Bank of Queensland Boston Consulting Group Matrix

Actionable Strategy Starts Here

Curious where Bank of Queensland’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases the strategic shape, but the full BCG Matrix gives you quadrant-by-quadrant placement, data-backed recommendations, and clear moves to reallocate capital or double down. Buy the full BCG Matrix to get a detailed Word report plus a concise Excel summary—ready to use in board decks and planning sessions. Purchase now and cut straight to competitive clarity.

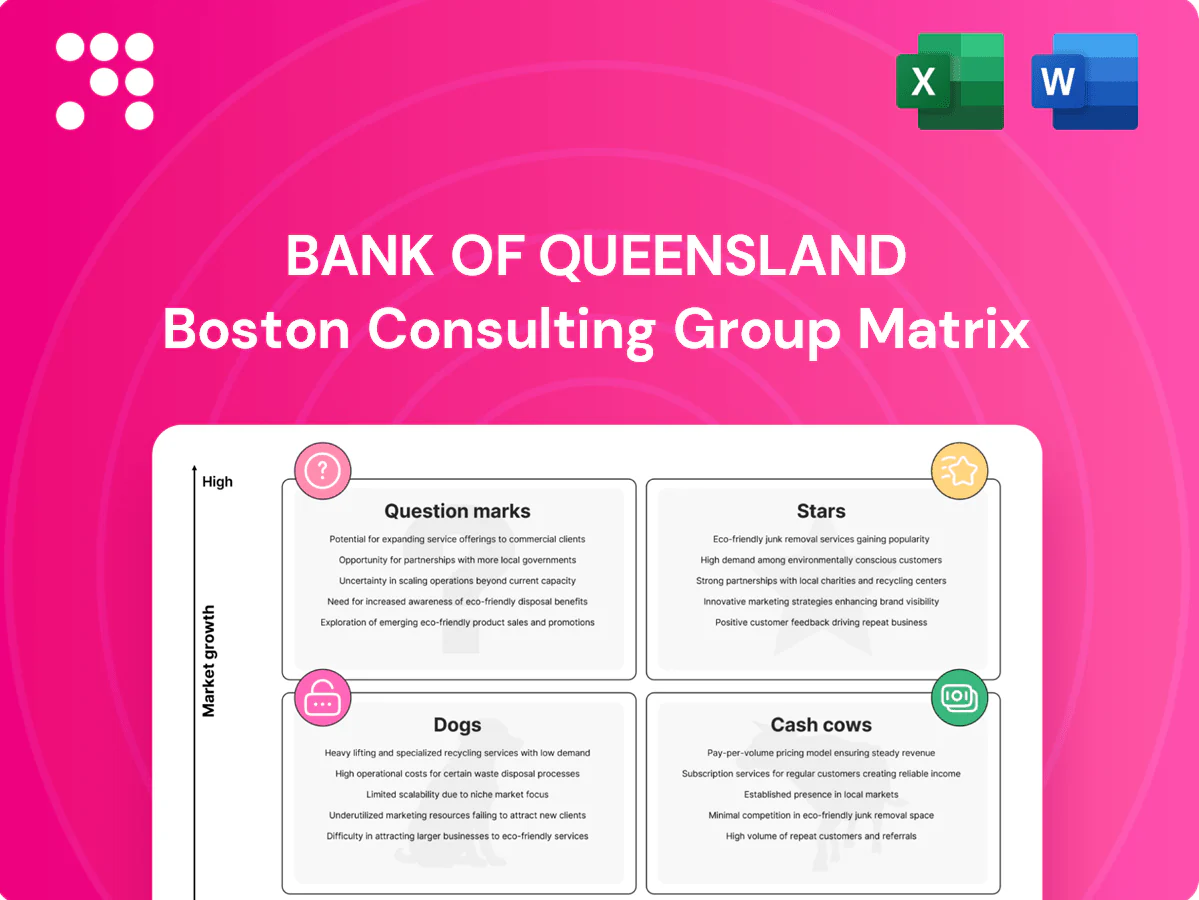

Stars

Owner-managed branches (relationship-led growth)

BOQ’s franchise-style, owner-managed network of 167 branches continues to punch above its weight, delivering relationship-led growth where personal service still wins; owner-managed branches outperformed network averages in 2024. In growth corridors and regional hubs, these branches capture outsized share as big banks centralize, helping BOQ sustain lending momentum. Keep fueling local marketing and banker productivity; hold the share while regional markets expand and this stays a star that compounds.

