Bouygues Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

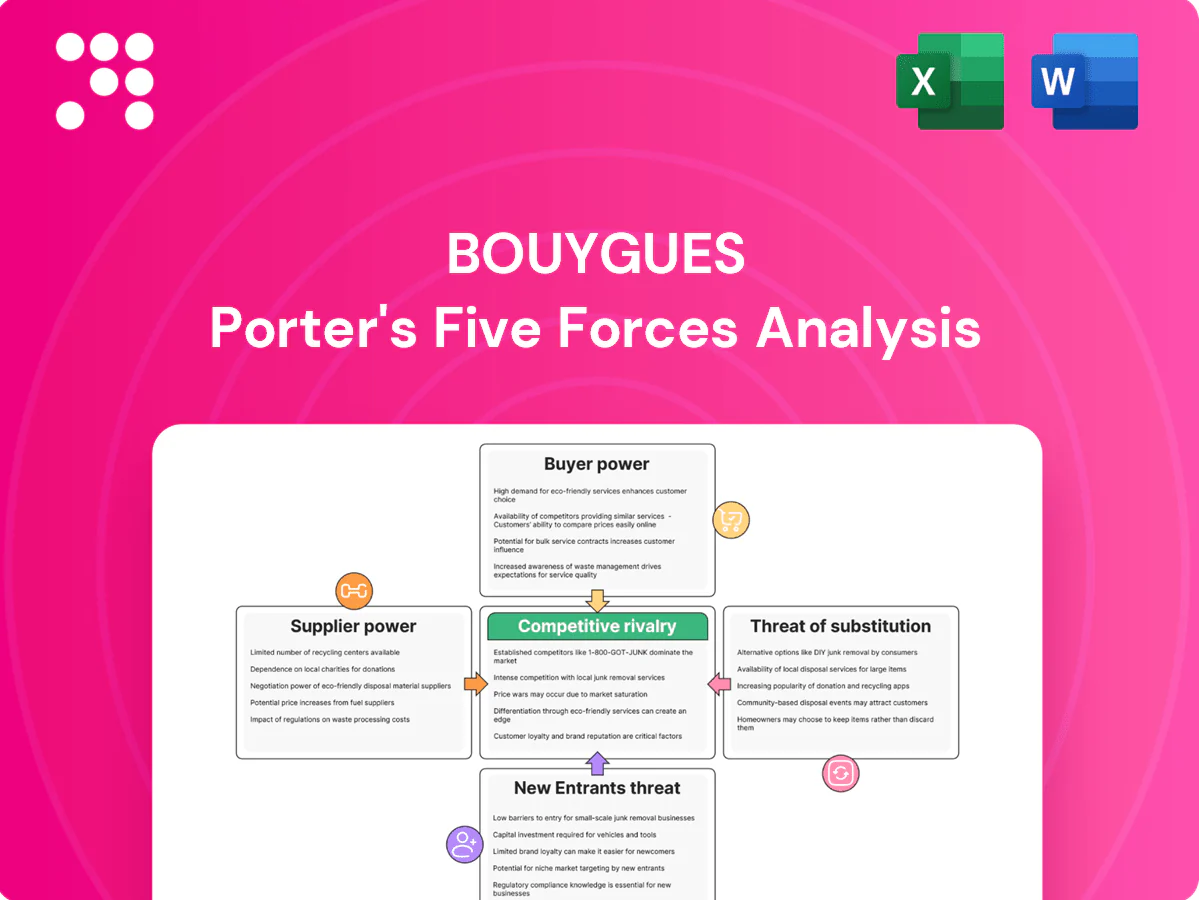

Bouygues faces moderate rivalry across construction, telecoms and media, while supplier and buyer power vary by segment and regulatory barriers constrain new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bouygues’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Construction procurement depends on cement, steel, asphalt and heavy equipment from a small set of global suppliers, increasing switching costs and price exposure for Bouygues. Telecom network gear and software are supplied by a few OEMs, concentrating bargaining power. TF1 faces leverage from content rights owners in renewal cycles for sports and studio deals. Bouygues offsets risks via scale, multi-sourcing and in-house capabilities such as Colas.

