Bouygues PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

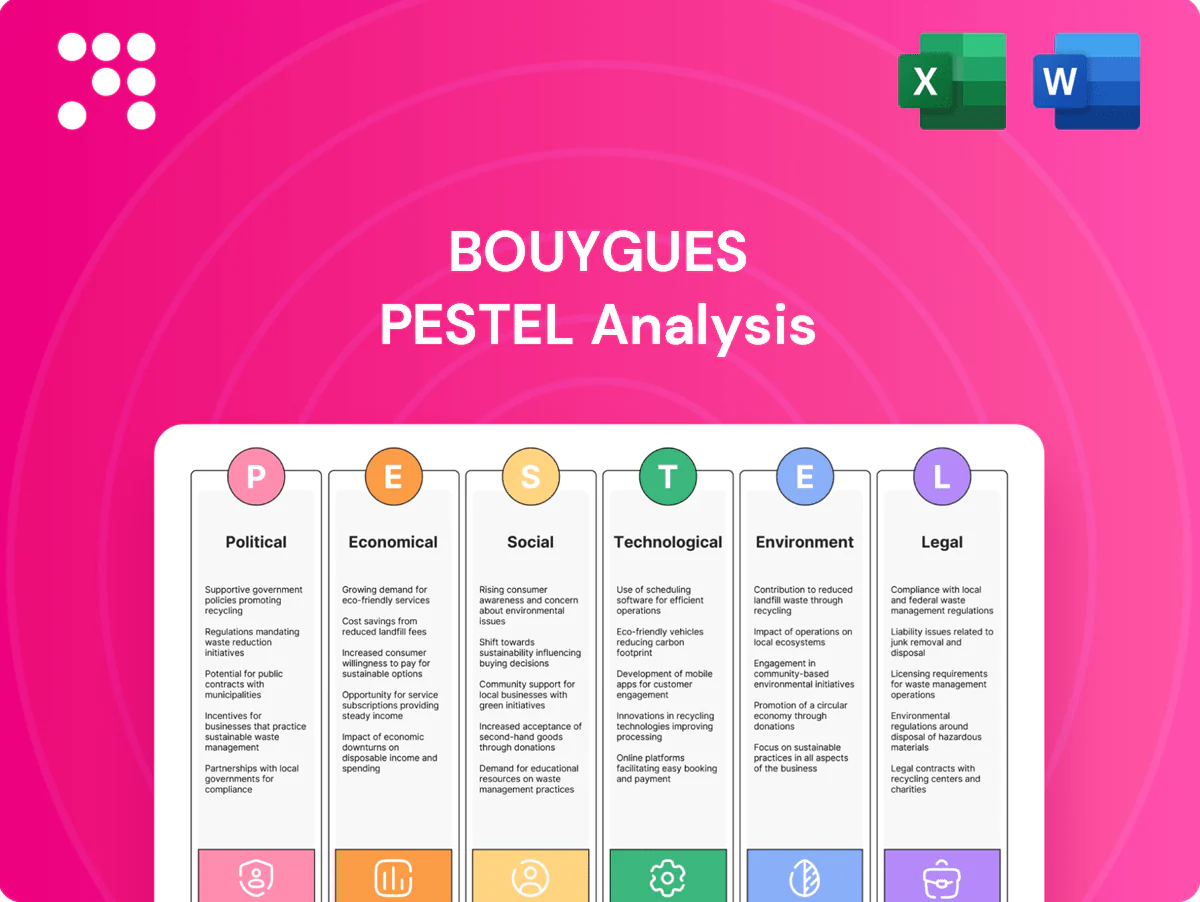

Our Bouygues PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, environmental pressures, and legal changes will shape the group's strategy and risk profile. Ideal for investors and strategists, it turns complex external data into clear insights. Purchase the full report to access detailed, actionable findings and ready-to-use charts.

Political factors

EU Green Deal and national transition plans

EU Green Deal and Fit for 55 steer funding to low-carbon construction, transport and energy, with Recovery and Resilience Facility commitments of €723.8bn and REPowerEU mobilising ~€300bn for energy projects. Bouygues can capture green public procurement in an EU public-procurement market ~14% of GDP (~€2tn/yr) but must meet stricter sustainability criteria. Compliance costs rise as EU ETS prices exceeded €80/t in 2024 and building retrofits face an EU investment gap ~€275bn/yr.

