-use, 38 medical in 2025) adds BSA/AML complexity.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Regulation | 12% assets (2024) | Compliance cost, capital planning |

| Support programs | SSBCI $10B; SBA up to 85% | Lower loss severity, higher originations |

| Rates | Fed 5.25–5.50%; 10y ~4.3% | Higher funding/hedge costs |

| Cannabis | 20+ adult, 38 medical (2025) | Operational & BSA risk |

What is included in the product

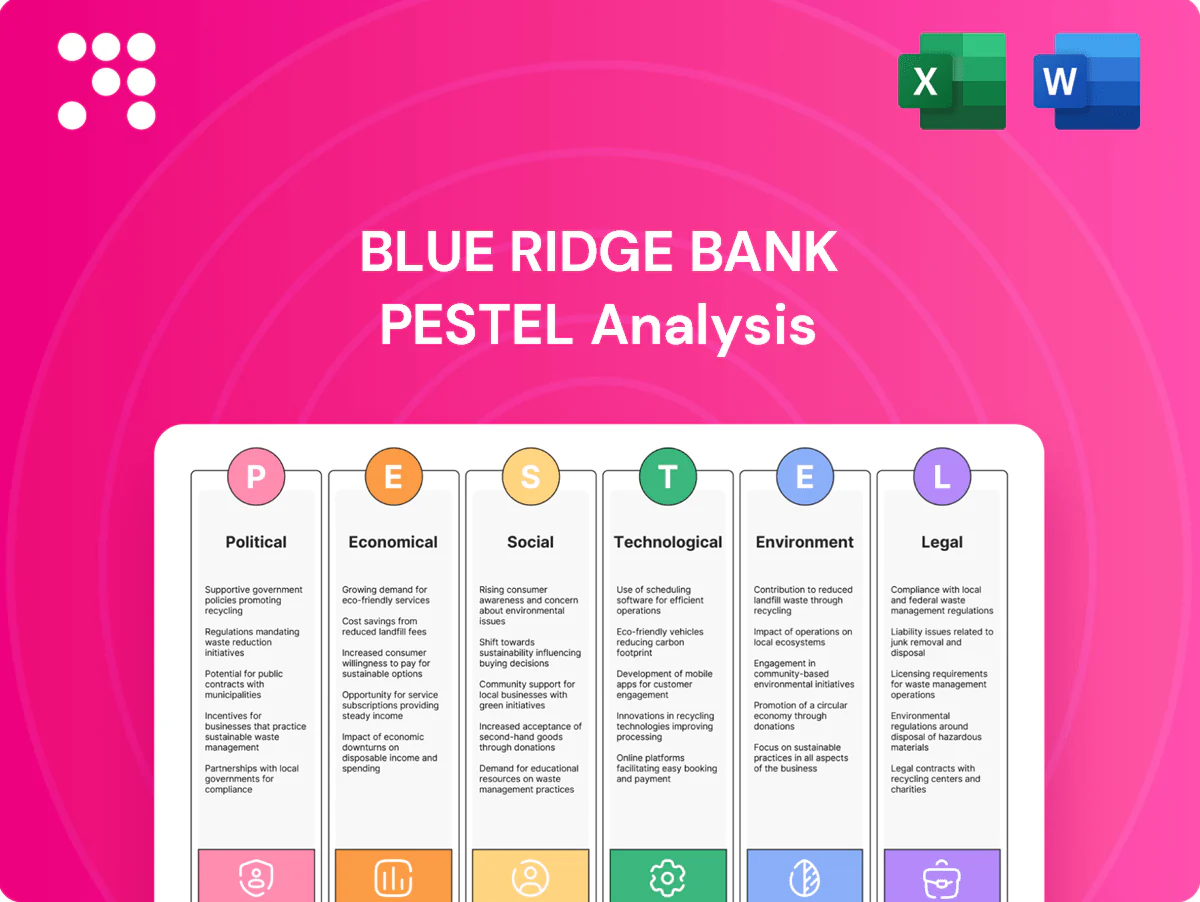

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Blue Ridge Bank, with data-backed, region-specific insights to identify risks, opportunities and forward-looking strategic responses for executives, investors and advisors.