SME lending in niche local markets

Australian Bureau of Statistics records about 2.4 million actively trading businesses, underpinning rising small business credit demand; BOQ’s branch-led model and local bankers deliver higher conversion rates in niche markets. Fast decisions plus local knowledge create a durable moat the majors struggle to replicate; allocate capital to underwriting tech and sector-specialist pods to scale. Preserve sub-48-hour turnaround targets and strict pricing discipline to expand without blowups.

Broker-channel home loans (acquisition engine)

Brokers now handle about 64% of Australia’s mortgage flow (MFAA 2024), making BOQ’s broker-channel a clear Star if it leverages superior service to win repeat volume. The market is growing and share is attainable with sharp SLAs; priority actions: accelerate credit decisioning and settlement speed. Maintain margin hygiene—Stars can burn cash if pricing loosens.

Digital savings and everyday accounts

Digital savings and everyday accounts are a Star for BOQ as deposit-gathering returns amid higher-for-longer rates; Australian household deposit balances rose through 2024 with retail savings rates commonly above 4%, making sticky, low-cost funding achievable. Strong app UX and fair rates drive retention; iterate budgets, round-ups and alerts and cut switching friction to scale and lower unit costs, creating a durable funding edge.

- Deposit tailwind: higher retail savings yields in 2024

- Retention drivers: app UX, fair rates, feature set

- Execution: reduce switch friction, scale to lower unit cost

Merchant services via partnerships

Card acceptance is rising as cash declines, with contactless payments accounting for about 80% of in-person card transactions in Australia in 2024; BOQ can ride partner rails to win SMEs at point of sale. Bundle pricing with accounts and lending to lock in LTV, and invest in fast onboarding plus dispute tooling to boost merchant retention and lifetime value.

- Partner rails to acquire SMEs at POS

- Bundle accounts+lending to raise LTV

- Prioritise onboarding speed

- Invest in dispute and reconciliation tooling

Local branches win: owner-managed footprint grows as brokers and contactless surge

BOQ’s 167 owner‑managed branches outperformed network averages in 2024, capturing regional share as majors centralise; ABS cites ~2.4m active businesses supporting SME credit growth. Brokers handle ~64% of mortgage flow (MFAA 2024), making broker channel a Star; contactless payments ~80% of in-person card transactions (2024). Retail savings rates >4% in 2024 fuel digital deposit growth—prioritise speed, UX and pricing discipline.

| Metric | 2024 value | Relevance |

|---|---|---|

| Branches | 167 | Local market share |

| Active businesses | 2.4m | SME demand |

| Broker share | 64% | Mortgage growth |

| Contactless | 80% | POS product |

| Retail savings | >4% | Sticky funding |

What is included in the product

BCG Matrix review of Bank of Queensland’s units—Stars, Cash Cows, Question Marks, Dogs—with investment, hold, or divest guidance.

One-page BCG Matrix for Bank of Queensland — places each business unit in a quadrant to spot growth gaps fast.

Cash Cows

Prime home loan book (seasoned portfolio)

Seasoned prime mortgages deliver steady interest income and low loss rates (Australian mortgage default rates around 0.1% in 2024), forming BOQ’s funding flywheel for lending and treasury. Prioritise repricing cadence, retention and offset penetration to protect NIMs. Minimal promotional spend required; focus on lowering cost-to-serve and tight arrears management to preserve cash generation.

Personal transaction accounts

Personal transaction accounts are a cash cow for Bank of Queensland, driving interchange revenue and supplying low-cost deposits to support lending; BOQ reported a retail deposit base of about A$53 billion in FY2024, making growth modest but the base large and predictable. Nudge digital engagement and cross-sell at onboarding and payroll moments to lift wallet share. Keep fraud losses tight and simplify fees to avoid churn.

Term deposits (stable funding base)

Term deposits are a mature, rate-sensitive and dependable funding source for Bank of Queensland, delivering predictable cash flow when priced to market and anchored by conservative repricing profiles.

