Brampton Brick SWOT Analysis

Your Strategic Toolkit Starts Here

Brampton Brick’s SWOT highlights durable market position in Canadian masonry and manufacturing scale, offset by commodity exposure and cyclical construction demand; opportunities include urban infill and sustainable product lines, while supply-chain pressures and regulatory shifts pose risks. Want deeper, research-backed insights and actionable strategies? Purchase the complete SWOT analysis—fully editable Word and Excel deliverables for planning, pitching, and investing.

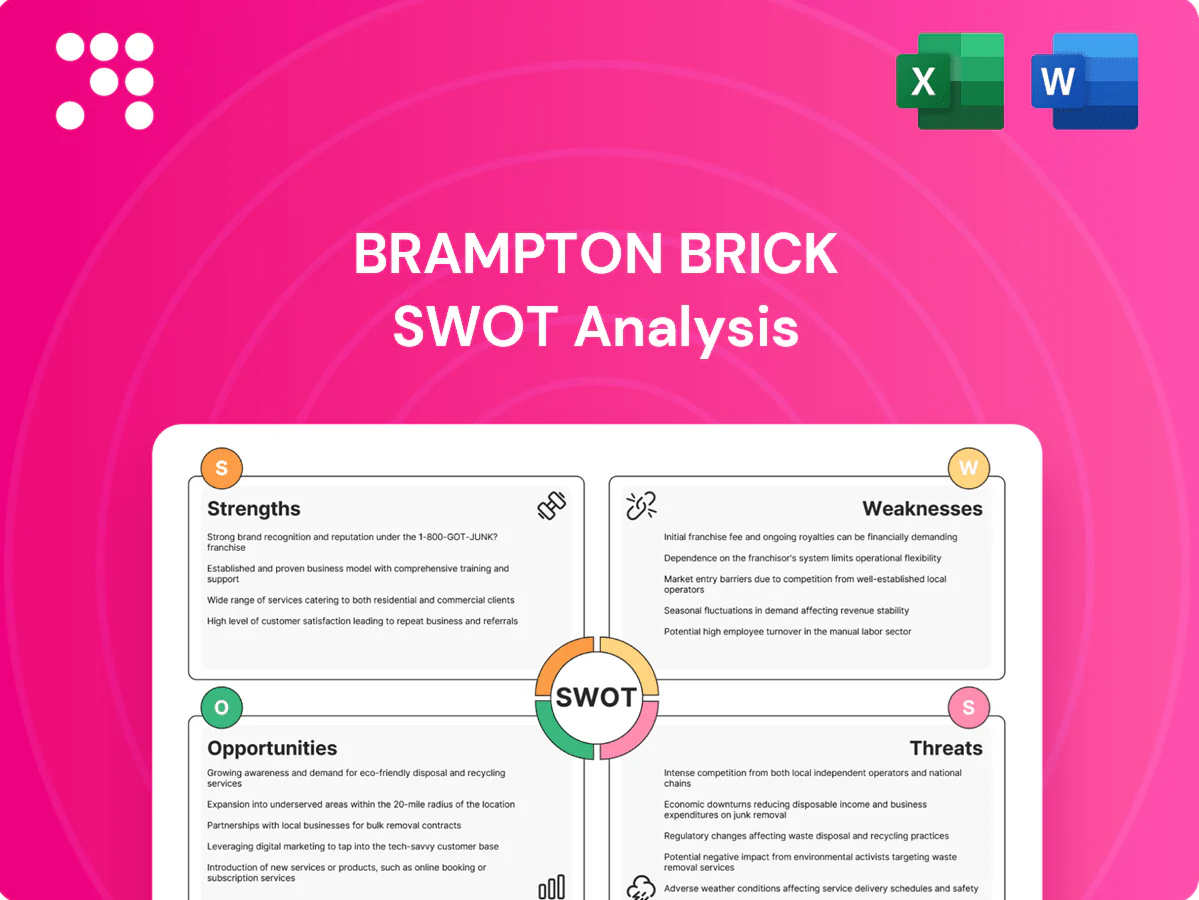

Strengths

Established regional footprint

Serving Ontario (≈15.0M), Quebec (≈8.6M) and the U.S. Northeast/Midwest (≈124M) anchors demand across diversified construction cycles; proximity to core markets trims long‑haul freight exposure for heavy masonry; longstanding local presence deepens distributor and contractor relationships; this footprint underpins steady share across residential and non‑residential jobs.

Diverse masonry portfolio

Diverse masonry portfolio of clay bricks and concrete blocks lets Brampton Brick address aesthetic residential facades and structural commercial walls, enabling cross-selling across channels. Mix flexibility helps balance cyclical segments and supports participation in specification-driven projects. The business leverages over 100 years of industry experience to win architect specifications.