Visually segmented by PESTEL categories for immediate interpretation and easily droppable into presentations, this Blue Ridge Bank PESTLE summary speeds alignment across teams and supports focused discussions on external risks and market positioning during planning sessions.

Economic factors

Interest rate cycle and margin

Net interest margin for Blue Ridge Bank is driven by Fed policy (federal funds 5.25–5.50% as of July 2025), deposit betas and asset repricing. Rapid hikes compress securities marks and raise funding costs; cuts squeeze asset yields. Balance-sheet hedging and mix management are key, with scenario analyses guiding pricing discipline.

Regional economic health

Regional employment strength and modest population growth support loan demand for Blue Ridge Bank; U.S. unemployment averaged 3.7% in 2024 and local labor markets in the Mid-Atlantic showed near-national growth, boosting retail and mortgage originations. Rising small-business formation (over 4 million applications nationwide in 2023–24) fuels CRE and commercial lending but concentrations in CRE or single industries raise cyclicality. Diversifying sector exposure and early delinquency monitoring cut loss severity and stabilize earnings.

Yield curve shape

An inverted 2s10s curve (about -60 bps at its 2023–24 trough) compresses spread banking at Blue Ridge and forces deposit-rate competition, pressuring NIM and liquidity costs. A 2025 partial steepening (~+30–40 bps YTD) can revive NIM but increases reinvestment risk as short rates remain elevated. Securities duration choices drive OCI volatility and regulatory capital swings, so dynamic ALM stress-testing and hedge optimization are essential.

Liquidity and deposit competition

Fintechs and large banks have bid up deposit rates amid a higher-rate regime (federal funds roughly 5.25%), pressuring Blue Ridge Bank's community-bank funding costs. Relationship banking and treasury services help defend core deposits through deeper client engagement. Brokered and wholesale funding add flexibility but raise cost and regulatory scrutiny. Pricing analytics optimize retention and margin.

- Higher-rate pressure — competitor bids ↑

- Defense — relationship banking & treasury services

- Supplement — brokered/wholesale funding (flexible but costlier)

- Optimize — pricing analytics for retention

Credit cycle and underwriting

Tighter financial conditions, with the federal funds rate near 5.25% in 2024–25, have exposed borrower stress in CRE and SMBs; Blue Ridge Bank mitigates this via prudent LTVs, covenants and sector limits to reduce tail risk, while countercyclical provisioning bolsters loss absorption and data-driven monitoring accelerates targeted interventions.

- CRE/SMB stress: heightened by higher rates

- Risk controls: conservative LTVs, covenants, sector caps

- Resilience: countercyclical reserves

- Early action: data-driven monitoring

Policy shifts, 12% assets, $10B SSBCI and higher rates press community bank compliance

NIM driven by Fed policy (federal funds 5.25–5.50% Jul 2025), deposit betas and asset repricing; hedging and mix management essential.

Regional job growth (US unemployment 3.7% 2024) supports loan demand; CRE/SMB stress elevated under higher rates.

2s10s inverted ≈-60bps (2023–24); 2025 YTD steepening +30–40bps; deposit competition lifts funding costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| Unemployment | 3.7% (2024) |

| 2s10s | -60bps trough; +30–40bps YTD 2025 |

Preview the Actual Deliverable

Blue Ridge Bank PESTLE Analysis

The Blue Ridge Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure. No placeholders or teasers; this is the final file available for immediate download.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, regional economic trends, and emerging fintech threats are shaping Blue Ridge Bank’s outlook in our concise PESTLE snapshot—essential reading for investors and strategists. This analysis highlights immediate risks and growth levers so you can make faster, smarter decisions. Purchase the full PESTLE report to access detailed evidence, actionable recommendations, and editable charts for boardroom-ready use.

Political factors

Regulatory oversight shifts

Changes in U.S. banking policy under different administrations can tighten or loosen supervision for community banks; in 2024 community banks held about 12% of U.S. banking assets. Blue Ridge Bank must adapt to evolving priorities at the OCC, FDIC, Federal Reserve and CFPB, which shift compliance budgets, product design and risk appetites. Proactive regulatory engagement reduces operational disruption.

