Brookline Bank Business Model Canvas

Unlock the bank's strategic Business Model Canvas: value props, revenue levers, and growth drivers

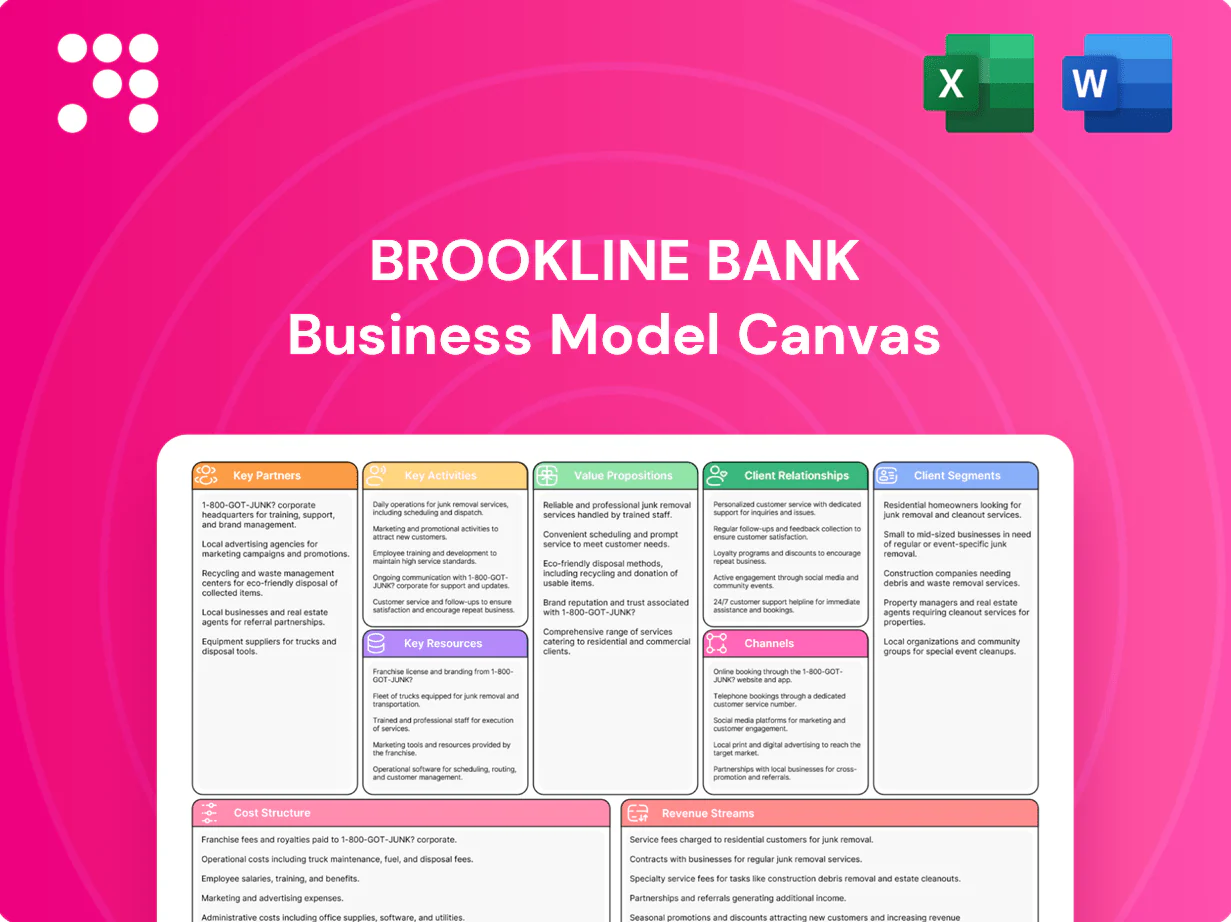

Unlock the full strategic blueprint behind Brookline Bank’s business model with our detailed Business Model Canvas. This in-depth file maps value propositions, customer segments, key partners, and revenue levers to show how the bank scales and outcompetes. Purchase the complete Canvas to download editable Word and Excel templates for analysis and strategic use.