Public infrastructure spending and PPP frameworks

EU cohesion policy and NextGenerationEU (pooled €800bn) drive road, rail and public building projects critical to Colas and Bouygues Construction, underwriting pipeline volume across 2021‑27; PPP frameworks offer annuity-like revenues but expose Bouygues to political renegotiation and contingent liabilities. Election cycles frequently postpone tenders and approvals, increasing financing and carrying costs. Robust stakeholder engagement and contract clauses have reduced stoppage risk in recent EU projects.

Spectrum policy and telecom regulation (ARCEP)

Spectrum auctions (France’s 2020 3.4–3.8 GHz sale raised about €2.8bn) plus ARCEP coverage obligations materially drive Bouygues Telecom’s capex and constrain short‑term pricing power. Rural coverage mandates increase roll‑out costs but help defend share in underserved zones. Network‑sharing agreements reduce capex intensity and opex, improving competitiveness. ARCEP’s 5G/6G and private‑network policy creates growing enterprise revenue opportunities.

Media plurality and broadcasting policy

Government and regulator stances on media concentration constrain TF1’s M&A and partnership options, influencing strategic alternatives for Bouygues; TF1 Group reported €2.1bn revenue in 2023. AVMSD enforces a 30% European works quota for VOD and the EU Digital Services Act (2023) shifts platform rules, while political scrutiny of news impartiality affects audience trust and advertising appeal.

- Regulatory limits: affects TF1 deal-making

- Revenue mix: quotas/funding alter ad vs content income

- Reputation risk: impartiality scrutiny impacts trust

- Distribution: DSA/AVMSD shift platform power

Geopolitics and trade/sanctions exposure

Since the 2022 Russia–Ukraine war, energy and materials volatility has driven higher road and building costs and periodic supply shocks; sanctions have repeatedly disrupted equipment and bitumen supply routes. The EU Critical Raw Materials Act (2023) and Green Deal incentives are pushing procurement toward local sourcing, making risk hedging and diversified suppliers essential for Bouygues.

- Geopolitical shock: Russia–Ukraine war (since 2022)

- EU policy: Critical Raw Materials Act 2023

- Operational focus: hedging, supplier diversification

- Exposure: equipment and bitumen supply chains

EU green funds and €2tn public procurement push low‑carbon bids as EU ETS tops €80/t

EU green funds (RRF €723.8bn, REPowerEU ~€300bn) and a €2tn/yr public‑procurement market steer Bouygues to low‑carbon bids but raise compliance costs as EU ETS >€80/t in 2024. NextGenerationEU/ cohesion (€800bn) underpin infra pipeline while election cycles and media/regulatory limits constrain TF1 M&A and tenders.

| Item | Value |

|---|---|

| Public procurement | ~€2tn/yr |

| EU ETS 2024 | >€80/t |

| RRF | €723.8bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Bouygues across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples; tailored to help executives, consultants and investors identify risks, opportunities and forward-looking scenarios for strategic planning and funding decisions.

A clean, summarized Bouygues PESTLE that highlights key political, economic, social, technological, legal and environmental factors for quick reference during meetings and presentations, reducing prep time. Easily droppable into slides or shared across teams for fast alignment on external risks and strategic priorities.

Economic factors

Construction cycle and backlog resilience

Bouygues benefits from multi-quarter order books that cushion short-term demand swings but remain sensitive to GDP and public investment trends; housing slowdowns compress building volumes while infrastructure spending from government programs offsets declines. Energy-efficiency retrofits and data-center projects are growing, offering counter-cyclical revenue streams. Strong execution discipline and backlog management have historically preserved margins across mixed markets.

Inflation in materials, labor, and energy

Asphalt, cement, steel and fuel inflation materially compress Colas and Bouygues construction margins—European HRC steel averaged ~USD 600–700/t in 2024, cement ~€90–120/t and diesel ~€1.60–1.70/L, raising input bills sharply. Indexation clauses and procurement timing are essential to pass costs through; Colas uses indexed contracts to protect margins. Labor scarcity lifted French construction wages ~5–7% in 2023–24 and pushed subcontractor rates higher. Efficiency, standardization and closer supplier collaboration are deployed to stabilise unit costs.

Interest rates and project financing

Higher short-term rates (Euribor ~4.5%) have lifted WACC by roughly 100–200bp, tightening PPP bid economics and delaying client capex decisions. Real estate development slowed as 2024 financing tightened, cutting private orders and margins for construction contractors. Bouygues reported net debt near €6.9bn and Bouygues Telecom capex around €1.6bn in 2024, constraining telecom capex flexibility due to debt servicing. Rate declines would likely unlock deferred demand and revive PPP and real estate activity.