Not flashy but critical for balance sheet stability, targeted tenors are used to smooth funding gaps between wholesale and transaction balances.

Automating rollovers and reducing manual operations keeps administration costs low and preserves term deposits as a cash-generative pillar of funding strategy.

Equipment and asset finance (seasoned niches)

Established broker and direct channels deliver consistent yields in known categories, with BOQ equipment and asset finance showing stable returns and a portfolio balance around A$3.2bn in 2024 and a reported loss rate near 0.2%, reflecting seasoned lending quality.

Portfolio seasoning keeps losses low; tightening residual risk and revaluing collateral reduced downside in 2024, while incremental tech investment shaved turnaround times and improved margins without heavy marketing spend.

- Channels: broker + direct

- 2024 balance: A$3.2bn

- Loss rate: ~0.2%

- Actions: tighter residuals, collateral revals, tech-led efficiency

Basic business transaction accounts

Basic SME operating accounts are high-retention, low-fee cash cows for BOQ, serving as a prime cross-sell gateway into lending, cards and merchant services while requiring minimal servicing margins.

- Maintain: prioritise transparent, fair pricing to retain stickiness

- Scale: streamline onboarding and alerts to cut call-centre load

- Upsell: use accounts as feeder for higher-margin products

Mortgages, A$53bn deposits & equipment finance: steady NII repricing focus

Seasoned mortgages, retail deposits and term deposits form BOQ’s cash cows, delivering steady NII with mortgage default ~0.1% in 2024 and retail deposits ~A$53bn (FY2024). Equipment & asset finance (~A$3.2bn, loss ~0.2%) and SME accounts add stable low-cost funding and cross-sell channels. Focus on repricing, cost-to-serve, automation and tight arrears/fraud control to protect margins.

| Asset | 2024 metric | Role |

|---|---|---|

| Mortgages | Default ~0.1% | Core NII |

| Retail deposits | A$53bn | Low-cost funding |

| Equipment finance | A$3.2bn / 0.2% loss | Stable yield |

Delivered as Shown

Bank of Queensland BCG Matrix

The file you’re previewing here is the exact BCG Matrix report you’ll receive after purchase — no watermarks, no demo text, just the finished, fully formatted document. It’s built for strategic clarity with market-backed analysis and clean visuals ready for presentation. Buy once and download immediately; the file is editable, printable, and plug-and-play for your planning or investor decks.

Actionable Strategy Starts Here

Curious where Bank of Queensland’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases the strategic shape, but the full BCG Matrix gives you quadrant-by-quadrant placement, data-backed recommendations, and clear moves to reallocate capital or double down. Buy the full BCG Matrix to get a detailed Word report plus a concise Excel summary—ready to use in board decks and planning sessions. Purchase now and cut straight to competitive clarity.

Stars

Owner-managed branches (relationship-led growth)

BOQ’s franchise-style, owner-managed network of 167 branches continues to punch above its weight, delivering relationship-led growth where personal service still wins; owner-managed branches outperformed network averages in 2024. In growth corridors and regional hubs, these branches capture outsized share as big banks centralize, helping BOQ sustain lending momentum. Keep fueling local marketing and banker productivity; hold the share while regional markets expand and this stays a star that compounds.

SME lending in niche local markets

Australian Bureau of Statistics records about 2.4 million actively trading businesses, underpinning rising small business credit demand; BOQ’s branch-led model and local bankers deliver higher conversion rates in niche markets. Fast decisions plus local knowledge create a durable moat the majors struggle to replicate; allocate capital to underwriting tech and sector-specialist pods to scale. Preserve sub-48-hour turnaround targets and strict pricing discipline to expand without blowups.

Broker-channel home loans (acquisition engine)

Brokers now handle about 64% of Australia’s mortgage flow (MFAA 2024), making BOQ’s broker-channel a clear Star if it leverages superior service to win repeat volume. The market is growing and share is attainable with sharp SLAs; priority actions: accelerate credit decisioning and settlement speed. Maintain margin hygiene—Stars can burn cash if pricing loosens.

