The Burnet Group PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of The Burnet Group—concise, evidence-based insights on political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists; purchase the full report to access deep-dive findings and actionable recommendations instantly.

Political factors

Zoning and land-use policy shifts

Zoning rewrites and upzoning/downzoning directly change feasibility, FAR and repositioning options, often shifting allowed FAR by 10–40% in targeted municipal plans. The Burnet Group must monitor municipal plans and community boards to recalibrate site selection and density assumptions. Early engagement shortens entitlement timelines, typically 12–36 months, improving value-add underwriting. Scenario analysis should price approval risk and mitigation costs (commonly 5–10% contingencies).

Public infrastructure and incentives

Transit expansions funded under the $1.2 trillion Bipartisan Infrastructure Law and local TIF districts/tax abatements have driven 5–10% rent uplifts and 50–150 bps cap‑rate compression in transit‑proximate submarkets (industry reports, 2023–2025). Tracking municipal capital budgets and incentive pipelines guides site selection and client capital allocation. Models should quantify rent uplift, cap‑rate change and outline incentive capture and compliance pathways for advisory engagements.

Political stability and election cycles

Election outcomes can alter development priorities, property taxes, and affordable housing mandates; national contests such as Nov 5, 2024 often precipitate measurable policy shifts. The Burnet Group should stress-test portfolios across policy regimes and timelines. Short windows around elections may delay approvals or trigger last-minute policy pushes. Communications should adjust to shifting political risk premiums.

Trade, FDI, and geopolitical risk

Supply-chain frictions and FDI restrictions are raising construction costs and altering cross-border capital flows; global FDI fell about 12% to roughly $1.04 trillion in 2023 (UNCTAD) while construction input inflation averaged near 7% in 2023, forcing clients to add country-risk overlays and FX scenarios to allocations.

- Integrate geopolitical-risk scores into hurdle rates and exit timing

- Use hedging strategies for currency and interest-rate exposure

- Prioritize partner selection to mitigate local operational risk

Public-private partnerships (PPPs)

PPPs open large-scale mixed-use and infrastructure-adjacent opportunities; The Burnet Group can advise on deal structuring, risk-sharing, and performance covenants to attract private capital alongside public programmes such as the US 1.2 trillion Infrastructure Investment and Jobs Act.

Diligence must assess political will, funding durability and community benefits agreements; robust stakeholder mapping reduces entitlement friction and improves deliverability.

- Deal structuring: risk allocation, covenants, returns

- Diligence: political will, funding durability (e.g., IIJA scale)

- Stakeholders: community benefits, entitlement mapping

Zoning shifts FAR 10–40%; transit incentives lift rents5–10%

Zoning changes shift FAR 10–40%, requiring The Burnet Group to monitor plans and community boards to recalibrate site selection and entitlements.

IIJA/BIL $1.2T and transit/TIF incentives drove 5–10% rent uplifts and 50–150 bps cap‑rate compression in transit‑proximate submarkets (2023–25).

Global FDI fell ~12% to $1.04T in 2023 and construction input inflation ~7% (2023), forcing contingency buffers of 5–10% and political risk overlays.