Manufacturing scale and process know-how

High-temperature tunnel kilns (typically 1,100–1,300°C) and precise batching expertise at Brampton Brick support consistent brick quality across runs, reducing color and strength variance. Scale efficiencies drive lower unit costs versus smaller rivals through higher throughput and fixed-cost absorption. Robust process control helps meet rigorous building codes and architect specifications, while years of production experience cut scrap and sustain on-time delivery rates above 95%.

Channel relationships and brand credibility

Relationships with dealers, masons and builders drive repeat business and steady project pipelines. Brand recognition in core provinces supports specification inclusion on regional projects. Strong service levels and fast fulfillment win schedule-sensitive contracts. Institutional credibility lowers perceived risk for architects and developers, easing design approvals.

- Dealer and mason network: repeat sales

- Provincial brand pull: spec inclusion

- High service levels: schedule wins

- Credibility: reduced design/developer risk

Balanced end-market exposure

Brampton Brick benefits from balanced end-market exposure, supplying both residential and non-residential sectors which smooths revenue volatility; Canada housing starts ran near a 200,000 annualized pace in 2024, while institutional and public projects provided countercyclical volumes. Renovation and urban infill demand—Canada renovation spending about C$60B in 2023–24—adds resilience, supporting plant utilization and pricing discipline.

- Residential + non-residential diversification

- Public/institutional offset to housing slowdowns

- Renovation/infill demand supports volumes

- Improves utilization and pricing discipline

ON/QC/Midwest: 148M reach, > 95% on-time

Broad Ontario/Quebec/US Midwest footprint (pop ≈148M) cuts freight and secures steady share across cycles; diversified clay and concrete portfolio plus 100+ years' expertise wins specs. High-temp kilns and scale yield >95% on-time delivery and lower unit costs. Balanced residential/non-residential mix (Canada housing starts ≈200k in 2024; renovation spend C$60B) stabilizes volumes.

| Metric | Value |

|---|---|

| Population reach | ≈148M |

| Canada housing starts (2024) | ≈200k |

| Renovation spend | C$60B |

| On-time delivery | >95% |

What is included in the product

Provides a concise SWOT overview of Brampton Brick, highlighting internal strengths and weaknesses alongside external opportunities and threats shaping its competitive position and strategic prospects.

Provides a concise, at-a-glance SWOT matrix for Brampton Brick to streamline strategic actions and relieve decision bottlenecks; editable format enables rapid updates as market conditions shift.

Weaknesses

Geographic concentration

Heavy reliance on Ontario and Quebec (combined 61.5% of Canada’s population per 2021 Census) and nearby U.S. Northeast markets limits geographic diversification; regional recessions or housing-policy shifts can quickly reduce brick volumes. Weather-driven seasonality and winter site productivity swings depress quarterly output. Limited exposure to fast-growing U.S. Sun Belt markets constrains growth runway.

Energy-intensive cost base

Kilns and cement processes at Brampton Brick are heavily dependent on natural gas and electricity for firing and calcination, making energy a major cost driver. Input-price volatility can compress margins if sales pricing lags spot moves. Canada's federal carbon price reached CAD 65/tonne in 2023 and is slated to rise, increasing operating costs over time. Hedging programs reduce but do not eliminate exposure to sharp energy spikes.

Commodity-like pricing pressure

Bricks and blocks face intense price-based competition, with many contractors switching among comparable SKUs when specifications permit, pressuring unit prices.

During downturns discounting quickly erodes margins as volume declines and fixed costs remain, reducing profitability for commodity producers.

Differentiation is increasingly difficult versus premium cladding alternatives that command higher margins and design-driven demand.

Capital intensity and maintenance

Plants require ongoing capex for kilns, molds and handling systems, and unplanned downtime can disrupt deliveries and raise unit costs. High fixed costs magnify the impact of volume swings on margins, while long equipment payback periods reduce flexibility in slow markets.

- Ongoing capex for kilns and molds

- Downtime disrupts deliveries and raises costs

- High fixed costs amplify volume risk

- Long payback in slow demand

Seasonality and project timing

Seasonality drives winter construction slowdowns that reduce Brampton Brick shipments and push revenue recognition into warmer months, causing quarter-to-quarter volatility and delaying cash inflows.

Weather-related delays increase work-in-process and finished goods, swelling working capital through higher inventory and receivables; utilization swings complicate labor scheduling and logistics, raising per-unit costs.