Digital savings and everyday accounts

Digital savings and everyday accounts are a Star for BOQ as deposit-gathering returns amid higher-for-longer rates; Australian household deposit balances rose through 2024 with retail savings rates commonly above 4%, making sticky, low-cost funding achievable. Strong app UX and fair rates drive retention; iterate budgets, round-ups and alerts and cut switching friction to scale and lower unit costs, creating a durable funding edge.

- Deposit tailwind: higher retail savings yields in 2024

- Retention drivers: app UX, fair rates, feature set

- Execution: reduce switch friction, scale to lower unit cost

Merchant services via partnerships

Card acceptance is rising as cash declines, with contactless payments accounting for about 80% of in-person card transactions in Australia in 2024; BOQ can ride partner rails to win SMEs at point of sale. Bundle pricing with accounts and lending to lock in LTV, and invest in fast onboarding plus dispute tooling to boost merchant retention and lifetime value.

- Partner rails to acquire SMEs at POS

- Bundle accounts+lending to raise LTV

- Prioritise onboarding speed

- Invest in dispute and reconciliation tooling

Local branches win: owner-managed footprint grows as brokers and contactless surge

BOQ’s 167 owner‑managed branches outperformed network averages in 2024, capturing regional share as majors centralise; ABS cites ~2.4m active businesses supporting SME credit growth. Brokers handle ~64% of mortgage flow (MFAA 2024), making broker channel a Star; contactless payments ~80% of in-person card transactions (2024). Retail savings rates >4% in 2024 fuel digital deposit growth—prioritise speed, UX and pricing discipline.

| Metric | 2024 value | Relevance |

|---|---|---|

| Branches | 167 | Local market share |

| Active businesses | 2.4m | SME demand |

| Broker share | 64% | Mortgage growth |

| Contactless | 80% | POS product |

| Retail savings | >4% | Sticky funding |

What is included in the product

BCG Matrix review of Bank of Queensland’s units—Stars, Cash Cows, Question Marks, Dogs—with investment, hold, or divest guidance.

One-page BCG Matrix for Bank of Queensland — places each business unit in a quadrant to spot growth gaps fast.

Cash Cows

Prime home loan book (seasoned portfolio)

Seasoned prime mortgages deliver steady interest income and low loss rates (Australian mortgage default rates around 0.1% in 2024), forming BOQ’s funding flywheel for lending and treasury. Prioritise repricing cadence, retention and offset penetration to protect NIMs. Minimal promotional spend required; focus on lowering cost-to-serve and tight arrears management to preserve cash generation.

Personal transaction accounts

Personal transaction accounts are a cash cow for Bank of Queensland, driving interchange revenue and supplying low-cost deposits to support lending; BOQ reported a retail deposit base of about A$53 billion in FY2024, making growth modest but the base large and predictable. Nudge digital engagement and cross-sell at onboarding and payroll moments to lift wallet share. Keep fraud losses tight and simplify fees to avoid churn.

Term deposits (stable funding base)

Term deposits are a mature, rate-sensitive and dependable funding source for Bank of Queensland, delivering predictable cash flow when priced to market and anchored by conservative repricing profiles.

Not flashy but critical for balance sheet stability, targeted tenors are used to smooth funding gaps between wholesale and transaction balances.

Automating rollovers and reducing manual operations keeps administration costs low and preserves term deposits as a cash-generative pillar of funding strategy.

Equipment and asset finance (seasoned niches)

Established broker and direct channels deliver consistent yields in known categories, with BOQ equipment and asset finance showing stable returns and a portfolio balance around A$3.2bn in 2024 and a reported loss rate near 0.2%, reflecting seasoned lending quality.

Portfolio seasoning keeps losses low; tightening residual risk and revaluing collateral reduced downside in 2024, while incremental tech investment shaved turnaround times and improved margins without heavy marketing spend.

- Channels: broker + direct

- 2024 balance: A$3.2bn

- Loss rate: ~0.2%

- Actions: tighter residuals, collateral revals, tech-led efficiency

Basic business transaction accounts

Basic SME operating accounts are high-retention, low-fee cash cows for BOQ, serving as a prime cross-sell gateway into lending, cards and merchant services while requiring minimal servicing margins.

