Bayerische Motoren Werke Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Bayerische Motoren Werke faces intense rivalry from global premium automakers, rising supplier leverage for EV components, strong buyer power from fleet and retail segments, moderate threat from new entrants due to high capital needs, and growing substitute risks from mobility services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BMW’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated EV battery and chip suppliers

Advanced EV batteries are concentrated—CATL accounted for about 36% of global cell capacity in 2023–24 and the top three battery makers control roughly two‑thirds of capacity—while foundry power (TSMC >50% revenue share in 2023) and a small set of automotive chip suppliers tighten leverage. Allocation constraints and qualification rules let suppliers prioritize higher‑margin OEMs or stall lines; BMW reduces risk via multi‑sourcing and strategic supply agreements, but bargaining power stays elevated due to long lead times and complex qualification.

Premium materials and rare inputs

Premium inputs—aluminum, carbon fiber, high-grade steel and rare earths for e-motors—expose BMW to input-cost volatility and ESG sourcing constraints, strengthening supplier leverage. BMW’s purchasing scale (BMW Group delivered 2,513,972 vehicles in 2023) helps secure volumes, but specialty inputs have few substitutes. Hedging and closed-loop recycling partially offset this supplier power.

Long-term partnerships and modular platforms

Structured multi-year contracts at BMW, supporting a Group with 2023 revenues of €142.6bn, raise supply reliability and curb opportunistic pricing. Platform commonality and standardized modules (CLAR/FAAR architectures) broaden the supplier pool, reducing individual supplier leverage over time. High switching costs persist for bespoke powertrain and semiconductor components, keeping some supplier power intact.

Localization, vertical moves, and dual sourcing

Localizing production and dual sourcing in 2024 cut BMW’s reliance on single regions and suppliers, improving negotiating leverage and reducing tariff and logistics exposure. Select vertical steps, such as battery assembly partnerships, shift margin dynamics toward OEMs and increase cost transparency. These moves diversify geopolitical and supply-chain risk.

- Local production: lowers regional dependency

- Dual sourcing: reduces single-vendor risk

- Vertical moves: improves cost visibility

- Risk diversification: geopolitical & logistics

Logistics, geopolitics, and sustainability mandates

Shipping constraints and trade frictions since 2022 have increased supplier leverage for flexible logistics partners; global container congestion lifted but peak-to-peak volatility kept premium rates ~5% in 2024. Tight human-rights and carbon standards in EU law cut eligible sources, and ESG-exceeding suppliers can command 5–12% price premiums. BMW’s deep supplier audits raise switching costs, protecting brand value.

- Logistics power: flexible shippers up

- Trade friction: higher volatility, ~5% premium

- ESG premium: 5–12%

- BMW audits: higher switching costs

Supplier leverage: ~36% battery, >50% foundry dominance

Suppliers hold elevated leverage due to concentrated EV-battery (CATL ~36% global capacity 2023–24) and semiconductor foundry dominance (TSMC >50% wafer revenue 2023), long lead times and complex qualification despite BMW Group scale (2.51m vehicles, €142.6bn revenue 2023). Multi-year contracts, multi-sourcing and localizing reduce but do not eliminate supplier power.

| Metric | Value |

|---|---|

| CATL share | ~36% |

| BMW deliveries 2023 | 2,513,972 |

| BMW revenue 2023 | €142.6bn |

| TSMC revenue share | >50% |

What is included in the product

Tailored exclusively for Bayerische Motoren Werke, this analysis uncovers key drivers of competition, supplier and buyer power, threats from new entrants and substitutes, and identifies disruptive forces and market dynamics that shape BMW’s pricing power and long-term profitability.

A clear, one-sheet summary of all five forces for Bayerische Motoren Werke (BMW)—perfect for quick strategic decisions and investor briefings. Swap in your own data, adjust pressure levels for EV and regulatory shifts, and embed the spider chart into decks without macros.

Customers Bargaining Power

Brand-premium dampens price sensitivity

BMW’s strong brand and performance focus curb direct price haggling among retail buyers, reflected in its 2024 global deliveries of about 2.2 million vehicles which sustain a brand premium and reduce price sensitivity. Buyers accept higher prices for design, tech, and driving dynamics, yet online price transparency still anchors negotiations. Incentives and financing terms remain decisive in final purchase decisions.