| Metric | Value |

|---|---|

| FAR shift | 10–40% |

| Rent uplift | 5–10% |

| Cap‑rate move | 50–150 bps |

| FDI (2023) | $1.04T (−12%) |

What is included in the product

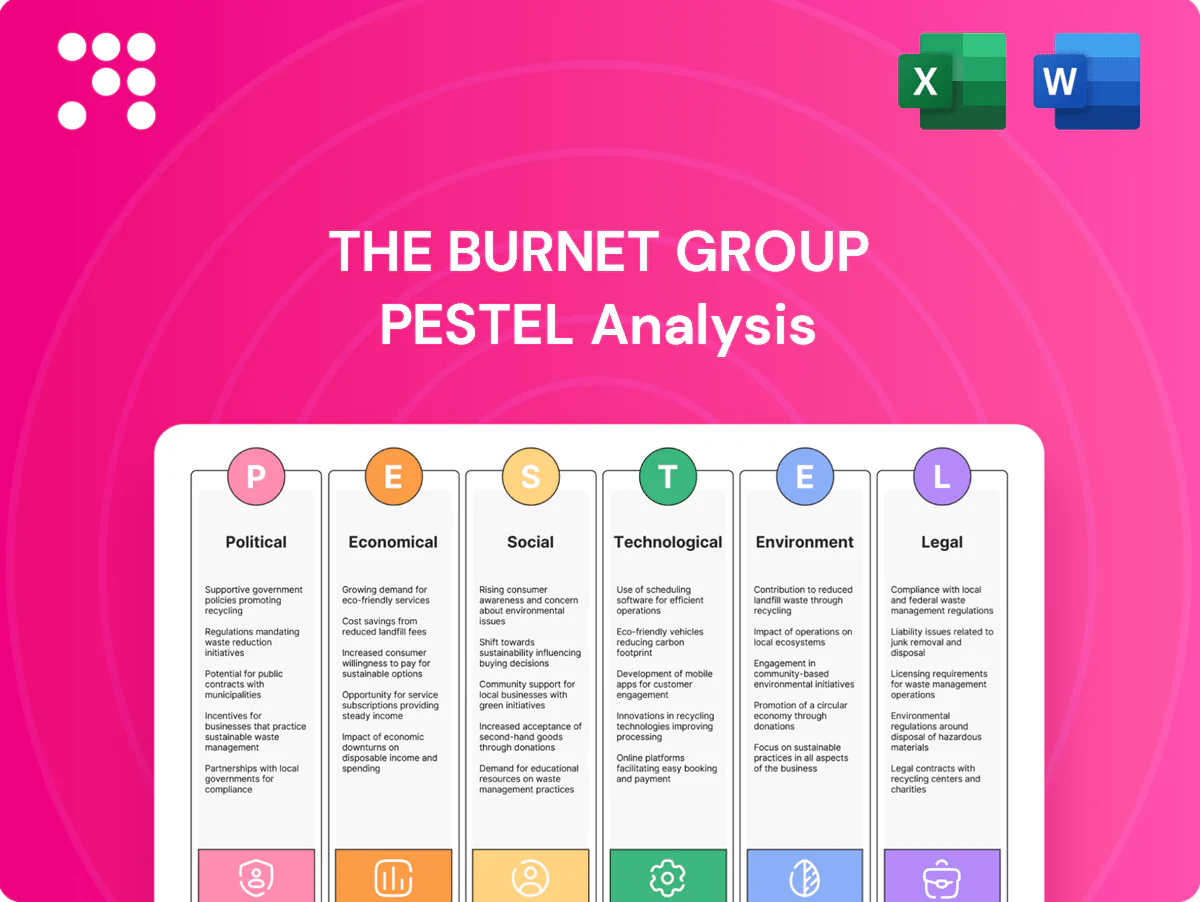

Explores how macro-environmental factors uniquely affect The Burnet Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking scenarios; designed for executives, consultants, and investors to identify risks, opportunities, and strategy-ready recommendations aligned to regional market and regulatory dynamics.

Provides a concise, visually segmented PESTLE summary of The Burnet Group that’s easily shared, dropped into presentations, and annotated for team planning.

Economic factors

Interest rates and credit conditions

Rate volatility—with the fed funds target near 5.25–5.50% and the 10-year Treasury around 4.0% in mid-2025—reshapes cap rates (up 150–300 bps vs 2021), DSCR cushions and development IRRs; The Burnet Group should model forward curves, layered debt structures and sensitivity bands across base/soft/hard scenarios. Tighter credit has widened bid-ask spreads and lengthened time-to-close by ~30–60 days; advisory must prioritize capital‑stack optimization and refinance-risk mitigation.

Macro growth and labor markets

US real GDP expanded about 2.5% in 2024 while unemployment averaged roughly 3.7%, and office utilization stabilized near 50–60%—all driving absorption and rent trajectories. Strong sectoral growth in tech, life sciences and logistics creates pronounced micro-market divergences in demand and pricing. The Burnet Group can map job nodes to demand pipelines and pricing power using employment clusters and commute-shed analytics. Vacancy forecasts must fold in sustained hybrid occupancy and automation, which can depress effective demand by several percentage points.

