Brookline Bank Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

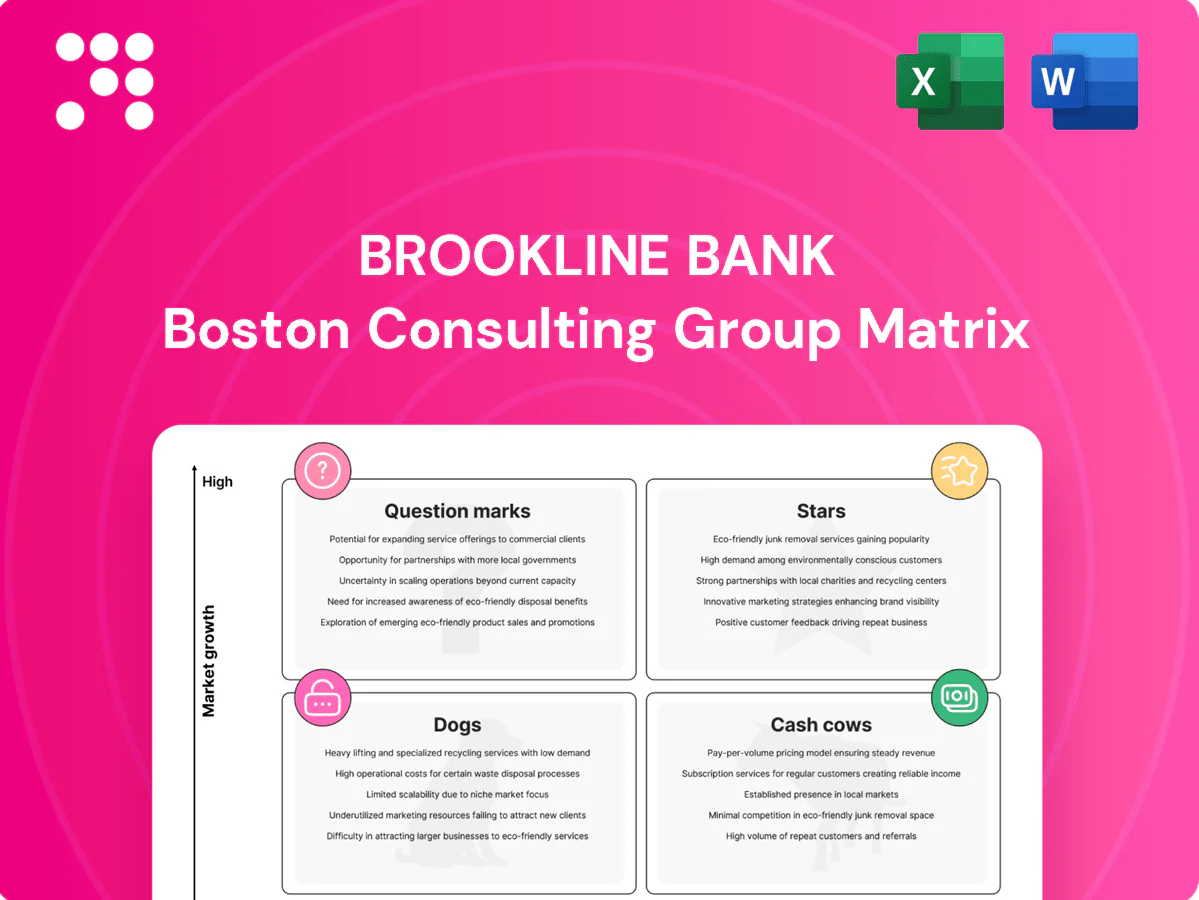

Curious where Brookline Bank’s products land—Stars, Cash Cows, Dogs or Question Marks? This preview scratches the surface; buy the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and tactical moves you can act on now. You’ll get a polished Word report plus an Excel summary, ready to present and use—skip the guesswork and make sharper investment and product decisions today.