Community banking policy support

Federal and state initiatives aim to preserve community banking and small-business credit access by supporting lenders through programs such as SBA guarantees and SSBCI; SBA 7(a) guarantees can cover up to 85% of a loan and SSBCI was funded at about 10 billion dollars. Accessing these programs can boost yield and lower loss severity by shifting credit risk to guarantees and incentives. Political commitment to these supports can wax and wane.

Geopolitical and macro stability

Global tensions raise funding costs and market volatility, with US federal funds at 5.25–5.50% (July 2025) and the 10-year Treasury near 4.3%, elevating term funding and hedging expenses for banks. Regional banks like Blue Ridge feel spillovers via deposit shifts and marked-to-market securities losses. Political stability reduces risk premia and supports lending confidence. Strong contingency planning preserves liquidity resilience.

Local government development priorities

Local government development priorities directly shape Blue Ridge Bank’s loan pipeline: county and municipal incentives, zoning changes, infrastructure spending and 5–20 year tax abatements drive real estate and small-business activity and can accelerate originations; strong local relationships surface early opportunities, while policy reversals or funding cuts elevate project delay risk and credit stress.

- Incentives influence deal flow

- Zoning & infrastructure steer collateral quality

- 5–20 year abatements affect borrower cash flow

- Policy reversals raise credit/default risk

Cannabis and emerging industries stance

Policy shifts, 12% assets, $10B SSBCI and higher rates press community bank compliance

Political shifts reshape supervision and compliance budgets for community banks (they held ~12% of U.S. banking assets in 2024), while federal/state programs (SSBCI ~$10B, SBA 7(a) guarantees up to 85%) and local incentives drive originations; rising rates (fed 5.25–5.50% and 10y ~4.3% in July 2025) raise funding costs and volatility. Cannabis state patchwork (20+ adult-use, 38 medical in 2025) adds BSA/AML complexity.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Regulation | 12% assets (2024) | Compliance cost, capital planning |

| Support programs | SSBCI $10B; SBA up to 85% | Lower loss severity, higher originations |

| Rates | Fed 5.25–5.50%; 10y ~4.3% | Higher funding/hedge costs |

| Cannabis | 20+ adult, 38 medical (2025) | Operational & BSA risk |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Blue Ridge Bank, with data-backed, region-specific insights to identify risks, opportunities and forward-looking strategic responses for executives, investors and advisors.

Visually segmented by PESTEL categories for immediate interpretation and easily droppable into presentations, this Blue Ridge Bank PESTLE summary speeds alignment across teams and supports focused discussions on external risks and market positioning during planning sessions.

Economic factors

Interest rate cycle and margin

Net interest margin for Blue Ridge Bank is driven by Fed policy (federal funds 5.25–5.50% as of July 2025), deposit betas and asset repricing. Rapid hikes compress securities marks and raise funding costs; cuts squeeze asset yields. Balance-sheet hedging and mix management are key, with scenario analyses guiding pricing discipline.

Regional economic health

Regional employment strength and modest population growth support loan demand for Blue Ridge Bank; U.S. unemployment averaged 3.7% in 2024 and local labor markets in the Mid-Atlantic showed near-national growth, boosting retail and mortgage originations. Rising small-business formation (over 4 million applications nationwide in 2023–24) fuels CRE and commercial lending but concentrations in CRE or single industries raise cyclicality. Diversifying sector exposure and early delinquency monitoring cut loss severity and stabilize earnings.

Yield curve shape

An inverted 2s10s curve (about -60 bps at its 2023–24 trough) compresses spread banking at Blue Ridge and forces deposit-rate competition, pressuring NIM and liquidity costs. A 2025 partial steepening (~+30–40 bps YTD) can revive NIM but increases reinvestment risk as short rates remain elevated. Securities duration choices drive OCI volatility and regulatory capital swings, so dynamic ALM stress-testing and hedge optimization are essential.