Fleet, leasing, and financial services scale

Corporate fleets and leasing partners buy BMW in bulk—BMW Group delivered about 2.4 million vehicles in 2024—allowing discounts and tighter service terms that compress margins. BMW Financial Services, with roughly EUR 110 billion in managed receivables in 2024, shapes total cost of ownership and deal structures, increasing customers' leverage. Fleet/leasing channels exert higher bargaining power than retail, with residual value guarantees used as a primary concession and risk-sharing lever.

High configurability and online comparison

High configurability lets buyers trade price for features but complicates margin control for BMW, a risk for a firm with 2023 revenue of €142.6 billion and automotive segment margin pressure.

Ubiquitous online configurators and comparison sites increase cross-brand transparency, while clear 2024 EV incentives and running-cost calculators amplify buyer leverage.

BMW mitigates by promoting curated trims and bundled packages to simplify choices and protect margins.

Switching costs via ecosystem and services

Integrated apps, infotainment, and driver-assist familiarity create soft lock-in for BMW owners, while BMWs receive over-the-air software updates across its software-defined models since 2021, reinforcing ongoing value and reducing churn.

Certified service networks in over 150 countries and transferable warranties add convenience value; loyalty programs and OTA feature rollouts further extend stickiness and lower buyer power at renewal.

- soft-lockin: integrated apps + driver-assist

- service: certified network in 150+ countries

- stickiness: OTA updates since 2021

- renewal impact: lower buyer bargaining power

After-sales expectations and warranty pressure

Premium BMW customers demand top-tier service, rapid parts availability and same‑day repairs; in 2024 BMW delivered about 2.5 million vehicles, shifting significant post-sale leverage to buyers who expect fast warranty remedies and goodwill gestures.

BMW counters with paid service plans and data-driven Predictive Maintenance via telematics, reducing warranty costs and preserving margins.

- Service expectation: high for premium buyers

- 2024 deliveries ~2.5M

- Value shifts post-sale via warranties

- Mitigation: service plans + predictive maintenance

Premium marque holds pricing with ~2.4M cars and €110bn

BMW’s premium brand limits retail price pressure despite online transparency; 2024 Group deliveries ~2.4M sustain pricing power. Fleet/leasing buyers hold higher leverage via bulk discounts and residual guarantees; BMW Financial Services managed ~EUR 110bn receivables in 2024. High configurability raises margin risk, while OTA updates and service networks create soft lock-in and lower churn.

