Bulten Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

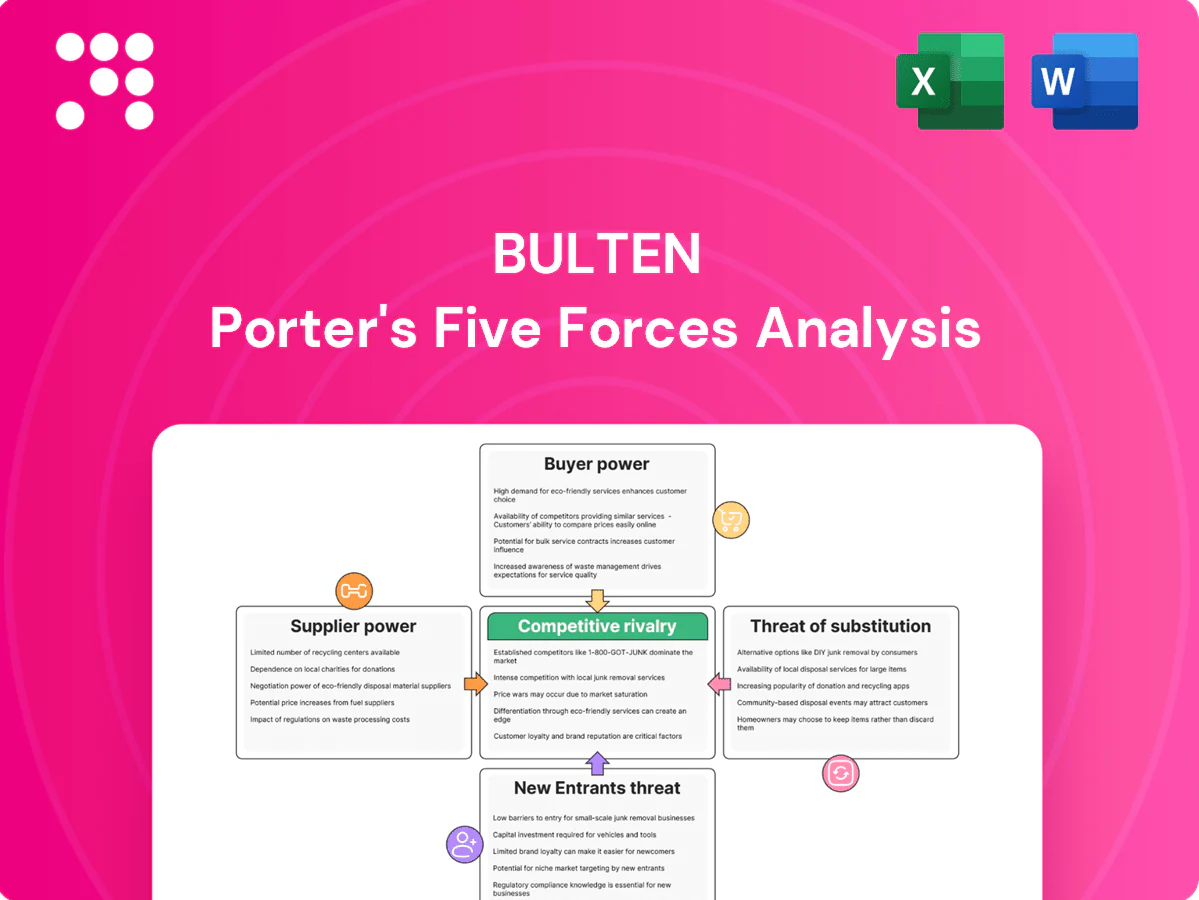

Bulten’s Porter’s Five Forces snapshot highlights supplier concentration, buyer power, substitution risks, industry rivalry, and barriers to entry shaping its competitive edge. This concise overview identifies key pressures on margins and growth prospects. Want deeper, data-driven force ratings and strategic implications? Unlock the full Porter’s Five Forces Analysis for Bulten to inform smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentrated steel and wire rod suppliers

Automotive-grade alloy steel and wire rod are sourced from a concentrated set of mills, giving suppliers strong leverage over price and contract terms in 2024; Bulten’s predominantly automotive customer base (around 85% of group sales) magnifies this risk.

