Bombardier Porter's Five Forces Analysis

From Overview to Strategy Blueprint

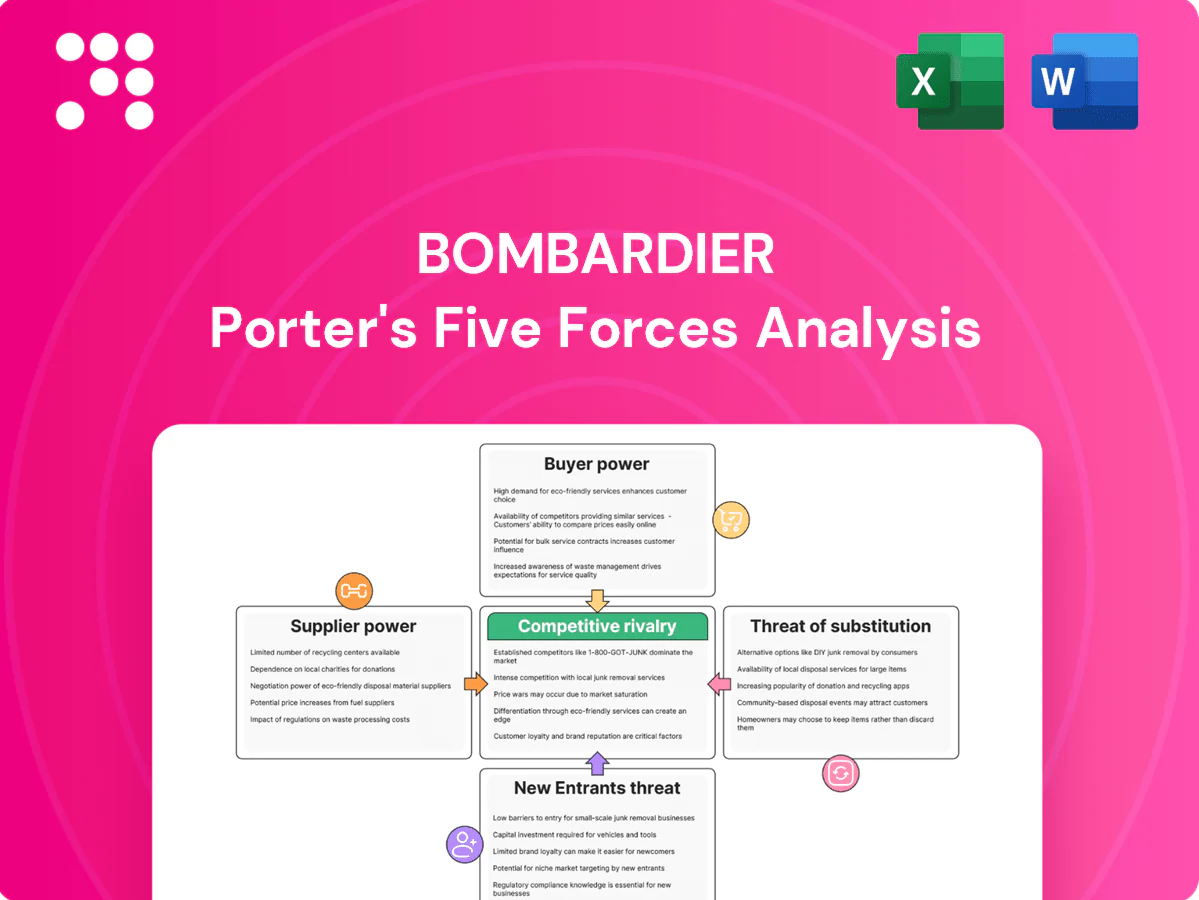

Bombardier faces intense competitive rivalry in aerospace and rail, significant supplier influence for specialized components, and strong buyer power from major airlines and transit authorities; barriers to entry are high but technological shifts and leasing models raise substitute threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bombardier’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated engine suppliers

Business jet engines are concentrated among Rolls-Royce, Pratt & Whitney Canada and GE, creating significant supplier concentration and bargaining power over airframe makers like Bombardier. Certification links engines to specific airframes, making engine swaps costly and raising switching barriers. Engine OEMs also control aftermarket spares and MRO approvals, reinforcing leverage. This dynamic can squeeze Bombardier margins and disrupt delivery timetables.

