BPER Banca Boston Consulting Group Matrix

See the Bigger Picture

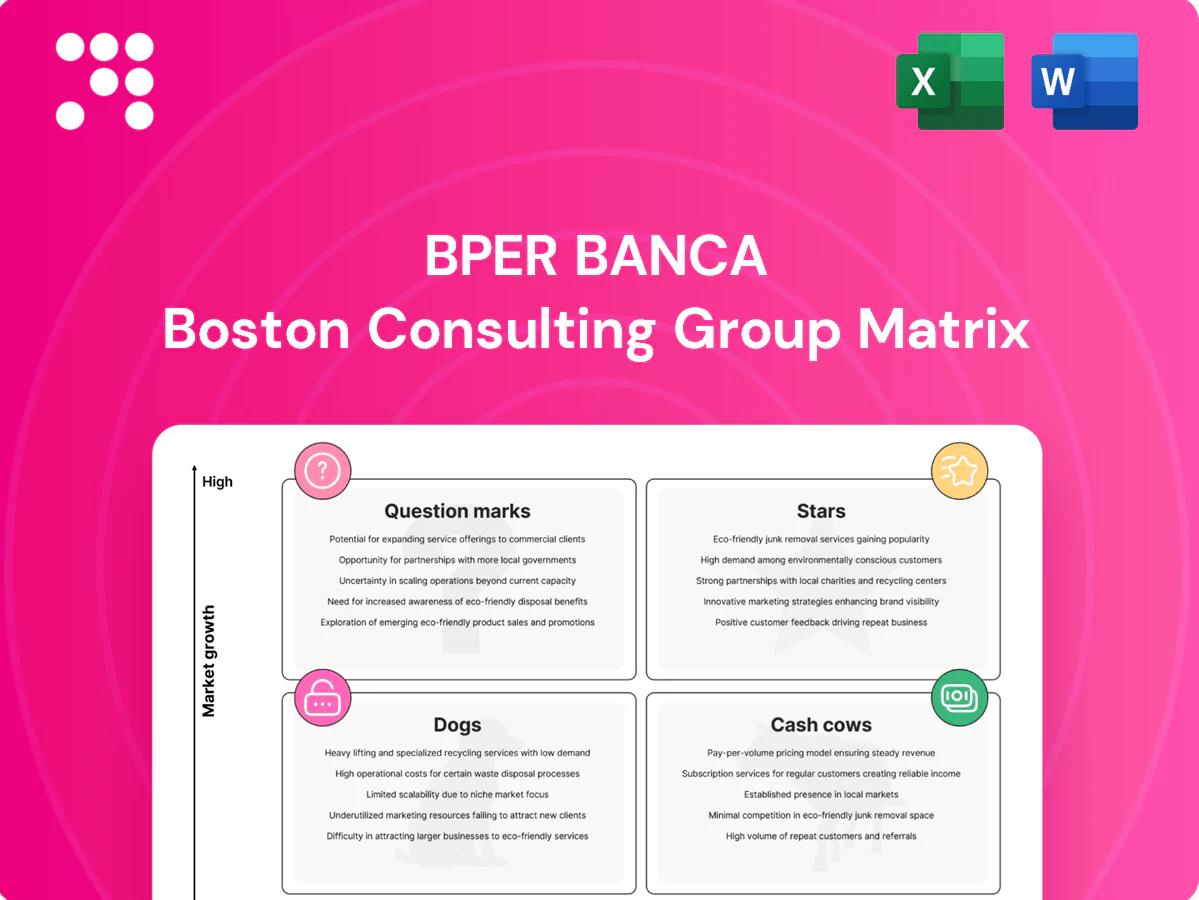

BPER Banca’s BCG Matrix snapshot shows where core services and segments sit today — who’s a Star, who’s a Cash Cow, and who needs attention. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placement, data-driven recommendations, and ready-to-use Word and Excel files. It’s a fast, practical tool to reallocate capital, sharpen strategy, and move from guesswork to confident decisions.

Stars

Multi‑channel retail engine in core regions

Strong brand, dense footprint (around 1,500 branches) and a slick digital front end are pulling in everyday banking activity where BPER already wins. The Italian market for convenience banking continues to grow as cash-to-card transactions rose ~8% in 2024. Keep investing in UX, data-led offers and local presence to defend share. Hold the line and it matures into a cash cow.