Liquidity and deposit competition

Fintechs and large banks have bid up deposit rates amid a higher-rate regime (federal funds roughly 5.25%), pressuring Blue Ridge Bank's community-bank funding costs. Relationship banking and treasury services help defend core deposits through deeper client engagement. Brokered and wholesale funding add flexibility but raise cost and regulatory scrutiny. Pricing analytics optimize retention and margin.

- Higher-rate pressure — competitor bids ↑

- Defense — relationship banking & treasury services

- Supplement — brokered/wholesale funding (flexible but costlier)

- Optimize — pricing analytics for retention

Credit cycle and underwriting

Tighter financial conditions, with the federal funds rate near 5.25% in 2024–25, have exposed borrower stress in CRE and SMBs; Blue Ridge Bank mitigates this via prudent LTVs, covenants and sector limits to reduce tail risk, while countercyclical provisioning bolsters loss absorption and data-driven monitoring accelerates targeted interventions.

- CRE/SMB stress: heightened by higher rates

- Risk controls: conservative LTVs, covenants, sector caps

- Resilience: countercyclical reserves

- Early action: data-driven monitoring

Policy shifts, 12% assets, $10B SSBCI and higher rates press community bank compliance

NIM driven by Fed policy (federal funds 5.25–5.50% Jul 2025), deposit betas and asset repricing; hedging and mix management essential.

Regional job growth (US unemployment 3.7% 2024) supports loan demand; CRE/SMB stress elevated under higher rates.

2s10s inverted ≈-60bps (2023–24); 2025 YTD steepening +30–40bps; deposit competition lifts funding costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| Unemployment | 3.7% (2024) |

| 2s10s | -60bps trough; +30–40bps YTD 2025 |

Preview the Actual Deliverable

Blue Ridge Bank PESTLE Analysis

The Blue Ridge Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure. No placeholders or teasers; this is the final file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, regional economic trends, and emerging fintech threats are shaping Blue Ridge Bank’s outlook in our concise PESTLE snapshot—essential reading for investors and strategists. This analysis highlights immediate risks and growth levers so you can make faster, smarter decisions. Purchase the full PESTLE report to access detailed evidence, actionable recommendations, and editable charts for boardroom-ready use.

Political factors

Regulatory oversight shifts

Changes in U.S. banking policy under different administrations can tighten or loosen supervision for community banks; in 2024 community banks held about 12% of U.S. banking assets. Blue Ridge Bank must adapt to evolving priorities at the OCC, FDIC, Federal Reserve and CFPB, which shift compliance budgets, product design and risk appetites. Proactive regulatory engagement reduces operational disruption.

Community banking policy support

Federal and state initiatives aim to preserve community banking and small-business credit access by supporting lenders through programs such as SBA guarantees and SSBCI; SBA 7(a) guarantees can cover up to 85% of a loan and SSBCI was funded at about 10 billion dollars. Accessing these programs can boost yield and lower loss severity by shifting credit risk to guarantees and incentives. Political commitment to these supports can wax and wane.

Geopolitical and macro stability

Global tensions raise funding costs and market volatility, with US federal funds at 5.25–5.50% (July 2025) and the 10-year Treasury near 4.3%, elevating term funding and hedging expenses for banks. Regional banks like Blue Ridge feel spillovers via deposit shifts and marked-to-market securities losses. Political stability reduces risk premia and supports lending confidence. Strong contingency planning preserves liquidity resilience.

Local government development priorities

Local government development priorities directly shape Blue Ridge Bank’s loan pipeline: county and municipal incentives, zoning changes, infrastructure spending and 5–20 year tax abatements drive real estate and small-business activity and can accelerate originations; strong local relationships surface early opportunities, while policy reversals or funding cuts elevate project delay risk and credit stress.

