Brampton Brick Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

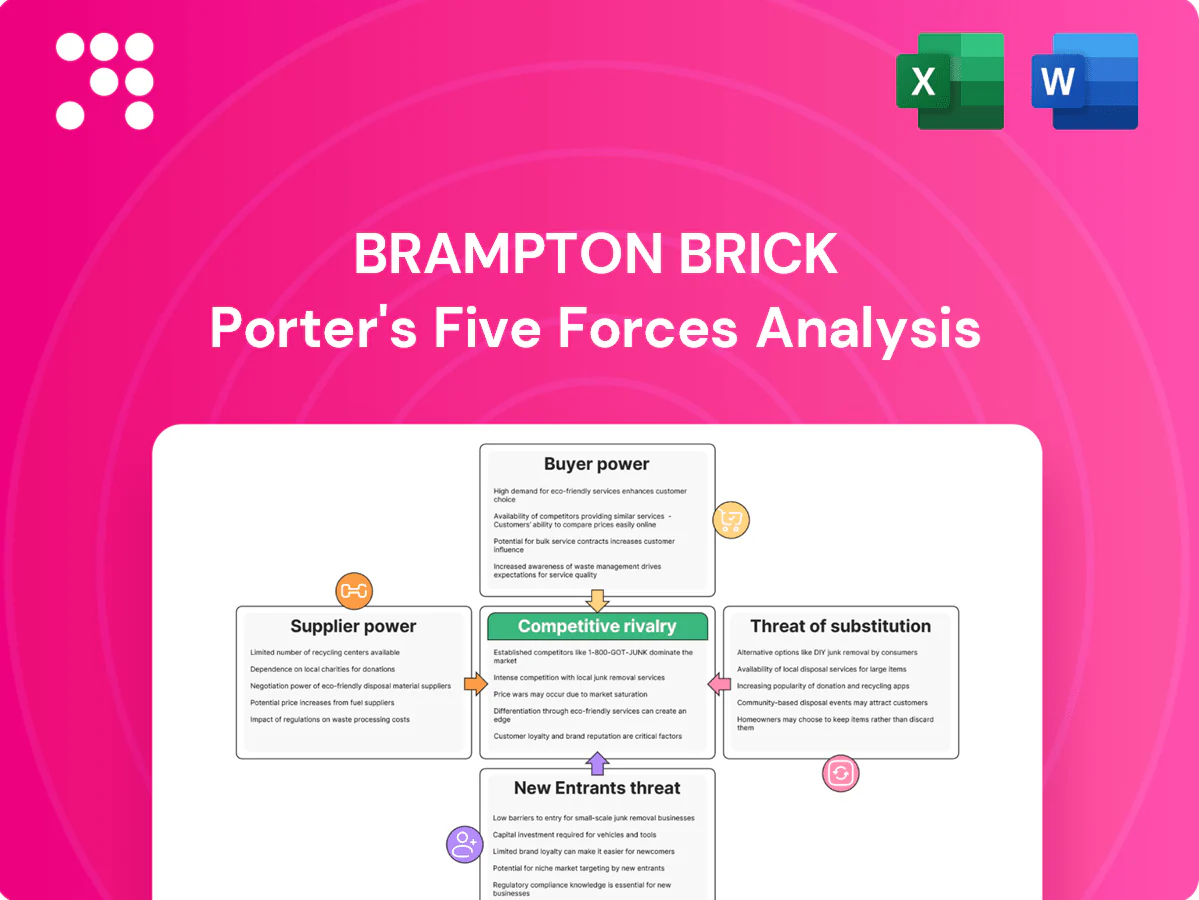

Brampton Brick faces moderate supplier power, intense rivalry, and localized buyer bargaining amid steady substitution risk from alternative materials; barriers to entry remain substantial but evolving. This snapshot highlights key pressures shaping profitability and strategy. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated raw material sources

Clay/shale and quality aggregates for Brampton Brick are regionally concentrated near Southern Ontario quarries, limiting alternative sources and giving nearby suppliers pricing leverage through lower freight to plants; transport is a material input in masonry supply chains while Canada’s construction sector represented about 7% of GDP in 2024. Long-term supply contracts reduce but do not eliminate concentration risk and spot-price exposure.