- Maintain: prioritise transparent, fair pricing to retain stickiness

- Scale: streamline onboarding and alerts to cut call-centre load

- Upsell: use accounts as feeder for higher-margin products

Mortgages, A$53bn deposits & equipment finance: steady NII repricing focus

Seasoned mortgages, retail deposits and term deposits form BOQ’s cash cows, delivering steady NII with mortgage default ~0.1% in 2024 and retail deposits ~A$53bn (FY2024). Equipment & asset finance (~A$3.2bn, loss ~0.2%) and SME accounts add stable low-cost funding and cross-sell channels. Focus on repricing, cost-to-serve, automation and tight arrears/fraud control to protect margins.

| Asset | 2024 metric | Role |

|---|---|---|

| Mortgages | Default ~0.1% | Core NII |

| Retail deposits | A$53bn | Low-cost funding |

| Equipment finance | A$3.2bn / 0.2% loss | Stable yield |

Delivered as Shown

Bank of Queensland BCG Matrix

The file you’re previewing here is the exact BCG Matrix report you’ll receive after purchase — no watermarks, no demo text, just the finished, fully formatted document. It’s built for strategic clarity with market-backed analysis and clean visuals ready for presentation. Buy once and download immediately; the file is editable, printable, and plug-and-play for your planning or investor decks.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Curious where Bank of Queensland’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases the strategic shape, but the full BCG Matrix gives you quadrant-by-quadrant placement, data-backed recommendations, and clear moves to reallocate capital or double down. Buy the full BCG Matrix to get a detailed Word report plus a concise Excel summary—ready to use in board decks and planning sessions. Purchase now and cut straight to competitive clarity.

Stars

Owner-managed branches (relationship-led growth)

BOQ’s franchise-style, owner-managed network of 167 branches continues to punch above its weight, delivering relationship-led growth where personal service still wins; owner-managed branches outperformed network averages in 2024. In growth corridors and regional hubs, these branches capture outsized share as big banks centralize, helping BOQ sustain lending momentum. Keep fueling local marketing and banker productivity; hold the share while regional markets expand and this stays a star that compounds.

SME lending in niche local markets

Australian Bureau of Statistics records about 2.4 million actively trading businesses, underpinning rising small business credit demand; BOQ’s branch-led model and local bankers deliver higher conversion rates in niche markets. Fast decisions plus local knowledge create a durable moat the majors struggle to replicate; allocate capital to underwriting tech and sector-specialist pods to scale. Preserve sub-48-hour turnaround targets and strict pricing discipline to expand without blowups.

Broker-channel home loans (acquisition engine)

Brokers now handle about 64% of Australia’s mortgage flow (MFAA 2024), making BOQ’s broker-channel a clear Star if it leverages superior service to win repeat volume. The market is growing and share is attainable with sharp SLAs; priority actions: accelerate credit decisioning and settlement speed. Maintain margin hygiene—Stars can burn cash if pricing loosens.

Digital savings and everyday accounts

Digital savings and everyday accounts are a Star for BOQ as deposit-gathering returns amid higher-for-longer rates; Australian household deposit balances rose through 2024 with retail savings rates commonly above 4%, making sticky, low-cost funding achievable. Strong app UX and fair rates drive retention; iterate budgets, round-ups and alerts and cut switching friction to scale and lower unit costs, creating a durable funding edge.

- Deposit tailwind: higher retail savings yields in 2024

- Retention drivers: app UX, fair rates, feature set

- Execution: reduce switch friction, scale to lower unit cost

Merchant services via partnerships

Card acceptance is rising as cash declines, with contactless payments accounting for about 80% of in-person card transactions in Australia in 2024; BOQ can ride partner rails to win SMEs at point of sale. Bundle pricing with accounts and lending to lock in LTV, and invest in fast onboarding plus dispute tooling to boost merchant retention and lifetime value.