| Metric | 2024 |

|---|---|

| Group deliveries | ~2.4M |

| Managed receivables | EUR 110bn |

| 2023 revenue | €142.6bn |

Preview Before You Purchase

Bayerische Motoren Werke Porter's Five Forces Analysis

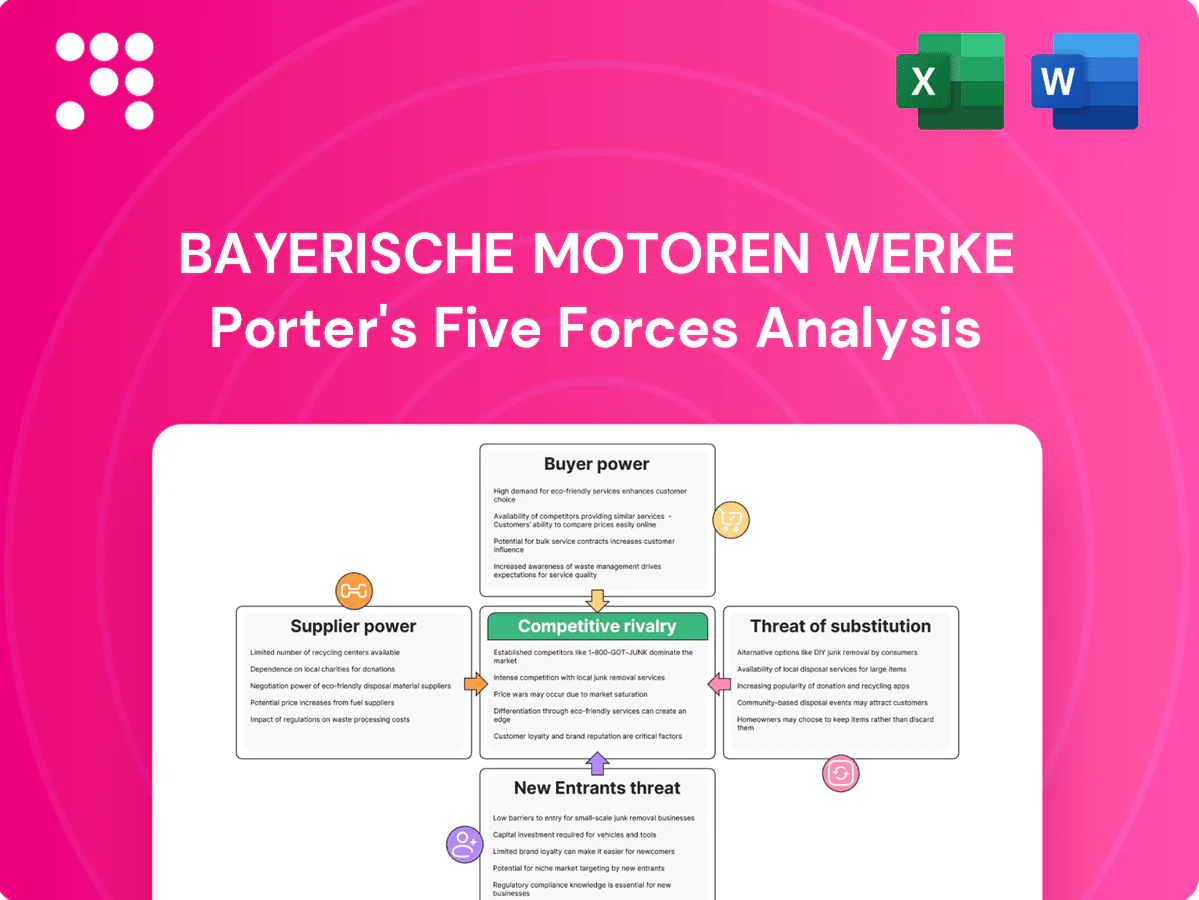

This Porter's Five Forces analysis of Bayerische Motoren Werke (BMW) assesses competitive rivalry, supplier and buyer power, and threats from new entrants and substitutes to inform strategic decisions. It highlights key industry drivers and implications for profitability. You're viewing the exact document you'll receive upon purchase—fully formatted and ready to use.

Go Beyond the Preview—Access the Full Strategic Report

Bayerische Motoren Werke faces intense rivalry from global premium automakers, rising supplier leverage for EV components, strong buyer power from fleet and retail segments, moderate threat from new entrants due to high capital needs, and growing substitute risks from mobility services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BMW’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated EV battery and chip suppliers

Advanced EV batteries are concentrated—CATL accounted for about 36% of global cell capacity in 2023–24 and the top three battery makers control roughly two‑thirds of capacity—while foundry power (TSMC >50% revenue share in 2023) and a small set of automotive chip suppliers tighten leverage. Allocation constraints and qualification rules let suppliers prioritize higher‑margin OEMs or stall lines; BMW reduces risk via multi‑sourcing and strategic supply agreements, but bargaining power stays elevated due to long lead times and complex qualification.

Premium materials and rare inputs

Premium inputs—aluminum, carbon fiber, high-grade steel and rare earths for e-motors—expose BMW to input-cost volatility and ESG sourcing constraints, strengthening supplier leverage. BMW’s purchasing scale (BMW Group delivered 2,513,972 vehicles in 2023) helps secure volumes, but specialty inputs have few substitutes. Hedging and closed-loop recycling partially offset this supplier power.

Long-term partnerships and modular platforms

Structured multi-year contracts at BMW, supporting a Group with 2023 revenues of €142.6bn, raise supply reliability and curb opportunistic pricing. Platform commonality and standardized modules (CLAR/FAAR architectures) broaden the supplier pool, reducing individual supplier leverage over time. High switching costs persist for bespoke powertrain and semiconductor components, keeping some supplier power intact.

Localization, vertical moves, and dual sourcing

Localizing production and dual sourcing in 2024 cut BMW’s reliance on single regions and suppliers, improving negotiating leverage and reducing tariff and logistics exposure. Select vertical steps, such as battery assembly partnerships, shift margin dynamics toward OEMs and increase cost transparency. These moves diversify geopolitical and supply-chain risk.

