Braskem PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, commodity cycles, and sustainability pressures are reshaping Braskem’s strategic outlook in our concise PESTLE snapshot. Use these insights to spot risks and growth levers for investors and strategists. Purchase the full PESTLE to get detailed, actionable analysis and editable templates for immediate use.

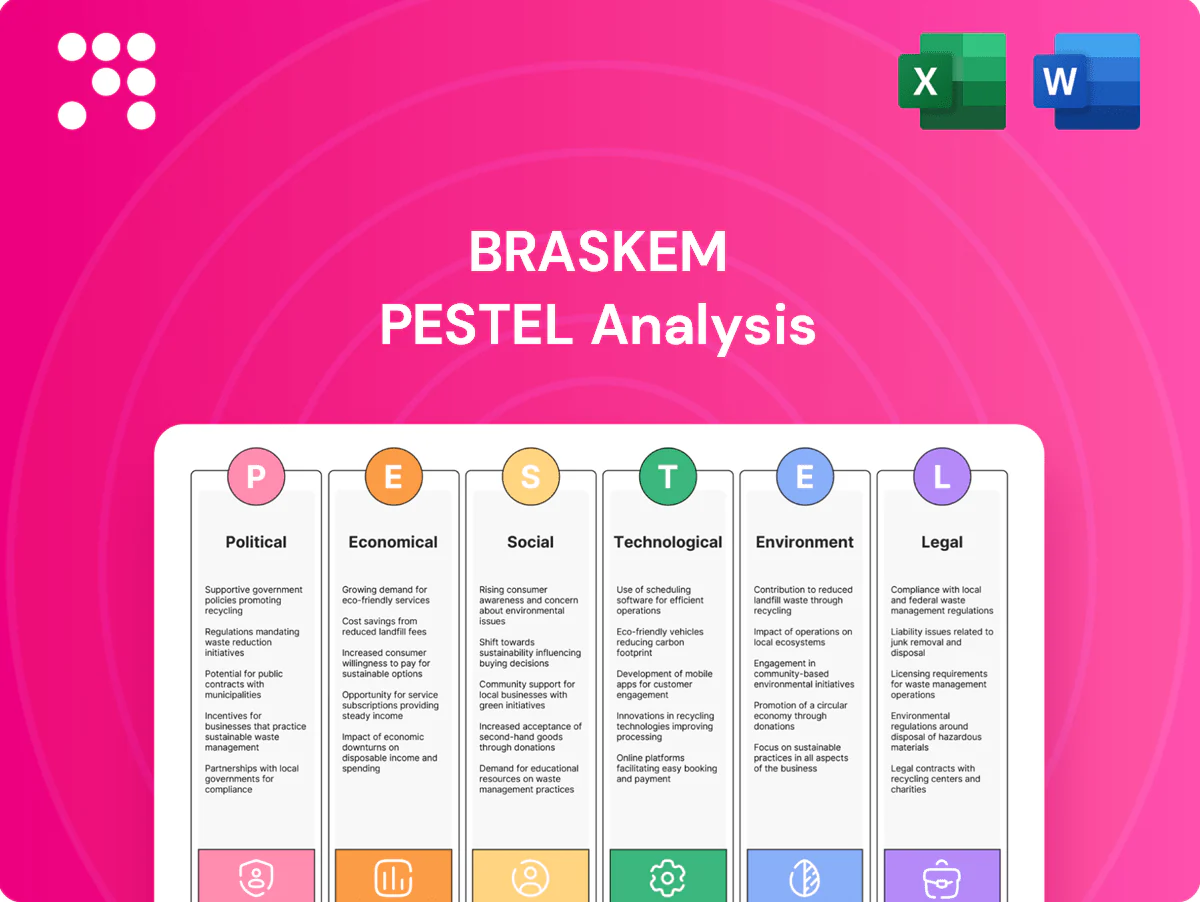

Political factors

Brazilian industrial policy and incentives

Brazilian industrial policy and incentives for petrochemicals and bio-based materials directly influence capital allocation and plant siting for Braskem, the largest petrochemical company in Latin America. BNDES, Brazil’s main development bank, remains a key source of long-term financing, while changes in fiscal regimes and tax credits materially affect project viability. Shifts in administration priorities can reallocate support between fossil-based and renewable chemistry, so monitoring policy continuity and subsidy durability is essential.