Construction costs and inflation

Materials and labor inflation—materials up about 5.6% YoY and construction wages up ~4.2% in 2024—erodes pro formas and forces larger contingencies. The Burnet Group should integrate commodity indices (CRB/LME) and wage series into dynamic cost models to reprice pipelines. Value engineering and project phasing can preserve IRR under cost shocks, while contracting strategies like GMPs and indexed escalators shift or cap downside risk.

Capital flows and liquidity cycles

Allocations from pensions (over $50 trillion in global assets), insurers (≈$30–35 trillion), and REITs shape competition and exit liquidity, while liquidity droughts push buyers toward off-market acquisitions and recapitalizations; The Burnet Group can advise on vintage timing and distressed opportunities as secondary volumes topped $100bn in 2023 and NAV lending expands.

- pensions: large allocs, exit pressure

- liquidity droughts: off-market & recaps

- secondaries & NAV lending: portfolio flexibility

Local fiscal health and taxation

Local fiscal health and taxation drive NOI and pricing: property taxes (about 70% of local own‑source revenue per U.S. Census Bureau) and municipal budget gaps can raise carrying costs, while transfer taxes (e.g., NYC up to 2.925% on residential transfers) compress sale proceeds; The Burnet Group should map fiscal risk into market selection and hold‑period assumptions and run stress tests with 100–300 bps tax‑rate shocks at city and state levels.

- Map fiscal risk to market selection

- Include 100–300 bps tax shocks in stress tests

- Pursue abatements/appeals to boost yields

- Monitor property tax reassessments and transfer tax rates

Zoning shifts FAR 10–40%; transit incentives lift rents5–10%

Elevated rates (Fed 5.25–5.50%, 10y ~4.0% mid‑2025) lift cap rates +150–300bps, press DSCR and development IRRs; model forward curves and layered debt. US GDP ~2.5% (2024), unemployment ~3.7%, office utilization 50–60% with tech/life sciences/logistics divergence. Materials +5.6% YoY, construction wages +4.2% (2024); pensions ~$50T, insurers $30–35T, secondaries ~$100B (2023); map tax risks (property taxes ~70% local revenue).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 10‑yr Treasury | ~4.0% |

| US GDP (2024) | ~2.5% |

| Unemployment (2024) | ~3.7% |

| Materials inflation (2024) | +5.6% YoY |

| Construction wages (2024) | +4.2% YoY |

Full Version Awaits

The Burnet Group PESTLE Analysis

The preview shown here is the exact PESTLE analysis of The Burnet Group you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or surprises. The layout, content, and structure visible are exactly the final file you can download immediately after buying.

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of The Burnet Group—concise, evidence-based insights on political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists; purchase the full report to access deep-dive findings and actionable recommendations instantly.

Political factors

Zoning and land-use policy shifts

Zoning rewrites and upzoning/downzoning directly change feasibility, FAR and repositioning options, often shifting allowed FAR by 10–40% in targeted municipal plans. The Burnet Group must monitor municipal plans and community boards to recalibrate site selection and density assumptions. Early engagement shortens entitlement timelines, typically 12–36 months, improving value-add underwriting. Scenario analysis should price approval risk and mitigation costs (commonly 5–10% contingencies).

Public infrastructure and incentives

Transit expansions funded under the $1.2 trillion Bipartisan Infrastructure Law and local TIF districts/tax abatements have driven 5–10% rent uplifts and 50–150 bps cap‑rate compression in transit‑proximate submarkets (industry reports, 2023–2025). Tracking municipal capital budgets and incentive pipelines guides site selection and client capital allocation. Models should quantify rent uplift, cap‑rate change and outline incentive capture and compliance pathways for advisory engagements.

Political stability and election cycles

Election outcomes can alter development priorities, property taxes, and affordable housing mandates; national contests such as Nov 5, 2024 often precipitate measurable policy shifts. The Burnet Group should stress-test portfolios across policy regimes and timelines. Short windows around elections may delay approvals or trigger last-minute policy pushes. Communications should adjust to shifting political risk premiums.

Trade, FDI, and geopolitical risk

Supply-chain frictions and FDI restrictions are raising construction costs and altering cross-border capital flows; global FDI fell about 12% to roughly $1.04 trillion in 2023 (UNCTAD) while construction input inflation averaged near 7% in 2023, forcing clients to add country-risk overlays and FX scenarios to allocations.

