BuzzFeed Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

BuzzFeed faces intense competitive rivalry in digital media, reliance on ad revenue and platforms increases supplier and buyer power, and low switching costs plus rising content substitutes heighten threat levels; network effects and brand scale offer some defense. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Platform gatekeepers

Distribution depends on Google, YouTube, Meta, TikTok and Apple, which together drove well over 70% of publisher referral and ad inventory in 2024, concentrating supplier power. Algorithm changes have cut publisher traffic and video views by as much as 50% in documented cases, slashing ad yield. Platform revenue‑share terms (eg App Store 30% standard) remain take‑it‑or‑leave‑it, and BuzzFeed lacks exclusive, must‑have assets to force better deals.

Cloud and adtech stack

Dependence on CDN, cloud, DSP/SSP and measurement vendors creates switching costs for BuzzFeed: in 2024 AWS, Azure and GCP controlled roughly 33%, 22% and 12% of cloud market respectively (Synergy Research), while programmatic accounted for about 86% of US display spend (eMarketer), concentrating supplier power. Fee structures and policy shifts from those vendors can compress ad margins and enforcement or outages can halt monetization. Multi-vendor strategies mitigate supplier risk but increase integration complexity and operating cost.

Creative and freelance talent

Writers, video producers and influencers with followings above 1 million command premium rates and stronger negotiation leverage. Talent can exit to independent channels or platforms, raising replacement and audience-reacquisition costs. The 2023 WGA strike (May–Sept 2023) highlighted rising unionization pressures that affect flexibility and expense. Investing in in-house brands reduces individual leverage but requires significant upfront cost.

Licensing and content sources

Agencies, music rights holders, stock media vendors and newswires control key inputs for BuzzFeed, and rights fees plus usage restrictions in 2024 slowed production and raised costs, while takedowns or disputes threaten back-catalog revenue.

- Suppliers: agencies, labels, stock libraries, newswires

- Effects: fees, usage limits, takedown risk on legacy content

- Tradeoff: owning IP reduces exposure but demands high capital

Data and measurement providers

Data and measurement providers (audience, attribution, brand safety) materially shape BuzzFeed sell-through and CPMs; attribution and brand-safety vendor downgrades can cut inventory value by 10–30% and disrupt buyer demand. Methodology shifts and privacy (IDFA/ATT) reduced addressability to ~10–15% by 2024, forcing retooling and incremental tech spend. Expanded first-party data and identity partnerships partially offset supplier power.

Platforms capture > 70% referrals; addressability ~10-15%

Supplier power is high: Google/Meta/TikTok/Apple drove >70% of publisher referrals and ad inventory in 2024, algorithm shifts cut traffic up to 50% and attribution/privacy (ATT) cut addressability to ~10–15%, lowering CPMs 10–30%. Cloud and programmatic concentration (AWS 33%, Azure 22%, GCP 12%; programmatic ~86% US display) raise switching costs; top creators command premium rates.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Platforms | >70% referrals | High leverage |

| Cloud | AWS33%/Azure22%/GCP12% | Switching cost |

| Programmatic | ~86% US display | Revenue pressure |

What is included in the product

Concise Porter's Five Forces review tailored to BuzzFeed, uncovering competitive intensity, buyer/supplier leverage, substitute threats, and entry barriers, with strategic commentary on disruptive digital media trends and implications for pricing, profitability, and market positioning.

A concise Porter's Five Forces for BuzzFeed that turns competitive complexity into actionable strategy—adjust pressure sliders, export-ready radar charts, and copy-ready layouts to speed boardroom decisions and refocus content, ad, and distribution priorities.

Customers Bargaining Power

Advertisers and agencies

Large brands and holding companies secure volume discounts and performance guarantees with publishers, and can reallocate budgets quickly across platforms—US digital ad spend reached about 262.5 billion USD in 2024, amplifying their leverage. Standardized metrics (viewability, iAB benchmarks) heighten comparability and price pressure, while deep agency relationships and BuzzFeed's proprietary formats can blunt demands.

Programmatic buyers

Open-exchange programmatic buyers benchmark CPMs across thousands of sites, driving downward pressure; programmatic made up roughly 86% of US display ad spend in 2024, increasing buyers’ leverage. Header bidding intensifies price competition by surfacing bids across SSPs. Brand-safety filters reduce demand for sensitive content, while private marketplaces and contextual deals boost yield and CPMs for vetted inventory.

Audience multi-homing

Consumers freely switch among countless content sources as 5.34 billion people used the internet in 2024, making multi-homing the norm; low switching costs erode loyalty to any single publisher. Engagement must be re-earned each session, driving higher paid and creative acquisition spend. Strong franchises and communities measurably boost retention and lifetime value.