Avionics and systems lock-in

Core avionics and flight controls from Honeywell and Collins are deeply integrated into Bombardier type certifications; FAA/EASA recertification to change vendors requires multi-year, multi-million-dollar programs. Software and cybersecurity update cycles further entrench vendor dependencies and proprietary interfaces. These dynamics give suppliers significant bargaining power over pricing and roadmap influence in 2024.

Materials and long-lead items

Advanced composites, titanium, and specialty alloys face supply constraints and geopolitical risk, with industry analysts in 2024 reporting single-digit to low-double-digit percent supply shortfalls for critical aerospace materials. Long-lead items—landing gear (18–36 months), actuation systems (12–24 months), cabin systems (6–18 months)—require early commitments; disruptions can cascade into multi-month production delays, letting suppliers secure premium terms due to limited substitutes and tight specs.

Aftermarket parts dependence

Aftermarket parts dependence concentrates bargaining power with subsystem OEMs through proprietary catalogs and licensing, and as of 2024 PMA alternatives remain limited in business aviation compared with commercial fleets. Parts pricing and lead times (commonly causing downtime of weeks to months) directly affect operator uptime and squeeze Bombardier’s service margins. Supplier control over approved repair schemes also shapes total cost of ownership across an aircraft lifecycle.

- Proprietary catalogs concentrate OEM leverage

- PMA penetration in bizav remains limited vs commercial

- Pricing and lead times drive downtime and margin pressure

- Repair-scheme control influences lifecycle TCO

SAF and sustainability inputs

Scaling SAF and greener materials depends on external feedstock, refinery and certification ecosystems; limited availability and price premiums raise operating costs for customers, with SAF supply under 0.1% of global jet fuel demand in 2024. Suppliers able to deliver certified low-emission solutions therefore gain strong negotiating leverage, and Bombardier’s sustainability commitments increase reliance on these partners.

- SAF supply <0.1% of jet fuel (2024)

- Premiums often double conventional jet fuel

- Certified suppliers = higher bargaining power

- Bombardier dependence rises procurement risk

Engines > 70%, long lead times and under 0.1% SAF squeeze margins

Supplier concentration (Rolls‑Royce, PWC, GE >70% share in bizjet engines in 2024), proprietary certifications and long lead times (landing gear 18–36 months) give suppliers strong pricing and delivery leverage, constraining Bombardier margins and schedules. SAF supply <0.1% of demand in 2024 raises costs and dependence on certified suppliers.

| Metric | 2024 |

|---|---|

| Engine OEM share | >70% |

| Landing gear lead time | 18–36 months |

| SAF supply | <0.1% global demand |

What is included in the product

Tailored Porter’s Five Forces analysis for Bombardier assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive risks and strategic opportunities.

A clear one-sheet summary of Bombardier's five forces—perfect for quick strategic and investment decisions, with a clean layout ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated fleet buyers

Fractional operators, charter providers and governments purchase business jets in batches, with large buyers like NetJets (≈700 jets fleet) and major charter groups leveraging scale and publicity to demand price cuts and bespoke configurations. They routinely play OEMs against each other across comparable models, squeezing discounts and aftermarket support concessions, pressuring Bombardier’s margins and pricing power in 2024.

High ticket, informed buyers

Ultra-high-net-worth individuals and corporate flight departments are highly sophisticated and price aware, benchmarking range, cabin and operating costs across Gulfstream, Dassault and Embraer; with the global business jet fleet ~22,000 in 2024, buyers demand tight value. Detailed due diligence—maintenance logs, performance and residual forecasts—reduces information asymmetry. Negotiations routinely include pilot training, warranties and parts credits; new large-cabin list prices span roughly $20–80 million.