Partnerships

Local businesses and realtors

Partnering with local realtors and developers feeds Brookline Bank’s residential mortgage pipeline and construction lending, while local businesses refer clients for deposit and cash management services. Co-marketing and community sponsorships boost brand visibility across Greater Boston. These ties deepen regional roots and drive meaningful cross-sell opportunities for loans, deposits, and treasury services.

Fintech and core banking vendors

Relationships with core processors and fintechs enable modern UX and shift onboarding from days to minutes, while RTP and FedNow adoption since 2023 expanded instant payment options in 2024. Robust APIs support treasury, ACH, RDC and card rails for real-time flows. Vendor SLAs typically guarantee 99.9% uptime plus security and compliance controls. Joint roadmaps cut delivery time and cost versus in-house builds.

Broker-dealers and wealth managers

Affiliations with broker-dealers and wealth managers supply Brookline Bank with investment products, advisory platforms, and custodial services that expand its fee-based offerings for individuals, families, and business owners. Shared compliance frameworks across partners reduce regulatory risk and improve suitability checks, enhancing client protection. Co-branded solutions help retain deposits and deepen wallet share by linking deposit and advisory relationships.

Correspondent lenders and secondary markets

Correspondent relationships provide Brookline Bank underwriting capacity and liquidity by enabling loan sales to GSEs and investors, supporting quicker turn times and balance sheet flexibility; the 2024 conforming loan limit is $766,550, guiding secondary market eligibility. Access to Fannie/Freddie optimizes balance sheet mix and capital use, while rate locks and hedging reduce pipeline risk and sharpen borrower pricing.

- Correspondent underwriting + loan sales

- GSE access (conforming limit 766,550 in 2024)

- Rate locks & hedging mitigate pipeline risk

- Improves competitive borrower pricing

Regulators and risk/insurance partners

Proactive engagement with regulators strengthens Brookline Bank's safety, soundness, and public trust through regular examinations, supervisory feedback, and compliance remediation cycles. Insurance partners cover credit, cyber, and operational exposures, reducing capital volatility from loss events. External auditors and consultants bolster model risk management and stress-testing, enabling prudent growth and resilience aligned with supervisory expectations.

- Regulatory exams: ongoing engagement

- Insurance: credit, cyber, operational

- Third-party: audit, model risk, stress tests

Partners, APIs and 99.9% SLAs accelerate mortgages, instant payments and GSE pricing

Local realtors, developers, fintechs, broker-dealers and correspondent banks drive Brookline Bank’s mortgage, deposit, treasury and wealth pipelines, enhancing cross-sell and regional share. Vendor SLAs (99.9% uptime) and APIs enable instant rails (RTP/FedNow adoption since 2023; expanded in 2024). GSE access (2024 conforming limit 766,550) improves liquidity and pricing while insurers, auditors and regulators reduce capital and compliance risk.

| Partner | 2024 Metric |

|---|---|

| GSE/conforming | $766,550 limit |

| Vendor SLA | 99.9% uptime |

| Payments | RTP/FedNow live (2024) |

What is included in the product

A comprehensive Brookline Bank Business Model Canvas outlining customer segments, channels, value propositions, revenue streams and key partners across the 9 BMC blocks, with linked competitive advantages and SWOT insights for presentations, strategy and investor use.

Condenses Brookline Bank’s strategy into a clean, editable one-page canvas that saves hours of formatting, enables quick comparisons, and supports team collaboration for faster decision-making.

Activities

Deposit gathering and liquidity management

Designing competitive checking, savings, and CDs drives stable, low-cost funding, aligning with Brookline Bank’s 2024 focus on deposit growth amid a higher-rate environment (fed funds ~5.25–5.50% in 2024). Daily liquidity monitoring matches cash flows to loans and securities, reducing funding stress. Pricing, promotions, and relationship tiers optimize cost of funds while branch, digital, and business bankers execute acquisition and retention.