- Incentives influence deal flow

- Zoning & infrastructure steer collateral quality

- 5–20 year abatements affect borrower cash flow

- Policy reversals raise credit/default risk

Cannabis and emerging industries stance

Policy shifts, 12% assets, $10B SSBCI and higher rates press community bank compliance

Political shifts reshape supervision and compliance budgets for community banks (they held ~12% of U.S. banking assets in 2024), while federal/state programs (SSBCI ~$10B, SBA 7(a) guarantees up to 85%) and local incentives drive originations; rising rates (fed 5.25–5.50% and 10y ~4.3% in July 2025) raise funding costs and volatility. Cannabis state patchwork (20+ adult-use, 38 medical in 2025) adds BSA/AML complexity.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Regulation | 12% assets (2024) | Compliance cost, capital planning |

| Support programs | SSBCI $10B; SBA up to 85% | Lower loss severity, higher originations |

| Rates | Fed 5.25–5.50%; 10y ~4.3% | Higher funding/hedge costs |

| Cannabis | 20+ adult, 38 medical (2025) | Operational & BSA risk |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Blue Ridge Bank, with data-backed, region-specific insights to identify risks, opportunities and forward-looking strategic responses for executives, investors and advisors.

Visually segmented by PESTEL categories for immediate interpretation and easily droppable into presentations, this Blue Ridge Bank PESTLE summary speeds alignment across teams and supports focused discussions on external risks and market positioning during planning sessions.

Economic factors

Interest rate cycle and margin

Net interest margin for Blue Ridge Bank is driven by Fed policy (federal funds 5.25–5.50% as of July 2025), deposit betas and asset repricing. Rapid hikes compress securities marks and raise funding costs; cuts squeeze asset yields. Balance-sheet hedging and mix management are key, with scenario analyses guiding pricing discipline.

Regional economic health

Regional employment strength and modest population growth support loan demand for Blue Ridge Bank; U.S. unemployment averaged 3.7% in 2024 and local labor markets in the Mid-Atlantic showed near-national growth, boosting retail and mortgage originations. Rising small-business formation (over 4 million applications nationwide in 2023–24) fuels CRE and commercial lending but concentrations in CRE or single industries raise cyclicality. Diversifying sector exposure and early delinquency monitoring cut loss severity and stabilize earnings.

Yield curve shape

An inverted 2s10s curve (about -60 bps at its 2023–24 trough) compresses spread banking at Blue Ridge and forces deposit-rate competition, pressuring NIM and liquidity costs. A 2025 partial steepening (~+30–40 bps YTD) can revive NIM but increases reinvestment risk as short rates remain elevated. Securities duration choices drive OCI volatility and regulatory capital swings, so dynamic ALM stress-testing and hedge optimization are essential.

Liquidity and deposit competition

Fintechs and large banks have bid up deposit rates amid a higher-rate regime (federal funds roughly 5.25%), pressuring Blue Ridge Bank's community-bank funding costs. Relationship banking and treasury services help defend core deposits through deeper client engagement. Brokered and wholesale funding add flexibility but raise cost and regulatory scrutiny. Pricing analytics optimize retention and margin.

- Higher-rate pressure — competitor bids ↑

- Defense — relationship banking & treasury services

- Supplement — brokered/wholesale funding (flexible but costlier)

- Optimize — pricing analytics for retention

Credit cycle and underwriting

Tighter financial conditions, with the federal funds rate near 5.25% in 2024–25, have exposed borrower stress in CRE and SMBs; Blue Ridge Bank mitigates this via prudent LTVs, covenants and sector limits to reduce tail risk, while countercyclical provisioning bolsters loss absorption and data-driven monitoring accelerates targeted interventions.

- CRE/SMB stress: heightened by higher rates

- Risk controls: conservative LTVs, covenants, sector caps

- Resilience: countercyclical reserves

- Early action: data-driven monitoring

Policy shifts, 12% assets, $10B SSBCI and higher rates press community bank compliance

NIM driven by Fed policy (federal funds 5.25–5.50% Jul 2025), deposit betas and asset repricing; hedging and mix management essential.

Regional job growth (US unemployment 3.7% 2024) supports loan demand; CRE/SMB stress elevated under higher rates.

2s10s inverted ≈-60bps (2023–24); 2025 YTD steepening +30–40bps; deposit competition lifts funding costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| Unemployment | 3.7% (2024) |

| 2s10s | -60bps trough; +30–40bps YTD 2025 |

Preview the Actual Deliverable

Blue Ridge Bank PESTLE Analysis

The Blue Ridge Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure. No placeholders or teasers; this is the final file available for immediate download.