- Partner rails to acquire SMEs at POS

- Bundle accounts+lending to raise LTV

- Prioritise onboarding speed

- Invest in dispute and reconciliation tooling

Local branches win: owner-managed footprint grows as brokers and contactless surge

BOQ’s 167 owner‑managed branches outperformed network averages in 2024, capturing regional share as majors centralise; ABS cites ~2.4m active businesses supporting SME credit growth. Brokers handle ~64% of mortgage flow (MFAA 2024), making broker channel a Star; contactless payments ~80% of in-person card transactions (2024). Retail savings rates >4% in 2024 fuel digital deposit growth—prioritise speed, UX and pricing discipline.

| Metric | 2024 value | Relevance |

|---|---|---|

| Branches | 167 | Local market share |

| Active businesses | 2.4m | SME demand |

| Broker share | 64% | Mortgage growth |

| Contactless | 80% | POS product |

| Retail savings | >4% | Sticky funding |

What is included in the product

BCG Matrix review of Bank of Queensland’s units—Stars, Cash Cows, Question Marks, Dogs—with investment, hold, or divest guidance.

One-page BCG Matrix for Bank of Queensland — places each business unit in a quadrant to spot growth gaps fast.

Cash Cows

Prime home loan book (seasoned portfolio)

Seasoned prime mortgages deliver steady interest income and low loss rates (Australian mortgage default rates around 0.1% in 2024), forming BOQ’s funding flywheel for lending and treasury. Prioritise repricing cadence, retention and offset penetration to protect NIMs. Minimal promotional spend required; focus on lowering cost-to-serve and tight arrears management to preserve cash generation.

Personal transaction accounts

Personal transaction accounts are a cash cow for Bank of Queensland, driving interchange revenue and supplying low-cost deposits to support lending; BOQ reported a retail deposit base of about A$53 billion in FY2024, making growth modest but the base large and predictable. Nudge digital engagement and cross-sell at onboarding and payroll moments to lift wallet share. Keep fraud losses tight and simplify fees to avoid churn.

Term deposits (stable funding base)

Term deposits are a mature, rate-sensitive and dependable funding source for Bank of Queensland, delivering predictable cash flow when priced to market and anchored by conservative repricing profiles.

Not flashy but critical for balance sheet stability, targeted tenors are used to smooth funding gaps between wholesale and transaction balances.

Automating rollovers and reducing manual operations keeps administration costs low and preserves term deposits as a cash-generative pillar of funding strategy.

Equipment and asset finance (seasoned niches)

Established broker and direct channels deliver consistent yields in known categories, with BOQ equipment and asset finance showing stable returns and a portfolio balance around A$3.2bn in 2024 and a reported loss rate near 0.2%, reflecting seasoned lending quality.

Portfolio seasoning keeps losses low; tightening residual risk and revaluing collateral reduced downside in 2024, while incremental tech investment shaved turnaround times and improved margins without heavy marketing spend.

- Channels: broker + direct

- 2024 balance: A$3.2bn

- Loss rate: ~0.2%

- Actions: tighter residuals, collateral revals, tech-led efficiency

Basic business transaction accounts

Basic SME operating accounts are high-retention, low-fee cash cows for BOQ, serving as a prime cross-sell gateway into lending, cards and merchant services while requiring minimal servicing margins.

- Maintain: prioritise transparent, fair pricing to retain stickiness

- Scale: streamline onboarding and alerts to cut call-centre load

- Upsell: use accounts as feeder for higher-margin products

Mortgages, A$53bn deposits & equipment finance: steady NII repricing focus

Seasoned mortgages, retail deposits and term deposits form BOQ’s cash cows, delivering steady NII with mortgage default ~0.1% in 2024 and retail deposits ~A$53bn (FY2024). Equipment & asset finance (~A$3.2bn, loss ~0.2%) and SME accounts add stable low-cost funding and cross-sell channels. Focus on repricing, cost-to-serve, automation and tight arrears/fraud control to protect margins.

| Asset | 2024 metric | Role |

|---|---|---|

| Mortgages | Default ~0.1% | Core NII |

| Retail deposits | A$53bn | Low-cost funding |

| Equipment finance | A$3.2bn / 0.2% loss | Stable yield |

Delivered as Shown

Bank of Queensland BCG Matrix

The file you’re previewing here is the exact BCG Matrix report you’ll receive after purchase — no watermarks, no demo text, just the finished, fully formatted document. It’s built for strategic clarity with market-backed analysis and clean visuals ready for presentation. Buy once and download immediately; the file is editable, printable, and plug-and-play for your planning or investor decks.