Boeing Boston Consulting Group Matrix

See the Bigger Picture

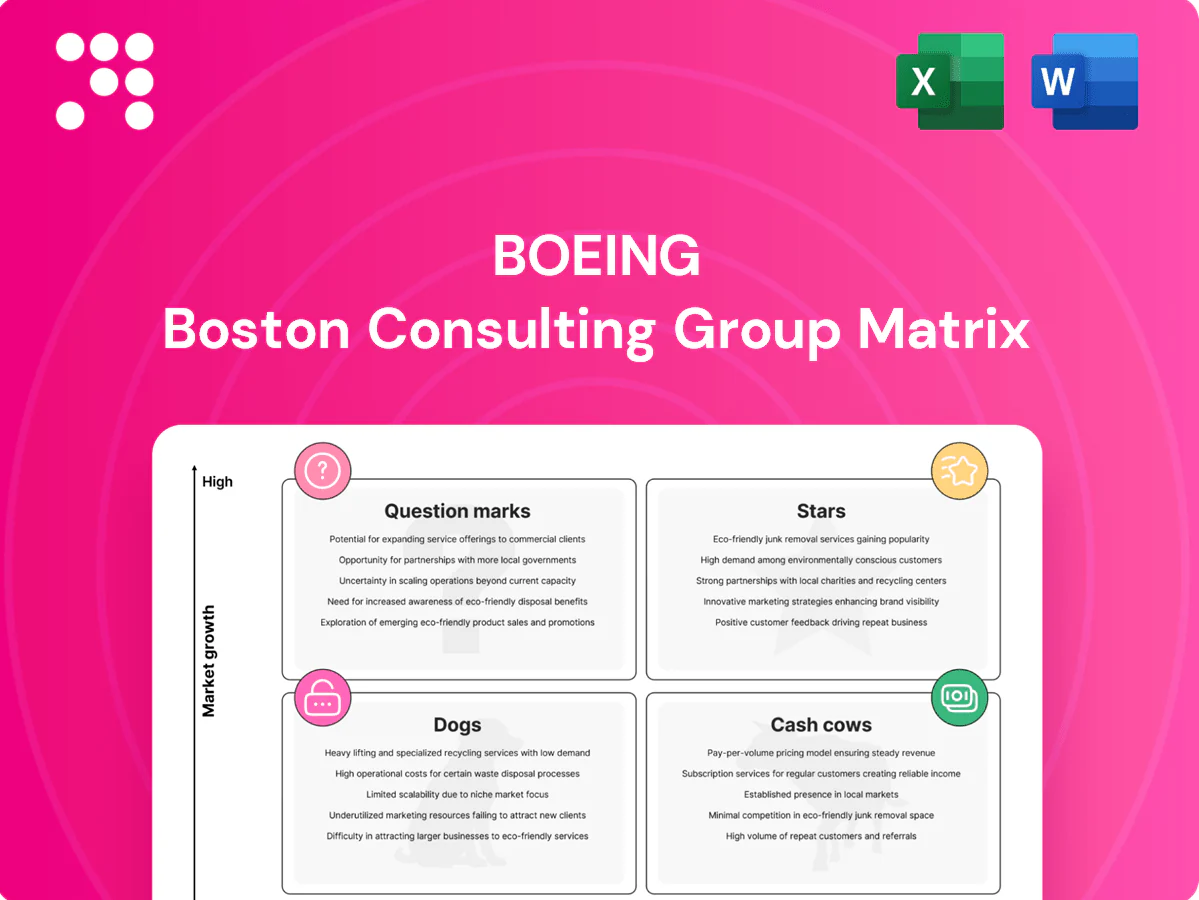

Boeing’s BCG Matrix preview shows which aircraft lines are flying high and which are draining cash—think Stars, Cash Cows, Question Marks, and Dogs mapped to real-market signals. This snapshot hints at where to double down, cut losses, or pivot—but the full report gives quadrant-by-quadrant data, strategic moves, and ready-to-use Word and Excel files. Purchase the complete BCG Matrix for a clear, actionable roadmap you can present and act on today.

Stars

787 Dreamliner program

Widebody demand is rebounding (IATA: long‑haul traffic ~85% of 2019 in 2024), and the 787 benefits from an installed base >1,000 and a hefty backlog (~700 undelivered), keeping strong airline interest. Its long‑range fuel efficiency (~20% better per seat vs older widebodies) drives repeat orders as growth returns. The program still consumes cash for rate increases and supplier stabilization (billions in incremental costs), but the growth tailwind is real; hold share and it should mature into a steadier earner.

