Brighthouse Financial Business Model Canvas

Retirement insurer Business Model Canvas: revenue drivers, distribution, risk, growth

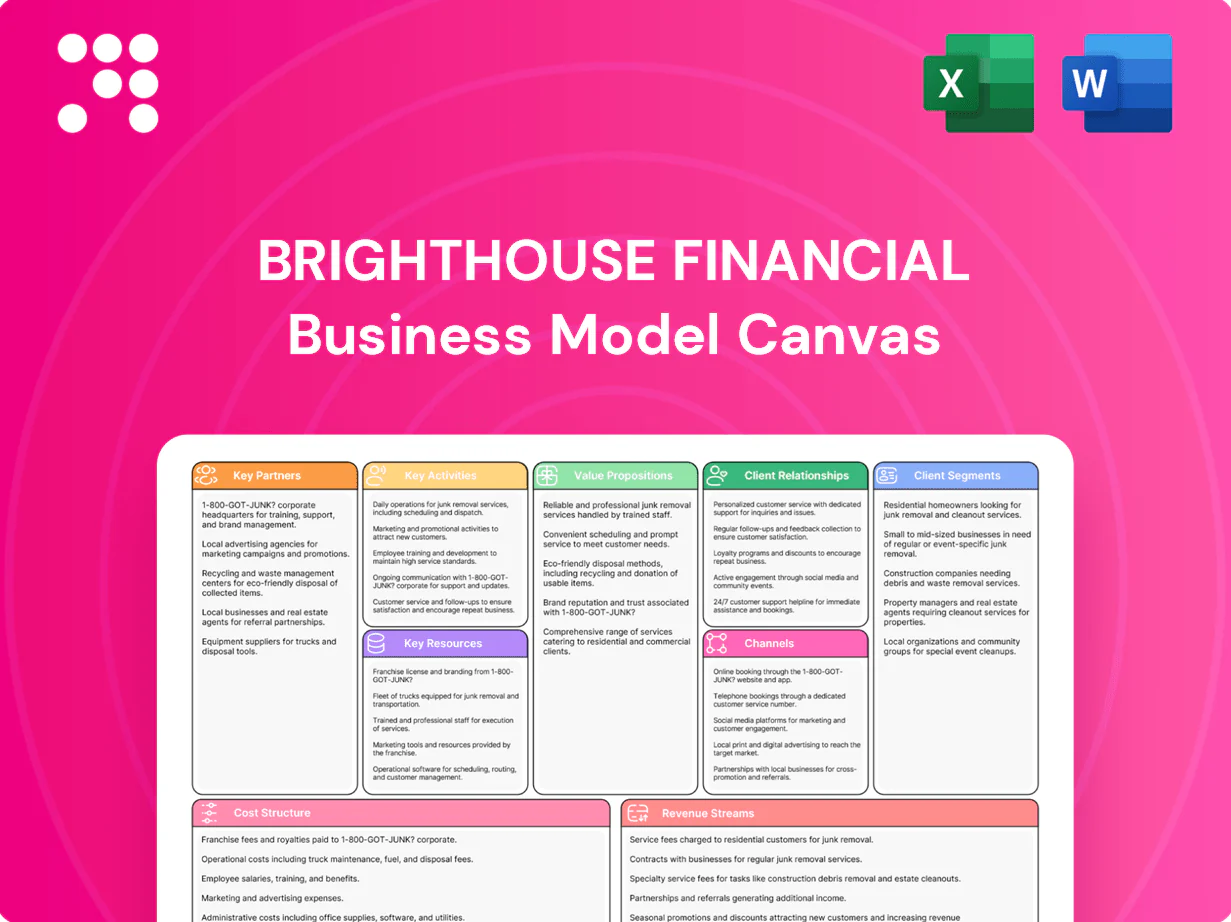

Explore Brighthouse Financial’s Business Model Canvas to understand how it aligns product design, distribution partners, and capital strategies to deliver retirement solutions. This concise yet insightful snapshot highlights revenue drivers, risk management, and growth levers. Download the full, editable canvas in Word/Excel for a detailed, section-by-section playbook to inform investment or strategic decisions.