Switching via secondary market

Robust pre-owned markets let buyers switch models and brands faster, with used business-jet transactions representing about 55% of market activity in 2024, increasing bargaining leverage. Residual value performance is a clear bargaining chip in new sales; weakening residuals force customers to demand deeper discounts and aftermarket support. This dynamic ties Bombardier to long-term value commitments on pricing and trade-in guarantees.

Total cost and uptime focus

Buyers optimize lifecycle costs, not just acquisition price; in 2024 the global aircraft MRO market was estimated at US$85–90 billion, shifting procurement toward total-cost-of-ownership metrics.

Guaranteed maintenance programs and AOG SLAs (response times often under 2–4 hours) are central to deals; reliability gaps can trigger contractual penalties or lost renewals, shifting bargaining power toward customers demanding measurable service outcomes.

- Lifecycle cost focus

- Guaranteed maintenance & AOG SLAs

- Penalties and renewal risk

- Customer leverage for measurable uptime

ESG and noise/emissions demands

In 2024 corporate buyers face intensified sustainability reporting pressures, driving demands for SAF compatibility, lower CO2 emissions and quieter operations; compliance now influences airport access and reputational risk, and customers use these mandates to extract technology upgrades and favorable commercial terms from Bombardier.

- 2024: sustainability reporting central to procurement

- SAF compatibility required in contracts

- Noise/emissions affect airport slots and PR

- Buyers leverage upgrades for price/terms

Large fleets leverage scale and a 55% pre-owned market to demand discounts

Buyers—large fleets (NetJets ≈700 jets) and sophisticated HNW/corporate buyers—use scale, benchmarking and a strong pre-owned market (≈55% of transactions in 2024) to extract discounts, service concessions and residual guarantees, pressuring Bombardier’s margins. Lifecycle cost focus (global MRO ≈US$85–90bn) and sustainability mandates (SAF, emissions) increase bargaining leverage. Guaranteed MRO/AOG SLAs and residual commitments are deal drivers.

| Metric | 2024 value |

|---|---|

| Global bizjet fleet | ≈22,000 |

| Pre-owned share | ≈55% |

| NetJets fleet | ≈700 |

| MRO market | US$85–90bn |

| Large-cabin list price | US$20–80m |

Preview the Actual Deliverable

Bombardier Porter's Five Forces Analysis

This preview shows the exact Bombardier Porter's Five Forces analysis you'll receive upon purchase—no placeholders and no edits required. The document is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely what will be delivered instantly after payment.

From Overview to Strategy Blueprint

Bombardier faces intense competitive rivalry in aerospace and rail, significant supplier influence for specialized components, and strong buyer power from major airlines and transit authorities; barriers to entry are high but technological shifts and leasing models raise substitute threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bombardier’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated engine suppliers

Business jet engines are concentrated among Rolls-Royce, Pratt & Whitney Canada and GE, creating significant supplier concentration and bargaining power over airframe makers like Bombardier. Certification links engines to specific airframes, making engine swaps costly and raising switching barriers. Engine OEMs also control aftermarket spares and MRO approvals, reinforcing leverage. This dynamic can squeeze Bombardier margins and disrupt delivery timetables.

Avionics and systems lock-in

Core avionics and flight controls from Honeywell and Collins are deeply integrated into Bombardier type certifications; FAA/EASA recertification to change vendors requires multi-year, multi-million-dollar programs. Software and cybersecurity update cycles further entrench vendor dependencies and proprietary interfaces. These dynamics give suppliers significant bargaining power over pricing and roadmap influence in 2024.

Materials and long-lead items

Advanced composites, titanium, and specialty alloys face supply constraints and geopolitical risk, with industry analysts in 2024 reporting single-digit to low-double-digit percent supply shortfalls for critical aerospace materials. Long-lead items—landing gear (18–36 months), actuation systems (12–24 months), cabin systems (6–18 months)—require early commitments; disruptions can cascade into multi-month production delays, letting suppliers secure premium terms due to limited substitutes and tight specs.