Regulated and scarce resources

ARCEP and municipalities control access to radio spectrum and rights-of-way in France, acting as quasi-suppliers with strong leverage over Bouygues' telecom and infrastructure projects. Permit timing and conditions can materially alter project economics by delaying revenue and raising financing costs. Energy and bitumen volatility transmit via supplier contracts; Brent crude averaged about $86/bl in 2024, and long-term frameworks with indexation clauses partially hedge these risks.

Specialized subcontractors

Complex civil works rely on niche subcontractors for tunneling, signaling and electrification whose finite capacity and certification constraints strengthen supplier leverage; tight labor markets in 2024 further amplified this pressure. Framework agreements and partnering models are used to secure multi-year availability, while Bouygues’ scale enables it to bundle packages and negotiate improved terms.

Technology lock-in

Telecom vendor lock-in for RAN/core and OSS/BSS raises switching costs and integration risk, with operators often facing tens to hundreds of millions EUR for phased migrations; Open RAN improves interoperability but 2024 deployments remain limited by maturity and performance concerns, preserving incumbent vendors influence over pricing and roadmaps.

- Incumbents retain pricing leverage

- Open RAN adoption rising but cautious

- Phased swaps and dual-vendor reduce single-vendor risk

Sustainability and compliance demands

ESG, safety and traceability rules narrow Bouygues suppliers, raising bargaining power for compliant providers; long-term contracts are used to secure scarce low-carbon inputs that in 2024 carried premiums (circa 10–35% across green steel/concrete markets) and reduce supply risk. TF1’s content pipeline must meet French audiovisual investment obligations (circa 20% of turnover), so supplier selection favors rights-compliant partners and co-development of greener solutions.

- ESG-driven supplier pool shrinks → higher supplier leverage

- Low-carbon materials scarce; 2024 premiums ~10–35%

- TF1 content needs rights/local-investment compliance (~20% rule)

- Long-term partnerships secure supply and enable joint decarbonization

Concentrated cement/steel exposure and tight 2024 labor markets raise project risk

High concentration in cement/steel/telecom gear raises switching costs and price exposure for Bouygues; niche civil subcontractors and tight 2024 labor markets amplify leverage. ARCEP/municipal rights-of-way act as quasi-suppliers affecting project timing. ESG-driven low-carbon inputs carried 2024 premiums (circa 10–35%), mitigated by long-term contracts and in-house capabilities.

| Metric | 2024 data |

|---|---|

| Brent crude | $86/bl |

| Green materials premium | 10–35% |

| TF1 audiovisual invest. rule | ~20% turnover |

What is included in the product

Tailored Porter’s Five Forces analysis for Bouygues that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and regulatory risks shaping its profitability and market positioning.

Concise Bouygues Porter's Five Forces—visual radar chart plus editable pressure sliders to instantly reveal strategic threats and opportunities for rapid, board-ready decisions.

Customers Bargaining Power

Public-sector contracting

Government and infrastructure clients run competitive tenders with standardized specs that compress contractor margins and, per the European Commission, public procurement represents about 14% of EU GDP, concentrating buyer power. Prequalification narrows suppliers but increases buyer leverage on pricing and liquidated damages. Payment schedules and risk-transfer clauses are major negotiation levers. Bouygues’ track record and design-build expertise help preserve value.

Large private developers

Large private developers bundle multi-year pipelines to extract volume discounts typically in the 5–10% range, comparing offers from Vinci, Eiffage and international peers to benchmark total cost of ownership.

Differentiation through in-house EPC integration and lifecycle services at Bouygues reduces pure price focus, with integrated contracts often commanding 3–6% premium over commodity bids.

Collaborative, alliancing-style contracts are increasingly used to rebalance risk-sharing, with industry pilots in 2024 reallocating 20–30% of schedule and cost overrun risk to joint governance models.