- Winter shipment declines

- Revenue timing shifts

- Higher inventory & receivables

- Variable utilization → labor/logistics strain

Ontario+Quebec 61.5%; carbon to CAD 170/t raises costs

Heavy reliance on Ontario and Quebec (61.5% of Canada’s population per 2021 Census) limits geographic diversification and exposure to regional housing cycles. Kilns and cement processes are energy-intensive; Canada’s federal carbon price reached CAD 65/tonne in 2023 and is scheduled to rise toward CAD 170/tonne by 2030, raising operating costs. Seasonality compresses winter shipments and increases working capital needs.

| Weakness | Key fact |

|---|---|

| Geographic concentration | Ontario+Quebec = 61.5% (2021 Census) |

| Carbon cost risk | CAD 65/t (2023); target ≈ CAD 170/t by 2030 |

| Seasonality | Winter shipment declines → higher inventory |

Same Document Delivered

Brampton Brick SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Brampton Brick's strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable version ready for use.

Your Strategic Toolkit Starts Here

Brampton Brick’s SWOT highlights durable market position in Canadian masonry and manufacturing scale, offset by commodity exposure and cyclical construction demand; opportunities include urban infill and sustainable product lines, while supply-chain pressures and regulatory shifts pose risks. Want deeper, research-backed insights and actionable strategies? Purchase the complete SWOT analysis—fully editable Word and Excel deliverables for planning, pitching, and investing.

Strengths

Established regional footprint

Serving Ontario (≈15.0M), Quebec (≈8.6M) and the U.S. Northeast/Midwest (≈124M) anchors demand across diversified construction cycles; proximity to core markets trims long‑haul freight exposure for heavy masonry; longstanding local presence deepens distributor and contractor relationships; this footprint underpins steady share across residential and non‑residential jobs.

Diverse masonry portfolio

Diverse masonry portfolio of clay bricks and concrete blocks lets Brampton Brick address aesthetic residential facades and structural commercial walls, enabling cross-selling across channels. Mix flexibility helps balance cyclical segments and supports participation in specification-driven projects. The business leverages over 100 years of industry experience to win architect specifications.

Manufacturing scale and process know-how

High-temperature tunnel kilns (typically 1,100–1,300°C) and precise batching expertise at Brampton Brick support consistent brick quality across runs, reducing color and strength variance. Scale efficiencies drive lower unit costs versus smaller rivals through higher throughput and fixed-cost absorption. Robust process control helps meet rigorous building codes and architect specifications, while years of production experience cut scrap and sustain on-time delivery rates above 95%.

Channel relationships and brand credibility

Relationships with dealers, masons and builders drive repeat business and steady project pipelines. Brand recognition in core provinces supports specification inclusion on regional projects. Strong service levels and fast fulfillment win schedule-sensitive contracts. Institutional credibility lowers perceived risk for architects and developers, easing design approvals.

- Dealer and mason network: repeat sales

- Provincial brand pull: spec inclusion

- High service levels: schedule wins

- Credibility: reduced design/developer risk

Balanced end-market exposure

Brampton Brick benefits from balanced end-market exposure, supplying both residential and non-residential sectors which smooths revenue volatility; Canada housing starts ran near a 200,000 annualized pace in 2024, while institutional and public projects provided countercyclical volumes. Renovation and urban infill demand—Canada renovation spending about C$60B in 2023–24—adds resilience, supporting plant utilization and pricing discipline.

- Residential + non-residential diversification

- Public/institutional offset to housing slowdowns

- Renovation/infill demand supports volumes

- Improves utilization and pricing discipline

ON/QC/Midwest: 148M reach, > 95% on-time

Broad Ontario/Quebec/US Midwest footprint (pop ≈148M) cuts freight and secures steady share across cycles; diversified clay and concrete portfolio plus 100+ years' expertise wins specs. High-temp kilns and scale yield >95% on-time delivery and lower unit costs. Balanced residential/non-residential mix (Canada housing starts ≈200k in 2024; renovation spend C$60B) stabilizes volumes.

| Metric | Value |

|---|---|

| Population reach | ≈148M |

| Canada housing starts (2024) | ≈200k |

| Renovation spend | C$60B |

| On-time delivery | >95% |

What is included in the product

Provides a concise SWOT overview of Brampton Brick, highlighting internal strengths and weaknesses alongside external opportunities and threats shaping its competitive position and strategic prospects.

Provides a concise, at-a-glance SWOT matrix for Brampton Brick to streamline strategic actions and relieve decision bottlenecks; editable format enables rapid updates as market conditions shift.

