BMC Software Porter's Five Forces Analysis

Don't Miss the Bigger Picture

BMC Software faces intense buyer pressure, platform competition, and growing cloud-based substitutes, while supplier influence and regulatory shifts shape strategic choices. This snapshot highlights key tensions and strategic levers. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Compute, storage and marketplace distribution from AWS (≈34% global IaaS/PaaS share in 2024), Azure (≈24%) and GCP (≈10%) give hyperscalers pricing and roadmap leverage over BMC, while egress fees (commonly up to ~$0.09/GB) and preferential partner programs materially affect cost-to-serve and margins. Multi-cloud reduces single-vendor dependency but raises engineering overhead and ops costs. Co-sell leverage with hyperscalers can offset supplier power when joint wins are large and repeatable.

Specialized tooling and data feeds

BMC's reliance on third-party telemetry, security intel and proprietary APIs creates supplier leverage because access can be gated or repriced, and 2024 vendor licensing shifts have driven double-digit integration cost increases in some enterprises. Deep, code-level integrations produce quasi-lock-in to specific suppliers, forcing costly rework if terms change. Diversifying data sources and adding abstraction layers reduces single-supplier bargaining power.

Talent and partner ecosystem

Senior engineers, AI/ML specialists and domain SMEs are scarce, with US total compensation for experienced AI engineers frequently exceeding $200,000 in 2024, increasing supplier leverage. Services partners and GSIs—many employing 400,000–750,000 staff—shape delivery capacity and go-to-market reach. Tight labor markets and 2024 wage inflation raise supplier power. Partner certifications and enablement can partially rebalance dependence by shifting delivery to certified partners.

Open-source components and licenses

Core OSS stacks cut direct licensing costs but add compliance and support risk; by 2024 roughly 90% of enterprises used OSS in production (Linux Foundation 2024), making sudden license shifts (SSPL-like) capable of rapidly changing total cost of ownership. Forking reduces vendor exposure but raises maintenance burden and headcount costs, while vendor-backed OSS (Red Hat ~ $4.4B FY24) can restore pricing power via support premiums.

- OSS adoption: 90% enterprises (2024)

- Vendor premium: Red Hat ~ $4.4B FY24

- Risk: license shifts can spike TCO quickly

- Mitigation: forking = lower vendor risk, higher maintenance

Hardware and network dependencies

Appliance, on-prem, and data center deployments depend on server, storage, and network vendors; 2024 surveys show about 60% of enterprises retained hybrid/on-prem footprints, so supplier supply-chain constraints can lengthen delivery timelines and pressure support SLAs; standardization limits supplier differentiation but availability shocks increase supplier power; hybrid options spread dependency across layers.

- 60%: enterprises with hybrid/on-prem in 2024

- Standardization: reduces supplier differentiation

- Availability shocks: raise supplier bargaining power

- Hybrid: diversifies dependency across stack

Hyperscalers 34%/24%/10%, OSS 90%, AI pay $200k+ drive pricing power

Hyperscalers (AWS 34%/Azure 24%/GCP 10% in 2024) and telemetry/security vendors hold strong pricing and roadmap leverage; egress fees and gated APIs raise costs. OSS ubiquity (90% enterprises 2024) and senior AI pay (> $200k) amplify supplier power; multi-cloud, abstraction and partner co-sell mitigate it.