Trade tariffs and market access

PE, PP and PVC flows face tariffs, antidumping duties and quotas across the Americas, Europe and Asia, constraining Braskem’s export optionality and pricing. Trade remedies often protect local producers, reducing Braskem’s access to higher-margin markets. Regional frameworks such as Mercosur and USMCA-adjacent dynamics shape cross-border competitiveness. Proactive diversification of sales channels mitigates tariff shocks.

Energy and feedstock policy

Policies on natural gas (≈$7–8/MMBtu in 2024) and naphtha (≈$650/t CFR Asia in 2024) plus fuel taxation materially change cracker margins and feedstock competitiveness for Braskem. Subsidies or price caps can distort input costs versus global peers, shifting economics by double-digit percentage points. Alignment with Brazil’s energy transition policies may unlock incentives for electrification and low-carbon hydrogen, while long-term contracts tied to policy-stable benchmarks reduce price volatility.

Geopolitical risk and sanctions

Geopolitical conflicts and sanctions since 2022 have disrupted crude/NGL flows, altered shipping routes and increased insurance and bunker costs—Brent averaged about 86 USD/bbl in 2024, squeezing feedstock economics and pressuring ethylene/propylene margins and resin arbitrage across Atlantic and Pacific trades.

- Diversified sourcing: US ethane + Brazilian naphtha hedges

- Risk screening: sanctions monitoring across supplier base

- Mitigants: logistics hedges, inventory buffers to reduce exposure

Infrastructure and permitting

Permitting timelines for crackers, pipelines and terminals vary by jurisdiction, commonly spanning several months to multiple years, and have been decisive for Braskem’s project schedules in Brazil and the US Gulf Coast. Political pressure, especially around sensitive communities, can accelerate or stall expansions through local vetoes or federal interventions. Public-private partnerships and early stakeholder engagement have proven effective in smoothing approvals and unlocking access to port and rail upgrades.

- Permitting timelines: months to years

- Political risk: community opposition can halt projects

- Mitigation: PPPs and early engagement

Political and energy policy risks reshape petrochemical CAPEX, feedstock costs and export access

Political risks—industrial policy, BNDES financing and tax incentives—drive Braskem’s CAPEX and site choices; energy policies shift feedstock economics (nat gas $7–8/MMBtu 2024; naphtha ~$650/t CFR Asia 2024; Brent ~$86/bbl 2024). Trade remedies and tariffs constrain exports; permitting delays and local opposition add schedule risk.

| Item | 2024 |

|---|---|

| Brent | $86/bbl |

| Nat gas | $7–8/MMBtu |

| Naphtha | $650/t |

What is included in the product

Explores how macro-environmental factors uniquely affect Braskem across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven examples tied to Brazil, North America, and global feedstock markets. Designed for executives and investors, it highlights actionable risks and opportunities and includes forward-looking insights for scenario planning and regulatory strategy.

Condensed Braskem PESTLE highlights external risks and opportunities in plain language, making it easy to drop into presentations, share across teams, and guide strategic planning.

Economic factors

Commodity cycle and resin margins

PE (≈110 Mt/yr), PP (≈80 Mt/yr) and PVC (≈45 Mt/yr) pricing tracks global capacity cycles and end‑market demand in packaging, construction and autos; 2024 saw tighter supply after 2023 outages, lifting resin spreads. Downcycles compress spreads as new nameplate capacity comes online; upcycles expand margins when supply is tight. Braskem’s operating discipline and flexible utilization have preserved cash in troughs, and a balanced commodities‑to‑specialties mix cushions cyclicality.

Feedstock cost volatility

Feedstock cost volatility is driven by naphtha-linked versus ethane/propane-linked differentials that swing with oil-gas spreads; Brent averaged about 86.6 USD/bbl in 2024 while Henry Hub averaged ~3.66 USD/MMBtu (EIA 2024). Braskem’s competitiveness hinges on regional slate flexibility and contract structures that manage basis risk. Opportunistic switching and basis hedging are key value drivers, and integrating bio-ethanol routes creates an alternative cost curve from sugarcane feedstocks.

FX exposure and inflation

Braskem faces translation and transaction risk from revenues and costs in BRL, USD, MXN and EUR, with 2024 average USD/BRL near 5.0 amplifying FX volatility on reported results. Inflation pressures—IPCA ~3.9% (Brazil 2024), Mexico ~4.5%, US CPI ~3.4%, Eurozone ~2.4%—raise wages, utilities and maintenance capex. Matching debt currency to cash flows and applying price indexation and surcharges have materially defended margins and reduced balance-sheet stress.

