Bohai Leasing Co. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

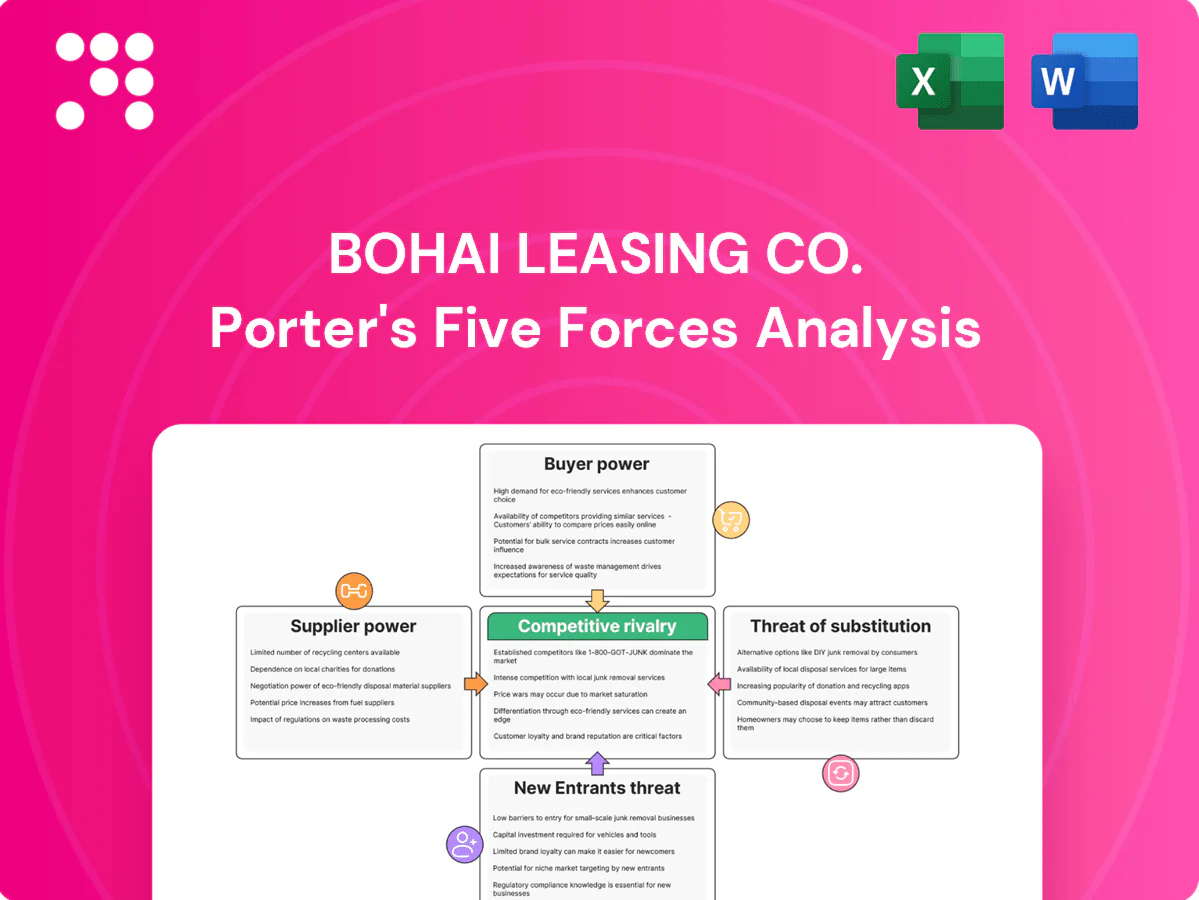

Bohai Leasing faces moderate rivalry driven by large state-backed rivals and cyclical equipment demand, while regulatory ties and financing access shape its bargaining power.

Supplier leverage is muted by diversified OEM relationships, but buyer concentration and credit risk elevate pressure on margins and contract terms.

Threats from new entrants and substitutes are limited by capital intensity and long-term contracts, yet digital financing innovations could disrupt traditional leasing models.

This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Bohai Leasing Co..

Suppliers Bargaining Power

Concentrated OEM base

Aircraft supply is dominated by a few OEMs (Airbus and Boeing hold over 80% market share), giving them pricing and delivery leverage over lessors. Large backlogs and multi-year certification timelines constrain availability and raise acquisition costs; narrowbodies represent roughly 70% of global backlog, keeping supplier power structurally elevated. Bohai must actively manage order positions and diversify models to mitigate dependence while monitoring cyclical shifts.