| Metric | 2024 |

|---|---|

| Hyperscaler share | 34%/24%/10% |

| OSS use | 90% |

| Senior AI comp | >$200k |

What is included in the product

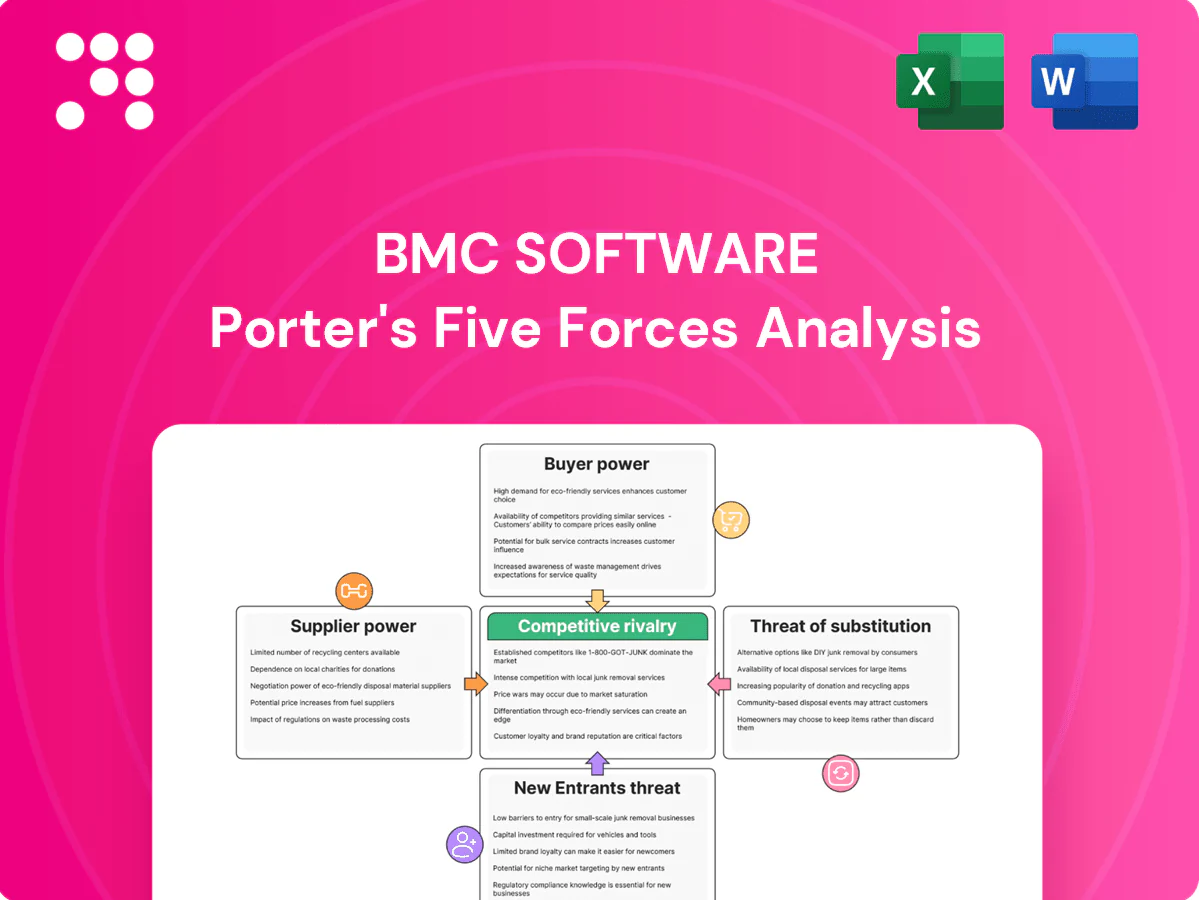

Analyzes competitive rivalry, supplier and buyer power, threat of substitutes and new entrants for BMC Software, highlighting pricing pressure, strategic barriers to entry, and marketplace dynamics; identifies emerging disruptive forces and tactical levers to defend and grow market share.

A concise, one-sheet Porter's Five Forces for BMC Software that highlights competitive pressures and actionable mitigation steps—easy to drop into decks and update as market shifts occur.

Customers Bargaining Power

Concentrated enterprise customers

Global 2000 buyers (the 2000 largest public companies) leverage RFPs, audits and bespoke contract terms to extract discounts and risk-shifting concessions. Large enterprise deal sizes, frequently exceeding $1M ARR, increase price sensitivity and negotiation leverage. Multi-year renewals hinge on measurable ROI and SLAs—customers commonly require 99.9%+ uptime and documented cost savings. Referenceability and security certifications (SOC 2, ISO 27001) serve as critical bargaining chips.

High switching costs but credible alternatives

Process integrations and data models create strong inertia, but vendors like ServiceNow (FY2024 ~$8.9B), IBM (~$60.5B) and OpenText (~$3.6B) offer migratable suites, enabling moves. Buyers exploit competitive bids to extract concessions, often securing 10–20% discounts on large enterprise deals. Professional services and migration tooling have cut migration friction by roughly 30% over recent years. Adoption of outcome-based pricing rose to about 25% of enterprise contracts in 2024, helping defend perceived value.