737 MAX family recovery

Single-aisle is the fastest-growing segment (≈70% of long‑term demand) and Boeing’s 737 MAX remains a major contender with over 3,000 MAX units still on backlog at end‑2024, keeping a robust delivery pipeline. Ongoing investment in quality, recertification and customer support is essential. If Boeing nails execution, the MAX franchise can compound into a dominant cash generator.

Freighter portfolio (777F/767F + BCFs)

E‑commerce and resilient cargo flows kept freighter demand strong in 2024—global e‑commerce ~6.3 trillion USD and air cargo CTKs up mid single digits—while Boeing holds the lion’s share of large freighters (~70–80% of the widebody freighter fleet). Factory 777F/767F output plus BCF conversion lines provide flexibility and scale, but growth needs continued slot allocation and partner conversion capacity. Strong market share in a growing niche equals classic Star behavior.

P‑8 Poseidon maritime patrol

Boeing P‑8 Poseidon is the category leader in maritime patrol, adopted by more than a dozen countries as of 2024 and anchored by the US Navy as the primary operator. Rising maritime ISR priorities and expanding allied defense budgets drove new orders and upgrade contracts in 2024, keeping the line hot. High share in a growing mission set with ongoing capability refresh programs fits the Star profile.

- Adopted by >12 countries (2024)

- Ongoing USN procurements and international orders/upgrades in 2024

- Leads maritime ISR market share

- Requires continual capability refresh to retain advantage

Global Services growth engines

Global Services growth engines track rising aircraft utilization: line maintenance, mods and digital ops expanded with fleet flying hours up ~8% in 2024, driving Global Services revenue +9% to $14.2B and higher aftermarket demand. Boeing’s cross-fleet data, parts distribution and 700+ MRO locations create customer stickiness, though investments in tooling, faster turn-times and cloud-native digital platforms remain required to capture lifetime value.

- Fleet utilization +8% (2024)

- Global Services revenue +9% to $14.2B (2024)

- 700+ MRO sites = distribution scale

- Priorities: tooling, turn-times, digital platforms

Backlog power: widebody ~700, single-aisle >3,000; freighters 70–80%, services $14.2B

Widebody 787 (backlog ~700) and 737 MAX (backlog >3,000 end‑2024) plus freighters (70–80% share) and P‑8 (>12 nations) are Boeing Stars: high share in growing segments with strong demand—long‑haul ~85% of 2019 (2024) and services revenue +9% to $14.2B. Execution and supplier/capex drain remain key to convert growth into cash.

| Asset | 2024 metric |

|---|---|

| 787 backlog | ~700 |

| 737 MAX backlog | >3,000 |

| Freighter share | 70–80% |

| Global Services | $14.2B (+9%) |

What is included in the product

BCG analysis of Boeing's units—maps Stars, Cash Cows, Question Marks, Dogs and recommends invest, hold or divest.

One-page Boeing BCG Matrix clarifying portfolio choices to cut complexity and guide strategic investment.

Cash Cows

Aftermarket parts and distribution

Aftermarket parts and distribution are mature, recurring, margin-rich businesses—every flight cycle consumes parts and Boeing supports over 25,000 commercial aircraft in service globally. Boeing’s catalog and logistics network generate steady cashflow and high spare-parts margins. Growth is modest (low-single digits) but utilization and fleet flying hours keep revenues consistent. Maintain parts availability and pricing discipline to preserve cash generation.

Legacy platform sustainment (737NG, 747, 767)

Legacy-platform sustainment for 737NG, 747 and 767 supports thousands of in‑service frames, with 747 production having ended in 2022 but global fleets needing support through 2024 and beyond. Demand is low‑growth yet reliable, yielding higher aftermarket margins versus new deliveries. Investments focus on efficiency and inventory turns to reduce cost-to-serve. Cash flows from these services fund Boeing’s heavier R&D and new-program bets.

Defense sustainment and upgrades

Once fielded, Boeing defense platforms generate predictable, sticky sustainment revenues—aftermarket services and depot work delivered double-digit margins and a defense backlog exceeding $50 billion in 2024. Upgrades and depot contracts face limited competition, yielding attractive returns; market growth is modest (low single digits) but backlog depth supports stable cash flow. Optimizing contract terms and on-time delivery enhances cash conversion and margins.