Partnerships

Independent advisors and brokers

Brighthouse relies on independent financial advisors and broker-dealers to distribute annuities and life insurance, a channel that represented about 50% of U.S. annuity distribution in 2024. These partners provide client access and perform suitability assessments, ensuring products match needs. They explain complex features and riders to consumers, while strong wholesaling support and training sustain advisor engagement and retention.

Reinsurers

Reinsurers help Brighthouse manage longevity, mortality and market risks, transferring portions of blocks to stabilize earnings and capital; the global reinsurance market exceeded $320 billion in premiums in 2024, underpinning capacity for such transfers. Structured treaties provide capital relief and support new-product launches by reducing statutory reserve volatility and improving return-on-capital. Counterparty strength is critical for resilience, since reinsurer ratings drive regulatory capital recognition and counterparty credit exposure limits.

Asset managers and hedging banks

External asset managers run multi-asset portfolios backing Brighthouse liabilities, targeting efficient spreads and matching durations while supporting >90% of investable funds in separate account mandates.

Hedging banks provide derivatives and bespoke hedging programs for guarantees, leveraging an OTC derivatives market with notional outstanding around $610 trillion (BIS 2024) to transfer risk.

These partnerships optimize asset-liability management and spreads, and committed liquidity lines support stress scenarios and intraday needs.

Technology and insurtech vendors

Technology and insurtech vendors power Brighthouse Financials digital stack, enabling e-applications, automated underwriting, policy administration, and customer service while data and analytics partners sharpen pricing and risk models.

Cybersecurity partners secure sensitive customer data and regulatory compliance, and open APIs streamline advisor workflows to reduce friction and improve sales conversion.

- Digital platforms: e-apps, underwriting, policy admin, service

- Data & analytics: pricing and risk insights

- Cybersecurity: data protection & compliance

- APIs: advisor workflow automation

Distribution alliances with banks and IMOs

Distribution alliances with banks, wirehouses and insurance marketing organizations extend Brighthouse Financials reach into retail and institutional channels, leveraging shelf placement agreements to increase product visibility and prioritization. Joint marketing and advisor training programs drive product adoption while aligned compliance frameworks ensure suitability and regulatory oversight.

- Banks, wirehouses, IMOs: channel expansion

- Shelf placement: higher visibility

- Joint marketing/training: adoption

- Compliance alignment: suitable sales

Annuity ecosystem: advisors, reinsurers, hedging banks and asset managers share risk

Brighthouse depends on independent advisors and broker-dealers (≈50% of U.S. annuity distribution in 2024) for sales and suitability. Reinsurers (global premiums >$320B in 2024) and hedging banks (OTC notional ≈$610T, BIS 2024) transfer longevity, mortality and guarantee risk. External asset managers run >90% of investable funds in separate accounts to match liabilities.

| Partner | Role | 2024 metric |

|---|---|---|

| Advisors/Broker-dealers | Distribution/suitability | ~50% annuity channel |

| Reinsurers | Risk transfer/capital relief | Global premiums >$320B |

| Hedging banks | Derivatives/guarantee hedges | OTC notional ≈$610T |

| Asset managers | Liability-matching | >90% separate accounts |

What is included in the product

A concise, pre-written Business Model Canvas tailored to Brighthouse Financial’s strategy, covering customer segments, channels, value propositions, revenue streams, cost structure, key partners, activities, resources, and customer relationships with real-world insights. Designed for analysts and investors, it includes competitive advantages, SWOT-linked analysis, and a polished format for presentations and decision-making.

High-level, editable one-page snapshot of Brighthouse Financial’s business model to quickly identify core components, streamline boardroom discussions, save hours of formatting, and enable shareable team collaboration for fast deliverables and executive review.

Activities

Product design and pricing

Actuarial teams design Brighthouse variable and fixed annuities and life insurance products, calibrating fees, guarantees and riders to market conditions (2024 10-year Treasury ~4.0%) to balance profitability and competitiveness. Stress testing and scenario analysis (including low-rate and high-volatility paths) shape feature sets, while competitive benchmarking refines value and pricing relative to peers.