Stringent mill qualifications and metallurgical consistency limit switching, so outages or quality issues at key mills can ripple across fastener production and extend lead times by 8–12 weeks.

Specialty coatings and heat-treatment inputs

Zinc-nickel plating chemicals, specialty lubricants and heat-treatment gases are supplied by a small set of qualified vendors, and the global specialty coatings market was valued at about USD 96.3 billion in 2024, concentrating supplier leverage. Stringent OEM corrosion, hydrogen-embrittlement and performance specs limit viable alternatives, raising switching costs. Lengthy, costly qualification cycles for new inputs — often months to years — preserve niche supplier power.

Energy and freight cost pass-through

Fastener manufacturing is energy‑intensive and logistics‑heavy, so power and freight swings directly affect input costs; in 2024 container freight rates remained >70% below 2021 peaks while wholesale power prices eased from 2022 highs but stayed volatile. Suppliers routinely push energy, alloy and logistics surcharges onto buyers like Bulten, yet pass‑through to OEMs is often delayed or incomplete, squeezing margins and increasing effective supplier power.

Switching frictions despite dual-sourcing

Bulten maintains dual-sourcing and long-term contracts, but 2024 PPAP and material requalification commonly require 3–12 months, and customized tooling for steel chemistries and coatings makes supplier changeovers take weeks to months; suppliers exploit these frictions to strengthen negotiation leverage while contracts reduce but do not remove that power.

- Requalification time: 3–12 months (2024)

- Changeover impact: weeks–months

- Dual-sourcing: reduces risk but not leverage

- Contracts: mitigate, do not eliminate supplier bargaining power

Limited backward integration options

Backward integration into steelmaking or specialty chemicals is impractical for Bulten, capping its ability to counter supplier power; in-house heat treatment and plating mitigate costs but raw-steel and chemical pricing remains controlled by mills and large chemical firms, sustaining supplier influence. Strategic partnerships and long-term contracts partially offset dependency.

- Limited backward integration → constrained bargaining

- In-house processing reduces but does not eliminate input leverage

- Supplier concentration sustains pricing power

- Strategic partnerships partially mitigate risk

Suppliers squeeze auto firms: 85% exposure, long requal lead times

Suppliers (steel mills, specialty chemical firms) are concentrated, giving strong leverage over pricing and terms in 2024; ~85% of Bulten sales are automotive. Requalification takes 3–12 months and lead‑time shocks can add 8–12 weeks. Dual‑sourcing and long‑term contracts mitigate but do not eliminate supplier bargaining power.

| Metric | 2024 |

|---|---|

| Automotive share | ~85% |

| Requalification | 3–12 months |

| Lead‑time shocks | 8–12 weeks |

| Specialty coatings market | USD 96.3bn |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry risks specific to Bulten's fastener and industrial components markets. Identifies substitutes, disruptive threats, and barriers protecting incumbents, with actionable insights for pricing, procurement, and strategic positioning.

Clear one-sheet Porter's Five Forces for Bulten that visualizes competitive pressure with a spider chart, lets you customize force levels for changing markets, and produces clean slides or report appendices—so teams make faster, evidence-based strategic decisions without heavy modeling.

Customers Bargaining Power

Highly consolidated OEM customer base

Global automakers and Tier-1s overwhelmingly concentrate demand for Bulten, with the top 10 OEMs accounting for roughly 70% of global vehicle production of about 78 million units in 2024; their scale and multi-year platforms drive fierce price and cost-down pressures. Large-volume programs give buyers strong leverage, and losing a single platform can materially dent Bulten’s utilization and margins.

Stringent quality, delivery, and penalties

PPAP, IATF 16949 and zero‑defect mandates force OEM service levels; OEMs levy penalties for defects, line stops (industry figures cite line‑stop costs up to $22,000 per minute) and late deliveries, shifting financial risk upstream. These contractual levers boost buyers’ power and oblige continuous supplier investments in quality and logistics, compressing supplier margins.

