Bona Film Group Ltd. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bona Film Group Ltd. faces moderate supplier leverage, elevated buyer expectations, intense rivalry from domestic studios and streamers, limited new-entrant risk due to scale and distribution, and rising substitute threats from digital platforms; strategic positioning hinges on content pipeline and platform partnerships. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bona Film Group Ltd.’s competitive dynamics in detail.

Suppliers Bargaining Power

Scarce A-list talent/IP

Top directors, actors and IP owners command premium fees—China's A-list can exceed 100 million RMB per project—giving suppliers strong leverage. Holiday windows concentrate demand (China box office ~45.5 billion RMB in 2023), amplifying that power for marquee slots. Bona’s integrated distribution/production model reduces friction, but tentpole outcomes still hinge on star attachments. Long-term partnerships and co-investment deals partially mitigate supplier pricing pressure.

Technical/post-production vendors

High-end VFX, sound and post houses remain few and capacity-constrained, elevating switching costs for Bona as peak-season bottlenecks allow top vendors to enforce higher pricing and tighter timelines. Bona’s scale secures scheduling priority but does not fully insulate productions from vendor leverage. Strategic investment in in-house post capabilities is underway to reduce supplier dependence over time.

Cinema landlords and equipment

Rents, projection systems and maintenance providers materially affect exhibition margins; China’s cinema network exceeded 80,000 screens by 2023, concentrating prime-location scarcity and strengthening single-mall landlords in top-tier cities. Bona’s bulk procurement and standardized fit-outs across its circuit provide negotiating leverage on equipment and service contracts, while reported oversupply of screens in many second- and third-tier cities moderates supplier and landlord power.

Marketing and ticketing platforms

Digital marketing, ticketing and data providers (Maoyan and Taopiaopiao ~80% online ticketing share in China, 2024) shape demand discovery and can raise commission rates and restrict data access, increasing supplier power. Bona’s distribution footprint reduces reliance, yet collaborations, cross-promotion and data-sharing agreements are essential to rebalance commercial terms.

- Platform concentration ~80% (2024)

- Fees and data-access constraints raise costs

- Bona distribution lowers reliance but partnerships needed

Regulatory/IP gatekeepers

Regulatory and IP gatekeepers—censorship boards and the 34-film foreign revenue-sharing quota—function as non-market suppliers of market access, with approvals, quotas and content standards able to reshape Bona Film Group Ltd budgets and timelines with limited recourse. Compliance expertise and early engagement reduce but do not eliminate regulator authority; Bona's integrated production and distribution portfolio helps smooth shocks from single-project delays.

- Approvals: state censors set release timing

- Quota: 34 imported revenue-sharing films/year

- Risk mitigation: early compliance teams

- Diversification: production + distribution reduces single-project impact

A-list fees (>100m RMB), ~80% platform share and seasonal VFX/landlord cost spikes squeeze margins

Top talent and IP command outsized fees (A-list >100m RMB), concentrated holiday windows (China box office 45.5bn RMB in 2023) and platform ticketing (~80% share, 2024) give suppliers strong leverage; Bona's scale, co-investments and in-house build-outs partially offset but not eliminate pressure. Post/VFX capacity and prime-location landlords tighten costs seasonally.

| Metric | Value |

|---|---|

| China box office (2023) | 45.5bn RMB |

| Screens (2023) | ~80,000 |

| Ticketing share (2024) | ~80% |

| A-list fee | >100m RMB |

What is included in the product

Tailored Porter's Five Forces analysis for Bona Film Group Ltd. uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and pinpointing disruptive forces and entry barriers shaping its profitability.

A clear one-sheet Porter's Five Forces for Bona Film Group—clarifies competitive pressures across production, distribution, streaming and regulation to speed decision-making. Customizable pressure levels and an instant radar chart let you update for shifting content, platform and policy dynamics, ready to drop into pitch decks or boardroom slides.