Training and simulation services

Pilot and crew training is required, recurring, and scalable for Boeing’s services; margins rise with higher simulator utilization and software-based course content. Growth is steady—Boeing’s 2024 Pilot and Technician Outlook projects roughly 612,000 new pilots needed through 2043—so training remains a predictable cash cow rather than an explosive growth segment.

- Required recurring revenue

- Higher utilization = better margins

- Software upsells scale profitably

- 2024 demand supports steady throughput

Global Services time-and-materials MRO

Line and base maintenance on mature fleets within Boeing Global Services generate steady cash flow, with line/base MRO typically delivering mid-single-digit to low-double-digit operating margins; 2024 industry MRO spend was roughly $88 billion, supporting predictable revenues. Competition exists, but high switching costs and operator proximity sustain pricing power. Low-to-moderate market growth means efficiency — turnaround time and labor productivity — drives yield improvement.

- Steady cash: dependable repeat work from mature fleets

- Competitive moat: switching costs + proximity

- Growth: low–moderate; efficiency-led

- Key KPIs: turnaround time, labor productivity, shop utilization

Cash-first aero services: tighten pricing, boost availability, lift FCF

Aftermarket parts, legacy sustainment, defense depot work and training are mature, high-margin cash cows supporting Boeing’s core cash generation. Boeing supports ~25,000 commercial aircraft in service; 2024 defense backlog >$50B; 2024 industry MRO spend ~$88B; Pilot/tech demand ~612,000 through 2043. Focus: availability, pricing discipline, inventory turns and utilization to maximize free cash flow.

| Segment | 2024 Metric | Margin/Notes |

|---|---|---|

| Aftermarket parts | ~25,000 aircraft supported | High margins, recurring |

| Defense sustainment | Backlog >$50B | Double-digit margins |

| MRO | $88B industry spend | Mid- to low-double-digit margins |

| Training | 612,000 pilots need to 2043 | Scalable, steady margins |

What You’re Viewing Is Included

Boeing BCG Matrix

The file you're previewing is the final Boeing BCG Matrix you'll receive after purchase. No watermarks, no placeholder text—just a polished, analysis-ready matrix focused on Boeing's portfolio and market positions. It's formatted for easy editing, printing, and slide-ready use. Buy once, download immediately—no surprises. Ready to plug into strategy meetings or investor decks.

See the Bigger Picture

Boeing’s BCG Matrix preview shows which aircraft lines are flying high and which are draining cash—think Stars, Cash Cows, Question Marks, and Dogs mapped to real-market signals. This snapshot hints at where to double down, cut losses, or pivot—but the full report gives quadrant-by-quadrant data, strategic moves, and ready-to-use Word and Excel files. Purchase the complete BCG Matrix for a clear, actionable roadmap you can present and act on today.

Stars

787 Dreamliner program

Widebody demand is rebounding (IATA: long‑haul traffic ~85% of 2019 in 2024), and the 787 benefits from an installed base >1,000 and a hefty backlog (~700 undelivered), keeping strong airline interest. Its long‑range fuel efficiency (~20% better per seat vs older widebodies) drives repeat orders as growth returns. The program still consumes cash for rate increases and supplier stabilization (billions in incremental costs), but the growth tailwind is real; hold share and it should mature into a steadier earner.

737 MAX family recovery

Single-aisle is the fastest-growing segment (≈70% of long‑term demand) and Boeing’s 737 MAX remains a major contender with over 3,000 MAX units still on backlog at end‑2024, keeping a robust delivery pipeline. Ongoing investment in quality, recertification and customer support is essential. If Boeing nails execution, the MAX franchise can compound into a dominant cash generator.

Freighter portfolio (777F/767F + BCFs)

E‑commerce and resilient cargo flows kept freighter demand strong in 2024—global e‑commerce ~6.3 trillion USD and air cargo CTKs up mid single digits—while Boeing holds the lion’s share of large freighters (~70–80% of the widebody freighter fleet). Factory 777F/767F output plus BCF conversion lines provide flexibility and scale, but growth needs continued slot allocation and partner conversion capacity. Strong market share in a growing niche equals classic Star behavior.

