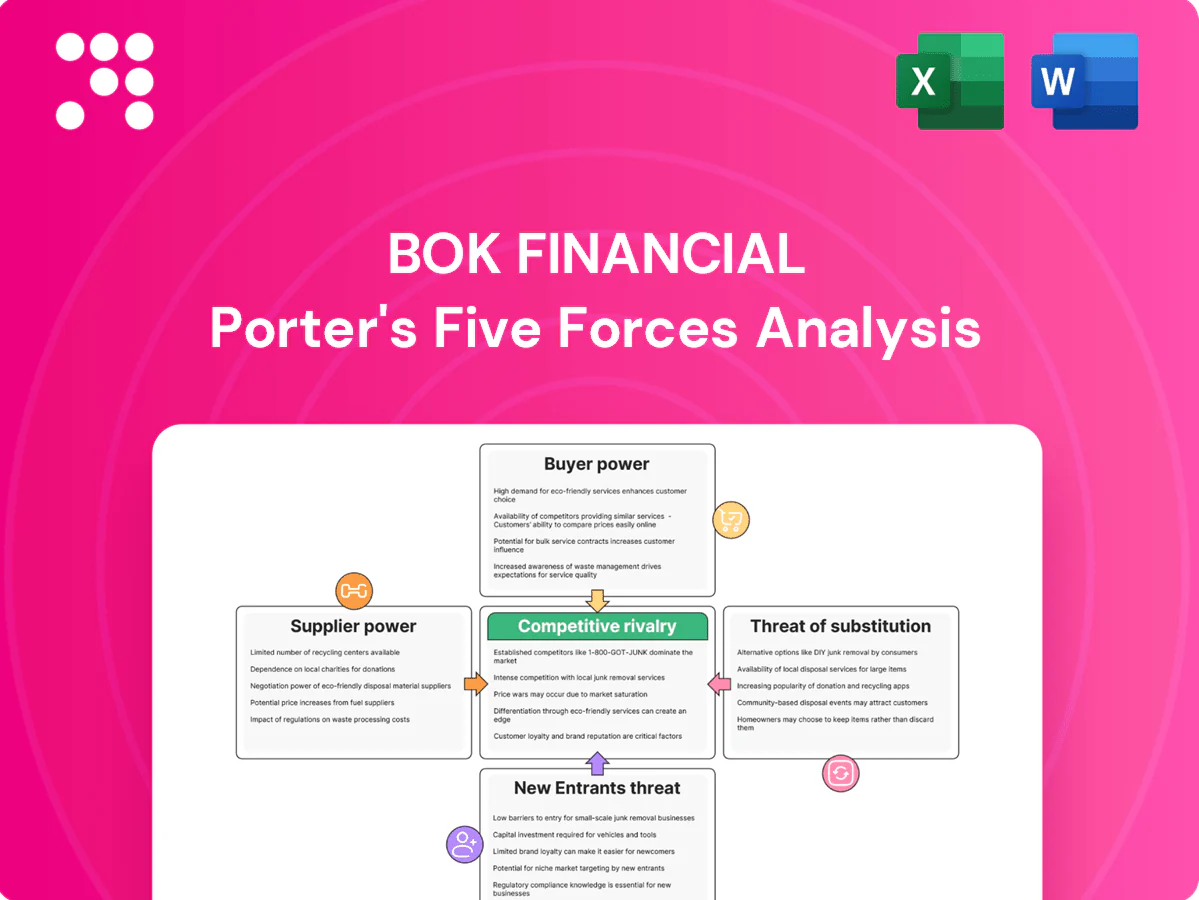

BOK Financial Porter's Five Forces Analysis

From Overview to Strategy Blueprint

BOK Financial faces moderate competitive rivalry, rising digital disruption, and nuanced buyer power shaped by regional client relationships; supplier and substitute threats remain limited but evolving. This snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore BOK Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core technology vendors

Core processing, digital banking, and payments rails are concentrated among FIS, Fiserv and Jack Henry, giving vendors significant leverage over pricing and contract terms; these three dominate U.S. core relationships. Core conversions typically take 18–36 months and cost tens of millions, creating high lock-in and forcing BOK Financial into multi-year deals with limited alternatives, pressuring margins and slowing time-to-market for new features.