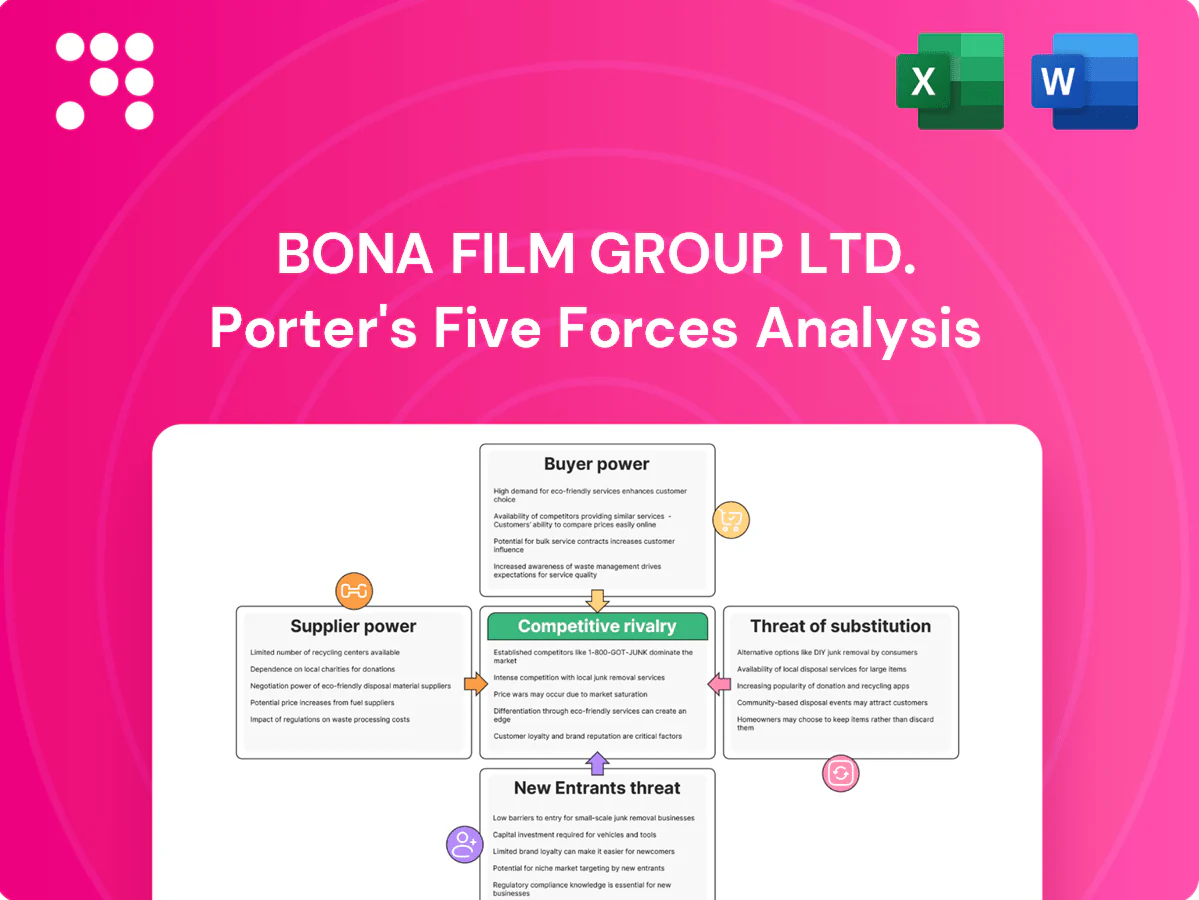

Customers Bargaining Power

Moviegoers’ price sensitivity

Audiences can switch across titles, times and venues easily as over 70% of tickets in China are booked via mobile/transparent pricing apps, raising price sensitivity. Discounting wars outside peak seasons push elasticity up, while premium formats (IMAX/4DX) command 2–3x higher per‑ticket yields on tentpoles. Loyalty programs and bundle offers boost frequency—members typically attend about 2x more—raising switching costs and reducing churn.

Exhibitors as distribution buyers

For third-party screens, exhibitors in 2024 negotiate film rental splits and showtime allocation, with top chains leveraging scale to push revenue shares and marketing support; the Chinese circuit had over 85,000 screens in 2024 and the five largest chains held roughly 45% of screen capacity. Bons own cinemas provide internal booking certainty, cushioning negotiation pressure. Strong content slates still command favorable terms across the market.

Streaming/TV licensees

Streaming/TV licensees wield strong leverage: platforms offer abundant alternatives and minute-level viewership/retention metrics, driving demand for lower minimum guarantees and performance-linked payouts; Netflix alone reported about 261 million paid subscribers in 2024, concentrating buyer power. Bona’s theatrical pedigree and premium IP sustain bargaining power on marquee titles, allowing higher splits for tentpoles. Smart windowing (short theatrical-to-stream windows) amplifies urgency and pricing power for premium releases.