Capital providers’ influence

Capital providers—banks, bondholders, ABS investors and ECAs—set covenants and spreads that directly shape Bohai Leasing’s pricing and risk sharing; China's 2024 GDP growth of about 5.2% influenced funding conditions and investor risk appetite. Ratings shifts and market cycles can rapidly widen spreads, while strong liquidity ties and staggered maturities mitigate exposure. Lenders can tighten deal structures, shifting more residual risk onto the lessor.

Maintenance and MRO dependence

MRO vendors and engine shops are highly concentrated for new-generation engines: CFM LEAP and Pratt & Whitney GTF families together account for roughly 70% of narrowbody engine shop demand through 2024, squeezing independent capacity. OEM-controlled parts pricing and scarce shop slots raise lifecycle costs and turnaround times, with global commercial MRO market near $87bn (2023) and tight 2024 backlogs. Power-by-the-hour and pooled-inventory contracts materially dampen cost volatility and supply risk, but delays still erode re-leasing turnaround and residual values.

Asset scarcity cycles

Asset scarcity cycles elevate supplier power for Bohai Leasing as new-tech aircraft remain supply-constrained amid a global commercial backlog of roughly 14,000 aircraft in 2024, and with about 40% of the world fleet on lease this tightness feeds higher lease-rate sensitivity to OEM production-rate shifts; counter-cyclical purchases and sale-leaseback sourcing partially offset costs while secondary-market liquidity provides relief only at market-clearing prices.

- Supply constraint: backlog ~14,000 (2024)

- Leasing penetration: ~40% of fleet

- Mitigants: counter-cyclical buys, sale-leasebacks

- Relief: secondary market at market-clearing prices

Specialized container/equipment makers

Specialized container and high-end equipment suppliers can pass through input-cost volatility, limiting Bohai Leasing’s margin control; in 2024 the global container fleet was roughly 25 million TEU, sustaining supplier pricing leverage.

Standardization lowers differentiation, so large-scale buyers secure better terms while long-term supply frameworks and volume commitments improve Bohai’s pricing; currency and commodity swings in 2024 amplified supplier bargaining power.

- Pass-through pricing: high

- Scale advantage: strong for large lessors

- LT contracts: reduce unit cost

- Macro risks: FX/steel volatility in 2024

Dominant OEMs and MROs squeeze margins amid ~14,000-aircraft backlog

Supplier power is high: OEMs (Airbus/Boeing >80% share) and concentrated MRO/engine shops raise prices and delay deliveries amid a ~14,000-aircraft backlog (2024). Leasing penetration ~40% and tight narrowbody supply keep lease-rate sensitivity elevated; financing spreads and parts costs (global MRO ~$87bn in 2023) further constrain margins.

| Metric | 2024/2023 |

|---|---|

| Global backlog | ~14,000 (2024) |

| Leased fleet | ~40% |

| OEM share | Airbus+Boeing >80% |

| Global MRO | $87bn (2023) |

What is included in the product

Concise Porter's Five Forces assessment of Bohai Leasing Co., highlighting competitive rivalry, buyer and supplier bargaining power, threats from new entrants and substitutes, and regulatory barriers; identifies disruptive forces and strategic levers to defend margins and sustain market position.

Bohai Leasing Co. Porter's Five Forces Analysis delivers a clear one-sheet summary of competitive pressures—ideal for swift, boardroom-ready decisions—and lets you customize pressure levels to reflect new data or regulatory shifts, removing analysis bottlenecks and speeding strategic response.

Customers Bargaining Power

Large anchor clients

Major airlines, shipping lines and infrastructure operators exert strong bargaining power: the top 10 airlines operated roughly 40% of the global commercial fleet in 2024, enabling multi-asset deals and leverage over maintenance reserves; concentration risk forces larger concessions at renewal and can pressure Bohai Leasing margins, while landing marquee clients often establishes pricing benchmarks across Asia-Pacific and global markets.

Alternative financing options

Clients can bypass leasing by using bank loans, ECA-backed debt or capital markets, with China's 5-year LPR at 3.65% in 2024 making buyouts more attractive; sale-leasebacks and PDP financing further compress yields. Competition forces Bohai Leasing to compete on flexibility, transaction speed and transferring residual-value risk to preserve margins. In tighter credit cycles leasing regains appeal, reducing buyer power as corporates turn to off-balance solutions.