Funding providers and depositors

Depositors and wholesale lenders supply banks’ primary raw material—funds—and BOK Financial faces pressure when rate-sensitive deposits migrate in higher-rate environments, forcing higher costs or greater reliance on wholesale markets. Large corporate and institutional depositors, often above the $250,000 FDIC insurance threshold, exert pricing power through ticket size and mobility. Diversifying funding sources mitigates but does not remove supplier bargaining leverage.

Skilled labor and compliance talent

Specialized bankers, risk, tech, and compliance professionals are scarce, giving talent meaningful bargaining power; BLS median wages in May 2023 were $109,020 for software developers and roughly $79,030 for compliance officers, underscoring cost differentials that persisted into 2024. Compensation, retention, and recruitment costs rise in tight markets, regulatory complexity heightens dependence on experienced staff, and wage pressure can lift operating expenses and risk service quality if unaddressed.

Payment networks and clearing systems

Card networks, ACH, Fedwire, RTP and other rails enforce non-negotiable rules and fees (card interchange typically ~1–3% plus fixed cents; ACH fees commonly $0.20–$0.60 per item), making participation essential for customer utility and constraining BOK Financial’s leverage. Mandatory compliance and protocol changes (RTP real-time requirements, Fedwire settlement rules) force costly, fixed-timeline tech updates. Scale discounts exist but practical switching is limited by network effects and certification timelines.

- Network fees: card interchange ~1–3% + fixed cents

- ACH costs: ~$0.20–$0.60/tx

- RTP/Fedwire: real-time/overnight settlement mandates ongoing upgrade costs

- Switching constrained: certification, integrations, limited alternative rails

Third-party data, cloud, and cybersecurity vendors

Threat environments and digital scale push BOK Financial to rely on specialized third-party data, cloud, and cybersecurity vendors; the global public cloud market reached about $600B in 2024 and the cybersecurity market roughly $200B, enabling vendors to command premium pricing for certified security, proprietary data feeds, analytics, and managed services. Vendor due diligence and continuous monitoring add operational cost and complexity, while consolidation — with the top three cloud providers holding roughly 70% share in 2024 — strengthens supplier bargaining power.

- Vendor premiums for certified security and data feeds

- Ongoing due diligence and monitoring costs

- Top-3 cloud vendors ~70% market share (2024)

- Cloud market ~$600B and cybersecurity ~$200B (2024)

Core-banking incumbents' lock-in and funding squeeze margins; cloud ~70%, interchange 1–3%

Core banking vendors (FIS/Fiserv/Jack Henry) dominate U.S. cores, creating high lock-in and multi-year contracts that raise costs and slow feature rollout.

Funding suppliers—rate-sensitive depositors and wholesale lenders—pressure funding costs in rising-rate cycles; large uninsured deposits wield pricing leverage.

Cloud and security vendors (top-3 ~70% share in 2024), card networks (interchange ~1–3%), and ACH ($0.20–$0.60/tx) further constrain margins.

| Metric | 2024 value |

|---|---|

| Top-3 cloud share | ~70% |

| Card interchange | 1–3% + fixed cents |

| ACH fee | $0.20–$0.60/tx |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for BOK Financial, with detailed analysis of each force, identification of disruptive threats and substitutes, and evaluation of supplier/buyer power to assess pricing and profitability—fully editable for reports and strategy decks.

A clear one-sheet summary of BOK Financial's Porter's Five Forces—instantly visualize competitive pressure with an editable spider chart, customize scores for evolving market data, and copy straight into decks or reports for fast, board-ready strategic decisions.

Customers Bargaining Power

Rate sensitivity and price transparency

Customers compare deposit rates and loan pricing instantly via digital channels; with the fed funds rate at 5.25–5.50% at end-2024, rising-rate cycles have lifted deposit betas and customers demand higher yields, while loan applicants shop multiple quotes, compressing spreads—this transparency amplifies buyer power and pressures BOK Financials net interest margin.