Advertisers and brand partners

Advertisers can reallocate budgets across digital, social and offline channels, pressuring media like Bona as global ad spend reached roughly $870 billion in 2024; measurability demands tighter ROI proofs for placements and sponsorships. Bona’s vertically integrated reach across production, distribution and cinemas enables bundled offers, and first-party audience data increases targeting precision and deal stickiness.

- Budget fluidity: cross-channel shifts

- ROI focus: measurable KPIs required

- Integrated packaging: production→distribution→exhibition

- Data advantage: better targeting, higher retention

Online ticketing intermediaries

Online ticketing intermediaries shape demand via rankings, reviews and subsidies; in China in 2024 online channels made over 90% of box-office transactions and top platforms (Maoyan, Tao Piao Piao) held roughly 80% combined share. Consolidation has pushed effective commissions and data control up, with commission/subsidy mixes often in the 15–30% range, while co-marketing and exclusives trade margin for volume. Greater use of direct channels, loyalty memberships and bundled offers can cut intermediary dependence by reducing commissions by an estimated 10–15 percentage points.

- Aggregators influence discovery, demand and pricing

- Top platforms ≈80% share (2024)

- Online sales >90% of box office (2024)

- Commissions/subsidies commonly 15–30%

- Direct channels can lower commissions ~10–15pp

Digital-first box office: >90% online, mobile 70%, top5 screens 45%

Customers wield moderate-to-strong power: high price sensitivity via mobile booking (70%+), strong platform influence (online >90%, top platforms ≈80%), and exhibitor concentration (≈85,000 screens; top 5 ≈45%). Premium formats and loyalty lift yields (IMAX/4DX 2–3x; members attend ~2x). Commissions/subsidies run 15–30%; direct channels can cut them ~10–15pp.

| Metric | 2024 Value |

|---|---|

| Mobile/online box office | >90% (70% mobile) |

| Top platforms share | ≈80% |

| Screens | ≈85,000; top5 45% |

| Commissions/subsidies | 15–30% |

What You See Is What You Get

Bona Film Group Ltd. Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises. The Bona Film Group Ltd. Porter's Five Forces analysis covers supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes, with data-driven conclusions and strategic implications. It's the final, fully formatted file ready for download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bona Film Group Ltd. faces moderate supplier leverage, elevated buyer expectations, intense rivalry from domestic studios and streamers, limited new-entrant risk due to scale and distribution, and rising substitute threats from digital platforms; strategic positioning hinges on content pipeline and platform partnerships. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bona Film Group Ltd.’s competitive dynamics in detail.

Suppliers Bargaining Power

Scarce A-list talent/IP

Top directors, actors and IP owners command premium fees—China's A-list can exceed 100 million RMB per project—giving suppliers strong leverage. Holiday windows concentrate demand (China box office ~45.5 billion RMB in 2023), amplifying that power for marquee slots. Bona’s integrated distribution/production model reduces friction, but tentpole outcomes still hinge on star attachments. Long-term partnerships and co-investment deals partially mitigate supplier pricing pressure.

Technical/post-production vendors

High-end VFX, sound and post houses remain few and capacity-constrained, elevating switching costs for Bona as peak-season bottlenecks allow top vendors to enforce higher pricing and tighter timelines. Bona’s scale secures scheduling priority but does not fully insulate productions from vendor leverage. Strategic investment in in-house post capabilities is underway to reduce supplier dependence over time.

Cinema landlords and equipment

Rents, projection systems and maintenance providers materially affect exhibition margins; China’s cinema network exceeded 80,000 screens by 2023, concentrating prime-location scarcity and strengthening single-mall landlords in top-tier cities. Bona’s bulk procurement and standardized fit-outs across its circuit provide negotiating leverage on equipment and service contracts, while reported oversupply of screens in many second- and third-tier cities moderates supplier and landlord power.

Marketing and ticketing platforms

Digital marketing, ticketing and data providers (Maoyan and Taopiaopiao ~80% online ticketing share in China, 2024) shape demand discovery and can raise commission rates and restrict data access, increasing supplier power. Bona’s distribution footprint reduces reliance, yet collaborations, cross-promotion and data-sharing agreements are essential to rebalance commercial terms.