Logistics and supply chain

Freight rate volatility and container availability materially affect Braskem export realizations; container freight rates fell over 60% from 2021 peaks by 2024 (Drewry), easing export costs but leaving margin sensitivity to short-term spikes. Rail and trucking reliability in Brazil constrain domestic delivery and slow inventory turns, increasing working-capital needs. Multi-hub shipping and near-customer warehouses reduce disruption risk, and digital logistics visibility cuts inventory days and improves cash conversion.

- Freight rates: >60% decline vs 2021 peaks (Drewry)

- Container availability/port congestion: direct impact on export timing

- Rail/truck reliability: raises domestic lead times and inventory days

- Multi-hub + near-customer warehouses: lower disruption risk

- Digital visibility: shortens inventory days, improves working capital

Capital intensity and interest rates

Cracker debottlenecks ($50–200m), advanced recycling units ($50–150m) and bio-based expansions ($200–500m) require substantial capex, so higher interest rates increase required hurdle returns and extend payback periods. Staged investments and JV structures reduce funding and execution risk, while access to green financing can lower project WACC by ~150–200 basis points.

- Capex ranges: debottleneck, recycling, bio-based

- Higher rates = longer payback

- Staged investments/JVs de-risk

- Green finance lowers WACC ~1.5–2.0pp

Political and energy policy risks reshape petrochemical CAPEX, feedstock costs and export access

Braskem’s margins track PE/PP/PVC cycles; 2024 supply tightening lifted spreads while flexible utilization and specialties mix cushion troughs. Competitiveness depends on feedstock slate (naphtha vs ethane) and FX exposures (USD/BRL ~5.0 in 2024) with inflation and freight volatility affecting working capital. Capex needs for recycling/bio raise hurdle rates; green finance can cut WACC ~150–200bp.

| Metric | 2024/2025 |

|---|---|

| Brent (avg 2024) | 86.6 USD/bbl |

| Henry Hub (avg 2024) | 3.66 USD/MMBtu |

| USD/BRL (avg 2024) | ~5.0 |

| Brazil IPCA 2024 | 3.9% |

| Freight change vs 2021 | >60% decline |

| Green finance WACC benefit | ~150–200 bp |

| Capex ranges | Debottleneck $50–200m; Recycling $50–150m; Bio $200–500m |

Preview Before You Purchase

Braskem PESTLE Analysis

The preview shown here is the exact Braskem PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with professional structure and no placeholders. The file visible here is the final version and will be available for immediate download after payment.

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, commodity cycles, and sustainability pressures are reshaping Braskem’s strategic outlook in our concise PESTLE snapshot. Use these insights to spot risks and growth levers for investors and strategists. Purchase the full PESTLE to get detailed, actionable analysis and editable templates for immediate use.

Political factors

Brazilian industrial policy and incentives

Brazilian industrial policy and incentives for petrochemicals and bio-based materials directly influence capital allocation and plant siting for Braskem, the largest petrochemical company in Latin America. BNDES, Brazil’s main development bank, remains a key source of long-term financing, while changes in fiscal regimes and tax credits materially affect project viability. Shifts in administration priorities can reallocate support between fossil-based and renewable chemistry, so monitoring policy continuity and subsidy durability is essential.

Trade tariffs and market access

PE, PP and PVC flows face tariffs, antidumping duties and quotas across the Americas, Europe and Asia, constraining Braskem’s export optionality and pricing. Trade remedies often protect local producers, reducing Braskem’s access to higher-margin markets. Regional frameworks such as Mercosur and USMCA-adjacent dynamics shape cross-border competitiveness. Proactive diversification of sales channels mitigates tariff shocks.

Energy and feedstock policy

Policies on natural gas (≈$7–8/MMBtu in 2024) and naphtha (≈$650/t CFR Asia in 2024) plus fuel taxation materially change cracker margins and feedstock competitiveness for Braskem. Subsidies or price caps can distort input costs versus global peers, shifting economics by double-digit percentage points. Alignment with Brazil’s energy transition policies may unlock incentives for electrification and low-carbon hydrogen, while long-term contracts tied to policy-stable benchmarks reduce price volatility.

Geopolitical risk and sanctions

Geopolitical conflicts and sanctions since 2022 have disrupted crude/NGL flows, altered shipping routes and increased insurance and bunker costs—Brent averaged about 86 USD/bbl in 2024, squeezing feedstock economics and pressuring ethylene/propylene margins and resin arbitrage across Atlantic and Pacific trades.