P‑8 Poseidon maritime patrol

Boeing P‑8 Poseidon is the category leader in maritime patrol, adopted by more than a dozen countries as of 2024 and anchored by the US Navy as the primary operator. Rising maritime ISR priorities and expanding allied defense budgets drove new orders and upgrade contracts in 2024, keeping the line hot. High share in a growing mission set with ongoing capability refresh programs fits the Star profile.

- Adopted by >12 countries (2024)

- Ongoing USN procurements and international orders/upgrades in 2024

- Leads maritime ISR market share

- Requires continual capability refresh to retain advantage

Global Services growth engines

Global Services growth engines track rising aircraft utilization: line maintenance, mods and digital ops expanded with fleet flying hours up ~8% in 2024, driving Global Services revenue +9% to $14.2B and higher aftermarket demand. Boeing’s cross-fleet data, parts distribution and 700+ MRO locations create customer stickiness, though investments in tooling, faster turn-times and cloud-native digital platforms remain required to capture lifetime value.

- Fleet utilization +8% (2024)

- Global Services revenue +9% to $14.2B (2024)

- 700+ MRO sites = distribution scale

- Priorities: tooling, turn-times, digital platforms

Backlog power: widebody ~700, single-aisle >3,000; freighters 70–80%, services $14.2B

Widebody 787 (backlog ~700) and 737 MAX (backlog >3,000 end‑2024) plus freighters (70–80% share) and P‑8 (>12 nations) are Boeing Stars: high share in growing segments with strong demand—long‑haul ~85% of 2019 (2024) and services revenue +9% to $14.2B. Execution and supplier/capex drain remain key to convert growth into cash.

| Asset | 2024 metric |

|---|---|

| 787 backlog | ~700 |

| 737 MAX backlog | >3,000 |

| Freighter share | 70–80% |

| Global Services | $14.2B (+9%) |

What is included in the product

BCG analysis of Boeing's units—maps Stars, Cash Cows, Question Marks, Dogs and recommends invest, hold or divest.

One-page Boeing BCG Matrix clarifying portfolio choices to cut complexity and guide strategic investment.

Cash Cows

Aftermarket parts and distribution

Aftermarket parts and distribution are mature, recurring, margin-rich businesses—every flight cycle consumes parts and Boeing supports over 25,000 commercial aircraft in service globally. Boeing’s catalog and logistics network generate steady cashflow and high spare-parts margins. Growth is modest (low-single digits) but utilization and fleet flying hours keep revenues consistent. Maintain parts availability and pricing discipline to preserve cash generation.

Legacy platform sustainment (737NG, 747, 767)

Legacy-platform sustainment for 737NG, 747 and 767 supports thousands of in‑service frames, with 747 production having ended in 2022 but global fleets needing support through 2024 and beyond. Demand is low‑growth yet reliable, yielding higher aftermarket margins versus new deliveries. Investments focus on efficiency and inventory turns to reduce cost-to-serve. Cash flows from these services fund Boeing’s heavier R&D and new-program bets.

Defense sustainment and upgrades

Once fielded, Boeing defense platforms generate predictable, sticky sustainment revenues—aftermarket services and depot work delivered double-digit margins and a defense backlog exceeding $50 billion in 2024. Upgrades and depot contracts face limited competition, yielding attractive returns; market growth is modest (low single digits) but backlog depth supports stable cash flow. Optimizing contract terms and on-time delivery enhances cash conversion and margins.

Training and simulation services

Pilot and crew training is required, recurring, and scalable for Boeing’s services; margins rise with higher simulator utilization and software-based course content. Growth is steady—Boeing’s 2024 Pilot and Technician Outlook projects roughly 612,000 new pilots needed through 2043—so training remains a predictable cash cow rather than an explosive growth segment.

- Required recurring revenue

- Higher utilization = better margins

- Software upsells scale profitably

- 2024 demand supports steady throughput

Global Services time-and-materials MRO

Line and base maintenance on mature fleets within Boeing Global Services generate steady cash flow, with line/base MRO typically delivering mid-single-digit to low-double-digit operating margins; 2024 industry MRO spend was roughly $88 billion, supporting predictable revenues. Competition exists, but high switching costs and operator proximity sustain pricing power. Low-to-moderate market growth means efficiency — turnaround time and labor productivity — drives yield improvement.