- Integrate geopolitical-risk scores into hurdle rates and exit timing

- Use hedging strategies for currency and interest-rate exposure

- Prioritize partner selection to mitigate local operational risk

Public-private partnerships (PPPs)

PPPs open large-scale mixed-use and infrastructure-adjacent opportunities; The Burnet Group can advise on deal structuring, risk-sharing, and performance covenants to attract private capital alongside public programmes such as the US 1.2 trillion Infrastructure Investment and Jobs Act.

Diligence must assess political will, funding durability and community benefits agreements; robust stakeholder mapping reduces entitlement friction and improves deliverability.

- Deal structuring: risk allocation, covenants, returns

- Diligence: political will, funding durability (e.g., IIJA scale)

- Stakeholders: community benefits, entitlement mapping

Zoning shifts FAR 10–40%; transit incentives lift rents5–10%

Zoning changes shift FAR 10–40%, requiring The Burnet Group to monitor plans and community boards to recalibrate site selection and entitlements.

IIJA/BIL $1.2T and transit/TIF incentives drove 5–10% rent uplifts and 50–150 bps cap‑rate compression in transit‑proximate submarkets (2023–25).

Global FDI fell ~12% to $1.04T in 2023 and construction input inflation ~7% (2023), forcing contingency buffers of 5–10% and political risk overlays.

| Metric | Value |

|---|---|

| FAR shift | 10–40% |

| Rent uplift | 5–10% |

| Cap‑rate move | 50–150 bps |

| FDI (2023) | $1.04T (−12%) |

What is included in the product

Explores how macro-environmental factors uniquely affect The Burnet Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking scenarios; designed for executives, consultants, and investors to identify risks, opportunities, and strategy-ready recommendations aligned to regional market and regulatory dynamics.

Provides a concise, visually segmented PESTLE summary of The Burnet Group that’s easily shared, dropped into presentations, and annotated for team planning.

Economic factors

Interest rates and credit conditions

Rate volatility—with the fed funds target near 5.25–5.50% and the 10-year Treasury around 4.0% in mid-2025—reshapes cap rates (up 150–300 bps vs 2021), DSCR cushions and development IRRs; The Burnet Group should model forward curves, layered debt structures and sensitivity bands across base/soft/hard scenarios. Tighter credit has widened bid-ask spreads and lengthened time-to-close by ~30–60 days; advisory must prioritize capital‑stack optimization and refinance-risk mitigation.

Macro growth and labor markets

US real GDP expanded about 2.5% in 2024 while unemployment averaged roughly 3.7%, and office utilization stabilized near 50–60%—all driving absorption and rent trajectories. Strong sectoral growth in tech, life sciences and logistics creates pronounced micro-market divergences in demand and pricing. The Burnet Group can map job nodes to demand pipelines and pricing power using employment clusters and commute-shed analytics. Vacancy forecasts must fold in sustained hybrid occupancy and automation, which can depress effective demand by several percentage points.

Construction costs and inflation

Materials and labor inflation—materials up about 5.6% YoY and construction wages up ~4.2% in 2024—erodes pro formas and forces larger contingencies. The Burnet Group should integrate commodity indices (CRB/LME) and wage series into dynamic cost models to reprice pipelines. Value engineering and project phasing can preserve IRR under cost shocks, while contracting strategies like GMPs and indexed escalators shift or cap downside risk.

Capital flows and liquidity cycles

Allocations from pensions (over $50 trillion in global assets), insurers (≈$30–35 trillion), and REITs shape competition and exit liquidity, while liquidity droughts push buyers toward off-market acquisitions and recapitalizations; The Burnet Group can advise on vintage timing and distressed opportunities as secondary volumes topped $100bn in 2023 and NAV lending expands.

- pensions: large allocs, exit pressure

- liquidity droughts: off-market & recaps

- secondaries & NAV lending: portfolio flexibility

Local fiscal health and taxation

Local fiscal health and taxation drive NOI and pricing: property taxes (about 70% of local own‑source revenue per U.S. Census Bureau) and municipal budget gaps can raise carrying costs, while transfer taxes (e.g., NYC up to 2.925% on residential transfers) compress sale proceeds; The Burnet Group should map fiscal risk into market selection and hold‑period assumptions and run stress tests with 100–300 bps tax‑rate shocks at city and state levels.