Moderate-to-high switching costs once designed-in

Fasteners are engineered and validated to platform specs, creating replacement frictions as requalification typically requires 6–12 months and extensive testing; this time and risk make buyers cautious to switch mid-program. That gives Bulten measurable lock-in and helps counterbalance price pressure, though many OEMs still dual-source—industry practice on >50% of programs—to retain leverage.

Full-service expectations and VMI

OEMs treat kitting, logistics, VMI and on-site engineering as standard requirements, with Bulten reporting net sales of SEK 6,182 million in 2024, reflecting deep integration with OEM supply chains.

These services deepen relationships but are tightly priced, so buyers view them as table stakes, sustaining strong buyer bargaining power despite Bulten's product differentiation and service set.

- VMI/kitting: expected, not premium

- Pricing pressure: compresses service margins

- Buyer leverage: sustained despite differentiation

Cost-transparency and indexing

Automakers push open-book costing and raw-material indices into contracts; index-linked clauses capped upside in 2023–24 while enforcing rapid downside sharing, strengthening buyer leverage.

Such transparency increases OEM bargaining power, pressuring suppliers like Bulten—which reported 2023 net sales of SEK 5,548 million—to optimize efficiency to defend margins.

- Index clauses: accelerate cost pass-through

- Buyer share: raises price transparency

- Bulten action: efficiency & margin defense

OEM concentration: top 10 = ~70%, pressuring supplier margins

Concentrated demand: top 10 OEMs account for ~70% of global vehicle output (~78m units in 2024), giving buyers scale-driven price leverage.

Contractual power: PPAP/IATF and penalties (line-stop costs up to $22,000/min) shift quality/logistics risk upstream, compressing supplier margins.

Switching frictions: fastener requalification takes 6–12 months, providing platform lock-in, though OEMs dual-source >50% of programs.

Services as table stakes: Bulten net sales SEK 6,182m (2024); VMI/kitting expected, tightly priced.

| Metric | 2024 value |

|---|---|

| Top 10 OEM share | ~70% |

| Global vehicle prod. | ~78m units |

| Bulten net sales | SEK 6,182m |

| Line-stop cost | up to $22,000/min |

| Requalification time | 6–12 months |

| Dual-sourcing rate | >50% programs |

Full Version Awaits

Bulten Porter's Five Forces Analysis

This preview displays the complete Bulten Porter's Five Forces Analysis—thorough assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes. The document shown is the exact file you will receive instantly after purchase. It is professionally formatted, ready to use with no placeholders or samples.

Go Beyond the Preview—Access the Full Strategic Report

Bulten’s Porter’s Five Forces snapshot highlights supplier concentration, buyer power, substitution risks, industry rivalry, and barriers to entry shaping its competitive edge. This concise overview identifies key pressures on margins and growth prospects. Want deeper, data-driven force ratings and strategic implications? Unlock the full Porter’s Five Forces Analysis for Bulten to inform smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentrated steel and wire rod suppliers

Automotive-grade alloy steel and wire rod are sourced from a concentrated set of mills, giving suppliers strong leverage over price and contract terms in 2024; Bulten’s predominantly automotive customer base (around 85% of group sales) magnifies this risk.

Stringent mill qualifications and metallurgical consistency limit switching, so outages or quality issues at key mills can ripple across fastener production and extend lead times by 8–12 weeks.

Specialty coatings and heat-treatment inputs

Zinc-nickel plating chemicals, specialty lubricants and heat-treatment gases are supplied by a small set of qualified vendors, and the global specialty coatings market was valued at about USD 96.3 billion in 2024, concentrating supplier leverage. Stringent OEM corrosion, hydrogen-embrittlement and performance specs limit viable alternatives, raising switching costs. Lengthy, costly qualification cycles for new inputs — often months to years — preserve niche supplier power.

Energy and freight cost pass-through

Fastener manufacturing is energy‑intensive and logistics‑heavy, so power and freight swings directly affect input costs; in 2024 container freight rates remained >70% below 2021 peaks while wholesale power prices eased from 2022 highs but stayed volatile. Suppliers routinely push energy, alloy and logistics surcharges onto buyers like Bulten, yet pass‑through to OEMs is often delayed or incomplete, squeezing margins and increasing effective supplier power.