SME lending and relationship banking

SME lending is BPER’s home turf: relationship managers and sector know-how drive high utilization and deep cross-sell into cash management and trade finance. Italian SMEs account for roughly 99.9% of firms and about 67% of employment (Eurostat/ISTAT), keeping credit demand resilient in niche sectors. Ongoing investment in risk analytics and proactive coverage is required to control default risk and preserve margins. Nail it and it will spin steady profits for years.

Digital payments and everyday transactions

Card spend rose ~22% YoY in 2024, instant transfers volumes climbed ~35% and e‑commerce acquiring grew ~28%, and BPER’s installed base of ~3.5m active cards gives scale on interchange and fees. Pushing contactless adoption, merchant POS solutions and frictionless in‑app flows will lock behavioral stickiness. Growth is shifting spend from cash to digital now; the customer‑merchant bank flywheel drives higher interchange and ancillary fee payback.

Wealth management cross‑sell to affluent

Wealth management cross-sell to affluent at BPER drives fee income as deposits shift into advisory portfolios and funds; in 2024 fee-bearing AUM migrations typically lift recurring fees by c.15–25% versus deposit margins. BPER’s retail branch reach and digital guidance tools accelerate uptake, while advisor productivity improvements and curated product shelves are essential to sustain conversion. If momentum holds, this becomes a cornerstone fee earner.

Bancassurance for retail protection

Bancassurance for retail protection attaches simple life and protection products to loans and savings, with 2024 YTD bancassurance protection sales up c.10% as awareness and pricing improve; penetration is rising across branches. Continue intensive branch training and embed offers in digital and branch journeys to convert prospects. Growth is high now and is on track to become reliable fee income.

- attach-to-loans

- penetration+10%2024

- train-branches

- embed-in-journeys

- high-growth→stable-fees

Convert scale & UX into cash: ~1,500 branches, ~3.5m cards, +22% spend

Stars: strong brand and ~1,500 branches plus slick digital UI drive growth in everyday banking and SME lending; card base ~3.5m with card spend +22% YoY (2024) and instant transfers +35% YoY. Wealth AUM migration lifts fees +15–25% and bancassurance sales +10% (2024); invest in UX, risk analytics and advisor productivity to convert growth into cash cows.

| Metric | 2024 |

|---|---|

| Branches | ~1,500 |

| Active cards | ~3.5m |

| Card spend YoY | +22% |

| Instant transfers YoY | +35% |

| Wealth fee lift | +15–25% |

| Bancassurance sales | +10% |

What is included in the product

BCG analysis of BPER Banca: strategic guidance on Stars, Cash Cows, Question Marks and Dogs, with investment and divestment recommendations.

One-page BPER Banca BCG Matrix easing portfolio decisions by spotlighting priorities at a glance.

Cash Cows

Core current accounts and deposits

Core current accounts and deposits form BPER Banca’s cash cow with a large, sticky base—around €85bn customer deposits at end-2024—low servicing cost and a mature low-growth market; scale delivers cheap funding, so optimizing pricing and churn control maximizes net interest spread. Minimal promotional spend keeps steady cash generation.

Residential mortgages book

Residential mortgages book: established portfolio delivering predictable margins and low loss rates, with origination growth modest while servicing and cross-sell remain efficient; management focuses tightly on cost of funding and prepayment management to protect spread, making the mortgage book a dependable income bedrock for BPER.

Leasing and factoring franchises

Leasing and factoring franchises show stable demand from existing corporate clients, with defensible niches in SMEs and mid-corporates and standardized processes that benefit from seasoned credit selection; BPER reported net fee and commission income around EUR 1.1bn in 2023, underpinning reliable fee streams.

Incremental automation in origination and servicing is boosting returns and lowering cost-to-income, supporting predictable interest and fee cashflows with low promotional needs and limited capital intensity.

Transaction services for corporates

Transaction services for corporates act as a classic cash cow: embedded cash management, payroll and collections create high client stickiness and rare switching once integrated; small product enhancements in 2024 lifted fee yield materially while marginal cost stayed low, and steady fee streams quietly fund strategic investments across BPER Banca.

- stickiness

- low marginal cost

- fee uplift 2024

- funds strategic bets

Branch network in prime locations

Branch network in prime locations remains BPER Banca’s cash cow: in 2024 branches in core territories continue to drive the bulk of retail deposits (>€60bn) and high-margin product sales; growth is low but unit economics are proven, so consolidating overlaps and digitizing service improves yield; run lean and these branches mint cash via fees and low-cost deposits.