Aftermarket parts dependence

Aftermarket parts dependence concentrates bargaining power with subsystem OEMs through proprietary catalogs and licensing, and as of 2024 PMA alternatives remain limited in business aviation compared with commercial fleets. Parts pricing and lead times (commonly causing downtime of weeks to months) directly affect operator uptime and squeeze Bombardier’s service margins. Supplier control over approved repair schemes also shapes total cost of ownership across an aircraft lifecycle.

- Proprietary catalogs concentrate OEM leverage

- PMA penetration in bizav remains limited vs commercial

- Pricing and lead times drive downtime and margin pressure

- Repair-scheme control influences lifecycle TCO

SAF and sustainability inputs

Scaling SAF and greener materials depends on external feedstock, refinery and certification ecosystems; limited availability and price premiums raise operating costs for customers, with SAF supply under 0.1% of global jet fuel demand in 2024. Suppliers able to deliver certified low-emission solutions therefore gain strong negotiating leverage, and Bombardier’s sustainability commitments increase reliance on these partners.

- SAF supply <0.1% of jet fuel (2024)

- Premiums often double conventional jet fuel

- Certified suppliers = higher bargaining power

- Bombardier dependence rises procurement risk

Engines > 70%, long lead times and under 0.1% SAF squeeze margins

Supplier concentration (Rolls‑Royce, PWC, GE >70% share in bizjet engines in 2024), proprietary certifications and long lead times (landing gear 18–36 months) give suppliers strong pricing and delivery leverage, constraining Bombardier margins and schedules. SAF supply <0.1% of demand in 2024 raises costs and dependence on certified suppliers.

| Metric | 2024 |

|---|---|

| Engine OEM share | >70% |

| Landing gear lead time | 18–36 months |

| SAF supply | <0.1% global demand |

What is included in the product

Tailored Porter’s Five Forces analysis for Bombardier assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive risks and strategic opportunities.

A clear one-sheet summary of Bombardier's five forces—perfect for quick strategic and investment decisions, with a clean layout ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated fleet buyers

Fractional operators, charter providers and governments purchase business jets in batches, with large buyers like NetJets (≈700 jets fleet) and major charter groups leveraging scale and publicity to demand price cuts and bespoke configurations. They routinely play OEMs against each other across comparable models, squeezing discounts and aftermarket support concessions, pressuring Bombardier’s margins and pricing power in 2024.

High ticket, informed buyers

Ultra-high-net-worth individuals and corporate flight departments are highly sophisticated and price aware, benchmarking range, cabin and operating costs across Gulfstream, Dassault and Embraer; with the global business jet fleet ~22,000 in 2024, buyers demand tight value. Detailed due diligence—maintenance logs, performance and residual forecasts—reduces information asymmetry. Negotiations routinely include pilot training, warranties and parts credits; new large-cabin list prices span roughly $20–80 million.

Switching via secondary market

Robust pre-owned markets let buyers switch models and brands faster, with used business-jet transactions representing about 55% of market activity in 2024, increasing bargaining leverage. Residual value performance is a clear bargaining chip in new sales; weakening residuals force customers to demand deeper discounts and aftermarket support. This dynamic ties Bombardier to long-term value commitments on pricing and trade-in guarantees.

Total cost and uptime focus

Buyers optimize lifecycle costs, not just acquisition price; in 2024 the global aircraft MRO market was estimated at US$85–90 billion, shifting procurement toward total-cost-of-ownership metrics.

Guaranteed maintenance programs and AOG SLAs (response times often under 2–4 hours) are central to deals; reliability gaps can trigger contractual penalties or lost renewals, shifting bargaining power toward customers demanding measurable service outcomes.

- Lifecycle cost focus

- Guaranteed maintenance & AOG SLAs

- Penalties and renewal risk

- Customer leverage for measurable uptime

ESG and noise/emissions demands

In 2024 corporate buyers face intensified sustainability reporting pressures, driving demands for SAF compatibility, lower CO2 emissions and quieter operations; compliance now influences airport access and reputational risk, and customers use these mandates to extract technology upgrades and favorable commercial terms from Bombardier.