Energy intensity and fuel volatility

Kiln firing and drying for Brampton Brick rely heavily on natural gas and electricity, with energy representing about 25% of brick production costs; AECO natural gas averaged roughly C$2.75/MMBtu in 2024 and Ontario industrial electricity around 12.3 ¢/kWh in 2024. Price volatility and limited utility alternatives amplify supplier power, while hedging and efficiency upgrades mitigate but do not eliminate energy as a critical cost driver.

Specialized equipment and maintenance

Refractory linings, kiln parts and automation systems for brickmaking are concentrated among a few OEMs; 2024 industry reports estimate the top three suppliers control ≈60% of these specialist components. Switching vendors is costly and disruptive due to compatibility, downtime and bespoke installation needs. This specificity gives equipment suppliers clear bargaining leverage over pricing and service terms.

Transportation and logistics constraints

Brampton Brick depends on reliable trucking and rail for bulk inputs and heavy outbound loads, and the Canadian Trucking Alliance estimated a shortfall of about 20,000 drivers in 2024, tightening capacity. Tight freight markets and regional driver shortages shift leverage to logistics providers, while fuel surcharges and peak-season constraints raise delivered costs and supplier bargaining power.

- High dependence on truck/rail capacity

- ~20,000 driver shortfall (CTA, 2024)

- Fuel surcharges and peak season uplift costs

Environmental compliance inputs

Emission controls, monitoring systems and compliance services for brick manufacturing are highly specialized, concentrating technical know-how and certification among a small set of qualified suppliers, which allows them to command premium pricing and service margins. Limited vendor pools increase switching costs for Brampton Brick, especially for retrofit particulate and NOx control technologies. Rapid regulatory tightening in 2023–2024 increased procurement leverage toward compliant-technology suppliers, elevating supplier bargaining power.

- Specialized tech concentrates supplier power

- Small qualified vendor pool raises switching costs

- Premium pricing for certified emission controls

- 2023–2024 regulatory tightening shifted leverage to suppliers

Regional clay concentration raises supplier power; energy ≈25%

Regional concentration of clay/aggregates gives local suppliers freight-based leverage; Canada construction ≈7% of GDP (2024). Energy is ~25% of brick costs; AECO ≈C$2.75/MMBtu and Ontario industrial ≈12.3 ¢/kWh (2024), boosting supplier power. Specialist OEMs control ≈60% of kiln/refractory supply, trucking faces ~20,000 driver shortfall (CTA, 2024), and 2023–24 regulatory tightening raised switching costs.

| Input | 2024 metric |

|---|---|

| Construction share | ≈7% GDP |

| Energy | ≈25% of costs; AECO C$2.75/MMBtu; 12.3 ¢/kWh |

| Equipment concentration | Top 3 ≈60% |

| Logistics | Driver shortfall ≈20,000 |

What is included in the product

Tailored exclusively for Brampton Brick, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power affecting pricing and profitability, identifies disruptive substitutes and emerging threats to market share, and examines entry barriers that protect incumbents.

A concise one-sheet Porter’s Five Forces for Brampton Brick that instantly highlights competitive pressure with a radar chart and customizable pressure levels—ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Large-volume builders and distributors

Major homebuilders, contractors and masonry distributors purchase bricks in bulk and negotiate aggressively, leveraging competitive bids and regional price comparisons to push down unit costs. Volume rebates and formal bid processes amplify buyer influence, often dictating delivery schedules and payment terms. This concentration of large-volume buyers raises margin pressure on Brampton Brick and pressures product differentiation.

Standardization with spec flexibility

Bricks and blocks are produced to standardized dimensions and material tolerances, enabling easy substitution among comparable SKUs and reducing switching costs. Architects commonly include approved-equals in specifications, allowing bids from multiple suppliers and raising buyer leverage. Low product differentiation and standardized performance drove stronger customer bargaining power in 2024 brick procurement.