Price-sensitive telecom users

French mobile users are highly price-sensitive in a market with over 100% mobile penetration and four national operators; Bouygues holds around one-fifth of subscribers (ARCEP 2024), so consumers switch quickly for promotions. Number portability and no-lock contracts magnify buyer power, while fixed-mobile and content bundles plus network quality improve retention. Active churn management and segmented offers are therefore essential to protect ARPU and market share.

Enterprise and wholesale clients

Corporate telecom buyers push for SLAs and bespoke pricing via multi-operator RFPs and can multi-home, limiting supplier pricing power; Bouygues Telecom’s ~19% French mobile market share (2023) forces competitive responses. Vertical solutions and managed services (growing revenue share) raise stickiness, while long-term contracts lower price volatility but demand strict performance delivery.

- RFP-driven SLAs

- Multi-homing pressure

- Vertical services = higher retention

- Long-term contracts = stable but performance-bound

Advertisers and audiences

TF1 faces concentrated agency buyers and big brands that push CPMs while digital ad spend exceeded 60% in 2024, and TF1’s prime-time share was ~20%, weakening linear pricing; hybrid TV/digital and data-targeting raise yield, while premium live content preserves leverage.

- Concentrated buyers pressure CPMs

- Digital >60% of ad spend (2024)

- TF1 prime-time ~20% (2024)

- Hybrid/data + live content = higher yield

Public procurement 14% GDP; mobile churn; digital >60% ads; alliances shift 20–30% risk

Public procurement (~14% of EU GDP) centralises buyer power via competitive tenders and prequalification, compressing margins. Bouygues Telecom faces high churn with ~19% market share (ARCEP 2024) and >100% mobile penetration, so promos and bundles drive retention. TF1 sees digital >60% of ad spend (2024) and ~20% prime-time share, pressuring CPMs. Alliancing pilots (2024) shift 20–30% of overrun risk to joint models.

| Segment | Metric | 2024 data |

|---|---|---|

| Public procurement | Share of GDP | ~14% EU GDP |

| Telecom consumers | Market share / penetration | Bouygues ~19% / >100% penetration |

| Advertising | Digital / prime-time | Digital >60% / TF1 ~20% |

| Alliancing | Risk reallocated | 20–30% |

What You See Is What You Get

Bouygues Porter's Five Forces Analysis

This preview shows the exact Bouygues Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're viewing the final file; purchase grants instant access to this same deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bouygues faces moderate rivalry across construction, telecoms and media, while supplier and buyer power vary by segment and regulatory barriers constrain new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bouygues’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Construction procurement depends on cement, steel, asphalt and heavy equipment from a small set of global suppliers, increasing switching costs and price exposure for Bouygues. Telecom network gear and software are supplied by a few OEMs, concentrating bargaining power. TF1 faces leverage from content rights owners in renewal cycles for sports and studio deals. Bouygues offsets risks via scale, multi-sourcing and in-house capabilities such as Colas.

Regulated and scarce resources

ARCEP and municipalities control access to radio spectrum and rights-of-way in France, acting as quasi-suppliers with strong leverage over Bouygues' telecom and infrastructure projects. Permit timing and conditions can materially alter project economics by delaying revenue and raising financing costs. Energy and bitumen volatility transmit via supplier contracts; Brent crude averaged about $86/bl in 2024, and long-term frameworks with indexation clauses partially hedge these risks.

Specialized subcontractors

Complex civil works rely on niche subcontractors for tunneling, signaling and electrification whose finite capacity and certification constraints strengthen supplier leverage; tight labor markets in 2024 further amplified this pressure. Framework agreements and partnering models are used to secure multi-year availability, while Bouygues’ scale enables it to bundle packages and negotiate improved terms.

Technology lock-in

Telecom vendor lock-in for RAN/core and OSS/BSS raises switching costs and integration risk, with operators often facing tens to hundreds of millions EUR for phased migrations; Open RAN improves interoperability but 2024 deployments remain limited by maturity and performance concerns, preserving incumbent vendors influence over pricing and roadmaps.