- Map fiscal risk to market selection

- Include 100–300 bps tax shocks in stress tests

- Pursue abatements/appeals to boost yields

- Monitor property tax reassessments and transfer tax rates

Zoning shifts FAR 10–40%; transit incentives lift rents5–10%

Elevated rates (Fed 5.25–5.50%, 10y ~4.0% mid‑2025) lift cap rates +150–300bps, press DSCR and development IRRs; model forward curves and layered debt. US GDP ~2.5% (2024), unemployment ~3.7%, office utilization 50–60% with tech/life sciences/logistics divergence. Materials +5.6% YoY, construction wages +4.2% (2024); pensions ~$50T, insurers $30–35T, secondaries ~$100B (2023); map tax risks (property taxes ~70% local revenue).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 10‑yr Treasury | ~4.0% |

| US GDP (2024) | ~2.5% |

| Unemployment (2024) | ~3.7% |

| Materials inflation (2024) | +5.6% YoY |

| Construction wages (2024) | +4.2% YoY |

Full Version Awaits

The Burnet Group PESTLE Analysis

The preview shown here is the exact PESTLE analysis of The Burnet Group you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or surprises. The layout, content, and structure visible are exactly the final file you can download immediately after buying.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of The Burnet Group—concise, evidence-based insights on political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists; purchase the full report to access deep-dive findings and actionable recommendations instantly.

Political factors

Zoning and land-use policy shifts

Zoning rewrites and upzoning/downzoning directly change feasibility, FAR and repositioning options, often shifting allowed FAR by 10–40% in targeted municipal plans. The Burnet Group must monitor municipal plans and community boards to recalibrate site selection and density assumptions. Early engagement shortens entitlement timelines, typically 12–36 months, improving value-add underwriting. Scenario analysis should price approval risk and mitigation costs (commonly 5–10% contingencies).

Public infrastructure and incentives

Transit expansions funded under the $1.2 trillion Bipartisan Infrastructure Law and local TIF districts/tax abatements have driven 5–10% rent uplifts and 50–150 bps cap‑rate compression in transit‑proximate submarkets (industry reports, 2023–2025). Tracking municipal capital budgets and incentive pipelines guides site selection and client capital allocation. Models should quantify rent uplift, cap‑rate change and outline incentive capture and compliance pathways for advisory engagements.

Political stability and election cycles

Election outcomes can alter development priorities, property taxes, and affordable housing mandates; national contests such as Nov 5, 2024 often precipitate measurable policy shifts. The Burnet Group should stress-test portfolios across policy regimes and timelines. Short windows around elections may delay approvals or trigger last-minute policy pushes. Communications should adjust to shifting political risk premiums.

Trade, FDI, and geopolitical risk

Supply-chain frictions and FDI restrictions are raising construction costs and altering cross-border capital flows; global FDI fell about 12% to roughly $1.04 trillion in 2023 (UNCTAD) while construction input inflation averaged near 7% in 2023, forcing clients to add country-risk overlays and FX scenarios to allocations.

- Integrate geopolitical-risk scores into hurdle rates and exit timing

- Use hedging strategies for currency and interest-rate exposure

- Prioritize partner selection to mitigate local operational risk

Public-private partnerships (PPPs)

PPPs open large-scale mixed-use and infrastructure-adjacent opportunities; The Burnet Group can advise on deal structuring, risk-sharing, and performance covenants to attract private capital alongside public programmes such as the US 1.2 trillion Infrastructure Investment and Jobs Act.

Diligence must assess political will, funding durability and community benefits agreements; robust stakeholder mapping reduces entitlement friction and improves deliverability.

- Deal structuring: risk allocation, covenants, returns

- Diligence: political will, funding durability (e.g., IIJA scale)

- Stakeholders: community benefits, entitlement mapping

Zoning shifts FAR 10–40%; transit incentives lift rents5–10%

Zoning changes shift FAR 10–40%, requiring The Burnet Group to monitor plans and community boards to recalibrate site selection and entitlements.

IIJA/BIL $1.2T and transit/TIF incentives drove 5–10% rent uplifts and 50–150 bps cap‑rate compression in transit‑proximate submarkets (2023–25).