Cyclical demand and timing leverage

Construction cycles in Canada (~220,000 housing starts in 2024, StatCan) and the U.S. (~1.1m total starts in 2024, U.S. Census) drive Brampton Brick capacity utilization, creating downside pressure in slow phases. During downturns buyers extract price concessions and extended payment terms to keep plants operating. Project-driven timelines allow customers to bundle orders and secure volume discounts, concentrating bargaining power.

Channel concentration and private labels

Channel concentration and private labels heighten customer bargaining power for Brampton Brick; by 2024 major distributors and national retailers continued to centralize procurement, enabling preferred-supplier programs that compress margins and impose stricter payment and delivery terms.

Reliance on a few large accounts means losing one can cost meaningful regional share—industry commentary in 2024 underscores that single large distributors often represent a plant-level material portion of volumes, amplifying buyer leverage.

Quality, color, and lead-time requirements

Buyers demand consistent color ranges, textures, and strict on-time delivery; aesthetic or schedule failures prompt rapid switching to alternative brick suppliers, strengthening customer negotiating leverage. Performance sensitivity raises pressure on margins and contract terms, since industry OTIF targets sit around 95% for construction materials. This dynamic amplifies buyers' ability to extract concessions on price, lead times, and service levels.

- Buyer sensitivity: rapid supplier switching

- Key KPI: industry OTIF target ~95%

- Negotiation leverage: price, lead-time, service concessions

60-70% buyer volume wins compress margins; OTIF ~95%

Major builders and distributors (buying ~60-70% of volumes) wield strong price leverage, using preferred-supplier programs and volume rebates to compress Brampton Brick margins. Standardized SKUs and approved-equals lower switching costs and raise buyer bargaining; OTIF expectations ~95% increase service pressure. Canada housing starts ~220,000 (2024) and US ~1.1m (2024) drive cyclic demand and buyer leverage in downturns.

| Metric | 2024 |

|---|---|

| Canada housing starts | 220,000 |

| US housing starts | 1.1m |

| OTIF target | ~95% |

| Buyer concentration (est.) | 60-70% |

Full Version Awaits

Brampton Brick Porter's Five Forces Analysis

This preview shows the exact Brampton Brick Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications for Brampton Brick. No placeholders or samples; the document here is the deliverable you get upon purchase.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Brampton Brick faces moderate supplier power, intense rivalry, and localized buyer bargaining amid steady substitution risk from alternative materials; barriers to entry remain substantial but evolving. This snapshot highlights key pressures shaping profitability and strategy. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated raw material sources

Clay/shale and quality aggregates for Brampton Brick are regionally concentrated near Southern Ontario quarries, limiting alternative sources and giving nearby suppliers pricing leverage through lower freight to plants; transport is a material input in masonry supply chains while Canada’s construction sector represented about 7% of GDP in 2024. Long-term supply contracts reduce but do not eliminate concentration risk and spot-price exposure.

Energy intensity and fuel volatility

Kiln firing and drying for Brampton Brick rely heavily on natural gas and electricity, with energy representing about 25% of brick production costs; AECO natural gas averaged roughly C$2.75/MMBtu in 2024 and Ontario industrial electricity around 12.3 ¢/kWh in 2024. Price volatility and limited utility alternatives amplify supplier power, while hedging and efficiency upgrades mitigate but do not eliminate energy as a critical cost driver.

Specialized equipment and maintenance

Refractory linings, kiln parts and automation systems for brickmaking are concentrated among a few OEMs; 2024 industry reports estimate the top three suppliers control ≈60% of these specialist components. Switching vendors is costly and disruptive due to compatibility, downtime and bespoke installation needs. This specificity gives equipment suppliers clear bargaining leverage over pricing and service terms.