Large corporates and institutions

Large corporates negotiate aggressively on credit, treasury and wealth fees—enterprise mandates often require bundled pricing and bespoke covenants, compressing margins per relationship by up to 20–30% versus standard pricing. Industry surveys in 2023–24 show about 70% of firms multi-bank, lowering switching costs and increasing bargaining power. A handful of enterprise clients can drive double-digit percentage swings in relationship profitability.

Mortgage borrowers and brokers

Residential borrowers routinely rate-shop across banks and non-bank lenders, with brokers capturing roughly 30% of retail origination volume in 2024 and steering flow based on price and speed. Secondary market demand—GSEs and agencies buying about 70% of conforming loans—makes offers highly comparable. That transparency compresses gain-on-sale margins and origination fees to roughly 10–30 basis points in competitive markets.

Wealth management fee compression

- Benchmarking: ETFs 0.03–0.06%

- Robos: ~0.25% fee

- Advisory avg: ~0.70% AUM (2024)

- HNW: negotiate bespoke pricing

- Trend: unbundling → value-based fees

Low switching frictions via digital

- Account opening: faster onboarding

- APIs/aggregators: transparent pricing

- Single-product users: high churn

- Buyer leverage: pricing and service impact

Fee compression and price sensitivity squeeze margins at 5.25–5.50%

Customers wield rising price sensitivity: fed funds 5.25–5.50% (end-2024) lifts deposit betas and squeezes NIM; 70% of corporates multi-bank and negotiate fees; brokers steer ~30% of retail origination, compressing gain-on-sale; advisory fees benchmarked to ETFs 0.03–0.06%, robos ~0.25% vs industry avg ~0.70%, and 78% US mobile banking use lowers switching costs.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| Corporates multi-bank | 70% |

| Broker retail originations | ~30% |

| ETF fees | 0.03–0.06% |

| Robo fees | ~0.25% |

| Advisory avg | ~0.70% |

| Mobile banking usage | 78% |

Preview the Actual Deliverable

BOK Financial Porter's Five Forces Analysis

This preview shows the exact BOK Financial Porter's Five Forces analysis you'll receive after purchase—fully researched, professionally formatted, and ready for immediate use. It contains the same competitive intensity evaluation, supplier and buyer dynamics, threat assessments, and strategic implications. No placeholders or samples—this is the final deliverable you'll download instantly.

From Overview to Strategy Blueprint

BOK Financial faces moderate competitive rivalry, rising digital disruption, and nuanced buyer power shaped by regional client relationships; supplier and substitute threats remain limited but evolving. This snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore BOK Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core technology vendors

Core processing, digital banking, and payments rails are concentrated among FIS, Fiserv and Jack Henry, giving vendors significant leverage over pricing and contract terms; these three dominate U.S. core relationships. Core conversions typically take 18–36 months and cost tens of millions, creating high lock-in and forcing BOK Financial into multi-year deals with limited alternatives, pressuring margins and slowing time-to-market for new features.

Funding providers and depositors

Depositors and wholesale lenders supply banks’ primary raw material—funds—and BOK Financial faces pressure when rate-sensitive deposits migrate in higher-rate environments, forcing higher costs or greater reliance on wholesale markets. Large corporate and institutional depositors, often above the $250,000 FDIC insurance threshold, exert pricing power through ticket size and mobility. Diversifying funding sources mitigates but does not remove supplier bargaining leverage.

Skilled labor and compliance talent

Specialized bankers, risk, tech, and compliance professionals are scarce, giving talent meaningful bargaining power; BLS median wages in May 2023 were $109,020 for software developers and roughly $79,030 for compliance officers, underscoring cost differentials that persisted into 2024. Compensation, retention, and recruitment costs rise in tight markets, regulatory complexity heightens dependence on experienced staff, and wage pressure can lift operating expenses and risk service quality if unaddressed.