Risk and capital management

ALM and dynamic hedging programs mitigate equity, interest rate, and volatility exposures across the annuity and life portfolios, stabilizing surplus sensitivity. Capital allocation is governed by regulatory capital requirements and rating-agency metrics to preserve solvency and ratings. Strategic reinsurance transactions are used to optimize statutory and economic capital usage. Regular governance reviews and limits enforcement sustain discipline.

Distribution and wholesaling

Brighthouse educates advisors and supports sales with digital tools, training and field resources to drive annuity and life sales. Wholesalers provide case design and point-of-sale support to streamline recommendations and filings. Targeted marketing campaigns generate advisor and client interest while coordinated post-sale onboarding reduces friction and improves persistency.

Underwriting and policy administration

Efficient underwriting balances risk selection with speed, using automated rules and targeted manual review to protect margin while accelerating issue times. Policy issuance, billing, and servicing focus on accuracy and convenience to sustain persistency and reduce lapse-related strain on reserves. Claims handling is timely and empathetic, backed by data accuracy to ensure compliance and reliable reporting.

- Underwriting: automated + manual review

- Policy admin: issuance, billing, servicing

- Claims: prompt, empathetic handling

- Data: accuracy for compliance/reporting

Investment management

Investment management at Brighthouse targets risk-adjusted yield and liquidity across its roughly $112 billion invested asset base (2024), balancing spread income with market access.

Manager selection and oversight drive alpha, while hedging strategies are executed to match liability duration and convexity; ongoing monitoring recalibrates positions to 2024 macro shifts.

- Risk-adjusted yield focus

- Liquidity management

- Manager oversight

- Liability-aligned hedging

- Active macro monitoring (2024)

ALM, hedging and capital optimize annuity economics as rates settle near ~4.0%

Actuarial design, ALM/hedging and capital management calibrate annuity and life product economics to 2024 market conditions (10‑yr Treasury ~4.0%) while stress testing and reinsurance optimize capital. Distribution support, digital sales tools and underwriting automation drive issuance and persistency. Investment management oversees roughly $112 billion invested assets (2024) with liability‑aligned hedging.

| Metric | 2024 Value |

|---|---|

| Invested assets | $112 billion |

| 10‑yr Treasury | ~4.0% |

Full Document Unlocks After Purchase

Business Model Canvas

This preview is the actual Brighthouse Financial Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this same complete document with all sections included. The file is delivered ready-to-edit in Word and Excel. No surprises—what you see is the exact deliverable.

Retirement insurer Business Model Canvas: revenue drivers, distribution, risk, growth

Explore Brighthouse Financial’s Business Model Canvas to understand how it aligns product design, distribution partners, and capital strategies to deliver retirement solutions. This concise yet insightful snapshot highlights revenue drivers, risk management, and growth levers. Download the full, editable canvas in Word/Excel for a detailed, section-by-section playbook to inform investment or strategic decisions.

Partnerships

Independent advisors and brokers

Brighthouse relies on independent financial advisors and broker-dealers to distribute annuities and life insurance, a channel that represented about 50% of U.S. annuity distribution in 2024. These partners provide client access and perform suitability assessments, ensuring products match needs. They explain complex features and riders to consumers, while strong wholesaling support and training sustain advisor engagement and retention.

Reinsurers

Reinsurers help Brighthouse manage longevity, mortality and market risks, transferring portions of blocks to stabilize earnings and capital; the global reinsurance market exceeded $320 billion in premiums in 2024, underpinning capacity for such transfers. Structured treaties provide capital relief and support new-product launches by reducing statutory reserve volatility and improving return-on-capital. Counterparty strength is critical for resilience, since reinsurer ratings drive regulatory capital recognition and counterparty credit exposure limits.

Asset managers and hedging banks

External asset managers run multi-asset portfolios backing Brighthouse liabilities, targeting efficient spreads and matching durations while supporting >90% of investable funds in separate account mandates.

Hedging banks provide derivatives and bespoke hedging programs for guarantees, leveraging an OTC derivatives market with notional outstanding around $610 trillion (BIS 2024) to transfer risk.