- Steady cash: dependable repeat work from mature fleets

- Competitive moat: switching costs + proximity

- Growth: low–moderate; efficiency-led

- Key KPIs: turnaround time, labor productivity, shop utilization

Cash-first aero services: tighten pricing, boost availability, lift FCF

Aftermarket parts, legacy sustainment, defense depot work and training are mature, high-margin cash cows supporting Boeing’s core cash generation. Boeing supports ~25,000 commercial aircraft in service; 2024 defense backlog >$50B; 2024 industry MRO spend ~$88B; Pilot/tech demand ~612,000 through 2043. Focus: availability, pricing discipline, inventory turns and utilization to maximize free cash flow.

| Segment | 2024 Metric | Margin/Notes |

|---|---|---|

| Aftermarket parts | ~25,000 aircraft supported | High margins, recurring |

| Defense sustainment | Backlog >$50B | Double-digit margins |

| MRO | $88B industry spend | Mid- to low-double-digit margins |

| Training | 612,000 pilots need to 2043 | Scalable, steady margins |

What You’re Viewing Is Included

Boeing BCG Matrix

The file you're previewing is the final Boeing BCG Matrix you'll receive after purchase. No watermarks, no placeholder text—just a polished, analysis-ready matrix focused on Boeing's portfolio and market positions. It's formatted for easy editing, printing, and slide-ready use. Buy once, download immediately—no surprises. Ready to plug into strategy meetings or investor decks.

Description

See the Bigger Picture

Boeing’s BCG Matrix preview shows which aircraft lines are flying high and which are draining cash—think Stars, Cash Cows, Question Marks, and Dogs mapped to real-market signals. This snapshot hints at where to double down, cut losses, or pivot—but the full report gives quadrant-by-quadrant data, strategic moves, and ready-to-use Word and Excel files. Purchase the complete BCG Matrix for a clear, actionable roadmap you can present and act on today.

Stars

787 Dreamliner program

Widebody demand is rebounding (IATA: long‑haul traffic ~85% of 2019 in 2024), and the 787 benefits from an installed base >1,000 and a hefty backlog (~700 undelivered), keeping strong airline interest. Its long‑range fuel efficiency (~20% better per seat vs older widebodies) drives repeat orders as growth returns. The program still consumes cash for rate increases and supplier stabilization (billions in incremental costs), but the growth tailwind is real; hold share and it should mature into a steadier earner.

737 MAX family recovery

Single-aisle is the fastest-growing segment (≈70% of long‑term demand) and Boeing’s 737 MAX remains a major contender with over 3,000 MAX units still on backlog at end‑2024, keeping a robust delivery pipeline. Ongoing investment in quality, recertification and customer support is essential. If Boeing nails execution, the MAX franchise can compound into a dominant cash generator.

Freighter portfolio (777F/767F + BCFs)

E‑commerce and resilient cargo flows kept freighter demand strong in 2024—global e‑commerce ~6.3 trillion USD and air cargo CTKs up mid single digits—while Boeing holds the lion’s share of large freighters (~70–80% of the widebody freighter fleet). Factory 777F/767F output plus BCF conversion lines provide flexibility and scale, but growth needs continued slot allocation and partner conversion capacity. Strong market share in a growing niche equals classic Star behavior.

P‑8 Poseidon maritime patrol

Boeing P‑8 Poseidon is the category leader in maritime patrol, adopted by more than a dozen countries as of 2024 and anchored by the US Navy as the primary operator. Rising maritime ISR priorities and expanding allied defense budgets drove new orders and upgrade contracts in 2024, keeping the line hot. High share in a growing mission set with ongoing capability refresh programs fits the Star profile.

- Adopted by >12 countries (2024)

- Ongoing USN procurements and international orders/upgrades in 2024

- Leads maritime ISR market share

- Requires continual capability refresh to retain advantage

Global Services growth engines

Global Services growth engines track rising aircraft utilization: line maintenance, mods and digital ops expanded with fleet flying hours up ~8% in 2024, driving Global Services revenue +9% to $14.2B and higher aftermarket demand. Boeing’s cross-fleet data, parts distribution and 700+ MRO locations create customer stickiness, though investments in tooling, faster turn-times and cloud-native digital platforms remain required to capture lifetime value.