- Incumbents retain pricing leverage

- Open RAN adoption rising but cautious

- Phased swaps and dual-vendor reduce single-vendor risk

Sustainability and compliance demands

ESG, safety and traceability rules narrow Bouygues suppliers, raising bargaining power for compliant providers; long-term contracts are used to secure scarce low-carbon inputs that in 2024 carried premiums (circa 10–35% across green steel/concrete markets) and reduce supply risk. TF1’s content pipeline must meet French audiovisual investment obligations (circa 20% of turnover), so supplier selection favors rights-compliant partners and co-development of greener solutions.

- ESG-driven supplier pool shrinks → higher supplier leverage

- Low-carbon materials scarce; 2024 premiums ~10–35%

- TF1 content needs rights/local-investment compliance (~20% rule)

- Long-term partnerships secure supply and enable joint decarbonization

Concentrated cement/steel exposure and tight 2024 labor markets raise project risk

High concentration in cement/steel/telecom gear raises switching costs and price exposure for Bouygues; niche civil subcontractors and tight 2024 labor markets amplify leverage. ARCEP/municipal rights-of-way act as quasi-suppliers affecting project timing. ESG-driven low-carbon inputs carried 2024 premiums (circa 10–35%), mitigated by long-term contracts and in-house capabilities.

| Metric | 2024 data |

|---|---|

| Brent crude | $86/bl |

| Green materials premium | 10–35% |

| TF1 audiovisual invest. rule | ~20% turnover |

What is included in the product

Tailored Porter’s Five Forces analysis for Bouygues that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and regulatory risks shaping its profitability and market positioning.

Concise Bouygues Porter's Five Forces—visual radar chart plus editable pressure sliders to instantly reveal strategic threats and opportunities for rapid, board-ready decisions.

Customers Bargaining Power

Public-sector contracting

Government and infrastructure clients run competitive tenders with standardized specs that compress contractor margins and, per the European Commission, public procurement represents about 14% of EU GDP, concentrating buyer power. Prequalification narrows suppliers but increases buyer leverage on pricing and liquidated damages. Payment schedules and risk-transfer clauses are major negotiation levers. Bouygues’ track record and design-build expertise help preserve value.

Large private developers

Large private developers bundle multi-year pipelines to extract volume discounts typically in the 5–10% range, comparing offers from Vinci, Eiffage and international peers to benchmark total cost of ownership.

Differentiation through in-house EPC integration and lifecycle services at Bouygues reduces pure price focus, with integrated contracts often commanding 3–6% premium over commodity bids.

Collaborative, alliancing-style contracts are increasingly used to rebalance risk-sharing, with industry pilots in 2024 reallocating 20–30% of schedule and cost overrun risk to joint governance models.

Price-sensitive telecom users

French mobile users are highly price-sensitive in a market with over 100% mobile penetration and four national operators; Bouygues holds around one-fifth of subscribers (ARCEP 2024), so consumers switch quickly for promotions. Number portability and no-lock contracts magnify buyer power, while fixed-mobile and content bundles plus network quality improve retention. Active churn management and segmented offers are therefore essential to protect ARPU and market share.

Enterprise and wholesale clients

Corporate telecom buyers push for SLAs and bespoke pricing via multi-operator RFPs and can multi-home, limiting supplier pricing power; Bouygues Telecom’s ~19% French mobile market share (2023) forces competitive responses. Vertical solutions and managed services (growing revenue share) raise stickiness, while long-term contracts lower price volatility but demand strict performance delivery.

- RFP-driven SLAs

- Multi-homing pressure

- Vertical services = higher retention

- Long-term contracts = stable but performance-bound

Advertisers and audiences

TF1 faces concentrated agency buyers and big brands that push CPMs while digital ad spend exceeded 60% in 2024, and TF1’s prime-time share was ~20%, weakening linear pricing; hybrid TV/digital and data-targeting raise yield, while premium live content preserves leverage.