Performance accountability

Buyers in 2024 pressed BuzzFeed for clear ROI, viewability, and incremental lift, cutting underperforming placements quickly and shortening cycles to weeks, which raises revenue volatility; creative studios and commerce tie-ins allowed BuzzFeed to command premiums on higher-performing packages.

- ROI-driven buying

- Rapid cutoffs

- Short cycles = volatility

- Studios/commerce = premium

Privacy and compliance demands

Buyers demand consented data and compliant targeting, and 2024 surveys show 58% of marketers report reduced addressability after signal loss, pressuring CPMs and bidding transparency. Clean room and first‑party solutions raise cost to serve, increasing integration and measurement spend. Clear, auditable reporting—attribution and viewability—helps preserve advertiser spend despite targeting constraints.

- consented data required

- 58% report lower addressability (2024)

- clean rooms raise cost to serve

- transparent reporting preserves spend

Buyers leverage: US digital ad spend 262.5B, programmatic ~86%

Buyers hold strong leverage: US digital ad spend hit 262.5B in 2024 and programmatic was ~86%, enabling price benchmarking and rapid reallocations. Low switching costs (5.34B internet users) and ROI demands (58% report lower addressability) force short cycles and volatility, though studios/commerce and first‑party solutions can secure premiums.

| Metric | 2024 Value |

|---|---|

| US digital ad spend | 262.5B USD |

| Programmatic share | ~86% |

| Global internet users | 5.34B |

| Marketers reporting lower addressability | 58% |

What You See Is What You Get

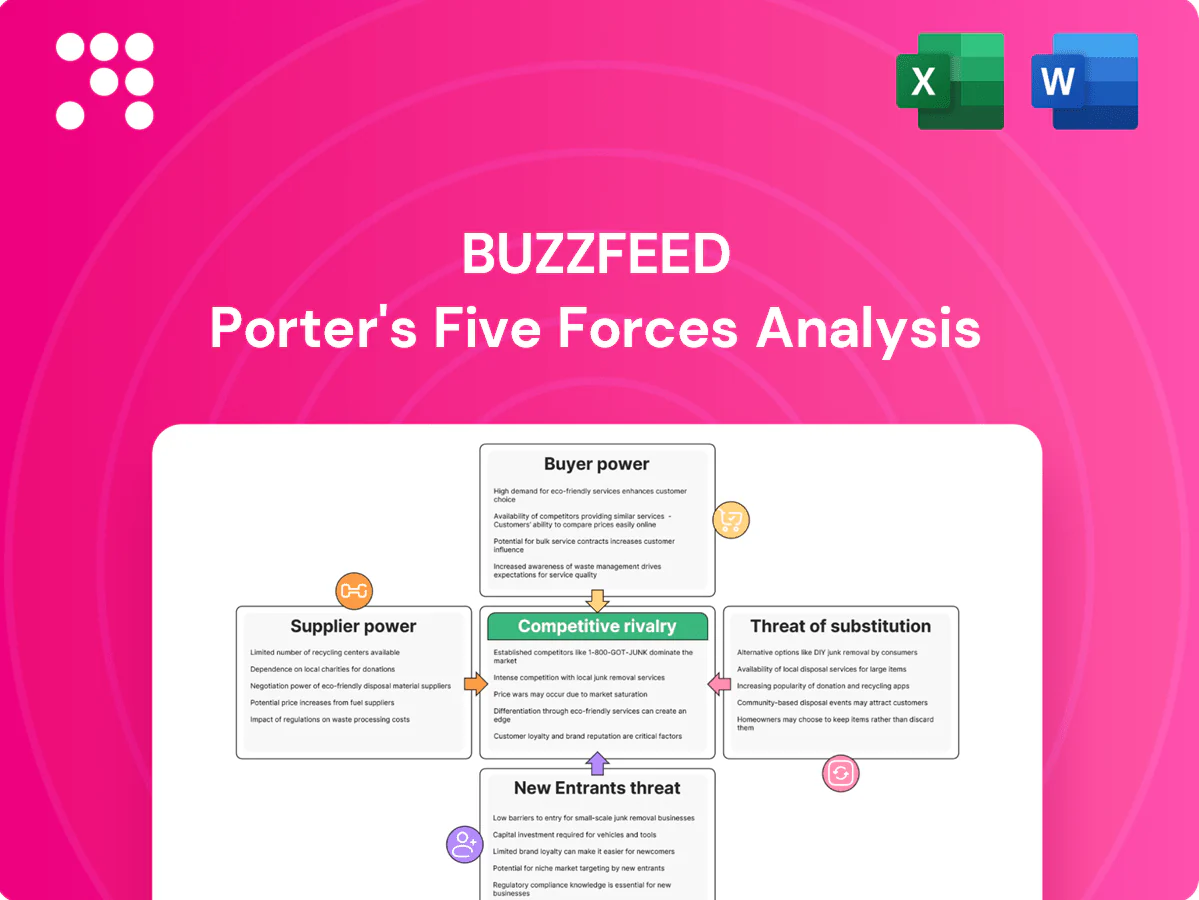

BuzzFeed Porter's Five Forces Analysis

This preview shows the exact BuzzFeed Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. It presents competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications in a ready-to-use format. After purchase you get this fully formatted file instantly.