Stars

Boston business cash management

High-growth adoption and deep local penetration position Brookline Bank’s treasury/cash management as a Boston business cash management leader: Greater Boston metro (~4.9M people) continues scaling tech and life‑science firms, driving urgent demand for payables, receivables, and liquidity tools. The channel brings sticky deposits and fee income but requires continued investment in API integrations and expanded sales coverage; prioritize funding to cement share and capture market growth.

Digital banking & mobile experience

Mobile usage keeps climbing—US mobile banking penetration reached about 73% in 2024, and Brookline’s app is table stakes plus, driving high engagement and retention. The product requires ongoing cash for upgrades, security, and UX polish, pressuring margins in the short term. Payoff is large if Brookline holds share as the market swells; continue shipping features and tightening uptime to protect growth.

Middle-market C&I lending

Middle-market C&I lending leverages Brookline Bank’s deep Boston-area operator relationships to capture real share in a growing regional economy; pipelines remain healthy across services, healthcare, and tech-adjacent firms. Capital intensity means underwriting discipline and pricing power are critical to protect margins and credit quality. Keep originations selective and focus on deepening cross-sell to expand fee income and client stickiness.

Commercial real estate banking (select segments)

Well-positioned sponsors in resilient asset classes (industrial, medical, mixed-use) still grow; US industrial vacancy remained near historic lows (~4% in 2024) supporting rent growth and lending. Brookline’s local knowledge is a moat, but continuous spend on monitoring and portfolio analytics is required. As markets normalize, leaders become durable cash engines—invest in data and keep top borrowers close.

- Moat: local market expertise

- 2024: industrial vacancy ~4%

- Priority: invest in analytics

- Strategy: retain best borrowers

Integrated SMB packages (checking + payments)

Bundled checking + payments for SMBs are high-growth Stars for Brookline Bank: industry 2024 data shows merchant-services attach rates above 50% with strong retention, driving recurring fees despite higher onboarding/support spend; local market share looks solid—keep pricing tight and onboarding friction-free to sustain adoption and lifetime value.

- High attach

- High stickiness

- Ongoing onboarding cost

- Maintain sharp bundle

Boston opportunity: 4.9M metro, 73% mobile users, >50% merchant attach—fund APIs, UX, analytics.

Brookline’s Stars—treasury/cash management, mobile banking, SMB bundled checking+payments and selective middle‑market C&I—benefit from Greater Boston ~4.9M population, US mobile banking penetration ~73% (2024), industrial vacancy ~4% (2024) and merchant‑services attach >50% (2024); prioritize funding for APIs, UX, analytics and selective originations to capture growth and lock deposits/fees.

| Product | 2024 metric | Priority | Action |

|---|---|---|---|

| Treasury | Boston metro 4.9M | Invest | API integrations |

| Mobile | 73% penetration | Upgrade | UX/security |

| SMB bundle | Attach >50% | Scale | Reduce onboarding friction |

| C&I | Healthy pipelines | Selective | Underwrite tightly |

What is included in the product

Brookline Bank BCG Matrix: strategic review of units with invest/hold/divest guidance for Stars, Cash Cows, Question Marks and Dogs, plus trend risks.

One-page BCG Matrix placing Brookline Bank units in quadrants for quick C-level decisions and slide-ready exports.

Cash Cows

Core consumer deposits

Core consumer deposits remain a mature, high-share cash cow in Brookline Bank’s legacy neighborhoods, providing the low-cost funding that underpinned the bank’s stability through 2024. Promotion needs are modest now; priorities are retention and targeted fee optimization to extract revenue without acquisition spend. Small operational efficiencies and automation can lift net interest margin incrementally; milk gently to avoid spooking loyal customers.

Mortgage servicing & escrow

Existing serviced book produces steady fee income even when originations slow; industry servicing fees average ~25 basis points (0.25% annually) in 2024, supporting predictable revenue. Operations are stable and scalable with minor tech tweaks—workflow automation can cut servicing costs and attrition. Low growth, high predictability — classic cash cow. Maintain service levels and control leakage to protect margins.