- 2024: sustainability reporting central to procurement

- SAF compatibility required in contracts

- Noise/emissions affect airport slots and PR

- Buyers leverage upgrades for price/terms

Large fleets leverage scale and a 55% pre-owned market to demand discounts

Buyers—large fleets (NetJets ≈700 jets) and sophisticated HNW/corporate buyers—use scale, benchmarking and a strong pre-owned market (≈55% of transactions in 2024) to extract discounts, service concessions and residual guarantees, pressuring Bombardier’s margins. Lifecycle cost focus (global MRO ≈US$85–90bn) and sustainability mandates (SAF, emissions) increase bargaining leverage. Guaranteed MRO/AOG SLAs and residual commitments are deal drivers.

| Metric | 2024 value |

|---|---|

| Global bizjet fleet | ≈22,000 |

| Pre-owned share | ≈55% |

| NetJets fleet | ≈700 |

| MRO market | US$85–90bn |

| Large-cabin list price | US$20–80m |

Preview the Actual Deliverable

Bombardier Porter's Five Forces Analysis

This preview shows the exact Bombardier Porter's Five Forces analysis you'll receive upon purchase—no placeholders and no edits required. The document is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely what will be delivered instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Bombardier faces intense competitive rivalry in aerospace and rail, significant supplier influence for specialized components, and strong buyer power from major airlines and transit authorities; barriers to entry are high but technological shifts and leasing models raise substitute threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bombardier’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated engine suppliers

Business jet engines are concentrated among Rolls-Royce, Pratt & Whitney Canada and GE, creating significant supplier concentration and bargaining power over airframe makers like Bombardier. Certification links engines to specific airframes, making engine swaps costly and raising switching barriers. Engine OEMs also control aftermarket spares and MRO approvals, reinforcing leverage. This dynamic can squeeze Bombardier margins and disrupt delivery timetables.

Avionics and systems lock-in

Core avionics and flight controls from Honeywell and Collins are deeply integrated into Bombardier type certifications; FAA/EASA recertification to change vendors requires multi-year, multi-million-dollar programs. Software and cybersecurity update cycles further entrench vendor dependencies and proprietary interfaces. These dynamics give suppliers significant bargaining power over pricing and roadmap influence in 2024.

Materials and long-lead items

Advanced composites, titanium, and specialty alloys face supply constraints and geopolitical risk, with industry analysts in 2024 reporting single-digit to low-double-digit percent supply shortfalls for critical aerospace materials. Long-lead items—landing gear (18–36 months), actuation systems (12–24 months), cabin systems (6–18 months)—require early commitments; disruptions can cascade into multi-month production delays, letting suppliers secure premium terms due to limited substitutes and tight specs.

Aftermarket parts dependence

Aftermarket parts dependence concentrates bargaining power with subsystem OEMs through proprietary catalogs and licensing, and as of 2024 PMA alternatives remain limited in business aviation compared with commercial fleets. Parts pricing and lead times (commonly causing downtime of weeks to months) directly affect operator uptime and squeeze Bombardier’s service margins. Supplier control over approved repair schemes also shapes total cost of ownership across an aircraft lifecycle.

- Proprietary catalogs concentrate OEM leverage

- PMA penetration in bizav remains limited vs commercial

- Pricing and lead times drive downtime and margin pressure

- Repair-scheme control influences lifecycle TCO

SAF and sustainability inputs

Scaling SAF and greener materials depends on external feedstock, refinery and certification ecosystems; limited availability and price premiums raise operating costs for customers, with SAF supply under 0.1% of global jet fuel demand in 2024. Suppliers able to deliver certified low-emission solutions therefore gain strong negotiating leverage, and Bombardier’s sustainability commitments increase reliance on these partners.