- Concentrated buyers pressure CPMs

- Digital >60% of ad spend (2024)

- TF1 prime-time ~20% (2024)

- Hybrid/data + live content = higher yield

Public procurement 14% GDP; mobile churn; digital >60% ads; alliances shift 20–30% risk

Public procurement (~14% of EU GDP) centralises buyer power via competitive tenders and prequalification, compressing margins. Bouygues Telecom faces high churn with ~19% market share (ARCEP 2024) and >100% mobile penetration, so promos and bundles drive retention. TF1 sees digital >60% of ad spend (2024) and ~20% prime-time share, pressuring CPMs. Alliancing pilots (2024) shift 20–30% of overrun risk to joint models.

| Segment | Metric | 2024 data |

|---|---|---|

| Public procurement | Share of GDP | ~14% EU GDP |

| Telecom consumers | Market share / penetration | Bouygues ~19% / >100% penetration |

| Advertising | Digital / prime-time | Digital >60% / TF1 ~20% |

| Alliancing | Risk reallocated | 20–30% |

What You See Is What You Get

Bouygues Porter's Five Forces Analysis

This preview shows the exact Bouygues Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're viewing the final file; purchase grants instant access to this same deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bouygues faces moderate rivalry across construction, telecoms and media, while supplier and buyer power vary by segment and regulatory barriers constrain new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bouygues’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Construction procurement depends on cement, steel, asphalt and heavy equipment from a small set of global suppliers, increasing switching costs and price exposure for Bouygues. Telecom network gear and software are supplied by a few OEMs, concentrating bargaining power. TF1 faces leverage from content rights owners in renewal cycles for sports and studio deals. Bouygues offsets risks via scale, multi-sourcing and in-house capabilities such as Colas.

Regulated and scarce resources

ARCEP and municipalities control access to radio spectrum and rights-of-way in France, acting as quasi-suppliers with strong leverage over Bouygues' telecom and infrastructure projects. Permit timing and conditions can materially alter project economics by delaying revenue and raising financing costs. Energy and bitumen volatility transmit via supplier contracts; Brent crude averaged about $86/bl in 2024, and long-term frameworks with indexation clauses partially hedge these risks.

Specialized subcontractors

Complex civil works rely on niche subcontractors for tunneling, signaling and electrification whose finite capacity and certification constraints strengthen supplier leverage; tight labor markets in 2024 further amplified this pressure. Framework agreements and partnering models are used to secure multi-year availability, while Bouygues’ scale enables it to bundle packages and negotiate improved terms.

Technology lock-in

Telecom vendor lock-in for RAN/core and OSS/BSS raises switching costs and integration risk, with operators often facing tens to hundreds of millions EUR for phased migrations; Open RAN improves interoperability but 2024 deployments remain limited by maturity and performance concerns, preserving incumbent vendors influence over pricing and roadmaps.

- Incumbents retain pricing leverage

- Open RAN adoption rising but cautious

- Phased swaps and dual-vendor reduce single-vendor risk

Sustainability and compliance demands

ESG, safety and traceability rules narrow Bouygues suppliers, raising bargaining power for compliant providers; long-term contracts are used to secure scarce low-carbon inputs that in 2024 carried premiums (circa 10–35% across green steel/concrete markets) and reduce supply risk. TF1’s content pipeline must meet French audiovisual investment obligations (circa 20% of turnover), so supplier selection favors rights-compliant partners and co-development of greener solutions.

- ESG-driven supplier pool shrinks → higher supplier leverage

- Low-carbon materials scarce; 2024 premiums ~10–35%

- TF1 content needs rights/local-investment compliance (~20% rule)

- Long-term partnerships secure supply and enable joint decarbonization

Concentrated cement/steel exposure and tight 2024 labor markets raise project risk

High concentration in cement/steel/telecom gear raises switching costs and price exposure for Bouygues; niche civil subcontractors and tight 2024 labor markets amplify leverage. ARCEP/municipal rights-of-way act as quasi-suppliers affecting project timing. ESG-driven low-carbon inputs carried 2024 premiums (circa 10–35%), mitigated by long-term contracts and in-house capabilities.

| Metric | 2024 data |

|---|---|

| Brent crude | $86/bl |

| Green materials premium | 10–35% |

| TF1 audiovisual invest. rule | ~20% turnover |

What is included in the product

Tailored Porter’s Five Forces analysis for Bouygues that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and regulatory risks shaping its profitability and market positioning.