Small business checking

Small business checking sits as a cash cow for Brookline Bank with an established base and predictable balances supporting dependable fee income; Brookline Bancorp reported total deposits of about $8.6 billion as of mid‑2024, highlighting scale. Growth is slow but churn stays low when service quality is high, reducing acquisition spend. Minimal marketing beyond periodic refreshes is required; optimize pricing and digital self‑service to widen the spread.

Branch-based consumer banking (core markets)

Branch-based consumer banking in Brookline Bank acts as a cash cow: entrenched presence in long-held neighborhoods keeps deposits sticky and churn low, while foot traffic is largely flat but relationship depth per customer remains high, supporting fee income and core deposit stability. Limited incremental capex preserves healthy return on tangible equity, and the physical footprint is prioritized for advisory and cross-sell rather than raw account acquisition.

- Deposit stickiness: neighborhood anchoring

- Traffic: flat; relationships: deep

- Capex: constrained to protect ROE

- Use: advisory/cross-sell over acquisition

ACH & wires for existing clients

ACH and wires for existing Brookline clients are habitual and recurring, with volumes steady; the US ACH network processed about 31 billion transactions in 2024, underscoring reliability. Margins are solid with modest compliance and platform costs, making the product highly bankable rather than a growth rocket. Keep reliability top-notch and nudge incremental volume.

- Steady habitual usage

- 31B US ACH txns in 2024

- Solid margins; modest compliance/platform costs

- Focus: reliability + incremental volume

Core deposits and SME checking deliver low-cost balance-sheet stability; prioritize ACH reliability

Core consumer deposits, small business checking, servicing fees and payments are stable cash cows for Brookline Bank, funding low-cost balance-sheet stability through 2024. Retention, fee optimization and modest automation lift margins without acquisition spend. Preserve branch footprint for cross-sell; prioritize reliability for ACH/wires.

| Metric | 2024 |

|---|---|

| Total deposits | $8.6B |

| Servicing fee | ~25 bps |

| US ACH volume | 31B txns |

What You See Is What You Get

Brookline Bank BCG Matrix

The Brookline Bank BCG Matrix you’re previewing is the exact file you’ll receive after purchase — no watermarks, no demo slides, just the finished report. It’s fully formatted and tailored for Brookline Bank with clear, market-backed insights to inform strategic decisions. After purchase the ready-to-use document is delivered immediately to your inbox for editing, printing, or presenting. One payment, no surprises — plug it straight into your planning.

Visual. Strategic. Downloadable.

Curious where Brookline Bank’s products land—Stars, Cash Cows, Dogs or Question Marks? This preview scratches the surface; buy the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and tactical moves you can act on now. You’ll get a polished Word report plus an Excel summary, ready to present and use—skip the guesswork and make sharper investment and product decisions today.

Stars

Boston business cash management

High-growth adoption and deep local penetration position Brookline Bank’s treasury/cash management as a Boston business cash management leader: Greater Boston metro (~4.9M people) continues scaling tech and life‑science firms, driving urgent demand for payables, receivables, and liquidity tools. The channel brings sticky deposits and fee income but requires continued investment in API integrations and expanded sales coverage; prioritize funding to cement share and capture market growth.

Digital banking & mobile experience

Mobile usage keeps climbing—US mobile banking penetration reached about 73% in 2024, and Brookline’s app is table stakes plus, driving high engagement and retention. The product requires ongoing cash for upgrades, security, and UX polish, pressuring margins in the short term. Payoff is large if Brookline holds share as the market swells; continue shipping features and tightening uptime to protect growth.

Middle-market C&I lending

Middle-market C&I lending leverages Brookline Bank’s deep Boston-area operator relationships to capture real share in a growing regional economy; pipelines remain healthy across services, healthcare, and tech-adjacent firms. Capital intensity means underwriting discipline and pricing power are critical to protect margins and credit quality. Keep originations selective and focus on deepening cross-sell to expand fee income and client stickiness.