- Diversified sourcing: US ethane + Brazilian naphtha hedges

- Risk screening: sanctions monitoring across supplier base

- Mitigants: logistics hedges, inventory buffers to reduce exposure

Infrastructure and permitting

Permitting timelines for crackers, pipelines and terminals vary by jurisdiction, commonly spanning several months to multiple years, and have been decisive for Braskem’s project schedules in Brazil and the US Gulf Coast. Political pressure, especially around sensitive communities, can accelerate or stall expansions through local vetoes or federal interventions. Public-private partnerships and early stakeholder engagement have proven effective in smoothing approvals and unlocking access to port and rail upgrades.

- Permitting timelines: months to years

- Political risk: community opposition can halt projects

- Mitigation: PPPs and early engagement

Political and energy policy risks reshape petrochemical CAPEX, feedstock costs and export access

Political risks—industrial policy, BNDES financing and tax incentives—drive Braskem’s CAPEX and site choices; energy policies shift feedstock economics (nat gas $7–8/MMBtu 2024; naphtha ~$650/t CFR Asia 2024; Brent ~$86/bbl 2024). Trade remedies and tariffs constrain exports; permitting delays and local opposition add schedule risk.

| Item | 2024 |

|---|---|

| Brent | $86/bbl |

| Nat gas | $7–8/MMBtu |

| Naphtha | $650/t |

What is included in the product

Explores how macro-environmental factors uniquely affect Braskem across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven examples tied to Brazil, North America, and global feedstock markets. Designed for executives and investors, it highlights actionable risks and opportunities and includes forward-looking insights for scenario planning and regulatory strategy.

Condensed Braskem PESTLE highlights external risks and opportunities in plain language, making it easy to drop into presentations, share across teams, and guide strategic planning.

Economic factors

Commodity cycle and resin margins

PE (≈110 Mt/yr), PP (≈80 Mt/yr) and PVC (≈45 Mt/yr) pricing tracks global capacity cycles and end‑market demand in packaging, construction and autos; 2024 saw tighter supply after 2023 outages, lifting resin spreads. Downcycles compress spreads as new nameplate capacity comes online; upcycles expand margins when supply is tight. Braskem’s operating discipline and flexible utilization have preserved cash in troughs, and a balanced commodities‑to‑specialties mix cushions cyclicality.

Feedstock cost volatility

Feedstock cost volatility is driven by naphtha-linked versus ethane/propane-linked differentials that swing with oil-gas spreads; Brent averaged about 86.6 USD/bbl in 2024 while Henry Hub averaged ~3.66 USD/MMBtu (EIA 2024). Braskem’s competitiveness hinges on regional slate flexibility and contract structures that manage basis risk. Opportunistic switching and basis hedging are key value drivers, and integrating bio-ethanol routes creates an alternative cost curve from sugarcane feedstocks.

FX exposure and inflation

Braskem faces translation and transaction risk from revenues and costs in BRL, USD, MXN and EUR, with 2024 average USD/BRL near 5.0 amplifying FX volatility on reported results. Inflation pressures—IPCA ~3.9% (Brazil 2024), Mexico ~4.5%, US CPI ~3.4%, Eurozone ~2.4%—raise wages, utilities and maintenance capex. Matching debt currency to cash flows and applying price indexation and surcharges have materially defended margins and reduced balance-sheet stress.

Logistics and supply chain

Freight rate volatility and container availability materially affect Braskem export realizations; container freight rates fell over 60% from 2021 peaks by 2024 (Drewry), easing export costs but leaving margin sensitivity to short-term spikes. Rail and trucking reliability in Brazil constrain domestic delivery and slow inventory turns, increasing working-capital needs. Multi-hub shipping and near-customer warehouses reduce disruption risk, and digital logistics visibility cuts inventory days and improves cash conversion.

- Freight rates: >60% decline vs 2021 peaks (Drewry)

- Container availability/port congestion: direct impact on export timing

- Rail/truck reliability: raises domestic lead times and inventory days

- Multi-hub + near-customer warehouses: lower disruption risk

- Digital visibility: shortens inventory days, improves working capital

Capital intensity and interest rates

Cracker debottlenecks ($50–200m), advanced recycling units ($50–150m) and bio-based expansions ($200–500m) require substantial capex, so higher interest rates increase required hurdle returns and extend payback periods. Staged investments and JV structures reduce funding and execution risk, while access to green financing can lower project WACC by ~150–200 basis points.