- Local production: lowers regional dependency

- Dual sourcing: reduces single-vendor risk

- Vertical moves: improves cost visibility

- Risk diversification: geopolitical & logistics

Logistics, geopolitics, and sustainability mandates

Shipping constraints and trade frictions since 2022 have increased supplier leverage for flexible logistics partners; global container congestion lifted but peak-to-peak volatility kept premium rates ~5% in 2024. Tight human-rights and carbon standards in EU law cut eligible sources, and ESG-exceeding suppliers can command 5–12% price premiums. BMW’s deep supplier audits raise switching costs, protecting brand value.

- Logistics power: flexible shippers up

- Trade friction: higher volatility, ~5% premium

- ESG premium: 5–12%

- BMW audits: higher switching costs

Supplier leverage: ~36% battery, >50% foundry dominance

Suppliers hold elevated leverage due to concentrated EV-battery (CATL ~36% global capacity 2023–24) and semiconductor foundry dominance (TSMC >50% wafer revenue 2023), long lead times and complex qualification despite BMW Group scale (2.51m vehicles, €142.6bn revenue 2023). Multi-year contracts, multi-sourcing and localizing reduce but do not eliminate supplier power.

| Metric | Value |

|---|---|

| CATL share | ~36% |

| BMW deliveries 2023 | 2,513,972 |

| BMW revenue 2023 | €142.6bn |

| TSMC revenue share | >50% |

What is included in the product

Tailored exclusively for Bayerische Motoren Werke, this analysis uncovers key drivers of competition, supplier and buyer power, threats from new entrants and substitutes, and identifies disruptive forces and market dynamics that shape BMW’s pricing power and long-term profitability.

A clear, one-sheet summary of all five forces for Bayerische Motoren Werke (BMW)—perfect for quick strategic decisions and investor briefings. Swap in your own data, adjust pressure levels for EV and regulatory shifts, and embed the spider chart into decks without macros.

Customers Bargaining Power

Brand-premium dampens price sensitivity

BMW’s strong brand and performance focus curb direct price haggling among retail buyers, reflected in its 2024 global deliveries of about 2.2 million vehicles which sustain a brand premium and reduce price sensitivity. Buyers accept higher prices for design, tech, and driving dynamics, yet online price transparency still anchors negotiations. Incentives and financing terms remain decisive in final purchase decisions.

Fleet, leasing, and financial services scale

Corporate fleets and leasing partners buy BMW in bulk—BMW Group delivered about 2.4 million vehicles in 2024—allowing discounts and tighter service terms that compress margins. BMW Financial Services, with roughly EUR 110 billion in managed receivables in 2024, shapes total cost of ownership and deal structures, increasing customers' leverage. Fleet/leasing channels exert higher bargaining power than retail, with residual value guarantees used as a primary concession and risk-sharing lever.

High configurability and online comparison

High configurability lets buyers trade price for features but complicates margin control for BMW, a risk for a firm with 2023 revenue of €142.6 billion and automotive segment margin pressure.

Ubiquitous online configurators and comparison sites increase cross-brand transparency, while clear 2024 EV incentives and running-cost calculators amplify buyer leverage.

BMW mitigates by promoting curated trims and bundled packages to simplify choices and protect margins.

Switching costs via ecosystem and services

Integrated apps, infotainment, and driver-assist familiarity create soft lock-in for BMW owners, while BMWs receive over-the-air software updates across its software-defined models since 2021, reinforcing ongoing value and reducing churn.

Certified service networks in over 150 countries and transferable warranties add convenience value; loyalty programs and OTA feature rollouts further extend stickiness and lower buyer power at renewal.

- soft-lockin: integrated apps + driver-assist

- service: certified network in 150+ countries

- stickiness: OTA updates since 2021

- renewal impact: lower buyer bargaining power

After-sales expectations and warranty pressure

Premium BMW customers demand top-tier service, rapid parts availability and same‑day repairs; in 2024 BMW delivered about 2.5 million vehicles, shifting significant post-sale leverage to buyers who expect fast warranty remedies and goodwill gestures.