Global FDI fell ~12% to $1.04T in 2023 and construction input inflation ~7% (2023), forcing contingency buffers of 5–10% and political risk overlays.

| Metric | Value |

|---|---|

| FAR shift | 10–40% |

| Rent uplift | 5–10% |

| Cap‑rate move | 50–150 bps |

| FDI (2023) | $1.04T (−12%) |

What is included in the product

Explores how macro-environmental factors uniquely affect The Burnet Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking scenarios; designed for executives, consultants, and investors to identify risks, opportunities, and strategy-ready recommendations aligned to regional market and regulatory dynamics.

Provides a concise, visually segmented PESTLE summary of The Burnet Group that’s easily shared, dropped into presentations, and annotated for team planning.

Economic factors

Interest rates and credit conditions

Rate volatility—with the fed funds target near 5.25–5.50% and the 10-year Treasury around 4.0% in mid-2025—reshapes cap rates (up 150–300 bps vs 2021), DSCR cushions and development IRRs; The Burnet Group should model forward curves, layered debt structures and sensitivity bands across base/soft/hard scenarios. Tighter credit has widened bid-ask spreads and lengthened time-to-close by ~30–60 days; advisory must prioritize capital‑stack optimization and refinance-risk mitigation.

Macro growth and labor markets

US real GDP expanded about 2.5% in 2024 while unemployment averaged roughly 3.7%, and office utilization stabilized near 50–60%—all driving absorption and rent trajectories. Strong sectoral growth in tech, life sciences and logistics creates pronounced micro-market divergences in demand and pricing. The Burnet Group can map job nodes to demand pipelines and pricing power using employment clusters and commute-shed analytics. Vacancy forecasts must fold in sustained hybrid occupancy and automation, which can depress effective demand by several percentage points.

Construction costs and inflation

Materials and labor inflation—materials up about 5.6% YoY and construction wages up ~4.2% in 2024—erodes pro formas and forces larger contingencies. The Burnet Group should integrate commodity indices (CRB/LME) and wage series into dynamic cost models to reprice pipelines. Value engineering and project phasing can preserve IRR under cost shocks, while contracting strategies like GMPs and indexed escalators shift or cap downside risk.

Capital flows and liquidity cycles

Allocations from pensions (over $50 trillion in global assets), insurers (≈$30–35 trillion), and REITs shape competition and exit liquidity, while liquidity droughts push buyers toward off-market acquisitions and recapitalizations; The Burnet Group can advise on vintage timing and distressed opportunities as secondary volumes topped $100bn in 2023 and NAV lending expands.

- pensions: large allocs, exit pressure

- liquidity droughts: off-market & recaps

- secondaries & NAV lending: portfolio flexibility

Local fiscal health and taxation

Local fiscal health and taxation drive NOI and pricing: property taxes (about 70% of local own‑source revenue per U.S. Census Bureau) and municipal budget gaps can raise carrying costs, while transfer taxes (e.g., NYC up to 2.925% on residential transfers) compress sale proceeds; The Burnet Group should map fiscal risk into market selection and hold‑period assumptions and run stress tests with 100–300 bps tax‑rate shocks at city and state levels.

- Map fiscal risk to market selection

- Include 100–300 bps tax shocks in stress tests

- Pursue abatements/appeals to boost yields

- Monitor property tax reassessments and transfer tax rates

Zoning shifts FAR 10–40%; transit incentives lift rents5–10%

Elevated rates (Fed 5.25–5.50%, 10y ~4.0% mid‑2025) lift cap rates +150–300bps, press DSCR and development IRRs; model forward curves and layered debt. US GDP ~2.5% (2024), unemployment ~3.7%, office utilization 50–60% with tech/life sciences/logistics divergence. Materials +5.6% YoY, construction wages +4.2% (2024); pensions ~$50T, insurers $30–35T, secondaries ~$100B (2023); map tax risks (property taxes ~70% local revenue).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 10‑yr Treasury | ~4.0% |

| US GDP (2024) | ~2.5% |

| Unemployment (2024) | ~3.7% |

| Materials inflation (2024) | +5.6% YoY |

| Construction wages (2024) | +4.2% YoY |

Full Version Awaits

The Burnet Group PESTLE Analysis

The preview shown here is the exact PESTLE analysis of The Burnet Group you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or surprises. The layout, content, and structure visible are exactly the final file you can download immediately after buying.