Transportation and logistics constraints

Brampton Brick depends on reliable trucking and rail for bulk inputs and heavy outbound loads, and the Canadian Trucking Alliance estimated a shortfall of about 20,000 drivers in 2024, tightening capacity. Tight freight markets and regional driver shortages shift leverage to logistics providers, while fuel surcharges and peak-season constraints raise delivered costs and supplier bargaining power.

- High dependence on truck/rail capacity

- ~20,000 driver shortfall (CTA, 2024)

- Fuel surcharges and peak season uplift costs

Environmental compliance inputs

Emission controls, monitoring systems and compliance services for brick manufacturing are highly specialized, concentrating technical know-how and certification among a small set of qualified suppliers, which allows them to command premium pricing and service margins. Limited vendor pools increase switching costs for Brampton Brick, especially for retrofit particulate and NOx control technologies. Rapid regulatory tightening in 2023–2024 increased procurement leverage toward compliant-technology suppliers, elevating supplier bargaining power.

- Specialized tech concentrates supplier power

- Small qualified vendor pool raises switching costs

- Premium pricing for certified emission controls

- 2023–2024 regulatory tightening shifted leverage to suppliers

Regional clay concentration raises supplier power; energy ≈25%

Regional concentration of clay/aggregates gives local suppliers freight-based leverage; Canada construction ≈7% of GDP (2024). Energy is ~25% of brick costs; AECO ≈C$2.75/MMBtu and Ontario industrial ≈12.3 ¢/kWh (2024), boosting supplier power. Specialist OEMs control ≈60% of kiln/refractory supply, trucking faces ~20,000 driver shortfall (CTA, 2024), and 2023–24 regulatory tightening raised switching costs.

| Input | 2024 metric |

|---|---|

| Construction share | ≈7% GDP |

| Energy | ≈25% of costs; AECO C$2.75/MMBtu; 12.3 ¢/kWh |

| Equipment concentration | Top 3 ≈60% |

| Logistics | Driver shortfall ≈20,000 |

What is included in the product

Tailored exclusively for Brampton Brick, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power affecting pricing and profitability, identifies disruptive substitutes and emerging threats to market share, and examines entry barriers that protect incumbents.

A concise one-sheet Porter’s Five Forces for Brampton Brick that instantly highlights competitive pressure with a radar chart and customizable pressure levels—ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Large-volume builders and distributors

Major homebuilders, contractors and masonry distributors purchase bricks in bulk and negotiate aggressively, leveraging competitive bids and regional price comparisons to push down unit costs. Volume rebates and formal bid processes amplify buyer influence, often dictating delivery schedules and payment terms. This concentration of large-volume buyers raises margin pressure on Brampton Brick and pressures product differentiation.

Standardization with spec flexibility

Bricks and blocks are produced to standardized dimensions and material tolerances, enabling easy substitution among comparable SKUs and reducing switching costs. Architects commonly include approved-equals in specifications, allowing bids from multiple suppliers and raising buyer leverage. Low product differentiation and standardized performance drove stronger customer bargaining power in 2024 brick procurement.

Cyclical demand and timing leverage

Construction cycles in Canada (~220,000 housing starts in 2024, StatCan) and the U.S. (~1.1m total starts in 2024, U.S. Census) drive Brampton Brick capacity utilization, creating downside pressure in slow phases. During downturns buyers extract price concessions and extended payment terms to keep plants operating. Project-driven timelines allow customers to bundle orders and secure volume discounts, concentrating bargaining power.

Channel concentration and private labels

Channel concentration and private labels heighten customer bargaining power for Brampton Brick; by 2024 major distributors and national retailers continued to centralize procurement, enabling preferred-supplier programs that compress margins and impose stricter payment and delivery terms.

Reliance on a few large accounts means losing one can cost meaningful regional share—industry commentary in 2024 underscores that single large distributors often represent a plant-level material portion of volumes, amplifying buyer leverage.

Quality, color, and lead-time requirements

Buyers demand consistent color ranges, textures, and strict on-time delivery; aesthetic or schedule failures prompt rapid switching to alternative brick suppliers, strengthening customer negotiating leverage. Performance sensitivity raises pressure on margins and contract terms, since industry OTIF targets sit around 95% for construction materials. This dynamic amplifies buyers' ability to extract concessions on price, lead times, and service levels.