Telecom market competition and ARPU trends

Intense price competition in France caps ARPU growth and pressures returns on 5G and FTTH investments, while convergence bundles help reduce churn and enable upsell into higher-value fixed-mobile packages. Enterprise and wholesale segments are driving margin improvement through higher ARPU contracts and value-added services. Network quality and customer experience remain key differentiators for retention and pricing power.

- Price pressure limits consumer ARPU upside

- Convergence bundles lower churn, boost upsell

- Enterprise/wholesale = margin uplift

- Network quality = competitive edge

Advertising cycles and TF1 revenues

Ad spend for TF1 closely tracks consumer confidence and retail promotion budgets, making broadcast advertising revenues cyclical and sensitive to GDP and household consumption swings.

Shift toward digital, data-driven selling and addressable TV increases CPMs but requires investment in ad-tech and measurement to capture advertiser migration.

Event programming can buffer downturns yet raises content costs; Bouygues and TF1 diversify into production and streaming to mitigate cyclicality and stabilize recurring revenues.

- Ad sensitivity: consumer confidence → ad budgets

- Digital shift: addressable TV, data-driven sales

- Costs: event content ups expenses

- Mitigation: production & streaming diversification

EU green funds and €2tn public procurement push low‑carbon bids as EU ETS tops €80/t

Bouygues' backlog cushions GDP volatility but revenues remain sensitive to French GDP growth and public capex cycles; higher Euribor (~4.5%) tightened financing in 2024–25. Input inflation (HRC steel USD600–700/t, cement €90–120/t, diesel €1.60–1.70/L) and wages (+5–7% 2023–24) compressed margins; net debt ~€6.9bn limits telecom capex (~€1.6bn 2024).

| Metric | 2024/25 |

|---|---|

| Euribor | ~4.5% |

| Net debt | €6.9bn |

| Bouygues Telecom capex | €1.6bn |

| Steel | USD600–700/t |

| Cement | €90–120/t |

| Diesel | €1.60–1.70/L |

Full Version Awaits

Bouygues PESTLE Analysis

The Bouygues PESTLE Analysis preview shown here is the exact document you’ll receive after purchase, fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with no placeholders. After payment you’ll instantly download this same finished file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Our Bouygues PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, environmental pressures, and legal changes will shape the group's strategy and risk profile. Ideal for investors and strategists, it turns complex external data into clear insights. Purchase the full report to access detailed, actionable findings and ready-to-use charts.

Political factors

EU Green Deal and national transition plans

EU Green Deal and Fit for 55 steer funding to low-carbon construction, transport and energy, with Recovery and Resilience Facility commitments of €723.8bn and REPowerEU mobilising ~€300bn for energy projects. Bouygues can capture green public procurement in an EU public-procurement market ~14% of GDP (~€2tn/yr) but must meet stricter sustainability criteria. Compliance costs rise as EU ETS prices exceeded €80/t in 2024 and building retrofits face an EU investment gap ~€275bn/yr.

Public infrastructure spending and PPP frameworks

EU cohesion policy and NextGenerationEU (pooled €800bn) drive road, rail and public building projects critical to Colas and Bouygues Construction, underwriting pipeline volume across 2021‑27; PPP frameworks offer annuity-like revenues but expose Bouygues to political renegotiation and contingent liabilities. Election cycles frequently postpone tenders and approvals, increasing financing and carrying costs. Robust stakeholder engagement and contract clauses have reduced stoppage risk in recent EU projects.

Spectrum policy and telecom regulation (ARCEP)

Spectrum auctions (France’s 2020 3.4–3.8 GHz sale raised about €2.8bn) plus ARCEP coverage obligations materially drive Bouygues Telecom’s capex and constrain short‑term pricing power. Rural coverage mandates increase roll‑out costs but help defend share in underserved zones. Network‑sharing agreements reduce capex intensity and opex, improving competitiveness. ARCEP’s 5G/6G and private‑network policy creates growing enterprise revenue opportunities.

Media plurality and broadcasting policy

Government and regulator stances on media concentration constrain TF1’s M&A and partnership options, influencing strategic alternatives for Bouygues; TF1 Group reported €2.1bn revenue in 2023. AVMSD enforces a 30% European works quota for VOD and the EU Digital Services Act (2023) shifts platform rules, while political scrutiny of news impartiality affects audience trust and advertising appeal.