Deposits, mortgages & fees drive steady cash flow - €85bn

Core current accounts and deposits (~€85bn customer deposits end-2024) and branch-driven retail deposits (>€60bn in 2024) are BPER’s primary cash cows, delivering low-cost funding and steady NII. Mortgages and transaction services provide predictable margins and high stickiness; leasing/factoring and fees (net fees ~€1.1bn in 2023) add reliable non-interest income. Ongoing digitization trims cost-to-income, boosting free cash flow.

| Metric | Value |

|---|---|

| Total customer deposits (end-2024) | €85bn |

| Branch retail deposits (2024) | >€60bn |

| Net fee & commission (2023) | €1.1bn |

What You’re Viewing Is Included

BPER Banca BCG Matrix

The file you're previewing is the exact BPER Banca BCG Matrix you'll receive after purchase. No watermarks or demo text—just the fully formatted, professional report ready for strategic use. It includes market-backed placements and clear visuals for immediate presentation or editing. Buy once and download instantly—no surprises, no extra steps.

See the Bigger Picture

BPER Banca’s BCG Matrix snapshot shows where core services and segments sit today — who’s a Star, who’s a Cash Cow, and who needs attention. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placement, data-driven recommendations, and ready-to-use Word and Excel files. It’s a fast, practical tool to reallocate capital, sharpen strategy, and move from guesswork to confident decisions.

Stars

Multi‑channel retail engine in core regions

Strong brand, dense footprint (around 1,500 branches) and a slick digital front end are pulling in everyday banking activity where BPER already wins. The Italian market for convenience banking continues to grow as cash-to-card transactions rose ~8% in 2024. Keep investing in UX, data-led offers and local presence to defend share. Hold the line and it matures into a cash cow.

SME lending and relationship banking

SME lending is BPER’s home turf: relationship managers and sector know-how drive high utilization and deep cross-sell into cash management and trade finance. Italian SMEs account for roughly 99.9% of firms and about 67% of employment (Eurostat/ISTAT), keeping credit demand resilient in niche sectors. Ongoing investment in risk analytics and proactive coverage is required to control default risk and preserve margins. Nail it and it will spin steady profits for years.

Digital payments and everyday transactions

Card spend rose ~22% YoY in 2024, instant transfers volumes climbed ~35% and e‑commerce acquiring grew ~28%, and BPER’s installed base of ~3.5m active cards gives scale on interchange and fees. Pushing contactless adoption, merchant POS solutions and frictionless in‑app flows will lock behavioral stickiness. Growth is shifting spend from cash to digital now; the customer‑merchant bank flywheel drives higher interchange and ancillary fee payback.

Wealth management cross‑sell to affluent

Wealth management cross-sell to affluent at BPER drives fee income as deposits shift into advisory portfolios and funds; in 2024 fee-bearing AUM migrations typically lift recurring fees by c.15–25% versus deposit margins. BPER’s retail branch reach and digital guidance tools accelerate uptake, while advisor productivity improvements and curated product shelves are essential to sustain conversion. If momentum holds, this becomes a cornerstone fee earner.

Bancassurance for retail protection

Bancassurance for retail protection attaches simple life and protection products to loans and savings, with 2024 YTD bancassurance protection sales up c.10% as awareness and pricing improve; penetration is rising across branches. Continue intensive branch training and embed offers in digital and branch journeys to convert prospects. Growth is high now and is on track to become reliable fee income.

- attach-to-loans

- penetration+10%2024

- train-branches

- embed-in-journeys

- high-growth→stable-fees

Convert scale & UX into cash: ~1,500 branches, ~3.5m cards, +22% spend

Stars: strong brand and ~1,500 branches plus slick digital UI drive growth in everyday banking and SME lending; card base ~3.5m with card spend +22% YoY (2024) and instant transfers +35% YoY. Wealth AUM migration lifts fees +15–25% and bancassurance sales +10% (2024); invest in UX, risk analytics and advisor productivity to convert growth into cash cows.

| Metric | 2024 |

|---|---|

| Branches | ~1,500 |

| Active cards | ~3.5m |

| Card spend YoY | +22% |

| Instant transfers YoY | +35% |

| Wealth fee lift | +15–25% |

| Bancassurance sales | +10% |

What is included in the product

BCG analysis of BPER Banca: strategic guidance on Stars, Cash Cows, Question Marks and Dogs, with investment and divestment recommendations.

One-page BPER Banca BCG Matrix easing portfolio decisions by spotlighting priorities at a glance.