Demand for interoperability

Enterprises demand deep integration across DevOps, cloud and security stacks, and 80%+ of buyers now prioritize open APIs and prebuilt connectors; failure to support standards raises churn and procurement risk. Buyers insist on certified integrations and marketplace listings, with cloud marketplaces considered table stakes by most procurement teams in 2024.

Preference for flexible consumption

Customers now favor SaaS, modular SKUs and usage-based models to control spend; rigid perpetual licensing raises pushback and shelfware risk. Tiered pricing and bundling must align to customer maturity and use cases. Flexera 2024 found 69% cite cloud cost optimization as a top challenge, and FinOps-aligned transparency measurably improves retention.

- Preference: SaaS/modular/usage-based

- Risk: rigid licensing → shelfware

- Pricing: tiers map to maturity

- Retention: FinOps transparency

Service and support expectations

Regulated customers now treat premium support, compliance, and global coverage as non-negotiable, with 2024 surveys indicating roughly 60% of enterprises demand 24/7 SLAs and audit support.

SLA credits, security attestations, and audit assistance are key negotiation levers; robust CS and TAM motions create stickiness and reduce buyer power.

Poor incident response or missed SLAs materially amplifies customer leverage and churn risk.

- Support: premium, 24/7

- Compliance: attestations+audit

- Levers: SLA credits

- Defense: CS/TAM

- Risk: incident response

Buyers push outcome pricing, demand 99.9%+ uptime and deep discounts

Enterprise buyers extract 10–20% discounts on large deals (> $1M ARR), insist on 99.9%+ uptime and measurable ROI, and push outcome-based pricing (≈25% of contracts in 2024). 80%+ prioritize open APIs; 60% demand 24/7 SLAs. Strong CS/TAM and certified security reduce churn and buyer leverage.

| Metric | 2024 |

|---|---|

| Discounts | 10–20% |

| Outcome-based | 25% |

| API priority | 80%+ |

| 24/7 SLAs | 60% |

Preview the Actual Deliverable

BMC Software Porter's Five Forces Analysis

This preview shows the exact BMC Software Porter's Five Forces Analysis you'll receive—fully complete and professionally formatted. There are no placeholders or samples; the file available after purchase is identical to this preview and ready for immediate download and use. It includes supplier, buyer, threat, rivalry, and entry assessments with actionable insights.

Don't Miss the Bigger Picture

BMC Software faces intense buyer pressure, platform competition, and growing cloud-based substitutes, while supplier influence and regulatory shifts shape strategic choices. This snapshot highlights key tensions and strategic levers. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Compute, storage and marketplace distribution from AWS (≈34% global IaaS/PaaS share in 2024), Azure (≈24%) and GCP (≈10%) give hyperscalers pricing and roadmap leverage over BMC, while egress fees (commonly up to ~$0.09/GB) and preferential partner programs materially affect cost-to-serve and margins. Multi-cloud reduces single-vendor dependency but raises engineering overhead and ops costs. Co-sell leverage with hyperscalers can offset supplier power when joint wins are large and repeatable.

Specialized tooling and data feeds

BMC's reliance on third-party telemetry, security intel and proprietary APIs creates supplier leverage because access can be gated or repriced, and 2024 vendor licensing shifts have driven double-digit integration cost increases in some enterprises. Deep, code-level integrations produce quasi-lock-in to specific suppliers, forcing costly rework if terms change. Diversifying data sources and adding abstraction layers reduces single-supplier bargaining power.

Talent and partner ecosystem

Senior engineers, AI/ML specialists and domain SMEs are scarce, with US total compensation for experienced AI engineers frequently exceeding $200,000 in 2024, increasing supplier leverage. Services partners and GSIs—many employing 400,000–750,000 staff—shape delivery capacity and go-to-market reach. Tight labor markets and 2024 wage inflation raise supplier power. Partner certifications and enablement can partially rebalance dependence by shifting delivery to certified partners.