Payment networks and clearing systems

Card networks, ACH, Fedwire, RTP and other rails enforce non-negotiable rules and fees (card interchange typically ~1–3% plus fixed cents; ACH fees commonly $0.20–$0.60 per item), making participation essential for customer utility and constraining BOK Financial’s leverage. Mandatory compliance and protocol changes (RTP real-time requirements, Fedwire settlement rules) force costly, fixed-timeline tech updates. Scale discounts exist but practical switching is limited by network effects and certification timelines.

- Network fees: card interchange ~1–3% + fixed cents

- ACH costs: ~$0.20–$0.60/tx

- RTP/Fedwire: real-time/overnight settlement mandates ongoing upgrade costs

- Switching constrained: certification, integrations, limited alternative rails

Third-party data, cloud, and cybersecurity vendors

Threat environments and digital scale push BOK Financial to rely on specialized third-party data, cloud, and cybersecurity vendors; the global public cloud market reached about $600B in 2024 and the cybersecurity market roughly $200B, enabling vendors to command premium pricing for certified security, proprietary data feeds, analytics, and managed services. Vendor due diligence and continuous monitoring add operational cost and complexity, while consolidation — with the top three cloud providers holding roughly 70% share in 2024 — strengthens supplier bargaining power.

- Vendor premiums for certified security and data feeds

- Ongoing due diligence and monitoring costs

- Top-3 cloud vendors ~70% market share (2024)

- Cloud market ~$600B and cybersecurity ~$200B (2024)

Core-banking incumbents' lock-in and funding squeeze margins; cloud ~70%, interchange 1–3%

Core banking vendors (FIS/Fiserv/Jack Henry) dominate U.S. cores, creating high lock-in and multi-year contracts that raise costs and slow feature rollout.

Funding suppliers—rate-sensitive depositors and wholesale lenders—pressure funding costs in rising-rate cycles; large uninsured deposits wield pricing leverage.

Cloud and security vendors (top-3 ~70% share in 2024), card networks (interchange ~1–3%), and ACH ($0.20–$0.60/tx) further constrain margins.

| Metric | 2024 value |

|---|---|

| Top-3 cloud share | ~70% |

| Card interchange | 1–3% + fixed cents |

| ACH fee | $0.20–$0.60/tx |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for BOK Financial, with detailed analysis of each force, identification of disruptive threats and substitutes, and evaluation of supplier/buyer power to assess pricing and profitability—fully editable for reports and strategy decks.

A clear one-sheet summary of BOK Financial's Porter's Five Forces—instantly visualize competitive pressure with an editable spider chart, customize scores for evolving market data, and copy straight into decks or reports for fast, board-ready strategic decisions.

Customers Bargaining Power

Rate sensitivity and price transparency

Customers compare deposit rates and loan pricing instantly via digital channels; with the fed funds rate at 5.25–5.50% at end-2024, rising-rate cycles have lifted deposit betas and customers demand higher yields, while loan applicants shop multiple quotes, compressing spreads—this transparency amplifies buyer power and pressures BOK Financials net interest margin.

Large corporates and institutions

Large corporates negotiate aggressively on credit, treasury and wealth fees—enterprise mandates often require bundled pricing and bespoke covenants, compressing margins per relationship by up to 20–30% versus standard pricing. Industry surveys in 2023–24 show about 70% of firms multi-bank, lowering switching costs and increasing bargaining power. A handful of enterprise clients can drive double-digit percentage swings in relationship profitability.

Mortgage borrowers and brokers

Residential borrowers routinely rate-shop across banks and non-bank lenders, with brokers capturing roughly 30% of retail origination volume in 2024 and steering flow based on price and speed. Secondary market demand—GSEs and agencies buying about 70% of conforming loans—makes offers highly comparable. That transparency compresses gain-on-sale margins and origination fees to roughly 10–30 basis points in competitive markets.