- Fleet utilization +8% (2024)

- Global Services revenue +9% to $14.2B (2024)

- 700+ MRO sites = distribution scale

- Priorities: tooling, turn-times, digital platforms

Backlog power: widebody ~700, single-aisle >3,000; freighters 70–80%, services $14.2B

Widebody 787 (backlog ~700) and 737 MAX (backlog >3,000 end‑2024) plus freighters (70–80% share) and P‑8 (>12 nations) are Boeing Stars: high share in growing segments with strong demand—long‑haul ~85% of 2019 (2024) and services revenue +9% to $14.2B. Execution and supplier/capex drain remain key to convert growth into cash.

| Asset | 2024 metric |

|---|---|

| 787 backlog | ~700 |

| 737 MAX backlog | >3,000 |

| Freighter share | 70–80% |

| Global Services | $14.2B (+9%) |

What is included in the product

BCG analysis of Boeing's units—maps Stars, Cash Cows, Question Marks, Dogs and recommends invest, hold or divest.

One-page Boeing BCG Matrix clarifying portfolio choices to cut complexity and guide strategic investment.

Cash Cows

Aftermarket parts and distribution

Aftermarket parts and distribution are mature, recurring, margin-rich businesses—every flight cycle consumes parts and Boeing supports over 25,000 commercial aircraft in service globally. Boeing’s catalog and logistics network generate steady cashflow and high spare-parts margins. Growth is modest (low-single digits) but utilization and fleet flying hours keep revenues consistent. Maintain parts availability and pricing discipline to preserve cash generation.

Legacy platform sustainment (737NG, 747, 767)

Legacy-platform sustainment for 737NG, 747 and 767 supports thousands of in‑service frames, with 747 production having ended in 2022 but global fleets needing support through 2024 and beyond. Demand is low‑growth yet reliable, yielding higher aftermarket margins versus new deliveries. Investments focus on efficiency and inventory turns to reduce cost-to-serve. Cash flows from these services fund Boeing’s heavier R&D and new-program bets.

Defense sustainment and upgrades

Once fielded, Boeing defense platforms generate predictable, sticky sustainment revenues—aftermarket services and depot work delivered double-digit margins and a defense backlog exceeding $50 billion in 2024. Upgrades and depot contracts face limited competition, yielding attractive returns; market growth is modest (low single digits) but backlog depth supports stable cash flow. Optimizing contract terms and on-time delivery enhances cash conversion and margins.

Training and simulation services

Pilot and crew training is required, recurring, and scalable for Boeing’s services; margins rise with higher simulator utilization and software-based course content. Growth is steady—Boeing’s 2024 Pilot and Technician Outlook projects roughly 612,000 new pilots needed through 2043—so training remains a predictable cash cow rather than an explosive growth segment.

- Required recurring revenue

- Higher utilization = better margins

- Software upsells scale profitably

- 2024 demand supports steady throughput

Global Services time-and-materials MRO

Line and base maintenance on mature fleets within Boeing Global Services generate steady cash flow, with line/base MRO typically delivering mid-single-digit to low-double-digit operating margins; 2024 industry MRO spend was roughly $88 billion, supporting predictable revenues. Competition exists, but high switching costs and operator proximity sustain pricing power. Low-to-moderate market growth means efficiency — turnaround time and labor productivity — drives yield improvement.

- Steady cash: dependable repeat work from mature fleets

- Competitive moat: switching costs + proximity

- Growth: low–moderate; efficiency-led

- Key KPIs: turnaround time, labor productivity, shop utilization

Cash-first aero services: tighten pricing, boost availability, lift FCF

Aftermarket parts, legacy sustainment, defense depot work and training are mature, high-margin cash cows supporting Boeing’s core cash generation. Boeing supports ~25,000 commercial aircraft in service; 2024 defense backlog >$50B; 2024 industry MRO spend ~$88B; Pilot/tech demand ~612,000 through 2043. Focus: availability, pricing discipline, inventory turns and utilization to maximize free cash flow.

| Segment | 2024 Metric | Margin/Notes |

|---|---|---|

| Aftermarket parts | ~25,000 aircraft supported | High margins, recurring |

| Defense sustainment | Backlog >$50B | Double-digit margins |

| MRO | $88B industry spend | Mid- to low-double-digit margins |

| Training | 612,000 pilots need to 2043 | Scalable, steady margins |

What You’re Viewing Is Included

Boeing BCG Matrix

The file you're previewing is the final Boeing BCG Matrix you'll receive after purchase. No watermarks, no placeholder text—just a polished, analysis-ready matrix focused on Boeing's portfolio and market positions. It's formatted for easy editing, printing, and slide-ready use. Buy once, download immediately—no surprises. Ready to plug into strategy meetings or investor decks.