- Capex ranges: debottleneck, recycling, bio-based

- Higher rates = longer payback

- Staged investments/JVs de-risk

- Green finance lowers WACC ~1.5–2.0pp

Political and energy policy risks reshape petrochemical CAPEX, feedstock costs and export access

Braskem’s margins track PE/PP/PVC cycles; 2024 supply tightening lifted spreads while flexible utilization and specialties mix cushion troughs. Competitiveness depends on feedstock slate (naphtha vs ethane) and FX exposures (USD/BRL ~5.0 in 2024) with inflation and freight volatility affecting working capital. Capex needs for recycling/bio raise hurdle rates; green finance can cut WACC ~150–200bp.

| Metric | 2024/2025 |

|---|---|

| Brent (avg 2024) | 86.6 USD/bbl |

| Henry Hub (avg 2024) | 3.66 USD/MMBtu |

| USD/BRL (avg 2024) | ~5.0 |

| Brazil IPCA 2024 | 3.9% |

| Freight change vs 2021 | >60% decline |

| Green finance WACC benefit | ~150–200 bp |

| Capex ranges | Debottleneck $50–200m; Recycling $50–150m; Bio $200–500m |

Preview Before You Purchase

Braskem PESTLE Analysis

The preview shown here is the exact Braskem PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with professional structure and no placeholders. The file visible here is the final version and will be available for immediate download after payment.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, commodity cycles, and sustainability pressures are reshaping Braskem’s strategic outlook in our concise PESTLE snapshot. Use these insights to spot risks and growth levers for investors and strategists. Purchase the full PESTLE to get detailed, actionable analysis and editable templates for immediate use.

Political factors

Brazilian industrial policy and incentives

Brazilian industrial policy and incentives for petrochemicals and bio-based materials directly influence capital allocation and plant siting for Braskem, the largest petrochemical company in Latin America. BNDES, Brazil’s main development bank, remains a key source of long-term financing, while changes in fiscal regimes and tax credits materially affect project viability. Shifts in administration priorities can reallocate support between fossil-based and renewable chemistry, so monitoring policy continuity and subsidy durability is essential.

Trade tariffs and market access

PE, PP and PVC flows face tariffs, antidumping duties and quotas across the Americas, Europe and Asia, constraining Braskem’s export optionality and pricing. Trade remedies often protect local producers, reducing Braskem’s access to higher-margin markets. Regional frameworks such as Mercosur and USMCA-adjacent dynamics shape cross-border competitiveness. Proactive diversification of sales channels mitigates tariff shocks.

Energy and feedstock policy

Policies on natural gas (≈$7–8/MMBtu in 2024) and naphtha (≈$650/t CFR Asia in 2024) plus fuel taxation materially change cracker margins and feedstock competitiveness for Braskem. Subsidies or price caps can distort input costs versus global peers, shifting economics by double-digit percentage points. Alignment with Brazil’s energy transition policies may unlock incentives for electrification and low-carbon hydrogen, while long-term contracts tied to policy-stable benchmarks reduce price volatility.

Geopolitical risk and sanctions

Geopolitical conflicts and sanctions since 2022 have disrupted crude/NGL flows, altered shipping routes and increased insurance and bunker costs—Brent averaged about 86 USD/bbl in 2024, squeezing feedstock economics and pressuring ethylene/propylene margins and resin arbitrage across Atlantic and Pacific trades.

- Diversified sourcing: US ethane + Brazilian naphtha hedges

- Risk screening: sanctions monitoring across supplier base

- Mitigants: logistics hedges, inventory buffers to reduce exposure

Infrastructure and permitting

Permitting timelines for crackers, pipelines and terminals vary by jurisdiction, commonly spanning several months to multiple years, and have been decisive for Braskem’s project schedules in Brazil and the US Gulf Coast. Political pressure, especially around sensitive communities, can accelerate or stall expansions through local vetoes or federal interventions. Public-private partnerships and early stakeholder engagement have proven effective in smoothing approvals and unlocking access to port and rail upgrades.

- Permitting timelines: months to years

- Political risk: community opposition can halt projects

- Mitigation: PPPs and early engagement

Political and energy policy risks reshape petrochemical CAPEX, feedstock costs and export access

Political risks—industrial policy, BNDES financing and tax incentives—drive Braskem’s CAPEX and site choices; energy policies shift feedstock economics (nat gas $7–8/MMBtu 2024; naphtha ~$650/t CFR Asia 2024; Brent ~$86/bbl 2024). Trade remedies and tariffs constrain exports; permitting delays and local opposition add schedule risk.

| Item | 2024 |

|---|---|

| Brent | $86/bbl |

| Nat gas | $7–8/MMBtu |

| Naphtha | $650/t |

What is included in the product

Explores how macro-environmental factors uniquely affect Braskem across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven examples tied to Brazil, North America, and global feedstock markets. Designed for executives and investors, it highlights actionable risks and opportunities and includes forward-looking insights for scenario planning and regulatory strategy.