Lending and credit underwriting

Originations span residential mortgages, HELOCs, and commercial credits, with underwriting driven by cash flow, collateral, and character analysis. Ongoing portfolio monitoring and covenant tracking manage concentration and credit risk. Pricing reflects credit grade, term, and market conditions, with the US federal funds target at 5.25–5.50% and 30‑year mortgage rates near 7% in 2024.

Cash management and payments

Brookline Bank’s treasury services cover ACH, wires, RDC, lockbox and merchant services, supporting a payments ecosystem that saw roughly 31.5 billion ACH transfers in 2024. Onboarding configures entitlements, limits and layered fraud controls to reduce risk. ERP integration streamlines cash flow and reconciliations, while dedicated service teams manage exceptions, daily reconciliations and client education.

Risk, compliance, and cybersecurity

Risk, compliance, and cybersecurity at Brookline Bank maintain BSA/AML, KYC, fair lending, and privacy programs; cyber operations continuously monitor threats, apply patches, and run incident response; credit models, stress tests, and concentration limits define risk appetite; training and independent audits sustain a strong control environment.

- Compliance: BSA/AML, KYC, fair lending, privacy

- Cyber: monitoring, patching, IR

- Risk tools: credit models, stress tests, limits

- Controls: training, audits

Customer service and relationship management

Bankers at Brookline Bank provide advisory support across life and business stages, with contact centers, online chat and branch staff resolving the majority of needs quickly; CRM tools drove an 18% cross-sell uplift and enabled proactive outreach, while 2024 feedback loops informed product design and cut selected process cycle times by 12%.

- Advisory across life/business stages

- Omnichannel resolution: contact center, chat, branches

- CRM-driven 18% cross-sell uplift

- Feedback loops -> 12% faster processes

Deposit growth and credit discipline: fed funds 5.25–5.50%, 30‑yr ~7%

Designing deposit products, daily liquidity management, origination & portfolio monitoring, treasury payments, risk/compliance, and advisory drove Brookline Bank’s 2024 focus on deposit growth and credit discipline with fed funds 5.25–5.50% and 30‑yr mortgage ~7%. CRM delivered an 18% cross‑sell uplift; process cycle times fell 12%; ACH ecosystem handled ~31.5B transfers.

| Activity | 2024 Metric |

|---|---|

| Funding | Fed funds 5.25–5.50% |

| Mortgages | 30‑yr ~7% |

| Payments | ACH ~31.5B |

| CRM | +18% cross‑sell |

| OPS | -12% cycle time |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the exact Brookline Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this is the live deliverable with all content and structure visible. After ordering you'll download the complete file, ready to edit and present.

Unlock the bank's strategic Business Model Canvas: value props, revenue levers, and growth drivers

Unlock the full strategic blueprint behind Brookline Bank’s business model with our detailed Business Model Canvas. This in-depth file maps value propositions, customer segments, key partners, and revenue levers to show how the bank scales and outcompetes. Purchase the complete Canvas to download editable Word and Excel templates for analysis and strategic use.

Partnerships

Local businesses and realtors

Partnering with local realtors and developers feeds Brookline Bank’s residential mortgage pipeline and construction lending, while local businesses refer clients for deposit and cash management services. Co-marketing and community sponsorships boost brand visibility across Greater Boston. These ties deepen regional roots and drive meaningful cross-sell opportunities for loans, deposits, and treasury services.

Fintech and core banking vendors

Relationships with core processors and fintechs enable modern UX and shift onboarding from days to minutes, while RTP and FedNow adoption since 2023 expanded instant payment options in 2024. Robust APIs support treasury, ACH, RDC and card rails for real-time flows. Vendor SLAs typically guarantee 99.9% uptime plus security and compliance controls. Joint roadmaps cut delivery time and cost versus in-house builds.

Broker-dealers and wealth managers

Affiliations with broker-dealers and wealth managers supply Brookline Bank with investment products, advisory platforms, and custodial services that expand its fee-based offerings for individuals, families, and business owners. Shared compliance frameworks across partners reduce regulatory risk and improve suitability checks, enhancing client protection. Co-branded solutions help retain deposits and deepen wallet share by linking deposit and advisory relationships.