Contract duration and terms

Long tenors lock in asset utilization for Bohai Leasing but invite tougher negotiations on covenants and end-of-lease conditions.

Lessees increasingly push for power-by-the-hour and lower reserves in downturns, with roughly 50% of the global commercial fleet leased, boosting lessee bargaining power.

Return-condition disputes can erode economics, so balanced clauses and credit-based pricing discipline (tiered margins by lessee rating) are key.

Switching and downtime costs

Switching and reconfiguration downtime raise frictions for Bohai Leasing and customers, as aircraft redelivery can take weeks and incur maintenance and lease-end costs; buyers often press for concessions near redelivery to exploit timing. Bohai's strong remarketing networks and the fact that over 50% of commercial aircraft are leased (2024) reduce dependence on any single client, and standardized assets limit buyer leverage versus bespoke units.

- Redelivery timing: bargaining point

- Remarketing strength: lowers client dependence

- Standardization: reduces buyer leverage

Creditworthiness and renegotiations

Weaker lessees demand discounts or deferrals, boosting buyer power during stress; airline insolvency regimes permit lease rejections or rate resets, heightening exposure for Bohai Leasing. Credit screening and enhanced security packages limit downside, while diversification across industries and regions smooths renegotiation risk.

Leased fleet dominance boosts lessee power as top-10 carriers hold ~40% of global fleet

Major airlines and infrastructure operators hold strong leverage—top 10 carriers operated ~40% of the global fleet in 2024—pressuring margins and renewal terms. Alternatives (bank/ECA debt, capital markets) and China 5-yr LPR at 3.65% in 2024 make buyouts attractive, boosting lessee power; ~50%+ of commercial aircraft are leased, raising negotiating strength. Robust remarketing and credit discipline mitigate concentration risk.

| Metric | 2024 Value |

|---|---|

| Top-10 airline fleet share | ~40% |

| Commercial fleet leased | ~50%+ |

| China 5-yr LPR | 3.65% |

Preview Before You Purchase

Bohai Leasing Co. Porter's Five Forces Analysis

The Porter's Five Forces analysis of Bohai Leasing evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry within financial leasing and equipment finance sectors, highlighting regulatory impact and asset concentration risks. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is fully formatted, actionable, and ready for download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bohai Leasing faces moderate rivalry driven by large state-backed rivals and cyclical equipment demand, while regulatory ties and financing access shape its bargaining power.

Supplier leverage is muted by diversified OEM relationships, but buyer concentration and credit risk elevate pressure on margins and contract terms.

Threats from new entrants and substitutes are limited by capital intensity and long-term contracts, yet digital financing innovations could disrupt traditional leasing models.

This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Bohai Leasing Co..

Suppliers Bargaining Power

Concentrated OEM base

Aircraft supply is dominated by a few OEMs (Airbus and Boeing hold over 80% market share), giving them pricing and delivery leverage over lessors. Large backlogs and multi-year certification timelines constrain availability and raise acquisition costs; narrowbodies represent roughly 70% of global backlog, keeping supplier power structurally elevated. Bohai must actively manage order positions and diversify models to mitigate dependence while monitoring cyclical shifts.

Capital providers’ influence

Capital providers—banks, bondholders, ABS investors and ECAs—set covenants and spreads that directly shape Bohai Leasing’s pricing and risk sharing; China's 2024 GDP growth of about 5.2% influenced funding conditions and investor risk appetite. Ratings shifts and market cycles can rapidly widen spreads, while strong liquidity ties and staggered maturities mitigate exposure. Lenders can tighten deal structures, shifting more residual risk onto the lessor.

Maintenance and MRO dependence

MRO vendors and engine shops are highly concentrated for new-generation engines: CFM LEAP and Pratt & Whitney GTF families together account for roughly 70% of narrowbody engine shop demand through 2024, squeezing independent capacity. OEM-controlled parts pricing and scarce shop slots raise lifecycle costs and turnaround times, with global commercial MRO market near $87bn (2023) and tight 2024 backlogs. Power-by-the-hour and pooled-inventory contracts materially dampen cost volatility and supply risk, but delays still erode re-leasing turnaround and residual values.