Weaknesses

Geographic concentration

Heavy reliance on Ontario and Quebec (combined 61.5% of Canada’s population per 2021 Census) and nearby U.S. Northeast markets limits geographic diversification; regional recessions or housing-policy shifts can quickly reduce brick volumes. Weather-driven seasonality and winter site productivity swings depress quarterly output. Limited exposure to fast-growing U.S. Sun Belt markets constrains growth runway.

Energy-intensive cost base

Kilns and cement processes at Brampton Brick are heavily dependent on natural gas and electricity for firing and calcination, making energy a major cost driver. Input-price volatility can compress margins if sales pricing lags spot moves. Canada's federal carbon price reached CAD 65/tonne in 2023 and is slated to rise, increasing operating costs over time. Hedging programs reduce but do not eliminate exposure to sharp energy spikes.

Commodity-like pricing pressure

Bricks and blocks face intense price-based competition, with many contractors switching among comparable SKUs when specifications permit, pressuring unit prices.

During downturns discounting quickly erodes margins as volume declines and fixed costs remain, reducing profitability for commodity producers.

Differentiation is increasingly difficult versus premium cladding alternatives that command higher margins and design-driven demand.

Capital intensity and maintenance

Plants require ongoing capex for kilns, molds and handling systems, and unplanned downtime can disrupt deliveries and raise unit costs. High fixed costs magnify the impact of volume swings on margins, while long equipment payback periods reduce flexibility in slow markets.

- Ongoing capex for kilns and molds

- Downtime disrupts deliveries and raises costs

- High fixed costs amplify volume risk

- Long payback in slow demand

Seasonality and project timing

Seasonality drives winter construction slowdowns that reduce Brampton Brick shipments and push revenue recognition into warmer months, causing quarter-to-quarter volatility and delaying cash inflows.

Weather-related delays increase work-in-process and finished goods, swelling working capital through higher inventory and receivables; utilization swings complicate labor scheduling and logistics, raising per-unit costs.

- Winter shipment declines

- Revenue timing shifts

- Higher inventory & receivables

- Variable utilization → labor/logistics strain

Ontario+Quebec 61.5%; carbon to CAD 170/t raises costs

Heavy reliance on Ontario and Quebec (61.5% of Canada’s population per 2021 Census) limits geographic diversification and exposure to regional housing cycles. Kilns and cement processes are energy-intensive; Canada’s federal carbon price reached CAD 65/tonne in 2023 and is scheduled to rise toward CAD 170/tonne by 2030, raising operating costs. Seasonality compresses winter shipments and increases working capital needs.

| Weakness | Key fact |

|---|---|

| Geographic concentration | Ontario+Quebec = 61.5% (2021 Census) |

| Carbon cost risk | CAD 65/t (2023); target ≈ CAD 170/t by 2030 |

| Seasonality | Winter shipment declines → higher inventory |

Same Document Delivered

Brampton Brick SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Brampton Brick's strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable version ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Brampton Brick’s SWOT highlights durable market position in Canadian masonry and manufacturing scale, offset by commodity exposure and cyclical construction demand; opportunities include urban infill and sustainable product lines, while supply-chain pressures and regulatory shifts pose risks. Want deeper, research-backed insights and actionable strategies? Purchase the complete SWOT analysis—fully editable Word and Excel deliverables for planning, pitching, and investing.

Strengths

Established regional footprint

Serving Ontario (≈15.0M), Quebec (≈8.6M) and the U.S. Northeast/Midwest (≈124M) anchors demand across diversified construction cycles; proximity to core markets trims long‑haul freight exposure for heavy masonry; longstanding local presence deepens distributor and contractor relationships; this footprint underpins steady share across residential and non‑residential jobs.

Diverse masonry portfolio

Diverse masonry portfolio of clay bricks and concrete blocks lets Brampton Brick address aesthetic residential facades and structural commercial walls, enabling cross-selling across channels. Mix flexibility helps balance cyclical segments and supports participation in specification-driven projects. The business leverages over 100 years of industry experience to win architect specifications.

Manufacturing scale and process know-how

High-temperature tunnel kilns (typically 1,100–1,300°C) and precise batching expertise at Brampton Brick support consistent brick quality across runs, reducing color and strength variance. Scale efficiencies drive lower unit costs versus smaller rivals through higher throughput and fixed-cost absorption. Robust process control helps meet rigorous building codes and architect specifications, while years of production experience cut scrap and sustain on-time delivery rates above 95%.

Channel relationships and brand credibility

Relationships with dealers, masons and builders drive repeat business and steady project pipelines. Brand recognition in core provinces supports specification inclusion on regional projects. Strong service levels and fast fulfillment win schedule-sensitive contracts. Institutional credibility lowers perceived risk for architects and developers, easing design approvals.