- SAF supply <0.1% of jet fuel (2024)

- Premiums often double conventional jet fuel

- Certified suppliers = higher bargaining power

- Bombardier dependence rises procurement risk

Engines > 70%, long lead times and under 0.1% SAF squeeze margins

Supplier concentration (Rolls‑Royce, PWC, GE >70% share in bizjet engines in 2024), proprietary certifications and long lead times (landing gear 18–36 months) give suppliers strong pricing and delivery leverage, constraining Bombardier margins and schedules. SAF supply <0.1% of demand in 2024 raises costs and dependence on certified suppliers.

| Metric | 2024 |

|---|---|

| Engine OEM share | >70% |

| Landing gear lead time | 18–36 months |

| SAF supply | <0.1% global demand |

What is included in the product

Tailored Porter’s Five Forces analysis for Bombardier assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive risks and strategic opportunities.

A clear one-sheet summary of Bombardier's five forces—perfect for quick strategic and investment decisions, with a clean layout ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated fleet buyers

Fractional operators, charter providers and governments purchase business jets in batches, with large buyers like NetJets (≈700 jets fleet) and major charter groups leveraging scale and publicity to demand price cuts and bespoke configurations. They routinely play OEMs against each other across comparable models, squeezing discounts and aftermarket support concessions, pressuring Bombardier’s margins and pricing power in 2024.

High ticket, informed buyers

Ultra-high-net-worth individuals and corporate flight departments are highly sophisticated and price aware, benchmarking range, cabin and operating costs across Gulfstream, Dassault and Embraer; with the global business jet fleet ~22,000 in 2024, buyers demand tight value. Detailed due diligence—maintenance logs, performance and residual forecasts—reduces information asymmetry. Negotiations routinely include pilot training, warranties and parts credits; new large-cabin list prices span roughly $20–80 million.

Switching via secondary market

Robust pre-owned markets let buyers switch models and brands faster, with used business-jet transactions representing about 55% of market activity in 2024, increasing bargaining leverage. Residual value performance is a clear bargaining chip in new sales; weakening residuals force customers to demand deeper discounts and aftermarket support. This dynamic ties Bombardier to long-term value commitments on pricing and trade-in guarantees.

Total cost and uptime focus

Buyers optimize lifecycle costs, not just acquisition price; in 2024 the global aircraft MRO market was estimated at US$85–90 billion, shifting procurement toward total-cost-of-ownership metrics.

Guaranteed maintenance programs and AOG SLAs (response times often under 2–4 hours) are central to deals; reliability gaps can trigger contractual penalties or lost renewals, shifting bargaining power toward customers demanding measurable service outcomes.

- Lifecycle cost focus

- Guaranteed maintenance & AOG SLAs

- Penalties and renewal risk

- Customer leverage for measurable uptime

ESG and noise/emissions demands

In 2024 corporate buyers face intensified sustainability reporting pressures, driving demands for SAF compatibility, lower CO2 emissions and quieter operations; compliance now influences airport access and reputational risk, and customers use these mandates to extract technology upgrades and favorable commercial terms from Bombardier.

- 2024: sustainability reporting central to procurement

- SAF compatibility required in contracts

- Noise/emissions affect airport slots and PR

- Buyers leverage upgrades for price/terms

Large fleets leverage scale and a 55% pre-owned market to demand discounts

Buyers—large fleets (NetJets ≈700 jets) and sophisticated HNW/corporate buyers—use scale, benchmarking and a strong pre-owned market (≈55% of transactions in 2024) to extract discounts, service concessions and residual guarantees, pressuring Bombardier’s margins. Lifecycle cost focus (global MRO ≈US$85–90bn) and sustainability mandates (SAF, emissions) increase bargaining leverage. Guaranteed MRO/AOG SLAs and residual commitments are deal drivers.

| Metric | 2024 value |

|---|---|

| Global bizjet fleet | ≈22,000 |

| Pre-owned share | ≈55% |

| NetJets fleet | ≈700 |

| MRO market | US$85–90bn |

| Large-cabin list price | US$20–80m |

Preview the Actual Deliverable

Bombardier Porter's Five Forces Analysis

This preview shows the exact Bombardier Porter's Five Forces analysis you'll receive upon purchase—no placeholders and no edits required. The document is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely what will be delivered instantly after payment.