Asset scarcity cycles

Asset scarcity cycles elevate supplier power for Bohai Leasing as new-tech aircraft remain supply-constrained amid a global commercial backlog of roughly 14,000 aircraft in 2024, and with about 40% of the world fleet on lease this tightness feeds higher lease-rate sensitivity to OEM production-rate shifts; counter-cyclical purchases and sale-leaseback sourcing partially offset costs while secondary-market liquidity provides relief only at market-clearing prices.

- Supply constraint: backlog ~14,000 (2024)

- Leasing penetration: ~40% of fleet

- Mitigants: counter-cyclical buys, sale-leasebacks

- Relief: secondary market at market-clearing prices

Specialized container/equipment makers

Specialized container and high-end equipment suppliers can pass through input-cost volatility, limiting Bohai Leasing’s margin control; in 2024 the global container fleet was roughly 25 million TEU, sustaining supplier pricing leverage.

Standardization lowers differentiation, so large-scale buyers secure better terms while long-term supply frameworks and volume commitments improve Bohai’s pricing; currency and commodity swings in 2024 amplified supplier bargaining power.

- Pass-through pricing: high

- Scale advantage: strong for large lessors

- LT contracts: reduce unit cost

- Macro risks: FX/steel volatility in 2024

Dominant OEMs and MROs squeeze margins amid ~14,000-aircraft backlog

Supplier power is high: OEMs (Airbus/Boeing >80% share) and concentrated MRO/engine shops raise prices and delay deliveries amid a ~14,000-aircraft backlog (2024). Leasing penetration ~40% and tight narrowbody supply keep lease-rate sensitivity elevated; financing spreads and parts costs (global MRO ~$87bn in 2023) further constrain margins.

| Metric | 2024/2023 |

|---|---|

| Global backlog | ~14,000 (2024) |

| Leased fleet | ~40% |

| OEM share | Airbus+Boeing >80% |

| Global MRO | $87bn (2023) |

What is included in the product

Concise Porter's Five Forces assessment of Bohai Leasing Co., highlighting competitive rivalry, buyer and supplier bargaining power, threats from new entrants and substitutes, and regulatory barriers; identifies disruptive forces and strategic levers to defend margins and sustain market position.

Bohai Leasing Co. Porter's Five Forces Analysis delivers a clear one-sheet summary of competitive pressures—ideal for swift, boardroom-ready decisions—and lets you customize pressure levels to reflect new data or regulatory shifts, removing analysis bottlenecks and speeding strategic response.

Customers Bargaining Power

Large anchor clients

Major airlines, shipping lines and infrastructure operators exert strong bargaining power: the top 10 airlines operated roughly 40% of the global commercial fleet in 2024, enabling multi-asset deals and leverage over maintenance reserves; concentration risk forces larger concessions at renewal and can pressure Bohai Leasing margins, while landing marquee clients often establishes pricing benchmarks across Asia-Pacific and global markets.

Alternative financing options

Clients can bypass leasing by using bank loans, ECA-backed debt or capital markets, with China's 5-year LPR at 3.65% in 2024 making buyouts more attractive; sale-leasebacks and PDP financing further compress yields. Competition forces Bohai Leasing to compete on flexibility, transaction speed and transferring residual-value risk to preserve margins. In tighter credit cycles leasing regains appeal, reducing buyer power as corporates turn to off-balance solutions.

Contract duration and terms

Long tenors lock in asset utilization for Bohai Leasing but invite tougher negotiations on covenants and end-of-lease conditions.

Lessees increasingly push for power-by-the-hour and lower reserves in downturns, with roughly 50% of the global commercial fleet leased, boosting lessee bargaining power.

Return-condition disputes can erode economics, so balanced clauses and credit-based pricing discipline (tiered margins by lessee rating) are key.

Switching and downtime costs

Switching and reconfiguration downtime raise frictions for Bohai Leasing and customers, as aircraft redelivery can take weeks and incur maintenance and lease-end costs; buyers often press for concessions near redelivery to exploit timing. Bohai's strong remarketing networks and the fact that over 50% of commercial aircraft are leased (2024) reduce dependence on any single client, and standardized assets limit buyer leverage versus bespoke units.

- Redelivery timing: bargaining point

- Remarketing strength: lowers client dependence

- Standardization: reduces buyer leverage

Creditworthiness and renegotiations

Weaker lessees demand discounts or deferrals, boosting buyer power during stress; airline insolvency regimes permit lease rejections or rate resets, heightening exposure for Bohai Leasing. Credit screening and enhanced security packages limit downside, while diversification across industries and regions smooths renegotiation risk.