Cash Cows

Core current accounts and deposits

Core current accounts and deposits form BPER Banca’s cash cow with a large, sticky base—around €85bn customer deposits at end-2024—low servicing cost and a mature low-growth market; scale delivers cheap funding, so optimizing pricing and churn control maximizes net interest spread. Minimal promotional spend keeps steady cash generation.

Residential mortgages book

Residential mortgages book: established portfolio delivering predictable margins and low loss rates, with origination growth modest while servicing and cross-sell remain efficient; management focuses tightly on cost of funding and prepayment management to protect spread, making the mortgage book a dependable income bedrock for BPER.

Leasing and factoring franchises

Leasing and factoring franchises show stable demand from existing corporate clients, with defensible niches in SMEs and mid-corporates and standardized processes that benefit from seasoned credit selection; BPER reported net fee and commission income around EUR 1.1bn in 2023, underpinning reliable fee streams.

Incremental automation in origination and servicing is boosting returns and lowering cost-to-income, supporting predictable interest and fee cashflows with low promotional needs and limited capital intensity.

Transaction services for corporates

Transaction services for corporates act as a classic cash cow: embedded cash management, payroll and collections create high client stickiness and rare switching once integrated; small product enhancements in 2024 lifted fee yield materially while marginal cost stayed low, and steady fee streams quietly fund strategic investments across BPER Banca.

- stickiness

- low marginal cost

- fee uplift 2024

- funds strategic bets

Branch network in prime locations

Branch network in prime locations remains BPER Banca’s cash cow: in 2024 branches in core territories continue to drive the bulk of retail deposits (>€60bn) and high-margin product sales; growth is low but unit economics are proven, so consolidating overlaps and digitizing service improves yield; run lean and these branches mint cash via fees and low-cost deposits.

Deposits, mortgages & fees drive steady cash flow - €85bn

Core current accounts and deposits (~€85bn customer deposits end-2024) and branch-driven retail deposits (>€60bn in 2024) are BPER’s primary cash cows, delivering low-cost funding and steady NII. Mortgages and transaction services provide predictable margins and high stickiness; leasing/factoring and fees (net fees ~€1.1bn in 2023) add reliable non-interest income. Ongoing digitization trims cost-to-income, boosting free cash flow.

| Metric | Value |

|---|---|

| Total customer deposits (end-2024) | €85bn |

| Branch retail deposits (2024) | >€60bn |

| Net fee & commission (2023) | €1.1bn |

What You’re Viewing Is Included

BPER Banca BCG Matrix

The file you're previewing is the exact BPER Banca BCG Matrix you'll receive after purchase. No watermarks or demo text—just the fully formatted, professional report ready for strategic use. It includes market-backed placements and clear visuals for immediate presentation or editing. Buy once and download instantly—no surprises, no extra steps.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

BPER Banca’s BCG Matrix snapshot shows where core services and segments sit today — who’s a Star, who’s a Cash Cow, and who needs attention. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placement, data-driven recommendations, and ready-to-use Word and Excel files. It’s a fast, practical tool to reallocate capital, sharpen strategy, and move from guesswork to confident decisions.

Stars

Multi‑channel retail engine in core regions

Strong brand, dense footprint (around 1,500 branches) and a slick digital front end are pulling in everyday banking activity where BPER already wins. The Italian market for convenience banking continues to grow as cash-to-card transactions rose ~8% in 2024. Keep investing in UX, data-led offers and local presence to defend share. Hold the line and it matures into a cash cow.

SME lending and relationship banking

SME lending is BPER’s home turf: relationship managers and sector know-how drive high utilization and deep cross-sell into cash management and trade finance. Italian SMEs account for roughly 99.9% of firms and about 67% of employment (Eurostat/ISTAT), keeping credit demand resilient in niche sectors. Ongoing investment in risk analytics and proactive coverage is required to control default risk and preserve margins. Nail it and it will spin steady profits for years.

Digital payments and everyday transactions

Card spend rose ~22% YoY in 2024, instant transfers volumes climbed ~35% and e‑commerce acquiring grew ~28%, and BPER’s installed base of ~3.5m active cards gives scale on interchange and fees. Pushing contactless adoption, merchant POS solutions and frictionless in‑app flows will lock behavioral stickiness. Growth is shifting spend from cash to digital now; the customer‑merchant bank flywheel drives higher interchange and ancillary fee payback.