Switching frictions despite dual-sourcing

Bulten maintains dual-sourcing and long-term contracts, but 2024 PPAP and material requalification commonly require 3–12 months, and customized tooling for steel chemistries and coatings makes supplier changeovers take weeks to months; suppliers exploit these frictions to strengthen negotiation leverage while contracts reduce but do not remove that power.

- Requalification time: 3–12 months (2024)

- Changeover impact: weeks–months

- Dual-sourcing: reduces risk but not leverage

- Contracts: mitigate, do not eliminate supplier bargaining power

Limited backward integration options

Backward integration into steelmaking or specialty chemicals is impractical for Bulten, capping its ability to counter supplier power; in-house heat treatment and plating mitigate costs but raw-steel and chemical pricing remains controlled by mills and large chemical firms, sustaining supplier influence. Strategic partnerships and long-term contracts partially offset dependency.

- Limited backward integration → constrained bargaining

- In-house processing reduces but does not eliminate input leverage

- Supplier concentration sustains pricing power

- Strategic partnerships partially mitigate risk

Suppliers squeeze auto firms: 85% exposure, long requal lead times

Suppliers (steel mills, specialty chemical firms) are concentrated, giving strong leverage over pricing and terms in 2024; ~85% of Bulten sales are automotive. Requalification takes 3–12 months and lead‑time shocks can add 8–12 weeks. Dual‑sourcing and long‑term contracts mitigate but do not eliminate supplier bargaining power.

| Metric | 2024 |

|---|---|

| Automotive share | ~85% |

| Requalification | 3–12 months |

| Lead‑time shocks | 8–12 weeks |

| Specialty coatings market | USD 96.3bn |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry risks specific to Bulten's fastener and industrial components markets. Identifies substitutes, disruptive threats, and barriers protecting incumbents, with actionable insights for pricing, procurement, and strategic positioning.

Clear one-sheet Porter's Five Forces for Bulten that visualizes competitive pressure with a spider chart, lets you customize force levels for changing markets, and produces clean slides or report appendices—so teams make faster, evidence-based strategic decisions without heavy modeling.

Customers Bargaining Power

Highly consolidated OEM customer base

Global automakers and Tier-1s overwhelmingly concentrate demand for Bulten, with the top 10 OEMs accounting for roughly 70% of global vehicle production of about 78 million units in 2024; their scale and multi-year platforms drive fierce price and cost-down pressures. Large-volume programs give buyers strong leverage, and losing a single platform can materially dent Bulten’s utilization and margins.

Stringent quality, delivery, and penalties

PPAP, IATF 16949 and zero‑defect mandates force OEM service levels; OEMs levy penalties for defects, line stops (industry figures cite line‑stop costs up to $22,000 per minute) and late deliveries, shifting financial risk upstream. These contractual levers boost buyers’ power and oblige continuous supplier investments in quality and logistics, compressing supplier margins.

Moderate-to-high switching costs once designed-in

Fasteners are engineered and validated to platform specs, creating replacement frictions as requalification typically requires 6–12 months and extensive testing; this time and risk make buyers cautious to switch mid-program. That gives Bulten measurable lock-in and helps counterbalance price pressure, though many OEMs still dual-source—industry practice on >50% of programs—to retain leverage.

Full-service expectations and VMI

OEMs treat kitting, logistics, VMI and on-site engineering as standard requirements, with Bulten reporting net sales of SEK 6,182 million in 2024, reflecting deep integration with OEM supply chains.

These services deepen relationships but are tightly priced, so buyers view them as table stakes, sustaining strong buyer bargaining power despite Bulten's product differentiation and service set.

- VMI/kitting: expected, not premium

- Pricing pressure: compresses service margins

- Buyer leverage: sustained despite differentiation

Cost-transparency and indexing

Automakers push open-book costing and raw-material indices into contracts; index-linked clauses capped upside in 2023–24 while enforcing rapid downside sharing, strengthening buyer leverage.

Such transparency increases OEM bargaining power, pressuring suppliers like Bulten—which reported 2023 net sales of SEK 5,548 million—to optimize efficiency to defend margins.