- Buyer sensitivity: rapid supplier switching

- Key KPI: industry OTIF target ~95%

- Negotiation leverage: price, lead-time, service concessions

60-70% buyer volume wins compress margins; OTIF ~95%

Major builders and distributors (buying ~60-70% of volumes) wield strong price leverage, using preferred-supplier programs and volume rebates to compress Brampton Brick margins. Standardized SKUs and approved-equals lower switching costs and raise buyer bargaining; OTIF expectations ~95% increase service pressure. Canada housing starts ~220,000 (2024) and US ~1.1m (2024) drive cyclic demand and buyer leverage in downturns.

| Metric | 2024 |

|---|---|

| Canada housing starts | 220,000 |

| US housing starts | 1.1m |

| OTIF target | ~95% |

| Buyer concentration (est.) | 60-70% |

Full Version Awaits

Brampton Brick Porter's Five Forces Analysis

This preview shows the exact Brampton Brick Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications for Brampton Brick. No placeholders or samples; the document here is the deliverable you get upon purchase.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Brampton Brick faces moderate supplier power, intense rivalry, and localized buyer bargaining amid steady substitution risk from alternative materials; barriers to entry remain substantial but evolving. This snapshot highlights key pressures shaping profitability and strategy. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated raw material sources

Clay/shale and quality aggregates for Brampton Brick are regionally concentrated near Southern Ontario quarries, limiting alternative sources and giving nearby suppliers pricing leverage through lower freight to plants; transport is a material input in masonry supply chains while Canada’s construction sector represented about 7% of GDP in 2024. Long-term supply contracts reduce but do not eliminate concentration risk and spot-price exposure.

Energy intensity and fuel volatility

Kiln firing and drying for Brampton Brick rely heavily on natural gas and electricity, with energy representing about 25% of brick production costs; AECO natural gas averaged roughly C$2.75/MMBtu in 2024 and Ontario industrial electricity around 12.3 ¢/kWh in 2024. Price volatility and limited utility alternatives amplify supplier power, while hedging and efficiency upgrades mitigate but do not eliminate energy as a critical cost driver.

Specialized equipment and maintenance

Refractory linings, kiln parts and automation systems for brickmaking are concentrated among a few OEMs; 2024 industry reports estimate the top three suppliers control ≈60% of these specialist components. Switching vendors is costly and disruptive due to compatibility, downtime and bespoke installation needs. This specificity gives equipment suppliers clear bargaining leverage over pricing and service terms.

Transportation and logistics constraints

Brampton Brick depends on reliable trucking and rail for bulk inputs and heavy outbound loads, and the Canadian Trucking Alliance estimated a shortfall of about 20,000 drivers in 2024, tightening capacity. Tight freight markets and regional driver shortages shift leverage to logistics providers, while fuel surcharges and peak-season constraints raise delivered costs and supplier bargaining power.

- High dependence on truck/rail capacity

- ~20,000 driver shortfall (CTA, 2024)

- Fuel surcharges and peak season uplift costs

Environmental compliance inputs

Emission controls, monitoring systems and compliance services for brick manufacturing are highly specialized, concentrating technical know-how and certification among a small set of qualified suppliers, which allows them to command premium pricing and service margins. Limited vendor pools increase switching costs for Brampton Brick, especially for retrofit particulate and NOx control technologies. Rapid regulatory tightening in 2023–2024 increased procurement leverage toward compliant-technology suppliers, elevating supplier bargaining power.