Correspondent lenders and secondary markets

Correspondent relationships provide Brookline Bank underwriting capacity and liquidity by enabling loan sales to GSEs and investors, supporting quicker turn times and balance sheet flexibility; the 2024 conforming loan limit is $766,550, guiding secondary market eligibility. Access to Fannie/Freddie optimizes balance sheet mix and capital use, while rate locks and hedging reduce pipeline risk and sharpen borrower pricing.

- Correspondent underwriting + loan sales

- GSE access (conforming limit 766,550 in 2024)

- Rate locks & hedging mitigate pipeline risk

- Improves competitive borrower pricing

Regulators and risk/insurance partners

Proactive engagement with regulators strengthens Brookline Bank's safety, soundness, and public trust through regular examinations, supervisory feedback, and compliance remediation cycles. Insurance partners cover credit, cyber, and operational exposures, reducing capital volatility from loss events. External auditors and consultants bolster model risk management and stress-testing, enabling prudent growth and resilience aligned with supervisory expectations.

- Regulatory exams: ongoing engagement

- Insurance: credit, cyber, operational

- Third-party: audit, model risk, stress tests

Partners, APIs and 99.9% SLAs accelerate mortgages, instant payments and GSE pricing

Local realtors, developers, fintechs, broker-dealers and correspondent banks drive Brookline Bank’s mortgage, deposit, treasury and wealth pipelines, enhancing cross-sell and regional share. Vendor SLAs (99.9% uptime) and APIs enable instant rails (RTP/FedNow adoption since 2023; expanded in 2024). GSE access (2024 conforming limit 766,550) improves liquidity and pricing while insurers, auditors and regulators reduce capital and compliance risk.

| Partner | 2024 Metric |

|---|---|

| GSE/conforming | $766,550 limit |

| Vendor SLA | 99.9% uptime |

| Payments | RTP/FedNow live (2024) |

What is included in the product

A comprehensive Brookline Bank Business Model Canvas outlining customer segments, channels, value propositions, revenue streams and key partners across the 9 BMC blocks, with linked competitive advantages and SWOT insights for presentations, strategy and investor use.

Condenses Brookline Bank’s strategy into a clean, editable one-page canvas that saves hours of formatting, enables quick comparisons, and supports team collaboration for faster decision-making.

Activities

Deposit gathering and liquidity management

Designing competitive checking, savings, and CDs drives stable, low-cost funding, aligning with Brookline Bank’s 2024 focus on deposit growth amid a higher-rate environment (fed funds ~5.25–5.50% in 2024). Daily liquidity monitoring matches cash flows to loans and securities, reducing funding stress. Pricing, promotions, and relationship tiers optimize cost of funds while branch, digital, and business bankers execute acquisition and retention.

Lending and credit underwriting

Originations span residential mortgages, HELOCs, and commercial credits, with underwriting driven by cash flow, collateral, and character analysis. Ongoing portfolio monitoring and covenant tracking manage concentration and credit risk. Pricing reflects credit grade, term, and market conditions, with the US federal funds target at 5.25–5.50% and 30‑year mortgage rates near 7% in 2024.

Cash management and payments

Brookline Bank’s treasury services cover ACH, wires, RDC, lockbox and merchant services, supporting a payments ecosystem that saw roughly 31.5 billion ACH transfers in 2024. Onboarding configures entitlements, limits and layered fraud controls to reduce risk. ERP integration streamlines cash flow and reconciliations, while dedicated service teams manage exceptions, daily reconciliations and client education.

Risk, compliance, and cybersecurity

Risk, compliance, and cybersecurity at Brookline Bank maintain BSA/AML, KYC, fair lending, and privacy programs; cyber operations continuously monitor threats, apply patches, and run incident response; credit models, stress tests, and concentration limits define risk appetite; training and independent audits sustain a strong control environment.

- Compliance: BSA/AML, KYC, fair lending, privacy

- Cyber: monitoring, patching, IR

- Risk tools: credit models, stress tests, limits

- Controls: training, audits

Customer service and relationship management

Bankers at Brookline Bank provide advisory support across life and business stages, with contact centers, online chat and branch staff resolving the majority of needs quickly; CRM tools drove an 18% cross-sell uplift and enabled proactive outreach, while 2024 feedback loops informed product design and cut selected process cycle times by 12%.