These partnerships optimize asset-liability management and spreads, and committed liquidity lines support stress scenarios and intraday needs.

Technology and insurtech vendors

Technology and insurtech vendors power Brighthouse Financials digital stack, enabling e-applications, automated underwriting, policy administration, and customer service while data and analytics partners sharpen pricing and risk models.

Cybersecurity partners secure sensitive customer data and regulatory compliance, and open APIs streamline advisor workflows to reduce friction and improve sales conversion.

- Digital platforms: e-apps, underwriting, policy admin, service

- Data & analytics: pricing and risk insights

- Cybersecurity: data protection & compliance

- APIs: advisor workflow automation

Distribution alliances with banks and IMOs

Distribution alliances with banks, wirehouses and insurance marketing organizations extend Brighthouse Financials reach into retail and institutional channels, leveraging shelf placement agreements to increase product visibility and prioritization. Joint marketing and advisor training programs drive product adoption while aligned compliance frameworks ensure suitability and regulatory oversight.

- Banks, wirehouses, IMOs: channel expansion

- Shelf placement: higher visibility

- Joint marketing/training: adoption

- Compliance alignment: suitable sales

Annuity ecosystem: advisors, reinsurers, hedging banks and asset managers share risk

Brighthouse depends on independent advisors and broker-dealers (≈50% of U.S. annuity distribution in 2024) for sales and suitability. Reinsurers (global premiums >$320B in 2024) and hedging banks (OTC notional ≈$610T, BIS 2024) transfer longevity, mortality and guarantee risk. External asset managers run >90% of investable funds in separate accounts to match liabilities.

| Partner | Role | 2024 metric |

|---|---|---|

| Advisors/Broker-dealers | Distribution/suitability | ~50% annuity channel |

| Reinsurers | Risk transfer/capital relief | Global premiums >$320B |

| Hedging banks | Derivatives/guarantee hedges | OTC notional ≈$610T |

| Asset managers | Liability-matching | >90% separate accounts |

What is included in the product

A concise, pre-written Business Model Canvas tailored to Brighthouse Financial’s strategy, covering customer segments, channels, value propositions, revenue streams, cost structure, key partners, activities, resources, and customer relationships with real-world insights. Designed for analysts and investors, it includes competitive advantages, SWOT-linked analysis, and a polished format for presentations and decision-making.

High-level, editable one-page snapshot of Brighthouse Financial’s business model to quickly identify core components, streamline boardroom discussions, save hours of formatting, and enable shareable team collaboration for fast deliverables and executive review.

Activities

Product design and pricing

Actuarial teams design Brighthouse variable and fixed annuities and life insurance products, calibrating fees, guarantees and riders to market conditions (2024 10-year Treasury ~4.0%) to balance profitability and competitiveness. Stress testing and scenario analysis (including low-rate and high-volatility paths) shape feature sets, while competitive benchmarking refines value and pricing relative to peers.

Risk and capital management

ALM and dynamic hedging programs mitigate equity, interest rate, and volatility exposures across the annuity and life portfolios, stabilizing surplus sensitivity. Capital allocation is governed by regulatory capital requirements and rating-agency metrics to preserve solvency and ratings. Strategic reinsurance transactions are used to optimize statutory and economic capital usage. Regular governance reviews and limits enforcement sustain discipline.

Distribution and wholesaling

Brighthouse educates advisors and supports sales with digital tools, training and field resources to drive annuity and life sales. Wholesalers provide case design and point-of-sale support to streamline recommendations and filings. Targeted marketing campaigns generate advisor and client interest while coordinated post-sale onboarding reduces friction and improves persistency.

Underwriting and policy administration

Efficient underwriting balances risk selection with speed, using automated rules and targeted manual review to protect margin while accelerating issue times. Policy issuance, billing, and servicing focus on accuracy and convenience to sustain persistency and reduce lapse-related strain on reserves. Claims handling is timely and empathetic, backed by data accuracy to ensure compliance and reliable reporting.

- Underwriting: automated + manual review

- Policy admin: issuance, billing, servicing

- Claims: prompt, empathetic handling

- Data: accuracy for compliance/reporting

Investment management

Investment management at Brighthouse targets risk-adjusted yield and liquidity across its roughly $112 billion invested asset base (2024), balancing spread income with market access.