BMW counters with paid service plans and data-driven Predictive Maintenance via telematics, reducing warranty costs and preserving margins.

- Service expectation: high for premium buyers

- 2024 deliveries ~2.5M

- Value shifts post-sale via warranties

- Mitigation: service plans + predictive maintenance

Premium marque holds pricing with ~2.4M cars and €110bn

BMW’s premium brand limits retail price pressure despite online transparency; 2024 Group deliveries ~2.4M sustain pricing power. Fleet/leasing buyers hold higher leverage via bulk discounts and residual guarantees; BMW Financial Services managed ~EUR 110bn receivables in 2024. High configurability raises margin risk, while OTA updates and service networks create soft lock-in and lower churn.

| Metric | 2024 |

|---|---|

| Group deliveries | ~2.4M |

| Managed receivables | EUR 110bn |

| 2023 revenue | €142.6bn |

Preview Before You Purchase

Bayerische Motoren Werke Porter's Five Forces Analysis

This Porter's Five Forces analysis of Bayerische Motoren Werke (BMW) assesses competitive rivalry, supplier and buyer power, and threats from new entrants and substitutes to inform strategic decisions. It highlights key industry drivers and implications for profitability. You're viewing the exact document you'll receive upon purchase—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Bayerische Motoren Werke faces intense rivalry from global premium automakers, rising supplier leverage for EV components, strong buyer power from fleet and retail segments, moderate threat from new entrants due to high capital needs, and growing substitute risks from mobility services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BMW’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated EV battery and chip suppliers

Advanced EV batteries are concentrated—CATL accounted for about 36% of global cell capacity in 2023–24 and the top three battery makers control roughly two‑thirds of capacity—while foundry power (TSMC >50% revenue share in 2023) and a small set of automotive chip suppliers tighten leverage. Allocation constraints and qualification rules let suppliers prioritize higher‑margin OEMs or stall lines; BMW reduces risk via multi‑sourcing and strategic supply agreements, but bargaining power stays elevated due to long lead times and complex qualification.

Premium materials and rare inputs

Premium inputs—aluminum, carbon fiber, high-grade steel and rare earths for e-motors—expose BMW to input-cost volatility and ESG sourcing constraints, strengthening supplier leverage. BMW’s purchasing scale (BMW Group delivered 2,513,972 vehicles in 2023) helps secure volumes, but specialty inputs have few substitutes. Hedging and closed-loop recycling partially offset this supplier power.

Long-term partnerships and modular platforms

Structured multi-year contracts at BMW, supporting a Group with 2023 revenues of €142.6bn, raise supply reliability and curb opportunistic pricing. Platform commonality and standardized modules (CLAR/FAAR architectures) broaden the supplier pool, reducing individual supplier leverage over time. High switching costs persist for bespoke powertrain and semiconductor components, keeping some supplier power intact.

Localization, vertical moves, and dual sourcing

Localizing production and dual sourcing in 2024 cut BMW’s reliance on single regions and suppliers, improving negotiating leverage and reducing tariff and logistics exposure. Select vertical steps, such as battery assembly partnerships, shift margin dynamics toward OEMs and increase cost transparency. These moves diversify geopolitical and supply-chain risk.

- Local production: lowers regional dependency

- Dual sourcing: reduces single-vendor risk

- Vertical moves: improves cost visibility

- Risk diversification: geopolitical & logistics

Logistics, geopolitics, and sustainability mandates

Shipping constraints and trade frictions since 2022 have increased supplier leverage for flexible logistics partners; global container congestion lifted but peak-to-peak volatility kept premium rates ~5% in 2024. Tight human-rights and carbon standards in EU law cut eligible sources, and ESG-exceeding suppliers can command 5–12% price premiums. BMW’s deep supplier audits raise switching costs, protecting brand value.