- Advisory across life/business stages

- Omnichannel resolution: contact center, chat, branches

- CRM-driven 18% cross-sell uplift

- Feedback loops -> 12% faster processes

Deposit growth and credit discipline: fed funds 5.25–5.50%, 30‑yr ~7%

Designing deposit products, daily liquidity management, origination & portfolio monitoring, treasury payments, risk/compliance, and advisory drove Brookline Bank’s 2024 focus on deposit growth and credit discipline with fed funds 5.25–5.50% and 30‑yr mortgage ~7%. CRM delivered an 18% cross‑sell uplift; process cycle times fell 12%; ACH ecosystem handled ~31.5B transfers.

| Activity | 2024 Metric |

|---|---|

| Funding | Fed funds 5.25–5.50% |

| Mortgages | 30‑yr ~7% |

| Payments | ACH ~31.5B |

| CRM | +18% cross‑sell |

| OPS | -12% cycle time |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the exact Brookline Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this is the live deliverable with all content and structure visible. After ordering you'll download the complete file, ready to edit and present.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the bank's strategic Business Model Canvas: value props, revenue levers, and growth drivers

Unlock the full strategic blueprint behind Brookline Bank’s business model with our detailed Business Model Canvas. This in-depth file maps value propositions, customer segments, key partners, and revenue levers to show how the bank scales and outcompetes. Purchase the complete Canvas to download editable Word and Excel templates for analysis and strategic use.

Partnerships

Local businesses and realtors

Partnering with local realtors and developers feeds Brookline Bank’s residential mortgage pipeline and construction lending, while local businesses refer clients for deposit and cash management services. Co-marketing and community sponsorships boost brand visibility across Greater Boston. These ties deepen regional roots and drive meaningful cross-sell opportunities for loans, deposits, and treasury services.

Fintech and core banking vendors

Relationships with core processors and fintechs enable modern UX and shift onboarding from days to minutes, while RTP and FedNow adoption since 2023 expanded instant payment options in 2024. Robust APIs support treasury, ACH, RDC and card rails for real-time flows. Vendor SLAs typically guarantee 99.9% uptime plus security and compliance controls. Joint roadmaps cut delivery time and cost versus in-house builds.

Broker-dealers and wealth managers

Affiliations with broker-dealers and wealth managers supply Brookline Bank with investment products, advisory platforms, and custodial services that expand its fee-based offerings for individuals, families, and business owners. Shared compliance frameworks across partners reduce regulatory risk and improve suitability checks, enhancing client protection. Co-branded solutions help retain deposits and deepen wallet share by linking deposit and advisory relationships.

Correspondent lenders and secondary markets

Correspondent relationships provide Brookline Bank underwriting capacity and liquidity by enabling loan sales to GSEs and investors, supporting quicker turn times and balance sheet flexibility; the 2024 conforming loan limit is $766,550, guiding secondary market eligibility. Access to Fannie/Freddie optimizes balance sheet mix and capital use, while rate locks and hedging reduce pipeline risk and sharpen borrower pricing.

- Correspondent underwriting + loan sales

- GSE access (conforming limit 766,550 in 2024)

- Rate locks & hedging mitigate pipeline risk

- Improves competitive borrower pricing

Regulators and risk/insurance partners

Proactive engagement with regulators strengthens Brookline Bank's safety, soundness, and public trust through regular examinations, supervisory feedback, and compliance remediation cycles. Insurance partners cover credit, cyber, and operational exposures, reducing capital volatility from loss events. External auditors and consultants bolster model risk management and stress-testing, enabling prudent growth and resilience aligned with supervisory expectations.