- Index clauses: accelerate cost pass-through

- Buyer share: raises price transparency

- Bulten action: efficiency & margin defense

OEM concentration: top 10 = ~70%, pressuring supplier margins

Concentrated demand: top 10 OEMs account for ~70% of global vehicle output (~78m units in 2024), giving buyers scale-driven price leverage.

Contractual power: PPAP/IATF and penalties (line-stop costs up to $22,000/min) shift quality/logistics risk upstream, compressing supplier margins.

Switching frictions: fastener requalification takes 6–12 months, providing platform lock-in, though OEMs dual-source >50% of programs.

Services as table stakes: Bulten net sales SEK 6,182m (2024); VMI/kitting expected, tightly priced.

| Metric | 2024 value |

|---|---|

| Top 10 OEM share | ~70% |

| Global vehicle prod. | ~78m units |

| Bulten net sales | SEK 6,182m |

| Line-stop cost | up to $22,000/min |

| Requalification time | 6–12 months |

| Dual-sourcing rate | >50% programs |

Full Version Awaits

Bulten Porter's Five Forces Analysis

This preview displays the complete Bulten Porter's Five Forces Analysis—thorough assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes. The document shown is the exact file you will receive instantly after purchase. It is professionally formatted, ready to use with no placeholders or samples.

Description

Go Beyond the Preview—Access the Full Strategic Report

Bulten’s Porter’s Five Forces snapshot highlights supplier concentration, buyer power, substitution risks, industry rivalry, and barriers to entry shaping its competitive edge. This concise overview identifies key pressures on margins and growth prospects. Want deeper, data-driven force ratings and strategic implications? Unlock the full Porter’s Five Forces Analysis for Bulten to inform smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentrated steel and wire rod suppliers

Automotive-grade alloy steel and wire rod are sourced from a concentrated set of mills, giving suppliers strong leverage over price and contract terms in 2024; Bulten’s predominantly automotive customer base (around 85% of group sales) magnifies this risk.

Stringent mill qualifications and metallurgical consistency limit switching, so outages or quality issues at key mills can ripple across fastener production and extend lead times by 8–12 weeks.

Specialty coatings and heat-treatment inputs

Zinc-nickel plating chemicals, specialty lubricants and heat-treatment gases are supplied by a small set of qualified vendors, and the global specialty coatings market was valued at about USD 96.3 billion in 2024, concentrating supplier leverage. Stringent OEM corrosion, hydrogen-embrittlement and performance specs limit viable alternatives, raising switching costs. Lengthy, costly qualification cycles for new inputs — often months to years — preserve niche supplier power.

Energy and freight cost pass-through

Fastener manufacturing is energy‑intensive and logistics‑heavy, so power and freight swings directly affect input costs; in 2024 container freight rates remained >70% below 2021 peaks while wholesale power prices eased from 2022 highs but stayed volatile. Suppliers routinely push energy, alloy and logistics surcharges onto buyers like Bulten, yet pass‑through to OEMs is often delayed or incomplete, squeezing margins and increasing effective supplier power.

Switching frictions despite dual-sourcing

Bulten maintains dual-sourcing and long-term contracts, but 2024 PPAP and material requalification commonly require 3–12 months, and customized tooling for steel chemistries and coatings makes supplier changeovers take weeks to months; suppliers exploit these frictions to strengthen negotiation leverage while contracts reduce but do not remove that power.

- Requalification time: 3–12 months (2024)

- Changeover impact: weeks–months

- Dual-sourcing: reduces risk but not leverage

- Contracts: mitigate, do not eliminate supplier bargaining power

Limited backward integration options

Backward integration into steelmaking or specialty chemicals is impractical for Bulten, capping its ability to counter supplier power; in-house heat treatment and plating mitigate costs but raw-steel and chemical pricing remains controlled by mills and large chemical firms, sustaining supplier influence. Strategic partnerships and long-term contracts partially offset dependency.