- Logistics power: flexible shippers up

- Trade friction: higher volatility, ~5% premium

- ESG premium: 5–12%

- BMW audits: higher switching costs

Supplier leverage: ~36% battery, >50% foundry dominance

Suppliers hold elevated leverage due to concentrated EV-battery (CATL ~36% global capacity 2023–24) and semiconductor foundry dominance (TSMC >50% wafer revenue 2023), long lead times and complex qualification despite BMW Group scale (2.51m vehicles, €142.6bn revenue 2023). Multi-year contracts, multi-sourcing and localizing reduce but do not eliminate supplier power.

| Metric | Value |

|---|---|

| CATL share | ~36% |

| BMW deliveries 2023 | 2,513,972 |

| BMW revenue 2023 | €142.6bn |

| TSMC revenue share | >50% |

What is included in the product

Tailored exclusively for Bayerische Motoren Werke, this analysis uncovers key drivers of competition, supplier and buyer power, threats from new entrants and substitutes, and identifies disruptive forces and market dynamics that shape BMW’s pricing power and long-term profitability.

A clear, one-sheet summary of all five forces for Bayerische Motoren Werke (BMW)—perfect for quick strategic decisions and investor briefings. Swap in your own data, adjust pressure levels for EV and regulatory shifts, and embed the spider chart into decks without macros.

Customers Bargaining Power

Brand-premium dampens price sensitivity

BMW’s strong brand and performance focus curb direct price haggling among retail buyers, reflected in its 2024 global deliveries of about 2.2 million vehicles which sustain a brand premium and reduce price sensitivity. Buyers accept higher prices for design, tech, and driving dynamics, yet online price transparency still anchors negotiations. Incentives and financing terms remain decisive in final purchase decisions.

Fleet, leasing, and financial services scale

Corporate fleets and leasing partners buy BMW in bulk—BMW Group delivered about 2.4 million vehicles in 2024—allowing discounts and tighter service terms that compress margins. BMW Financial Services, with roughly EUR 110 billion in managed receivables in 2024, shapes total cost of ownership and deal structures, increasing customers' leverage. Fleet/leasing channels exert higher bargaining power than retail, with residual value guarantees used as a primary concession and risk-sharing lever.

High configurability and online comparison

High configurability lets buyers trade price for features but complicates margin control for BMW, a risk for a firm with 2023 revenue of €142.6 billion and automotive segment margin pressure.

Ubiquitous online configurators and comparison sites increase cross-brand transparency, while clear 2024 EV incentives and running-cost calculators amplify buyer leverage.

BMW mitigates by promoting curated trims and bundled packages to simplify choices and protect margins.

Switching costs via ecosystem and services

Integrated apps, infotainment, and driver-assist familiarity create soft lock-in for BMW owners, while BMWs receive over-the-air software updates across its software-defined models since 2021, reinforcing ongoing value and reducing churn.

Certified service networks in over 150 countries and transferable warranties add convenience value; loyalty programs and OTA feature rollouts further extend stickiness and lower buyer power at renewal.

- soft-lockin: integrated apps + driver-assist

- service: certified network in 150+ countries

- stickiness: OTA updates since 2021

- renewal impact: lower buyer bargaining power

After-sales expectations and warranty pressure

Premium BMW customers demand top-tier service, rapid parts availability and same‑day repairs; in 2024 BMW delivered about 2.5 million vehicles, shifting significant post-sale leverage to buyers who expect fast warranty remedies and goodwill gestures.

BMW counters with paid service plans and data-driven Predictive Maintenance via telematics, reducing warranty costs and preserving margins.

- Service expectation: high for premium buyers

- 2024 deliveries ~2.5M

- Value shifts post-sale via warranties

- Mitigation: service plans + predictive maintenance

Premium marque holds pricing with ~2.4M cars and €110bn

BMW’s premium brand limits retail price pressure despite online transparency; 2024 Group deliveries ~2.4M sustain pricing power. Fleet/leasing buyers hold higher leverage via bulk discounts and residual guarantees; BMW Financial Services managed ~EUR 110bn receivables in 2024. High configurability raises margin risk, while OTA updates and service networks create soft lock-in and lower churn.

| Metric | 2024 |

|---|---|

| Group deliveries | ~2.4M |

| Managed receivables | EUR 110bn |

| 2023 revenue | €142.6bn |

Preview Before You Purchase

Bayerische Motoren Werke Porter's Five Forces Analysis

This Porter's Five Forces analysis of Bayerische Motoren Werke (BMW) assesses competitive rivalry, supplier and buyer power, and threats from new entrants and substitutes to inform strategic decisions. It highlights key industry drivers and implications for profitability. You're viewing the exact document you'll receive upon purchase—fully formatted and ready to use.