Commercial real estate banking (select segments)

Well-positioned sponsors in resilient asset classes (industrial, medical, mixed-use) still grow; US industrial vacancy remained near historic lows (~4% in 2024) supporting rent growth and lending. Brookline’s local knowledge is a moat, but continuous spend on monitoring and portfolio analytics is required. As markets normalize, leaders become durable cash engines—invest in data and keep top borrowers close.

- Moat: local market expertise

- 2024: industrial vacancy ~4%

- Priority: invest in analytics

- Strategy: retain best borrowers

Integrated SMB packages (checking + payments)

Bundled checking + payments for SMBs are high-growth Stars for Brookline Bank: industry 2024 data shows merchant-services attach rates above 50% with strong retention, driving recurring fees despite higher onboarding/support spend; local market share looks solid—keep pricing tight and onboarding friction-free to sustain adoption and lifetime value.

- High attach

- High stickiness

- Ongoing onboarding cost

- Maintain sharp bundle

Boston opportunity: 4.9M metro, 73% mobile users, >50% merchant attach—fund APIs, UX, analytics.

Brookline’s Stars—treasury/cash management, mobile banking, SMB bundled checking+payments and selective middle‑market C&I—benefit from Greater Boston ~4.9M population, US mobile banking penetration ~73% (2024), industrial vacancy ~4% (2024) and merchant‑services attach >50% (2024); prioritize funding for APIs, UX, analytics and selective originations to capture growth and lock deposits/fees.

| Product | 2024 metric | Priority | Action |

|---|---|---|---|

| Treasury | Boston metro 4.9M | Invest | API integrations |

| Mobile | 73% penetration | Upgrade | UX/security |

| SMB bundle | Attach >50% | Scale | Reduce onboarding friction |

| C&I | Healthy pipelines | Selective | Underwrite tightly |

What is included in the product

Brookline Bank BCG Matrix: strategic review of units with invest/hold/divest guidance for Stars, Cash Cows, Question Marks and Dogs, plus trend risks.

One-page BCG Matrix placing Brookline Bank units in quadrants for quick C-level decisions and slide-ready exports.

Cash Cows

Core consumer deposits

Core consumer deposits remain a mature, high-share cash cow in Brookline Bank’s legacy neighborhoods, providing the low-cost funding that underpinned the bank’s stability through 2024. Promotion needs are modest now; priorities are retention and targeted fee optimization to extract revenue without acquisition spend. Small operational efficiencies and automation can lift net interest margin incrementally; milk gently to avoid spooking loyal customers.

Mortgage servicing & escrow

Existing serviced book produces steady fee income even when originations slow; industry servicing fees average ~25 basis points (0.25% annually) in 2024, supporting predictable revenue. Operations are stable and scalable with minor tech tweaks—workflow automation can cut servicing costs and attrition. Low growth, high predictability — classic cash cow. Maintain service levels and control leakage to protect margins.

Small business checking

Small business checking sits as a cash cow for Brookline Bank with an established base and predictable balances supporting dependable fee income; Brookline Bancorp reported total deposits of about $8.6 billion as of mid‑2024, highlighting scale. Growth is slow but churn stays low when service quality is high, reducing acquisition spend. Minimal marketing beyond periodic refreshes is required; optimize pricing and digital self‑service to widen the spread.

Branch-based consumer banking (core markets)

Branch-based consumer banking in Brookline Bank acts as a cash cow: entrenched presence in long-held neighborhoods keeps deposits sticky and churn low, while foot traffic is largely flat but relationship depth per customer remains high, supporting fee income and core deposit stability. Limited incremental capex preserves healthy return on tangible equity, and the physical footprint is prioritized for advisory and cross-sell rather than raw account acquisition.

- Deposit stickiness: neighborhood anchoring

- Traffic: flat; relationships: deep

- Capex: constrained to protect ROE

- Use: advisory/cross-sell over acquisition

ACH & wires for existing clients

ACH and wires for existing Brookline clients are habitual and recurring, with volumes steady; the US ACH network processed about 31 billion transactions in 2024, underscoring reliability. Margins are solid with modest compliance and platform costs, making the product highly bankable rather than a growth rocket. Keep reliability top-notch and nudge incremental volume.