- Limited backward integration → constrained bargaining

- In-house processing reduces but does not eliminate input leverage

- Supplier concentration sustains pricing power

- Strategic partnerships partially mitigate risk

Suppliers squeeze auto firms: 85% exposure, long requal lead times

Suppliers (steel mills, specialty chemical firms) are concentrated, giving strong leverage over pricing and terms in 2024; ~85% of Bulten sales are automotive. Requalification takes 3–12 months and lead‑time shocks can add 8–12 weeks. Dual‑sourcing and long‑term contracts mitigate but do not eliminate supplier bargaining power.

| Metric | 2024 |

|---|---|

| Automotive share | ~85% |

| Requalification | 3–12 months |

| Lead‑time shocks | 8–12 weeks |

| Specialty coatings market | USD 96.3bn |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry risks specific to Bulten's fastener and industrial components markets. Identifies substitutes, disruptive threats, and barriers protecting incumbents, with actionable insights for pricing, procurement, and strategic positioning.

Clear one-sheet Porter's Five Forces for Bulten that visualizes competitive pressure with a spider chart, lets you customize force levels for changing markets, and produces clean slides or report appendices—so teams make faster, evidence-based strategic decisions without heavy modeling.

Customers Bargaining Power

Highly consolidated OEM customer base

Global automakers and Tier-1s overwhelmingly concentrate demand for Bulten, with the top 10 OEMs accounting for roughly 70% of global vehicle production of about 78 million units in 2024; their scale and multi-year platforms drive fierce price and cost-down pressures. Large-volume programs give buyers strong leverage, and losing a single platform can materially dent Bulten’s utilization and margins.

Stringent quality, delivery, and penalties

PPAP, IATF 16949 and zero‑defect mandates force OEM service levels; OEMs levy penalties for defects, line stops (industry figures cite line‑stop costs up to $22,000 per minute) and late deliveries, shifting financial risk upstream. These contractual levers boost buyers’ power and oblige continuous supplier investments in quality and logistics, compressing supplier margins.

Moderate-to-high switching costs once designed-in

Fasteners are engineered and validated to platform specs, creating replacement frictions as requalification typically requires 6–12 months and extensive testing; this time and risk make buyers cautious to switch mid-program. That gives Bulten measurable lock-in and helps counterbalance price pressure, though many OEMs still dual-source—industry practice on >50% of programs—to retain leverage.

Full-service expectations and VMI

OEMs treat kitting, logistics, VMI and on-site engineering as standard requirements, with Bulten reporting net sales of SEK 6,182 million in 2024, reflecting deep integration with OEM supply chains.

These services deepen relationships but are tightly priced, so buyers view them as table stakes, sustaining strong buyer bargaining power despite Bulten's product differentiation and service set.

- VMI/kitting: expected, not premium

- Pricing pressure: compresses service margins

- Buyer leverage: sustained despite differentiation

Cost-transparency and indexing

Automakers push open-book costing and raw-material indices into contracts; index-linked clauses capped upside in 2023–24 while enforcing rapid downside sharing, strengthening buyer leverage.

Such transparency increases OEM bargaining power, pressuring suppliers like Bulten—which reported 2023 net sales of SEK 5,548 million—to optimize efficiency to defend margins.

- Index clauses: accelerate cost pass-through

- Buyer share: raises price transparency

- Bulten action: efficiency & margin defense

OEM concentration: top 10 = ~70%, pressuring supplier margins

Concentrated demand: top 10 OEMs account for ~70% of global vehicle output (~78m units in 2024), giving buyers scale-driven price leverage.

Contractual power: PPAP/IATF and penalties (line-stop costs up to $22,000/min) shift quality/logistics risk upstream, compressing supplier margins.

Switching frictions: fastener requalification takes 6–12 months, providing platform lock-in, though OEMs dual-source >50% of programs.

Services as table stakes: Bulten net sales SEK 6,182m (2024); VMI/kitting expected, tightly priced.

| Metric | 2024 value |

|---|---|

| Top 10 OEM share | ~70% |

| Global vehicle prod. | ~78m units |

| Bulten net sales | SEK 6,182m |

| Line-stop cost | up to $22,000/min |

| Requalification time | 6–12 months |

| Dual-sourcing rate | >50% programs |

Full Version Awaits

Bulten Porter's Five Forces Analysis

This preview displays the complete Bulten Porter's Five Forces Analysis—thorough assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes. The document shown is the exact file you will receive instantly after purchase. It is professionally formatted, ready to use with no placeholders or samples.