Condensed Braskem PESTLE highlights external risks and opportunities in plain language, making it easy to drop into presentations, share across teams, and guide strategic planning.

Economic factors

Commodity cycle and resin margins

PE (≈110 Mt/yr), PP (≈80 Mt/yr) and PVC (≈45 Mt/yr) pricing tracks global capacity cycles and end‑market demand in packaging, construction and autos; 2024 saw tighter supply after 2023 outages, lifting resin spreads. Downcycles compress spreads as new nameplate capacity comes online; upcycles expand margins when supply is tight. Braskem’s operating discipline and flexible utilization have preserved cash in troughs, and a balanced commodities‑to‑specialties mix cushions cyclicality.

Feedstock cost volatility

Feedstock cost volatility is driven by naphtha-linked versus ethane/propane-linked differentials that swing with oil-gas spreads; Brent averaged about 86.6 USD/bbl in 2024 while Henry Hub averaged ~3.66 USD/MMBtu (EIA 2024). Braskem’s competitiveness hinges on regional slate flexibility and contract structures that manage basis risk. Opportunistic switching and basis hedging are key value drivers, and integrating bio-ethanol routes creates an alternative cost curve from sugarcane feedstocks.

FX exposure and inflation

Braskem faces translation and transaction risk from revenues and costs in BRL, USD, MXN and EUR, with 2024 average USD/BRL near 5.0 amplifying FX volatility on reported results. Inflation pressures—IPCA ~3.9% (Brazil 2024), Mexico ~4.5%, US CPI ~3.4%, Eurozone ~2.4%—raise wages, utilities and maintenance capex. Matching debt currency to cash flows and applying price indexation and surcharges have materially defended margins and reduced balance-sheet stress.

Logistics and supply chain

Freight rate volatility and container availability materially affect Braskem export realizations; container freight rates fell over 60% from 2021 peaks by 2024 (Drewry), easing export costs but leaving margin sensitivity to short-term spikes. Rail and trucking reliability in Brazil constrain domestic delivery and slow inventory turns, increasing working-capital needs. Multi-hub shipping and near-customer warehouses reduce disruption risk, and digital logistics visibility cuts inventory days and improves cash conversion.

- Freight rates: >60% decline vs 2021 peaks (Drewry)

- Container availability/port congestion: direct impact on export timing

- Rail/truck reliability: raises domestic lead times and inventory days

- Multi-hub + near-customer warehouses: lower disruption risk

- Digital visibility: shortens inventory days, improves working capital

Capital intensity and interest rates

Cracker debottlenecks ($50–200m), advanced recycling units ($50–150m) and bio-based expansions ($200–500m) require substantial capex, so higher interest rates increase required hurdle returns and extend payback periods. Staged investments and JV structures reduce funding and execution risk, while access to green financing can lower project WACC by ~150–200 basis points.

- Capex ranges: debottleneck, recycling, bio-based

- Higher rates = longer payback

- Staged investments/JVs de-risk

- Green finance lowers WACC ~1.5–2.0pp

Political and energy policy risks reshape petrochemical CAPEX, feedstock costs and export access

Braskem’s margins track PE/PP/PVC cycles; 2024 supply tightening lifted spreads while flexible utilization and specialties mix cushion troughs. Competitiveness depends on feedstock slate (naphtha vs ethane) and FX exposures (USD/BRL ~5.0 in 2024) with inflation and freight volatility affecting working capital. Capex needs for recycling/bio raise hurdle rates; green finance can cut WACC ~150–200bp.

| Metric | 2024/2025 |

|---|---|

| Brent (avg 2024) | 86.6 USD/bbl |

| Henry Hub (avg 2024) | 3.66 USD/MMBtu |

| USD/BRL (avg 2024) | ~5.0 |

| Brazil IPCA 2024 | 3.9% |

| Freight change vs 2021 | >60% decline |

| Green finance WACC benefit | ~150–200 bp |

| Capex ranges | Debottleneck $50–200m; Recycling $50–150m; Bio $200–500m |

Preview Before You Purchase

Braskem PESTLE Analysis

The preview shown here is the exact Braskem PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with professional structure and no placeholders. The file visible here is the final version and will be available for immediate download after payment.