Manager selection and oversight drive alpha, while hedging strategies are executed to match liability duration and convexity; ongoing monitoring recalibrates positions to 2024 macro shifts.

- Risk-adjusted yield focus

- Liquidity management

- Manager oversight

- Liability-aligned hedging

- Active macro monitoring (2024)

ALM, hedging and capital optimize annuity economics as rates settle near ~4.0%

Actuarial design, ALM/hedging and capital management calibrate annuity and life product economics to 2024 market conditions (10‑yr Treasury ~4.0%) while stress testing and reinsurance optimize capital. Distribution support, digital sales tools and underwriting automation drive issuance and persistency. Investment management oversees roughly $112 billion invested assets (2024) with liability‑aligned hedging.

| Metric | 2024 Value |

|---|---|

| Invested assets | $112 billion |

| 10‑yr Treasury | ~4.0% |

Full Document Unlocks After Purchase

Business Model Canvas

This preview is the actual Brighthouse Financial Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this same complete document with all sections included. The file is delivered ready-to-edit in Word and Excel. No surprises—what you see is the exact deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Retirement insurer Business Model Canvas: revenue drivers, distribution, risk, growth

Explore Brighthouse Financial’s Business Model Canvas to understand how it aligns product design, distribution partners, and capital strategies to deliver retirement solutions. This concise yet insightful snapshot highlights revenue drivers, risk management, and growth levers. Download the full, editable canvas in Word/Excel for a detailed, section-by-section playbook to inform investment or strategic decisions.

Partnerships

Independent advisors and brokers

Brighthouse relies on independent financial advisors and broker-dealers to distribute annuities and life insurance, a channel that represented about 50% of U.S. annuity distribution in 2024. These partners provide client access and perform suitability assessments, ensuring products match needs. They explain complex features and riders to consumers, while strong wholesaling support and training sustain advisor engagement and retention.

Reinsurers

Reinsurers help Brighthouse manage longevity, mortality and market risks, transferring portions of blocks to stabilize earnings and capital; the global reinsurance market exceeded $320 billion in premiums in 2024, underpinning capacity for such transfers. Structured treaties provide capital relief and support new-product launches by reducing statutory reserve volatility and improving return-on-capital. Counterparty strength is critical for resilience, since reinsurer ratings drive regulatory capital recognition and counterparty credit exposure limits.

Asset managers and hedging banks

External asset managers run multi-asset portfolios backing Brighthouse liabilities, targeting efficient spreads and matching durations while supporting >90% of investable funds in separate account mandates.

Hedging banks provide derivatives and bespoke hedging programs for guarantees, leveraging an OTC derivatives market with notional outstanding around $610 trillion (BIS 2024) to transfer risk.

These partnerships optimize asset-liability management and spreads, and committed liquidity lines support stress scenarios and intraday needs.

Technology and insurtech vendors

Technology and insurtech vendors power Brighthouse Financials digital stack, enabling e-applications, automated underwriting, policy administration, and customer service while data and analytics partners sharpen pricing and risk models.

Cybersecurity partners secure sensitive customer data and regulatory compliance, and open APIs streamline advisor workflows to reduce friction and improve sales conversion.

- Digital platforms: e-apps, underwriting, policy admin, service

- Data & analytics: pricing and risk insights

- Cybersecurity: data protection & compliance

- APIs: advisor workflow automation

Distribution alliances with banks and IMOs

Distribution alliances with banks, wirehouses and insurance marketing organizations extend Brighthouse Financials reach into retail and institutional channels, leveraging shelf placement agreements to increase product visibility and prioritization. Joint marketing and advisor training programs drive product adoption while aligned compliance frameworks ensure suitability and regulatory oversight.