Wealth management cross‑sell to affluent

Wealth management cross-sell to affluent at BPER drives fee income as deposits shift into advisory portfolios and funds; in 2024 fee-bearing AUM migrations typically lift recurring fees by c.15–25% versus deposit margins. BPER’s retail branch reach and digital guidance tools accelerate uptake, while advisor productivity improvements and curated product shelves are essential to sustain conversion. If momentum holds, this becomes a cornerstone fee earner.

Bancassurance for retail protection

Bancassurance for retail protection attaches simple life and protection products to loans and savings, with 2024 YTD bancassurance protection sales up c.10% as awareness and pricing improve; penetration is rising across branches. Continue intensive branch training and embed offers in digital and branch journeys to convert prospects. Growth is high now and is on track to become reliable fee income.

- attach-to-loans

- penetration+10%2024

- train-branches

- embed-in-journeys

- high-growth→stable-fees

Convert scale & UX into cash: ~1,500 branches, ~3.5m cards, +22% spend

Stars: strong brand and ~1,500 branches plus slick digital UI drive growth in everyday banking and SME lending; card base ~3.5m with card spend +22% YoY (2024) and instant transfers +35% YoY. Wealth AUM migration lifts fees +15–25% and bancassurance sales +10% (2024); invest in UX, risk analytics and advisor productivity to convert growth into cash cows.

| Metric | 2024 |

|---|---|

| Branches | ~1,500 |

| Active cards | ~3.5m |

| Card spend YoY | +22% |

| Instant transfers YoY | +35% |

| Wealth fee lift | +15–25% |

| Bancassurance sales | +10% |

What is included in the product

BCG analysis of BPER Banca: strategic guidance on Stars, Cash Cows, Question Marks and Dogs, with investment and divestment recommendations.

One-page BPER Banca BCG Matrix easing portfolio decisions by spotlighting priorities at a glance.

Cash Cows

Core current accounts and deposits

Core current accounts and deposits form BPER Banca’s cash cow with a large, sticky base—around €85bn customer deposits at end-2024—low servicing cost and a mature low-growth market; scale delivers cheap funding, so optimizing pricing and churn control maximizes net interest spread. Minimal promotional spend keeps steady cash generation.

Residential mortgages book

Residential mortgages book: established portfolio delivering predictable margins and low loss rates, with origination growth modest while servicing and cross-sell remain efficient; management focuses tightly on cost of funding and prepayment management to protect spread, making the mortgage book a dependable income bedrock for BPER.

Leasing and factoring franchises

Leasing and factoring franchises show stable demand from existing corporate clients, with defensible niches in SMEs and mid-corporates and standardized processes that benefit from seasoned credit selection; BPER reported net fee and commission income around EUR 1.1bn in 2023, underpinning reliable fee streams.

Incremental automation in origination and servicing is boosting returns and lowering cost-to-income, supporting predictable interest and fee cashflows with low promotional needs and limited capital intensity.

Transaction services for corporates

Transaction services for corporates act as a classic cash cow: embedded cash management, payroll and collections create high client stickiness and rare switching once integrated; small product enhancements in 2024 lifted fee yield materially while marginal cost stayed low, and steady fee streams quietly fund strategic investments across BPER Banca.

- stickiness

- low marginal cost

- fee uplift 2024

- funds strategic bets

Branch network in prime locations

Branch network in prime locations remains BPER Banca’s cash cow: in 2024 branches in core territories continue to drive the bulk of retail deposits (>€60bn) and high-margin product sales; growth is low but unit economics are proven, so consolidating overlaps and digitizing service improves yield; run lean and these branches mint cash via fees and low-cost deposits.

Deposits, mortgages & fees drive steady cash flow - €85bn

Core current accounts and deposits (~€85bn customer deposits end-2024) and branch-driven retail deposits (>€60bn in 2024) are BPER’s primary cash cows, delivering low-cost funding and steady NII. Mortgages and transaction services provide predictable margins and high stickiness; leasing/factoring and fees (net fees ~€1.1bn in 2023) add reliable non-interest income. Ongoing digitization trims cost-to-income, boosting free cash flow.

| Metric | Value |

|---|---|

| Total customer deposits (end-2024) | €85bn |

| Branch retail deposits (2024) | >€60bn |

| Net fee & commission (2023) | €1.1bn |

What You’re Viewing Is Included

BPER Banca BCG Matrix

The file you're previewing is the exact BPER Banca BCG Matrix you'll receive after purchase. No watermarks or demo text—just the fully formatted, professional report ready for strategic use. It includes market-backed placements and clear visuals for immediate presentation or editing. Buy once and download instantly—no surprises, no extra steps.