- Platform concentration ~80% (2024)

- Fees and data-access constraints raise costs

- Bona distribution lowers reliance but partnerships needed

Regulatory/IP gatekeepers

Regulatory and IP gatekeepers—censorship boards and the 34-film foreign revenue-sharing quota—function as non-market suppliers of market access, with approvals, quotas and content standards able to reshape Bona Film Group Ltd budgets and timelines with limited recourse. Compliance expertise and early engagement reduce but do not eliminate regulator authority; Bona's integrated production and distribution portfolio helps smooth shocks from single-project delays.

- Approvals: state censors set release timing

- Quota: 34 imported revenue-sharing films/year

- Risk mitigation: early compliance teams

- Diversification: production + distribution reduces single-project impact

A-list fees (>100m RMB), ~80% platform share and seasonal VFX/landlord cost spikes squeeze margins

Top talent and IP command outsized fees (A-list >100m RMB), concentrated holiday windows (China box office 45.5bn RMB in 2023) and platform ticketing (~80% share, 2024) give suppliers strong leverage; Bona's scale, co-investments and in-house build-outs partially offset but not eliminate pressure. Post/VFX capacity and prime-location landlords tighten costs seasonally.

| Metric | Value |

|---|---|

| China box office (2023) | 45.5bn RMB |

| Screens (2023) | ~80,000 |

| Ticketing share (2024) | ~80% |

| A-list fee | >100m RMB |

What is included in the product

Tailored Porter's Five Forces analysis for Bona Film Group Ltd. uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and pinpointing disruptive forces and entry barriers shaping its profitability.

A clear one-sheet Porter's Five Forces for Bona Film Group—clarifies competitive pressures across production, distribution, streaming and regulation to speed decision-making. Customizable pressure levels and an instant radar chart let you update for shifting content, platform and policy dynamics, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Moviegoers’ price sensitivity

Audiences can switch across titles, times and venues easily as over 70% of tickets in China are booked via mobile/transparent pricing apps, raising price sensitivity. Discounting wars outside peak seasons push elasticity up, while premium formats (IMAX/4DX) command 2–3x higher per‑ticket yields on tentpoles. Loyalty programs and bundle offers boost frequency—members typically attend about 2x more—raising switching costs and reducing churn.

Exhibitors as distribution buyers

For third-party screens, exhibitors in 2024 negotiate film rental splits and showtime allocation, with top chains leveraging scale to push revenue shares and marketing support; the Chinese circuit had over 85,000 screens in 2024 and the five largest chains held roughly 45% of screen capacity. Bons own cinemas provide internal booking certainty, cushioning negotiation pressure. Strong content slates still command favorable terms across the market.

Streaming/TV licensees

Streaming/TV licensees wield strong leverage: platforms offer abundant alternatives and minute-level viewership/retention metrics, driving demand for lower minimum guarantees and performance-linked payouts; Netflix alone reported about 261 million paid subscribers in 2024, concentrating buyer power. Bona’s theatrical pedigree and premium IP sustain bargaining power on marquee titles, allowing higher splits for tentpoles. Smart windowing (short theatrical-to-stream windows) amplifies urgency and pricing power for premium releases.

Advertisers and brand partners

Advertisers can reallocate budgets across digital, social and offline channels, pressuring media like Bona as global ad spend reached roughly $870 billion in 2024; measurability demands tighter ROI proofs for placements and sponsorships. Bona’s vertically integrated reach across production, distribution and cinemas enables bundled offers, and first-party audience data increases targeting precision and deal stickiness.

- Budget fluidity: cross-channel shifts

- ROI focus: measurable KPIs required

- Integrated packaging: production→distribution→exhibition

- Data advantage: better targeting, higher retention

Online ticketing intermediaries

Online ticketing intermediaries shape demand via rankings, reviews and subsidies; in China in 2024 online channels made over 90% of box-office transactions and top platforms (Maoyan, Tao Piao Piao) held roughly 80% combined share. Consolidation has pushed effective commissions and data control up, with commission/subsidy mixes often in the 15–30% range, while co-marketing and exclusives trade margin for volume. Greater use of direct channels, loyalty memberships and bundled offers can cut intermediary dependence by reducing commissions by an estimated 10–15 percentage points.