Open-source components and licenses

Core OSS stacks cut direct licensing costs but add compliance and support risk; by 2024 roughly 90% of enterprises used OSS in production (Linux Foundation 2024), making sudden license shifts (SSPL-like) capable of rapidly changing total cost of ownership. Forking reduces vendor exposure but raises maintenance burden and headcount costs, while vendor-backed OSS (Red Hat ~ $4.4B FY24) can restore pricing power via support premiums.

- OSS adoption: 90% enterprises (2024)

- Vendor premium: Red Hat ~ $4.4B FY24

- Risk: license shifts can spike TCO quickly

- Mitigation: forking = lower vendor risk, higher maintenance

Hardware and network dependencies

Appliance, on-prem, and data center deployments depend on server, storage, and network vendors; 2024 surveys show about 60% of enterprises retained hybrid/on-prem footprints, so supplier supply-chain constraints can lengthen delivery timelines and pressure support SLAs; standardization limits supplier differentiation but availability shocks increase supplier power; hybrid options spread dependency across layers.

- 60%: enterprises with hybrid/on-prem in 2024

- Standardization: reduces supplier differentiation

- Availability shocks: raise supplier bargaining power

- Hybrid: diversifies dependency across stack

Hyperscalers 34%/24%/10%, OSS 90%, AI pay $200k+ drive pricing power

Hyperscalers (AWS 34%/Azure 24%/GCP 10% in 2024) and telemetry/security vendors hold strong pricing and roadmap leverage; egress fees and gated APIs raise costs. OSS ubiquity (90% enterprises 2024) and senior AI pay (> $200k) amplify supplier power; multi-cloud, abstraction and partner co-sell mitigate it.

| Metric | 2024 |

|---|---|

| Hyperscaler share | 34%/24%/10% |

| OSS use | 90% |

| Senior AI comp | >$200k |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of substitutes and new entrants for BMC Software, highlighting pricing pressure, strategic barriers to entry, and marketplace dynamics; identifies emerging disruptive forces and tactical levers to defend and grow market share.

A concise, one-sheet Porter's Five Forces for BMC Software that highlights competitive pressures and actionable mitigation steps—easy to drop into decks and update as market shifts occur.

Customers Bargaining Power

Concentrated enterprise customers

Global 2000 buyers (the 2000 largest public companies) leverage RFPs, audits and bespoke contract terms to extract discounts and risk-shifting concessions. Large enterprise deal sizes, frequently exceeding $1M ARR, increase price sensitivity and negotiation leverage. Multi-year renewals hinge on measurable ROI and SLAs—customers commonly require 99.9%+ uptime and documented cost savings. Referenceability and security certifications (SOC 2, ISO 27001) serve as critical bargaining chips.

High switching costs but credible alternatives

Process integrations and data models create strong inertia, but vendors like ServiceNow (FY2024 ~$8.9B), IBM (~$60.5B) and OpenText (~$3.6B) offer migratable suites, enabling moves. Buyers exploit competitive bids to extract concessions, often securing 10–20% discounts on large enterprise deals. Professional services and migration tooling have cut migration friction by roughly 30% over recent years. Adoption of outcome-based pricing rose to about 25% of enterprise contracts in 2024, helping defend perceived value.

Demand for interoperability

Enterprises demand deep integration across DevOps, cloud and security stacks, and 80%+ of buyers now prioritize open APIs and prebuilt connectors; failure to support standards raises churn and procurement risk. Buyers insist on certified integrations and marketplace listings, with cloud marketplaces considered table stakes by most procurement teams in 2024.

Preference for flexible consumption

Customers now favor SaaS, modular SKUs and usage-based models to control spend; rigid perpetual licensing raises pushback and shelfware risk. Tiered pricing and bundling must align to customer maturity and use cases. Flexera 2024 found 69% cite cloud cost optimization as a top challenge, and FinOps-aligned transparency measurably improves retention.

- Preference: SaaS/modular/usage-based

- Risk: rigid licensing → shelfware

- Pricing: tiers map to maturity

- Retention: FinOps transparency

Service and support expectations

Regulated customers now treat premium support, compliance, and global coverage as non-negotiable, with 2024 surveys indicating roughly 60% of enterprises demand 24/7 SLAs and audit support.

SLA credits, security attestations, and audit assistance are key negotiation levers; robust CS and TAM motions create stickiness and reduce buyer power.