Leased fleet dominance boosts lessee power as top-10 carriers hold ~40% of global fleet

Major airlines and infrastructure operators hold strong leverage—top 10 carriers operated ~40% of the global fleet in 2024—pressuring margins and renewal terms. Alternatives (bank/ECA debt, capital markets) and China 5-yr LPR at 3.65% in 2024 make buyouts attractive, boosting lessee power; ~50%+ of commercial aircraft are leased, raising negotiating strength. Robust remarketing and credit discipline mitigate concentration risk.

| Metric | 2024 Value |

|---|---|

| Top-10 airline fleet share | ~40% |

| Commercial fleet leased | ~50%+ |

| China 5-yr LPR | 3.65% |

Preview Before You Purchase

Bohai Leasing Co. Porter's Five Forces Analysis

The Porter's Five Forces analysis of Bohai Leasing evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry within financial leasing and equipment finance sectors, highlighting regulatory impact and asset concentration risks. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is fully formatted, actionable, and ready for download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bohai Leasing faces moderate rivalry driven by large state-backed rivals and cyclical equipment demand, while regulatory ties and financing access shape its bargaining power.

Supplier leverage is muted by diversified OEM relationships, but buyer concentration and credit risk elevate pressure on margins and contract terms.

Threats from new entrants and substitutes are limited by capital intensity and long-term contracts, yet digital financing innovations could disrupt traditional leasing models.

This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Bohai Leasing Co..

Suppliers Bargaining Power

Concentrated OEM base

Aircraft supply is dominated by a few OEMs (Airbus and Boeing hold over 80% market share), giving them pricing and delivery leverage over lessors. Large backlogs and multi-year certification timelines constrain availability and raise acquisition costs; narrowbodies represent roughly 70% of global backlog, keeping supplier power structurally elevated. Bohai must actively manage order positions and diversify models to mitigate dependence while monitoring cyclical shifts.

Capital providers’ influence

Capital providers—banks, bondholders, ABS investors and ECAs—set covenants and spreads that directly shape Bohai Leasing’s pricing and risk sharing; China's 2024 GDP growth of about 5.2% influenced funding conditions and investor risk appetite. Ratings shifts and market cycles can rapidly widen spreads, while strong liquidity ties and staggered maturities mitigate exposure. Lenders can tighten deal structures, shifting more residual risk onto the lessor.

Maintenance and MRO dependence

MRO vendors and engine shops are highly concentrated for new-generation engines: CFM LEAP and Pratt & Whitney GTF families together account for roughly 70% of narrowbody engine shop demand through 2024, squeezing independent capacity. OEM-controlled parts pricing and scarce shop slots raise lifecycle costs and turnaround times, with global commercial MRO market near $87bn (2023) and tight 2024 backlogs. Power-by-the-hour and pooled-inventory contracts materially dampen cost volatility and supply risk, but delays still erode re-leasing turnaround and residual values.

Asset scarcity cycles

Asset scarcity cycles elevate supplier power for Bohai Leasing as new-tech aircraft remain supply-constrained amid a global commercial backlog of roughly 14,000 aircraft in 2024, and with about 40% of the world fleet on lease this tightness feeds higher lease-rate sensitivity to OEM production-rate shifts; counter-cyclical purchases and sale-leaseback sourcing partially offset costs while secondary-market liquidity provides relief only at market-clearing prices.

- Supply constraint: backlog ~14,000 (2024)

- Leasing penetration: ~40% of fleet

- Mitigants: counter-cyclical buys, sale-leasebacks

- Relief: secondary market at market-clearing prices

Specialized container/equipment makers

Specialized container and high-end equipment suppliers can pass through input-cost volatility, limiting Bohai Leasing’s margin control; in 2024 the global container fleet was roughly 25 million TEU, sustaining supplier pricing leverage.

Standardization lowers differentiation, so large-scale buyers secure better terms while long-term supply frameworks and volume commitments improve Bohai’s pricing; currency and commodity swings in 2024 amplified supplier bargaining power.