- Dealer and mason network: repeat sales

- Provincial brand pull: spec inclusion

- High service levels: schedule wins

- Credibility: reduced design/developer risk

Balanced end-market exposure

Brampton Brick benefits from balanced end-market exposure, supplying both residential and non-residential sectors which smooths revenue volatility; Canada housing starts ran near a 200,000 annualized pace in 2024, while institutional and public projects provided countercyclical volumes. Renovation and urban infill demand—Canada renovation spending about C$60B in 2023–24—adds resilience, supporting plant utilization and pricing discipline.

- Residential + non-residential diversification

- Public/institutional offset to housing slowdowns

- Renovation/infill demand supports volumes

- Improves utilization and pricing discipline

ON/QC/Midwest: 148M reach, > 95% on-time

Broad Ontario/Quebec/US Midwest footprint (pop ≈148M) cuts freight and secures steady share across cycles; diversified clay and concrete portfolio plus 100+ years' expertise wins specs. High-temp kilns and scale yield >95% on-time delivery and lower unit costs. Balanced residential/non-residential mix (Canada housing starts ≈200k in 2024; renovation spend C$60B) stabilizes volumes.

| Metric | Value |

|---|---|

| Population reach | ≈148M |

| Canada housing starts (2024) | ≈200k |

| Renovation spend | C$60B |

| On-time delivery | >95% |

What is included in the product

Provides a concise SWOT overview of Brampton Brick, highlighting internal strengths and weaknesses alongside external opportunities and threats shaping its competitive position and strategic prospects.

Provides a concise, at-a-glance SWOT matrix for Brampton Brick to streamline strategic actions and relieve decision bottlenecks; editable format enables rapid updates as market conditions shift.

Weaknesses

Geographic concentration

Heavy reliance on Ontario and Quebec (combined 61.5% of Canada’s population per 2021 Census) and nearby U.S. Northeast markets limits geographic diversification; regional recessions or housing-policy shifts can quickly reduce brick volumes. Weather-driven seasonality and winter site productivity swings depress quarterly output. Limited exposure to fast-growing U.S. Sun Belt markets constrains growth runway.

Energy-intensive cost base

Kilns and cement processes at Brampton Brick are heavily dependent on natural gas and electricity for firing and calcination, making energy a major cost driver. Input-price volatility can compress margins if sales pricing lags spot moves. Canada's federal carbon price reached CAD 65/tonne in 2023 and is slated to rise, increasing operating costs over time. Hedging programs reduce but do not eliminate exposure to sharp energy spikes.

Commodity-like pricing pressure

Bricks and blocks face intense price-based competition, with many contractors switching among comparable SKUs when specifications permit, pressuring unit prices.

During downturns discounting quickly erodes margins as volume declines and fixed costs remain, reducing profitability for commodity producers.

Differentiation is increasingly difficult versus premium cladding alternatives that command higher margins and design-driven demand.

Capital intensity and maintenance

Plants require ongoing capex for kilns, molds and handling systems, and unplanned downtime can disrupt deliveries and raise unit costs. High fixed costs magnify the impact of volume swings on margins, while long equipment payback periods reduce flexibility in slow markets.

- Ongoing capex for kilns and molds

- Downtime disrupts deliveries and raises costs

- High fixed costs amplify volume risk

- Long payback in slow demand

Seasonality and project timing

Seasonality drives winter construction slowdowns that reduce Brampton Brick shipments and push revenue recognition into warmer months, causing quarter-to-quarter volatility and delaying cash inflows.

Weather-related delays increase work-in-process and finished goods, swelling working capital through higher inventory and receivables; utilization swings complicate labor scheduling and logistics, raising per-unit costs.

- Winter shipment declines

- Revenue timing shifts

- Higher inventory & receivables

- Variable utilization → labor/logistics strain

Ontario+Quebec 61.5%; carbon to CAD 170/t raises costs

Heavy reliance on Ontario and Quebec (61.5% of Canada’s population per 2021 Census) limits geographic diversification and exposure to regional housing cycles. Kilns and cement processes are energy-intensive; Canada’s federal carbon price reached CAD 65/tonne in 2023 and is scheduled to rise toward CAD 170/tonne by 2030, raising operating costs. Seasonality compresses winter shipments and increases working capital needs.

| Weakness | Key fact |

|---|---|

| Geographic concentration | Ontario+Quebec = 61.5% (2021 Census) |

| Carbon cost risk | CAD 65/t (2023); target ≈ CAD 170/t by 2030 |

| Seasonality | Winter shipment declines → higher inventory |

Same Document Delivered

Brampton Brick SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Brampton Brick's strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable version ready for use.