- Regulatory limits: affects TF1 deal-making

- Revenue mix: quotas/funding alter ad vs content income

- Reputation risk: impartiality scrutiny impacts trust

- Distribution: DSA/AVMSD shift platform power

Geopolitics and trade/sanctions exposure

Since the 2022 Russia–Ukraine war, energy and materials volatility has driven higher road and building costs and periodic supply shocks; sanctions have repeatedly disrupted equipment and bitumen supply routes. The EU Critical Raw Materials Act (2023) and Green Deal incentives are pushing procurement toward local sourcing, making risk hedging and diversified suppliers essential for Bouygues.

- Geopolitical shock: Russia–Ukraine war (since 2022)

- EU policy: Critical Raw Materials Act 2023

- Operational focus: hedging, supplier diversification

- Exposure: equipment and bitumen supply chains

EU green funds and €2tn public procurement push low‑carbon bids as EU ETS tops €80/t

EU green funds (RRF €723.8bn, REPowerEU ~€300bn) and a €2tn/yr public‑procurement market steer Bouygues to low‑carbon bids but raise compliance costs as EU ETS >€80/t in 2024. NextGenerationEU/ cohesion (€800bn) underpin infra pipeline while election cycles and media/regulatory limits constrain TF1 M&A and tenders.

| Item | Value |

|---|---|

| Public procurement | ~€2tn/yr |

| EU ETS 2024 | >€80/t |

| RRF | €723.8bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Bouygues across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples; tailored to help executives, consultants and investors identify risks, opportunities and forward-looking scenarios for strategic planning and funding decisions.

A clean, summarized Bouygues PESTLE that highlights key political, economic, social, technological, legal and environmental factors for quick reference during meetings and presentations, reducing prep time. Easily droppable into slides or shared across teams for fast alignment on external risks and strategic priorities.

Economic factors

Construction cycle and backlog resilience

Bouygues benefits from multi-quarter order books that cushion short-term demand swings but remain sensitive to GDP and public investment trends; housing slowdowns compress building volumes while infrastructure spending from government programs offsets declines. Energy-efficiency retrofits and data-center projects are growing, offering counter-cyclical revenue streams. Strong execution discipline and backlog management have historically preserved margins across mixed markets.

Inflation in materials, labor, and energy

Asphalt, cement, steel and fuel inflation materially compress Colas and Bouygues construction margins—European HRC steel averaged ~USD 600–700/t in 2024, cement ~€90–120/t and diesel ~€1.60–1.70/L, raising input bills sharply. Indexation clauses and procurement timing are essential to pass costs through; Colas uses indexed contracts to protect margins. Labor scarcity lifted French construction wages ~5–7% in 2023–24 and pushed subcontractor rates higher. Efficiency, standardization and closer supplier collaboration are deployed to stabilise unit costs.

Interest rates and project financing

Higher short-term rates (Euribor ~4.5%) have lifted WACC by roughly 100–200bp, tightening PPP bid economics and delaying client capex decisions. Real estate development slowed as 2024 financing tightened, cutting private orders and margins for construction contractors. Bouygues reported net debt near €6.9bn and Bouygues Telecom capex around €1.6bn in 2024, constraining telecom capex flexibility due to debt servicing. Rate declines would likely unlock deferred demand and revive PPP and real estate activity.

Telecom market competition and ARPU trends

Intense price competition in France caps ARPU growth and pressures returns on 5G and FTTH investments, while convergence bundles help reduce churn and enable upsell into higher-value fixed-mobile packages. Enterprise and wholesale segments are driving margin improvement through higher ARPU contracts and value-added services. Network quality and customer experience remain key differentiators for retention and pricing power.

- Price pressure limits consumer ARPU upside

- Convergence bundles lower churn, boost upsell

- Enterprise/wholesale = margin uplift

- Network quality = competitive edge

Advertising cycles and TF1 revenues

Ad spend for TF1 closely tracks consumer confidence and retail promotion budgets, making broadcast advertising revenues cyclical and sensitive to GDP and household consumption swings.

Shift toward digital, data-driven selling and addressable TV increases CPMs but requires investment in ad-tech and measurement to capture advertiser migration.

Event programming can buffer downturns yet raises content costs; Bouygues and TF1 diversify into production and streaming to mitigate cyclicality and stabilize recurring revenues.