- Pass-through pricing: high

- Scale advantage: strong for large lessors

- LT contracts: reduce unit cost

- Macro risks: FX/steel volatility in 2024

Dominant OEMs and MROs squeeze margins amid ~14,000-aircraft backlog

Supplier power is high: OEMs (Airbus/Boeing >80% share) and concentrated MRO/engine shops raise prices and delay deliveries amid a ~14,000-aircraft backlog (2024). Leasing penetration ~40% and tight narrowbody supply keep lease-rate sensitivity elevated; financing spreads and parts costs (global MRO ~$87bn in 2023) further constrain margins.

| Metric | 2024/2023 |

|---|---|

| Global backlog | ~14,000 (2024) |

| Leased fleet | ~40% |

| OEM share | Airbus+Boeing >80% |

| Global MRO | $87bn (2023) |

What is included in the product

Concise Porter's Five Forces assessment of Bohai Leasing Co., highlighting competitive rivalry, buyer and supplier bargaining power, threats from new entrants and substitutes, and regulatory barriers; identifies disruptive forces and strategic levers to defend margins and sustain market position.

Bohai Leasing Co. Porter's Five Forces Analysis delivers a clear one-sheet summary of competitive pressures—ideal for swift, boardroom-ready decisions—and lets you customize pressure levels to reflect new data or regulatory shifts, removing analysis bottlenecks and speeding strategic response.

Customers Bargaining Power

Large anchor clients

Major airlines, shipping lines and infrastructure operators exert strong bargaining power: the top 10 airlines operated roughly 40% of the global commercial fleet in 2024, enabling multi-asset deals and leverage over maintenance reserves; concentration risk forces larger concessions at renewal and can pressure Bohai Leasing margins, while landing marquee clients often establishes pricing benchmarks across Asia-Pacific and global markets.

Alternative financing options

Clients can bypass leasing by using bank loans, ECA-backed debt or capital markets, with China's 5-year LPR at 3.65% in 2024 making buyouts more attractive; sale-leasebacks and PDP financing further compress yields. Competition forces Bohai Leasing to compete on flexibility, transaction speed and transferring residual-value risk to preserve margins. In tighter credit cycles leasing regains appeal, reducing buyer power as corporates turn to off-balance solutions.

Contract duration and terms

Long tenors lock in asset utilization for Bohai Leasing but invite tougher negotiations on covenants and end-of-lease conditions.

Lessees increasingly push for power-by-the-hour and lower reserves in downturns, with roughly 50% of the global commercial fleet leased, boosting lessee bargaining power.

Return-condition disputes can erode economics, so balanced clauses and credit-based pricing discipline (tiered margins by lessee rating) are key.

Switching and downtime costs

Switching and reconfiguration downtime raise frictions for Bohai Leasing and customers, as aircraft redelivery can take weeks and incur maintenance and lease-end costs; buyers often press for concessions near redelivery to exploit timing. Bohai's strong remarketing networks and the fact that over 50% of commercial aircraft are leased (2024) reduce dependence on any single client, and standardized assets limit buyer leverage versus bespoke units.

- Redelivery timing: bargaining point

- Remarketing strength: lowers client dependence

- Standardization: reduces buyer leverage

Creditworthiness and renegotiations

Weaker lessees demand discounts or deferrals, boosting buyer power during stress; airline insolvency regimes permit lease rejections or rate resets, heightening exposure for Bohai Leasing. Credit screening and enhanced security packages limit downside, while diversification across industries and regions smooths renegotiation risk.

Leased fleet dominance boosts lessee power as top-10 carriers hold ~40% of global fleet

Major airlines and infrastructure operators hold strong leverage—top 10 carriers operated ~40% of the global fleet in 2024—pressuring margins and renewal terms. Alternatives (bank/ECA debt, capital markets) and China 5-yr LPR at 3.65% in 2024 make buyouts attractive, boosting lessee power; ~50%+ of commercial aircraft are leased, raising negotiating strength. Robust remarketing and credit discipline mitigate concentration risk.

| Metric | 2024 Value |

|---|---|

| Top-10 airline fleet share | ~40% |

| Commercial fleet leased | ~50%+ |

| China 5-yr LPR | 3.65% |

Preview Before You Purchase

Bohai Leasing Co. Porter's Five Forces Analysis

The Porter's Five Forces analysis of Bohai Leasing evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry within financial leasing and equipment finance sectors, highlighting regulatory impact and asset concentration risks. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is fully formatted, actionable, and ready for download and use.