- Specialized tech concentrates supplier power

- Small qualified vendor pool raises switching costs

- Premium pricing for certified emission controls

- 2023–2024 regulatory tightening shifted leverage to suppliers

Regional clay concentration raises supplier power; energy ≈25%

Regional concentration of clay/aggregates gives local suppliers freight-based leverage; Canada construction ≈7% of GDP (2024). Energy is ~25% of brick costs; AECO ≈C$2.75/MMBtu and Ontario industrial ≈12.3 ¢/kWh (2024), boosting supplier power. Specialist OEMs control ≈60% of kiln/refractory supply, trucking faces ~20,000 driver shortfall (CTA, 2024), and 2023–24 regulatory tightening raised switching costs.

| Input | 2024 metric |

|---|---|

| Construction share | ≈7% GDP |

| Energy | ≈25% of costs; AECO C$2.75/MMBtu; 12.3 ¢/kWh |

| Equipment concentration | Top 3 ≈60% |

| Logistics | Driver shortfall ≈20,000 |

What is included in the product

Tailored exclusively for Brampton Brick, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power affecting pricing and profitability, identifies disruptive substitutes and emerging threats to market share, and examines entry barriers that protect incumbents.

A concise one-sheet Porter’s Five Forces for Brampton Brick that instantly highlights competitive pressure with a radar chart and customizable pressure levels—ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Large-volume builders and distributors

Major homebuilders, contractors and masonry distributors purchase bricks in bulk and negotiate aggressively, leveraging competitive bids and regional price comparisons to push down unit costs. Volume rebates and formal bid processes amplify buyer influence, often dictating delivery schedules and payment terms. This concentration of large-volume buyers raises margin pressure on Brampton Brick and pressures product differentiation.

Standardization with spec flexibility

Bricks and blocks are produced to standardized dimensions and material tolerances, enabling easy substitution among comparable SKUs and reducing switching costs. Architects commonly include approved-equals in specifications, allowing bids from multiple suppliers and raising buyer leverage. Low product differentiation and standardized performance drove stronger customer bargaining power in 2024 brick procurement.

Cyclical demand and timing leverage

Construction cycles in Canada (~220,000 housing starts in 2024, StatCan) and the U.S. (~1.1m total starts in 2024, U.S. Census) drive Brampton Brick capacity utilization, creating downside pressure in slow phases. During downturns buyers extract price concessions and extended payment terms to keep plants operating. Project-driven timelines allow customers to bundle orders and secure volume discounts, concentrating bargaining power.

Channel concentration and private labels

Channel concentration and private labels heighten customer bargaining power for Brampton Brick; by 2024 major distributors and national retailers continued to centralize procurement, enabling preferred-supplier programs that compress margins and impose stricter payment and delivery terms.

Reliance on a few large accounts means losing one can cost meaningful regional share—industry commentary in 2024 underscores that single large distributors often represent a plant-level material portion of volumes, amplifying buyer leverage.

Quality, color, and lead-time requirements

Buyers demand consistent color ranges, textures, and strict on-time delivery; aesthetic or schedule failures prompt rapid switching to alternative brick suppliers, strengthening customer negotiating leverage. Performance sensitivity raises pressure on margins and contract terms, since industry OTIF targets sit around 95% for construction materials. This dynamic amplifies buyers' ability to extract concessions on price, lead times, and service levels.

- Buyer sensitivity: rapid supplier switching

- Key KPI: industry OTIF target ~95%

- Negotiation leverage: price, lead-time, service concessions

60-70% buyer volume wins compress margins; OTIF ~95%

Major builders and distributors (buying ~60-70% of volumes) wield strong price leverage, using preferred-supplier programs and volume rebates to compress Brampton Brick margins. Standardized SKUs and approved-equals lower switching costs and raise buyer bargaining; OTIF expectations ~95% increase service pressure. Canada housing starts ~220,000 (2024) and US ~1.1m (2024) drive cyclic demand and buyer leverage in downturns.

| Metric | 2024 |

|---|---|

| Canada housing starts | 220,000 |

| US housing starts | 1.1m |

| OTIF target | ~95% |

| Buyer concentration (est.) | 60-70% |

Full Version Awaits

Brampton Brick Porter's Five Forces Analysis

This preview shows the exact Brampton Brick Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications for Brampton Brick. No placeholders or samples; the document here is the deliverable you get upon purchase.