- Banks, wirehouses, IMOs: channel expansion

- Shelf placement: higher visibility

- Joint marketing/training: adoption

- Compliance alignment: suitable sales

Annuity ecosystem: advisors, reinsurers, hedging banks and asset managers share risk

Brighthouse depends on independent advisors and broker-dealers (≈50% of U.S. annuity distribution in 2024) for sales and suitability. Reinsurers (global premiums >$320B in 2024) and hedging banks (OTC notional ≈$610T, BIS 2024) transfer longevity, mortality and guarantee risk. External asset managers run >90% of investable funds in separate accounts to match liabilities.

| Partner | Role | 2024 metric |

|---|---|---|

| Advisors/Broker-dealers | Distribution/suitability | ~50% annuity channel |

| Reinsurers | Risk transfer/capital relief | Global premiums >$320B |

| Hedging banks | Derivatives/guarantee hedges | OTC notional ≈$610T |

| Asset managers | Liability-matching | >90% separate accounts |

What is included in the product

A concise, pre-written Business Model Canvas tailored to Brighthouse Financial’s strategy, covering customer segments, channels, value propositions, revenue streams, cost structure, key partners, activities, resources, and customer relationships with real-world insights. Designed for analysts and investors, it includes competitive advantages, SWOT-linked analysis, and a polished format for presentations and decision-making.

High-level, editable one-page snapshot of Brighthouse Financial’s business model to quickly identify core components, streamline boardroom discussions, save hours of formatting, and enable shareable team collaboration for fast deliverables and executive review.

Activities

Product design and pricing

Actuarial teams design Brighthouse variable and fixed annuities and life insurance products, calibrating fees, guarantees and riders to market conditions (2024 10-year Treasury ~4.0%) to balance profitability and competitiveness. Stress testing and scenario analysis (including low-rate and high-volatility paths) shape feature sets, while competitive benchmarking refines value and pricing relative to peers.

Risk and capital management

ALM and dynamic hedging programs mitigate equity, interest rate, and volatility exposures across the annuity and life portfolios, stabilizing surplus sensitivity. Capital allocation is governed by regulatory capital requirements and rating-agency metrics to preserve solvency and ratings. Strategic reinsurance transactions are used to optimize statutory and economic capital usage. Regular governance reviews and limits enforcement sustain discipline.

Distribution and wholesaling

Brighthouse educates advisors and supports sales with digital tools, training and field resources to drive annuity and life sales. Wholesalers provide case design and point-of-sale support to streamline recommendations and filings. Targeted marketing campaigns generate advisor and client interest while coordinated post-sale onboarding reduces friction and improves persistency.

Underwriting and policy administration

Efficient underwriting balances risk selection with speed, using automated rules and targeted manual review to protect margin while accelerating issue times. Policy issuance, billing, and servicing focus on accuracy and convenience to sustain persistency and reduce lapse-related strain on reserves. Claims handling is timely and empathetic, backed by data accuracy to ensure compliance and reliable reporting.

- Underwriting: automated + manual review

- Policy admin: issuance, billing, servicing

- Claims: prompt, empathetic handling

- Data: accuracy for compliance/reporting

Investment management

Investment management at Brighthouse targets risk-adjusted yield and liquidity across its roughly $112 billion invested asset base (2024), balancing spread income with market access.

Manager selection and oversight drive alpha, while hedging strategies are executed to match liability duration and convexity; ongoing monitoring recalibrates positions to 2024 macro shifts.

- Risk-adjusted yield focus

- Liquidity management

- Manager oversight

- Liability-aligned hedging

- Active macro monitoring (2024)

ALM, hedging and capital optimize annuity economics as rates settle near ~4.0%

Actuarial design, ALM/hedging and capital management calibrate annuity and life product economics to 2024 market conditions (10‑yr Treasury ~4.0%) while stress testing and reinsurance optimize capital. Distribution support, digital sales tools and underwriting automation drive issuance and persistency. Investment management oversees roughly $112 billion invested assets (2024) with liability‑aligned hedging.

| Metric | 2024 Value |

|---|---|

| Invested assets | $112 billion |

| 10‑yr Treasury | ~4.0% |

Full Document Unlocks After Purchase

Business Model Canvas

This preview is the actual Brighthouse Financial Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this same complete document with all sections included. The file is delivered ready-to-edit in Word and Excel. No surprises—what you see is the exact deliverable.