Poor incident response or missed SLAs materially amplifies customer leverage and churn risk.

- Support: premium, 24/7

- Compliance: attestations+audit

- Levers: SLA credits

- Defense: CS/TAM

- Risk: incident response

Buyers push outcome pricing, demand 99.9%+ uptime and deep discounts

Enterprise buyers extract 10–20% discounts on large deals (> $1M ARR), insist on 99.9%+ uptime and measurable ROI, and push outcome-based pricing (≈25% of contracts in 2024). 80%+ prioritize open APIs; 60% demand 24/7 SLAs. Strong CS/TAM and certified security reduce churn and buyer leverage.

| Metric | 2024 |

|---|---|

| Discounts | 10–20% |

| Outcome-based | 25% |

| API priority | 80%+ |

| 24/7 SLAs | 60% |

Preview the Actual Deliverable

BMC Software Porter's Five Forces Analysis

This preview shows the exact BMC Software Porter's Five Forces Analysis you'll receive—fully complete and professionally formatted. There are no placeholders or samples; the file available after purchase is identical to this preview and ready for immediate download and use. It includes supplier, buyer, threat, rivalry, and entry assessments with actionable insights.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

BMC Software faces intense buyer pressure, platform competition, and growing cloud-based substitutes, while supplier influence and regulatory shifts shape strategic choices. This snapshot highlights key tensions and strategic levers. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Dependence on hyperscale cloud

Compute, storage and marketplace distribution from AWS (≈34% global IaaS/PaaS share in 2024), Azure (≈24%) and GCP (≈10%) give hyperscalers pricing and roadmap leverage over BMC, while egress fees (commonly up to ~$0.09/GB) and preferential partner programs materially affect cost-to-serve and margins. Multi-cloud reduces single-vendor dependency but raises engineering overhead and ops costs. Co-sell leverage with hyperscalers can offset supplier power when joint wins are large and repeatable.

Specialized tooling and data feeds

BMC's reliance on third-party telemetry, security intel and proprietary APIs creates supplier leverage because access can be gated or repriced, and 2024 vendor licensing shifts have driven double-digit integration cost increases in some enterprises. Deep, code-level integrations produce quasi-lock-in to specific suppliers, forcing costly rework if terms change. Diversifying data sources and adding abstraction layers reduces single-supplier bargaining power.

Talent and partner ecosystem

Senior engineers, AI/ML specialists and domain SMEs are scarce, with US total compensation for experienced AI engineers frequently exceeding $200,000 in 2024, increasing supplier leverage. Services partners and GSIs—many employing 400,000–750,000 staff—shape delivery capacity and go-to-market reach. Tight labor markets and 2024 wage inflation raise supplier power. Partner certifications and enablement can partially rebalance dependence by shifting delivery to certified partners.

Open-source components and licenses

Core OSS stacks cut direct licensing costs but add compliance and support risk; by 2024 roughly 90% of enterprises used OSS in production (Linux Foundation 2024), making sudden license shifts (SSPL-like) capable of rapidly changing total cost of ownership. Forking reduces vendor exposure but raises maintenance burden and headcount costs, while vendor-backed OSS (Red Hat ~ $4.4B FY24) can restore pricing power via support premiums.

- OSS adoption: 90% enterprises (2024)

- Vendor premium: Red Hat ~ $4.4B FY24

- Risk: license shifts can spike TCO quickly

- Mitigation: forking = lower vendor risk, higher maintenance

Hardware and network dependencies

Appliance, on-prem, and data center deployments depend on server, storage, and network vendors; 2024 surveys show about 60% of enterprises retained hybrid/on-prem footprints, so supplier supply-chain constraints can lengthen delivery timelines and pressure support SLAs; standardization limits supplier differentiation but availability shocks increase supplier power; hybrid options spread dependency across layers.