- Ad sensitivity: consumer confidence → ad budgets

- Digital shift: addressable TV, data-driven sales

- Costs: event content ups expenses

- Mitigation: production & streaming diversification

EU green funds and €2tn public procurement push low‑carbon bids as EU ETS tops €80/t

Bouygues' backlog cushions GDP volatility but revenues remain sensitive to French GDP growth and public capex cycles; higher Euribor (~4.5%) tightened financing in 2024–25. Input inflation (HRC steel USD600–700/t, cement €90–120/t, diesel €1.60–1.70/L) and wages (+5–7% 2023–24) compressed margins; net debt ~€6.9bn limits telecom capex (~€1.6bn 2024).

| Metric | 2024/25 |

|---|---|

| Euribor | ~4.5% |

| Net debt | €6.9bn |

| Bouygues Telecom capex | €1.6bn |

| Steel | USD600–700/t |

| Cement | €90–120/t |

| Diesel | €1.60–1.70/L |

Full Version Awaits

Bouygues PESTLE Analysis

The Bouygues PESTLE Analysis preview shown here is the exact document you’ll receive after purchase, fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with no placeholders. After payment you’ll instantly download this same finished file.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our Bouygues PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, environmental pressures, and legal changes will shape the group's strategy and risk profile. Ideal for investors and strategists, it turns complex external data into clear insights. Purchase the full report to access detailed, actionable findings and ready-to-use charts.

Political factors

EU Green Deal and national transition plans

EU Green Deal and Fit for 55 steer funding to low-carbon construction, transport and energy, with Recovery and Resilience Facility commitments of €723.8bn and REPowerEU mobilising ~€300bn for energy projects. Bouygues can capture green public procurement in an EU public-procurement market ~14% of GDP (~€2tn/yr) but must meet stricter sustainability criteria. Compliance costs rise as EU ETS prices exceeded €80/t in 2024 and building retrofits face an EU investment gap ~€275bn/yr.

Public infrastructure spending and PPP frameworks

EU cohesion policy and NextGenerationEU (pooled €800bn) drive road, rail and public building projects critical to Colas and Bouygues Construction, underwriting pipeline volume across 2021‑27; PPP frameworks offer annuity-like revenues but expose Bouygues to political renegotiation and contingent liabilities. Election cycles frequently postpone tenders and approvals, increasing financing and carrying costs. Robust stakeholder engagement and contract clauses have reduced stoppage risk in recent EU projects.

Spectrum policy and telecom regulation (ARCEP)

Spectrum auctions (France’s 2020 3.4–3.8 GHz sale raised about €2.8bn) plus ARCEP coverage obligations materially drive Bouygues Telecom’s capex and constrain short‑term pricing power. Rural coverage mandates increase roll‑out costs but help defend share in underserved zones. Network‑sharing agreements reduce capex intensity and opex, improving competitiveness. ARCEP’s 5G/6G and private‑network policy creates growing enterprise revenue opportunities.

Media plurality and broadcasting policy

Government and regulator stances on media concentration constrain TF1’s M&A and partnership options, influencing strategic alternatives for Bouygues; TF1 Group reported €2.1bn revenue in 2023. AVMSD enforces a 30% European works quota for VOD and the EU Digital Services Act (2023) shifts platform rules, while political scrutiny of news impartiality affects audience trust and advertising appeal.

- Regulatory limits: affects TF1 deal-making

- Revenue mix: quotas/funding alter ad vs content income

- Reputation risk: impartiality scrutiny impacts trust

- Distribution: DSA/AVMSD shift platform power

Geopolitics and trade/sanctions exposure

Since the 2022 Russia–Ukraine war, energy and materials volatility has driven higher road and building costs and periodic supply shocks; sanctions have repeatedly disrupted equipment and bitumen supply routes. The EU Critical Raw Materials Act (2023) and Green Deal incentives are pushing procurement toward local sourcing, making risk hedging and diversified suppliers essential for Bouygues.