- Regulatory exams: ongoing engagement

- Insurance: credit, cyber, operational

- Third-party: audit, model risk, stress tests

Partners, APIs and 99.9% SLAs accelerate mortgages, instant payments and GSE pricing

Local realtors, developers, fintechs, broker-dealers and correspondent banks drive Brookline Bank’s mortgage, deposit, treasury and wealth pipelines, enhancing cross-sell and regional share. Vendor SLAs (99.9% uptime) and APIs enable instant rails (RTP/FedNow adoption since 2023; expanded in 2024). GSE access (2024 conforming limit 766,550) improves liquidity and pricing while insurers, auditors and regulators reduce capital and compliance risk.

| Partner | 2024 Metric |

|---|---|

| GSE/conforming | $766,550 limit |

| Vendor SLA | 99.9% uptime |

| Payments | RTP/FedNow live (2024) |

What is included in the product

A comprehensive Brookline Bank Business Model Canvas outlining customer segments, channels, value propositions, revenue streams and key partners across the 9 BMC blocks, with linked competitive advantages and SWOT insights for presentations, strategy and investor use.

Condenses Brookline Bank’s strategy into a clean, editable one-page canvas that saves hours of formatting, enables quick comparisons, and supports team collaboration for faster decision-making.

Activities

Deposit gathering and liquidity management

Designing competitive checking, savings, and CDs drives stable, low-cost funding, aligning with Brookline Bank’s 2024 focus on deposit growth amid a higher-rate environment (fed funds ~5.25–5.50% in 2024). Daily liquidity monitoring matches cash flows to loans and securities, reducing funding stress. Pricing, promotions, and relationship tiers optimize cost of funds while branch, digital, and business bankers execute acquisition and retention.

Lending and credit underwriting

Originations span residential mortgages, HELOCs, and commercial credits, with underwriting driven by cash flow, collateral, and character analysis. Ongoing portfolio monitoring and covenant tracking manage concentration and credit risk. Pricing reflects credit grade, term, and market conditions, with the US federal funds target at 5.25–5.50% and 30‑year mortgage rates near 7% in 2024.

Cash management and payments

Brookline Bank’s treasury services cover ACH, wires, RDC, lockbox and merchant services, supporting a payments ecosystem that saw roughly 31.5 billion ACH transfers in 2024. Onboarding configures entitlements, limits and layered fraud controls to reduce risk. ERP integration streamlines cash flow and reconciliations, while dedicated service teams manage exceptions, daily reconciliations and client education.

Risk, compliance, and cybersecurity

Risk, compliance, and cybersecurity at Brookline Bank maintain BSA/AML, KYC, fair lending, and privacy programs; cyber operations continuously monitor threats, apply patches, and run incident response; credit models, stress tests, and concentration limits define risk appetite; training and independent audits sustain a strong control environment.

- Compliance: BSA/AML, KYC, fair lending, privacy

- Cyber: monitoring, patching, IR

- Risk tools: credit models, stress tests, limits

- Controls: training, audits

Customer service and relationship management

Bankers at Brookline Bank provide advisory support across life and business stages, with contact centers, online chat and branch staff resolving the majority of needs quickly; CRM tools drove an 18% cross-sell uplift and enabled proactive outreach, while 2024 feedback loops informed product design and cut selected process cycle times by 12%.

- Advisory across life/business stages

- Omnichannel resolution: contact center, chat, branches

- CRM-driven 18% cross-sell uplift

- Feedback loops -> 12% faster processes

Deposit growth and credit discipline: fed funds 5.25–5.50%, 30‑yr ~7%

Designing deposit products, daily liquidity management, origination & portfolio monitoring, treasury payments, risk/compliance, and advisory drove Brookline Bank’s 2024 focus on deposit growth and credit discipline with fed funds 5.25–5.50% and 30‑yr mortgage ~7%. CRM delivered an 18% cross‑sell uplift; process cycle times fell 12%; ACH ecosystem handled ~31.5B transfers.

| Activity | 2024 Metric |

|---|---|

| Funding | Fed funds 5.25–5.50% |

| Mortgages | 30‑yr ~7% |

| Payments | ACH ~31.5B |

| CRM | +18% cross‑sell |

| OPS | -12% cycle time |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the exact Brookline Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this is the live deliverable with all content and structure visible. After ordering you'll download the complete file, ready to edit and present.