Wealth management fee compression

- Benchmarking: ETFs 0.03–0.06%

- Robos: ~0.25% fee

- Advisory avg: ~0.70% AUM (2024)

- HNW: negotiate bespoke pricing

- Trend: unbundling → value-based fees

Low switching frictions via digital

- Account opening: faster onboarding

- APIs/aggregators: transparent pricing

- Single-product users: high churn

- Buyer leverage: pricing and service impact

Fee compression and price sensitivity squeeze margins at 5.25–5.50%

Customers wield rising price sensitivity: fed funds 5.25–5.50% (end-2024) lifts deposit betas and squeezes NIM; 70% of corporates multi-bank and negotiate fees; brokers steer ~30% of retail origination, compressing gain-on-sale; advisory fees benchmarked to ETFs 0.03–0.06%, robos ~0.25% vs industry avg ~0.70%, and 78% US mobile banking use lowers switching costs.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| Corporates multi-bank | 70% |

| Broker retail originations | ~30% |

| ETF fees | 0.03–0.06% |

| Robo fees | ~0.25% |

| Advisory avg | ~0.70% |

| Mobile banking usage | 78% |

Preview the Actual Deliverable

BOK Financial Porter's Five Forces Analysis

This preview shows the exact BOK Financial Porter's Five Forces analysis you'll receive after purchase—fully researched, professionally formatted, and ready for immediate use. It contains the same competitive intensity evaluation, supplier and buyer dynamics, threat assessments, and strategic implications. No placeholders or samples—this is the final deliverable you'll download instantly.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

BOK Financial faces moderate competitive rivalry, rising digital disruption, and nuanced buyer power shaped by regional client relationships; supplier and substitute threats remain limited but evolving. This snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore BOK Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core technology vendors

Core processing, digital banking, and payments rails are concentrated among FIS, Fiserv and Jack Henry, giving vendors significant leverage over pricing and contract terms; these three dominate U.S. core relationships. Core conversions typically take 18–36 months and cost tens of millions, creating high lock-in and forcing BOK Financial into multi-year deals with limited alternatives, pressuring margins and slowing time-to-market for new features.

Funding providers and depositors

Depositors and wholesale lenders supply banks’ primary raw material—funds—and BOK Financial faces pressure when rate-sensitive deposits migrate in higher-rate environments, forcing higher costs or greater reliance on wholesale markets. Large corporate and institutional depositors, often above the $250,000 FDIC insurance threshold, exert pricing power through ticket size and mobility. Diversifying funding sources mitigates but does not remove supplier bargaining leverage.

Skilled labor and compliance talent

Specialized bankers, risk, tech, and compliance professionals are scarce, giving talent meaningful bargaining power; BLS median wages in May 2023 were $109,020 for software developers and roughly $79,030 for compliance officers, underscoring cost differentials that persisted into 2024. Compensation, retention, and recruitment costs rise in tight markets, regulatory complexity heightens dependence on experienced staff, and wage pressure can lift operating expenses and risk service quality if unaddressed.

Payment networks and clearing systems

Card networks, ACH, Fedwire, RTP and other rails enforce non-negotiable rules and fees (card interchange typically ~1–3% plus fixed cents; ACH fees commonly $0.20–$0.60 per item), making participation essential for customer utility and constraining BOK Financial’s leverage. Mandatory compliance and protocol changes (RTP real-time requirements, Fedwire settlement rules) force costly, fixed-timeline tech updates. Scale discounts exist but practical switching is limited by network effects and certification timelines.

- Network fees: card interchange ~1–3% + fixed cents

- ACH costs: ~$0.20–$0.60/tx

- RTP/Fedwire: real-time/overnight settlement mandates ongoing upgrade costs

- Switching constrained: certification, integrations, limited alternative rails

Third-party data, cloud, and cybersecurity vendors

Threat environments and digital scale push BOK Financial to rely on specialized third-party data, cloud, and cybersecurity vendors; the global public cloud market reached about $600B in 2024 and the cybersecurity market roughly $200B, enabling vendors to command premium pricing for certified security, proprietary data feeds, analytics, and managed services. Vendor due diligence and continuous monitoring add operational cost and complexity, while consolidation — with the top three cloud providers holding roughly 70% share in 2024 — strengthens supplier bargaining power.