- 60%: enterprises with hybrid/on-prem in 2024

- Standardization: reduces supplier differentiation

- Availability shocks: raise supplier bargaining power

- Hybrid: diversifies dependency across stack

Hyperscalers 34%/24%/10%, OSS 90%, AI pay $200k+ drive pricing power

Hyperscalers (AWS 34%/Azure 24%/GCP 10% in 2024) and telemetry/security vendors hold strong pricing and roadmap leverage; egress fees and gated APIs raise costs. OSS ubiquity (90% enterprises 2024) and senior AI pay (> $200k) amplify supplier power; multi-cloud, abstraction and partner co-sell mitigate it.

| Metric | 2024 |

|---|---|

| Hyperscaler share | 34%/24%/10% |

| OSS use | 90% |

| Senior AI comp | >$200k |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of substitutes and new entrants for BMC Software, highlighting pricing pressure, strategic barriers to entry, and marketplace dynamics; identifies emerging disruptive forces and tactical levers to defend and grow market share.

A concise, one-sheet Porter's Five Forces for BMC Software that highlights competitive pressures and actionable mitigation steps—easy to drop into decks and update as market shifts occur.

Customers Bargaining Power

Concentrated enterprise customers

Global 2000 buyers (the 2000 largest public companies) leverage RFPs, audits and bespoke contract terms to extract discounts and risk-shifting concessions. Large enterprise deal sizes, frequently exceeding $1M ARR, increase price sensitivity and negotiation leverage. Multi-year renewals hinge on measurable ROI and SLAs—customers commonly require 99.9%+ uptime and documented cost savings. Referenceability and security certifications (SOC 2, ISO 27001) serve as critical bargaining chips.

High switching costs but credible alternatives

Process integrations and data models create strong inertia, but vendors like ServiceNow (FY2024 ~$8.9B), IBM (~$60.5B) and OpenText (~$3.6B) offer migratable suites, enabling moves. Buyers exploit competitive bids to extract concessions, often securing 10–20% discounts on large enterprise deals. Professional services and migration tooling have cut migration friction by roughly 30% over recent years. Adoption of outcome-based pricing rose to about 25% of enterprise contracts in 2024, helping defend perceived value.

Demand for interoperability

Enterprises demand deep integration across DevOps, cloud and security stacks, and 80%+ of buyers now prioritize open APIs and prebuilt connectors; failure to support standards raises churn and procurement risk. Buyers insist on certified integrations and marketplace listings, with cloud marketplaces considered table stakes by most procurement teams in 2024.

Preference for flexible consumption

Customers now favor SaaS, modular SKUs and usage-based models to control spend; rigid perpetual licensing raises pushback and shelfware risk. Tiered pricing and bundling must align to customer maturity and use cases. Flexera 2024 found 69% cite cloud cost optimization as a top challenge, and FinOps-aligned transparency measurably improves retention.

- Preference: SaaS/modular/usage-based

- Risk: rigid licensing → shelfware

- Pricing: tiers map to maturity

- Retention: FinOps transparency

Service and support expectations

Regulated customers now treat premium support, compliance, and global coverage as non-negotiable, with 2024 surveys indicating roughly 60% of enterprises demand 24/7 SLAs and audit support.

SLA credits, security attestations, and audit assistance are key negotiation levers; robust CS and TAM motions create stickiness and reduce buyer power.

Poor incident response or missed SLAs materially amplifies customer leverage and churn risk.

- Support: premium, 24/7

- Compliance: attestations+audit

- Levers: SLA credits

- Defense: CS/TAM

- Risk: incident response

Buyers push outcome pricing, demand 99.9%+ uptime and deep discounts

Enterprise buyers extract 10–20% discounts on large deals (> $1M ARR), insist on 99.9%+ uptime and measurable ROI, and push outcome-based pricing (≈25% of contracts in 2024). 80%+ prioritize open APIs; 60% demand 24/7 SLAs. Strong CS/TAM and certified security reduce churn and buyer leverage.

| Metric | 2024 |

|---|---|

| Discounts | 10–20% |

| Outcome-based | 25% |

| API priority | 80%+ |

| 24/7 SLAs | 60% |

Preview the Actual Deliverable

BMC Software Porter's Five Forces Analysis

This preview shows the exact BMC Software Porter's Five Forces Analysis you'll receive—fully complete and professionally formatted. There are no placeholders or samples; the file available after purchase is identical to this preview and ready for immediate download and use. It includes supplier, buyer, threat, rivalry, and entry assessments with actionable insights.