- Steady habitual usage

- 31B US ACH txns in 2024

- Solid margins; modest compliance/platform costs

- Focus: reliability + incremental volume

Core deposits and SME checking deliver low-cost balance-sheet stability; prioritize ACH reliability

Core consumer deposits, small business checking, servicing fees and payments are stable cash cows for Brookline Bank, funding low-cost balance-sheet stability through 2024. Retention, fee optimization and modest automation lift margins without acquisition spend. Preserve branch footprint for cross-sell; prioritize reliability for ACH/wires.

| Metric | 2024 |

|---|---|

| Total deposits | $8.6B |

| Servicing fee | ~25 bps |

| US ACH volume | 31B txns |

What You See Is What You Get

Brookline Bank BCG Matrix

The Brookline Bank BCG Matrix you’re previewing is the exact file you’ll receive after purchase — no watermarks, no demo slides, just the finished report. It’s fully formatted and tailored for Brookline Bank with clear, market-backed insights to inform strategic decisions. After purchase the ready-to-use document is delivered immediately to your inbox for editing, printing, or presenting. One payment, no surprises — plug it straight into your planning.

Description

Visual. Strategic. Downloadable.

Curious where Brookline Bank’s products land—Stars, Cash Cows, Dogs or Question Marks? This preview scratches the surface; buy the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and tactical moves you can act on now. You’ll get a polished Word report plus an Excel summary, ready to present and use—skip the guesswork and make sharper investment and product decisions today.

Stars

Boston business cash management

High-growth adoption and deep local penetration position Brookline Bank’s treasury/cash management as a Boston business cash management leader: Greater Boston metro (~4.9M people) continues scaling tech and life‑science firms, driving urgent demand for payables, receivables, and liquidity tools. The channel brings sticky deposits and fee income but requires continued investment in API integrations and expanded sales coverage; prioritize funding to cement share and capture market growth.

Digital banking & mobile experience

Mobile usage keeps climbing—US mobile banking penetration reached about 73% in 2024, and Brookline’s app is table stakes plus, driving high engagement and retention. The product requires ongoing cash for upgrades, security, and UX polish, pressuring margins in the short term. Payoff is large if Brookline holds share as the market swells; continue shipping features and tightening uptime to protect growth.

Middle-market C&I lending

Middle-market C&I lending leverages Brookline Bank’s deep Boston-area operator relationships to capture real share in a growing regional economy; pipelines remain healthy across services, healthcare, and tech-adjacent firms. Capital intensity means underwriting discipline and pricing power are critical to protect margins and credit quality. Keep originations selective and focus on deepening cross-sell to expand fee income and client stickiness.

Commercial real estate banking (select segments)

Well-positioned sponsors in resilient asset classes (industrial, medical, mixed-use) still grow; US industrial vacancy remained near historic lows (~4% in 2024) supporting rent growth and lending. Brookline’s local knowledge is a moat, but continuous spend on monitoring and portfolio analytics is required. As markets normalize, leaders become durable cash engines—invest in data and keep top borrowers close.

- Moat: local market expertise

- 2024: industrial vacancy ~4%

- Priority: invest in analytics

- Strategy: retain best borrowers

Integrated SMB packages (checking + payments)

Bundled checking + payments for SMBs are high-growth Stars for Brookline Bank: industry 2024 data shows merchant-services attach rates above 50% with strong retention, driving recurring fees despite higher onboarding/support spend; local market share looks solid—keep pricing tight and onboarding friction-free to sustain adoption and lifetime value.

- High attach

- High stickiness

- Ongoing onboarding cost

- Maintain sharp bundle

Boston opportunity: 4.9M metro, 73% mobile users, >50% merchant attach—fund APIs, UX, analytics.