- Aggregators influence discovery, demand and pricing

- Top platforms ≈80% share (2024)

- Online sales >90% of box office (2024)

- Commissions/subsidies commonly 15–30%

- Direct channels can lower commissions ~10–15pp

Digital-first box office: >90% online, mobile 70%, top5 screens 45%

Customers wield moderate-to-strong power: high price sensitivity via mobile booking (70%+), strong platform influence (online >90%, top platforms ≈80%), and exhibitor concentration (≈85,000 screens; top 5 ≈45%). Premium formats and loyalty lift yields (IMAX/4DX 2–3x; members attend ~2x). Commissions/subsidies run 15–30%; direct channels can cut them ~10–15pp.

| Metric | 2024 Value |

|---|---|

| Mobile/online box office | >90% (70% mobile) |

| Top platforms share | ≈80% |

| Screens | ≈85,000; top5 45% |

| Commissions/subsidies | 15–30% |

What You See Is What You Get

Bona Film Group Ltd. Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises. The Bona Film Group Ltd. Porter's Five Forces analysis covers supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes, with data-driven conclusions and strategic implications. It's the final, fully formatted file ready for download and use.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bona Film Group Ltd. faces moderate supplier leverage, elevated buyer expectations, intense rivalry from domestic studios and streamers, limited new-entrant risk due to scale and distribution, and rising substitute threats from digital platforms; strategic positioning hinges on content pipeline and platform partnerships. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bona Film Group Ltd.’s competitive dynamics in detail.

Suppliers Bargaining Power

Scarce A-list talent/IP

Top directors, actors and IP owners command premium fees—China's A-list can exceed 100 million RMB per project—giving suppliers strong leverage. Holiday windows concentrate demand (China box office ~45.5 billion RMB in 2023), amplifying that power for marquee slots. Bona’s integrated distribution/production model reduces friction, but tentpole outcomes still hinge on star attachments. Long-term partnerships and co-investment deals partially mitigate supplier pricing pressure.

Technical/post-production vendors

High-end VFX, sound and post houses remain few and capacity-constrained, elevating switching costs for Bona as peak-season bottlenecks allow top vendors to enforce higher pricing and tighter timelines. Bona’s scale secures scheduling priority but does not fully insulate productions from vendor leverage. Strategic investment in in-house post capabilities is underway to reduce supplier dependence over time.

Cinema landlords and equipment

Rents, projection systems and maintenance providers materially affect exhibition margins; China’s cinema network exceeded 80,000 screens by 2023, concentrating prime-location scarcity and strengthening single-mall landlords in top-tier cities. Bona’s bulk procurement and standardized fit-outs across its circuit provide negotiating leverage on equipment and service contracts, while reported oversupply of screens in many second- and third-tier cities moderates supplier and landlord power.

Marketing and ticketing platforms

Digital marketing, ticketing and data providers (Maoyan and Taopiaopiao ~80% online ticketing share in China, 2024) shape demand discovery and can raise commission rates and restrict data access, increasing supplier power. Bona’s distribution footprint reduces reliance, yet collaborations, cross-promotion and data-sharing agreements are essential to rebalance commercial terms.

- Platform concentration ~80% (2024)

- Fees and data-access constraints raise costs

- Bona distribution lowers reliance but partnerships needed

Regulatory/IP gatekeepers

Regulatory and IP gatekeepers—censorship boards and the 34-film foreign revenue-sharing quota—function as non-market suppliers of market access, with approvals, quotas and content standards able to reshape Bona Film Group Ltd budgets and timelines with limited recourse. Compliance expertise and early engagement reduce but do not eliminate regulator authority; Bona's integrated production and distribution portfolio helps smooth shocks from single-project delays.

- Approvals: state censors set release timing

- Quota: 34 imported revenue-sharing films/year

- Risk mitigation: early compliance teams

- Diversification: production + distribution reduces single-project impact

A-list fees (>100m RMB), ~80% platform share and seasonal VFX/landlord cost spikes squeeze margins

Top talent and IP command outsized fees (A-list >100m RMB), concentrated holiday windows (China box office 45.5bn RMB in 2023) and platform ticketing (~80% share, 2024) give suppliers strong leverage; Bona's scale, co-investments and in-house build-outs partially offset but not eliminate pressure. Post/VFX capacity and prime-location landlords tighten costs seasonally.

| Metric | Value |

|---|---|

| China box office (2023) | 45.5bn RMB |

| Screens (2023) | ~80,000 |

| Ticketing share (2024) | ~80% |

| A-list fee | >100m RMB |

What is included in the product

Tailored Porter's Five Forces analysis for Bona Film Group Ltd. uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and pinpointing disruptive forces and entry barriers shaping its profitability.