- Geopolitical shock: Russia–Ukraine war (since 2022)

- EU policy: Critical Raw Materials Act 2023

- Operational focus: hedging, supplier diversification

- Exposure: equipment and bitumen supply chains

EU green funds and €2tn public procurement push low‑carbon bids as EU ETS tops €80/t

EU green funds (RRF €723.8bn, REPowerEU ~€300bn) and a €2tn/yr public‑procurement market steer Bouygues to low‑carbon bids but raise compliance costs as EU ETS >€80/t in 2024. NextGenerationEU/ cohesion (€800bn) underpin infra pipeline while election cycles and media/regulatory limits constrain TF1 M&A and tenders.

| Item | Value |

|---|---|

| Public procurement | ~€2tn/yr |

| EU ETS 2024 | >€80/t |

| RRF | €723.8bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Bouygues across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples; tailored to help executives, consultants and investors identify risks, opportunities and forward-looking scenarios for strategic planning and funding decisions.

A clean, summarized Bouygues PESTLE that highlights key political, economic, social, technological, legal and environmental factors for quick reference during meetings and presentations, reducing prep time. Easily droppable into slides or shared across teams for fast alignment on external risks and strategic priorities.

Economic factors

Construction cycle and backlog resilience

Bouygues benefits from multi-quarter order books that cushion short-term demand swings but remain sensitive to GDP and public investment trends; housing slowdowns compress building volumes while infrastructure spending from government programs offsets declines. Energy-efficiency retrofits and data-center projects are growing, offering counter-cyclical revenue streams. Strong execution discipline and backlog management have historically preserved margins across mixed markets.

Inflation in materials, labor, and energy

Asphalt, cement, steel and fuel inflation materially compress Colas and Bouygues construction margins—European HRC steel averaged ~USD 600–700/t in 2024, cement ~€90–120/t and diesel ~€1.60–1.70/L, raising input bills sharply. Indexation clauses and procurement timing are essential to pass costs through; Colas uses indexed contracts to protect margins. Labor scarcity lifted French construction wages ~5–7% in 2023–24 and pushed subcontractor rates higher. Efficiency, standardization and closer supplier collaboration are deployed to stabilise unit costs.

Interest rates and project financing

Higher short-term rates (Euribor ~4.5%) have lifted WACC by roughly 100–200bp, tightening PPP bid economics and delaying client capex decisions. Real estate development slowed as 2024 financing tightened, cutting private orders and margins for construction contractors. Bouygues reported net debt near €6.9bn and Bouygues Telecom capex around €1.6bn in 2024, constraining telecom capex flexibility due to debt servicing. Rate declines would likely unlock deferred demand and revive PPP and real estate activity.

Telecom market competition and ARPU trends

Intense price competition in France caps ARPU growth and pressures returns on 5G and FTTH investments, while convergence bundles help reduce churn and enable upsell into higher-value fixed-mobile packages. Enterprise and wholesale segments are driving margin improvement through higher ARPU contracts and value-added services. Network quality and customer experience remain key differentiators for retention and pricing power.

- Price pressure limits consumer ARPU upside

- Convergence bundles lower churn, boost upsell

- Enterprise/wholesale = margin uplift

- Network quality = competitive edge

Advertising cycles and TF1 revenues

Ad spend for TF1 closely tracks consumer confidence and retail promotion budgets, making broadcast advertising revenues cyclical and sensitive to GDP and household consumption swings.

Shift toward digital, data-driven selling and addressable TV increases CPMs but requires investment in ad-tech and measurement to capture advertiser migration.

Event programming can buffer downturns yet raises content costs; Bouygues and TF1 diversify into production and streaming to mitigate cyclicality and stabilize recurring revenues.

- Ad sensitivity: consumer confidence → ad budgets

- Digital shift: addressable TV, data-driven sales

- Costs: event content ups expenses

- Mitigation: production & streaming diversification

EU green funds and €2tn public procurement push low‑carbon bids as EU ETS tops €80/t

Bouygues' backlog cushions GDP volatility but revenues remain sensitive to French GDP growth and public capex cycles; higher Euribor (~4.5%) tightened financing in 2024–25. Input inflation (HRC steel USD600–700/t, cement €90–120/t, diesel €1.60–1.70/L) and wages (+5–7% 2023–24) compressed margins; net debt ~€6.9bn limits telecom capex (~€1.6bn 2024).

| Metric | 2024/25 |

|---|---|

| Euribor | ~4.5% |

| Net debt | €6.9bn |

| Bouygues Telecom capex | €1.6bn |

| Steel | USD600–700/t |

| Cement | €90–120/t |

| Diesel | €1.60–1.70/L |

Full Version Awaits

Bouygues PESTLE Analysis

The Bouygues PESTLE Analysis preview shown here is the exact document you’ll receive after purchase, fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with no placeholders. After payment you’ll instantly download this same finished file.