Brookline’s Stars—treasury/cash management, mobile banking, SMB bundled checking+payments and selective middle‑market C&I—benefit from Greater Boston ~4.9M population, US mobile banking penetration ~73% (2024), industrial vacancy ~4% (2024) and merchant‑services attach >50% (2024); prioritize funding for APIs, UX, analytics and selective originations to capture growth and lock deposits/fees.

| Product | 2024 metric | Priority | Action |

|---|---|---|---|

| Treasury | Boston metro 4.9M | Invest | API integrations |

| Mobile | 73% penetration | Upgrade | UX/security |

| SMB bundle | Attach >50% | Scale | Reduce onboarding friction |

| C&I | Healthy pipelines | Selective | Underwrite tightly |

What is included in the product

Brookline Bank BCG Matrix: strategic review of units with invest/hold/divest guidance for Stars, Cash Cows, Question Marks and Dogs, plus trend risks.

One-page BCG Matrix placing Brookline Bank units in quadrants for quick C-level decisions and slide-ready exports.

Cash Cows

Core consumer deposits

Core consumer deposits remain a mature, high-share cash cow in Brookline Bank’s legacy neighborhoods, providing the low-cost funding that underpinned the bank’s stability through 2024. Promotion needs are modest now; priorities are retention and targeted fee optimization to extract revenue without acquisition spend. Small operational efficiencies and automation can lift net interest margin incrementally; milk gently to avoid spooking loyal customers.

Mortgage servicing & escrow

Existing serviced book produces steady fee income even when originations slow; industry servicing fees average ~25 basis points (0.25% annually) in 2024, supporting predictable revenue. Operations are stable and scalable with minor tech tweaks—workflow automation can cut servicing costs and attrition. Low growth, high predictability — classic cash cow. Maintain service levels and control leakage to protect margins.

Small business checking

Small business checking sits as a cash cow for Brookline Bank with an established base and predictable balances supporting dependable fee income; Brookline Bancorp reported total deposits of about $8.6 billion as of mid‑2024, highlighting scale. Growth is slow but churn stays low when service quality is high, reducing acquisition spend. Minimal marketing beyond periodic refreshes is required; optimize pricing and digital self‑service to widen the spread.

Branch-based consumer banking (core markets)

Branch-based consumer banking in Brookline Bank acts as a cash cow: entrenched presence in long-held neighborhoods keeps deposits sticky and churn low, while foot traffic is largely flat but relationship depth per customer remains high, supporting fee income and core deposit stability. Limited incremental capex preserves healthy return on tangible equity, and the physical footprint is prioritized for advisory and cross-sell rather than raw account acquisition.

- Deposit stickiness: neighborhood anchoring

- Traffic: flat; relationships: deep

- Capex: constrained to protect ROE

- Use: advisory/cross-sell over acquisition

ACH & wires for existing clients

ACH and wires for existing Brookline clients are habitual and recurring, with volumes steady; the US ACH network processed about 31 billion transactions in 2024, underscoring reliability. Margins are solid with modest compliance and platform costs, making the product highly bankable rather than a growth rocket. Keep reliability top-notch and nudge incremental volume.

- Steady habitual usage

- 31B US ACH txns in 2024

- Solid margins; modest compliance/platform costs

- Focus: reliability + incremental volume

Core deposits and SME checking deliver low-cost balance-sheet stability; prioritize ACH reliability

Core consumer deposits, small business checking, servicing fees and payments are stable cash cows for Brookline Bank, funding low-cost balance-sheet stability through 2024. Retention, fee optimization and modest automation lift margins without acquisition spend. Preserve branch footprint for cross-sell; prioritize reliability for ACH/wires.

| Metric | 2024 |

|---|---|

| Total deposits | $8.6B |

| Servicing fee | ~25 bps |

| US ACH volume | 31B txns |

What You See Is What You Get

Brookline Bank BCG Matrix

The Brookline Bank BCG Matrix you’re previewing is the exact file you’ll receive after purchase — no watermarks, no demo slides, just the finished report. It’s fully formatted and tailored for Brookline Bank with clear, market-backed insights to inform strategic decisions. After purchase the ready-to-use document is delivered immediately to your inbox for editing, printing, or presenting. One payment, no surprises — plug it straight into your planning.