A clear one-sheet Porter's Five Forces for Bona Film Group—clarifies competitive pressures across production, distribution, streaming and regulation to speed decision-making. Customizable pressure levels and an instant radar chart let you update for shifting content, platform and policy dynamics, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Moviegoers’ price sensitivity

Audiences can switch across titles, times and venues easily as over 70% of tickets in China are booked via mobile/transparent pricing apps, raising price sensitivity. Discounting wars outside peak seasons push elasticity up, while premium formats (IMAX/4DX) command 2–3x higher per‑ticket yields on tentpoles. Loyalty programs and bundle offers boost frequency—members typically attend about 2x more—raising switching costs and reducing churn.

Exhibitors as distribution buyers

For third-party screens, exhibitors in 2024 negotiate film rental splits and showtime allocation, with top chains leveraging scale to push revenue shares and marketing support; the Chinese circuit had over 85,000 screens in 2024 and the five largest chains held roughly 45% of screen capacity. Bons own cinemas provide internal booking certainty, cushioning negotiation pressure. Strong content slates still command favorable terms across the market.

Streaming/TV licensees

Streaming/TV licensees wield strong leverage: platforms offer abundant alternatives and minute-level viewership/retention metrics, driving demand for lower minimum guarantees and performance-linked payouts; Netflix alone reported about 261 million paid subscribers in 2024, concentrating buyer power. Bona’s theatrical pedigree and premium IP sustain bargaining power on marquee titles, allowing higher splits for tentpoles. Smart windowing (short theatrical-to-stream windows) amplifies urgency and pricing power for premium releases.

Advertisers and brand partners

Advertisers can reallocate budgets across digital, social and offline channels, pressuring media like Bona as global ad spend reached roughly $870 billion in 2024; measurability demands tighter ROI proofs for placements and sponsorships. Bona’s vertically integrated reach across production, distribution and cinemas enables bundled offers, and first-party audience data increases targeting precision and deal stickiness.

- Budget fluidity: cross-channel shifts

- ROI focus: measurable KPIs required

- Integrated packaging: production→distribution→exhibition

- Data advantage: better targeting, higher retention

Online ticketing intermediaries

Online ticketing intermediaries shape demand via rankings, reviews and subsidies; in China in 2024 online channels made over 90% of box-office transactions and top platforms (Maoyan, Tao Piao Piao) held roughly 80% combined share. Consolidation has pushed effective commissions and data control up, with commission/subsidy mixes often in the 15–30% range, while co-marketing and exclusives trade margin for volume. Greater use of direct channels, loyalty memberships and bundled offers can cut intermediary dependence by reducing commissions by an estimated 10–15 percentage points.

- Aggregators influence discovery, demand and pricing

- Top platforms ≈80% share (2024)

- Online sales >90% of box office (2024)

- Commissions/subsidies commonly 15–30%

- Direct channels can lower commissions ~10–15pp

Digital-first box office: >90% online, mobile 70%, top5 screens 45%

Customers wield moderate-to-strong power: high price sensitivity via mobile booking (70%+), strong platform influence (online >90%, top platforms ≈80%), and exhibitor concentration (≈85,000 screens; top 5 ≈45%). Premium formats and loyalty lift yields (IMAX/4DX 2–3x; members attend ~2x). Commissions/subsidies run 15–30%; direct channels can cut them ~10–15pp.

| Metric | 2024 Value |

|---|---|

| Mobile/online box office | >90% (70% mobile) |

| Top platforms share | ≈80% |

| Screens | ≈85,000; top5 45% |

| Commissions/subsidies | 15–30% |

What You See Is What You Get

Bona Film Group Ltd. Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises. The Bona Film Group Ltd. Porter's Five Forces analysis covers supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes, with data-driven conclusions and strategic implications. It's the final, fully formatted file ready for download and use.