- Vendor premiums for certified security and data feeds

- Ongoing due diligence and monitoring costs

- Top-3 cloud vendors ~70% market share (2024)

- Cloud market ~$600B and cybersecurity ~$200B (2024)

Core-banking incumbents' lock-in and funding squeeze margins; cloud ~70%, interchange 1–3%

Core banking vendors (FIS/Fiserv/Jack Henry) dominate U.S. cores, creating high lock-in and multi-year contracts that raise costs and slow feature rollout.

Funding suppliers—rate-sensitive depositors and wholesale lenders—pressure funding costs in rising-rate cycles; large uninsured deposits wield pricing leverage.

Cloud and security vendors (top-3 ~70% share in 2024), card networks (interchange ~1–3%), and ACH ($0.20–$0.60/tx) further constrain margins.

| Metric | 2024 value |

|---|---|

| Top-3 cloud share | ~70% |

| Card interchange | 1–3% + fixed cents |

| ACH fee | $0.20–$0.60/tx |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for BOK Financial, with detailed analysis of each force, identification of disruptive threats and substitutes, and evaluation of supplier/buyer power to assess pricing and profitability—fully editable for reports and strategy decks.

A clear one-sheet summary of BOK Financial's Porter's Five Forces—instantly visualize competitive pressure with an editable spider chart, customize scores for evolving market data, and copy straight into decks or reports for fast, board-ready strategic decisions.

Customers Bargaining Power

Rate sensitivity and price transparency

Customers compare deposit rates and loan pricing instantly via digital channels; with the fed funds rate at 5.25–5.50% at end-2024, rising-rate cycles have lifted deposit betas and customers demand higher yields, while loan applicants shop multiple quotes, compressing spreads—this transparency amplifies buyer power and pressures BOK Financials net interest margin.

Large corporates and institutions

Large corporates negotiate aggressively on credit, treasury and wealth fees—enterprise mandates often require bundled pricing and bespoke covenants, compressing margins per relationship by up to 20–30% versus standard pricing. Industry surveys in 2023–24 show about 70% of firms multi-bank, lowering switching costs and increasing bargaining power. A handful of enterprise clients can drive double-digit percentage swings in relationship profitability.

Mortgage borrowers and brokers

Residential borrowers routinely rate-shop across banks and non-bank lenders, with brokers capturing roughly 30% of retail origination volume in 2024 and steering flow based on price and speed. Secondary market demand—GSEs and agencies buying about 70% of conforming loans—makes offers highly comparable. That transparency compresses gain-on-sale margins and origination fees to roughly 10–30 basis points in competitive markets.

Wealth management fee compression

- Benchmarking: ETFs 0.03–0.06%

- Robos: ~0.25% fee

- Advisory avg: ~0.70% AUM (2024)

- HNW: negotiate bespoke pricing

- Trend: unbundling → value-based fees

Low switching frictions via digital

- Account opening: faster onboarding

- APIs/aggregators: transparent pricing

- Single-product users: high churn

- Buyer leverage: pricing and service impact

Fee compression and price sensitivity squeeze margins at 5.25–5.50%

Customers wield rising price sensitivity: fed funds 5.25–5.50% (end-2024) lifts deposit betas and squeezes NIM; 70% of corporates multi-bank and negotiate fees; brokers steer ~30% of retail origination, compressing gain-on-sale; advisory fees benchmarked to ETFs 0.03–0.06%, robos ~0.25% vs industry avg ~0.70%, and 78% US mobile banking use lowers switching costs.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| Corporates multi-bank | 70% |

| Broker retail originations | ~30% |

| ETF fees | 0.03–0.06% |

| Robo fees | ~0.25% |

| Advisory avg | ~0.70% |

| Mobile banking usage | 78% |

Preview the Actual Deliverable

BOK Financial Porter's Five Forces Analysis

This preview shows the exact BOK Financial Porter's Five Forces analysis you'll receive after purchase—fully researched, professionally formatted, and ready for immediate use. It contains the same competitive intensity evaluation, supplier and buyer dynamics, threat assessments, and strategic implications. No placeholders or samples—this is the final deliverable you'll download instantly.