Concise Bouygues Porter's Five Forces—visual radar chart plus editable pressure sliders to instantly reveal strategic threats and opportunities for rapid, board-ready decisions.

Customers Bargaining Power

Public-sector contracting

Government and infrastructure clients run competitive tenders with standardized specs that compress contractor margins and, per the European Commission, public procurement represents about 14% of EU GDP, concentrating buyer power. Prequalification narrows suppliers but increases buyer leverage on pricing and liquidated damages. Payment schedules and risk-transfer clauses are major negotiation levers. Bouygues’ track record and design-build expertise help preserve value.

Large private developers

Large private developers bundle multi-year pipelines to extract volume discounts typically in the 5–10% range, comparing offers from Vinci, Eiffage and international peers to benchmark total cost of ownership.

Differentiation through in-house EPC integration and lifecycle services at Bouygues reduces pure price focus, with integrated contracts often commanding 3–6% premium over commodity bids.

Collaborative, alliancing-style contracts are increasingly used to rebalance risk-sharing, with industry pilots in 2024 reallocating 20–30% of schedule and cost overrun risk to joint governance models.

Price-sensitive telecom users

French mobile users are highly price-sensitive in a market with over 100% mobile penetration and four national operators; Bouygues holds around one-fifth of subscribers (ARCEP 2024), so consumers switch quickly for promotions. Number portability and no-lock contracts magnify buyer power, while fixed-mobile and content bundles plus network quality improve retention. Active churn management and segmented offers are therefore essential to protect ARPU and market share.

Enterprise and wholesale clients

Corporate telecom buyers push for SLAs and bespoke pricing via multi-operator RFPs and can multi-home, limiting supplier pricing power; Bouygues Telecom’s ~19% French mobile market share (2023) forces competitive responses. Vertical solutions and managed services (growing revenue share) raise stickiness, while long-term contracts lower price volatility but demand strict performance delivery.

- RFP-driven SLAs

- Multi-homing pressure

- Vertical services = higher retention

- Long-term contracts = stable but performance-bound

Advertisers and audiences

TF1 faces concentrated agency buyers and big brands that push CPMs while digital ad spend exceeded 60% in 2024, and TF1’s prime-time share was ~20%, weakening linear pricing; hybrid TV/digital and data-targeting raise yield, while premium live content preserves leverage.

- Concentrated buyers pressure CPMs

- Digital >60% of ad spend (2024)

- TF1 prime-time ~20% (2024)

- Hybrid/data + live content = higher yield

Public procurement 14% GDP; mobile churn; digital >60% ads; alliances shift 20–30% risk

Public procurement (~14% of EU GDP) centralises buyer power via competitive tenders and prequalification, compressing margins. Bouygues Telecom faces high churn with ~19% market share (ARCEP 2024) and >100% mobile penetration, so promos and bundles drive retention. TF1 sees digital >60% of ad spend (2024) and ~20% prime-time share, pressuring CPMs. Alliancing pilots (2024) shift 20–30% of overrun risk to joint models.

| Segment | Metric | 2024 data |

|---|---|---|

| Public procurement | Share of GDP | ~14% EU GDP |

| Telecom consumers | Market share / penetration | Bouygues ~19% / >100% penetration |

| Advertising | Digital / prime-time | Digital >60% / TF1 ~20% |

| Alliancing | Risk reallocated | 20–30% |

What You See Is What You Get

Bouygues Porter's Five Forces Analysis

This preview shows the exact Bouygues Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're viewing the final file; purchase grants instant access to this same deliverable.