Go Beyond the Preview—Access the Full Strategic Report

BuzzFeed faces intense competitive rivalry in digital media, reliance on ad revenue and platforms increases supplier and buyer power, and low switching costs plus rising content substitutes heighten threat levels; network effects and brand scale offer some defense. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Platform gatekeepers

Distribution depends on Google, YouTube, Meta, TikTok and Apple, which together drove well over 70% of publisher referral and ad inventory in 2024, concentrating supplier power. Algorithm changes have cut publisher traffic and video views by as much as 50% in documented cases, slashing ad yield. Platform revenue‑share terms (eg App Store 30% standard) remain take‑it‑or‑leave‑it, and BuzzFeed lacks exclusive, must‑have assets to force better deals.

Cloud and adtech stack

Dependence on CDN, cloud, DSP/SSP and measurement vendors creates switching costs for BuzzFeed: in 2024 AWS, Azure and GCP controlled roughly 33%, 22% and 12% of cloud market respectively (Synergy Research), while programmatic accounted for about 86% of US display spend (eMarketer), concentrating supplier power. Fee structures and policy shifts from those vendors can compress ad margins and enforcement or outages can halt monetization. Multi-vendor strategies mitigate supplier risk but increase integration complexity and operating cost.

Creative and freelance talent

Writers, video producers and influencers with followings above 1 million command premium rates and stronger negotiation leverage. Talent can exit to independent channels or platforms, raising replacement and audience-reacquisition costs. The 2023 WGA strike (May–Sept 2023) highlighted rising unionization pressures that affect flexibility and expense. Investing in in-house brands reduces individual leverage but requires significant upfront cost.

Licensing and content sources

Agencies, music rights holders, stock media vendors and newswires control key inputs for BuzzFeed, and rights fees plus usage restrictions in 2024 slowed production and raised costs, while takedowns or disputes threaten back-catalog revenue.

- Suppliers: agencies, labels, stock libraries, newswires

- Effects: fees, usage limits, takedown risk on legacy content

- Tradeoff: owning IP reduces exposure but demands high capital

Data and measurement providers

Data and measurement providers (audience, attribution, brand safety) materially shape BuzzFeed sell-through and CPMs; attribution and brand-safety vendor downgrades can cut inventory value by 10–30% and disrupt buyer demand. Methodology shifts and privacy (IDFA/ATT) reduced addressability to ~10–15% by 2024, forcing retooling and incremental tech spend. Expanded first-party data and identity partnerships partially offset supplier power.

Platforms capture > 70% referrals; addressability ~10-15%

Supplier power is high: Google/Meta/TikTok/Apple drove >70% of publisher referrals and ad inventory in 2024, algorithm shifts cut traffic up to 50% and attribution/privacy (ATT) cut addressability to ~10–15%, lowering CPMs 10–30%. Cloud and programmatic concentration (AWS 33%, Azure 22%, GCP 12%; programmatic ~86% US display) raise switching costs; top creators command premium rates.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Platforms | >70% referrals | High leverage |

| Cloud | AWS33%/Azure22%/GCP12% | Switching cost |

| Programmatic | ~86% US display | Revenue pressure |

What is included in the product

Concise Porter's Five Forces review tailored to BuzzFeed, uncovering competitive intensity, buyer/supplier leverage, substitute threats, and entry barriers, with strategic commentary on disruptive digital media trends and implications for pricing, profitability, and market positioning.

A concise Porter's Five Forces for BuzzFeed that turns competitive complexity into actionable strategy—adjust pressure sliders, export-ready radar charts, and copy-ready layouts to speed boardroom decisions and refocus content, ad, and distribution priorities.

Customers Bargaining Power

Advertisers and agencies

Large brands and holding companies secure volume discounts and performance guarantees with publishers, and can reallocate budgets quickly across platforms—US digital ad spend reached about 262.5 billion USD in 2024, amplifying their leverage. Standardized metrics (viewability, iAB benchmarks) heighten comparability and price pressure, while deep agency relationships and BuzzFeed's proprietary formats can blunt demands.

Programmatic buyers

Open-exchange programmatic buyers benchmark CPMs across thousands of sites, driving downward pressure; programmatic made up roughly 86% of US display ad spend in 2024, increasing buyers’ leverage. Header bidding intensifies price competition by surfacing bids across SSPs. Brand-safety filters reduce demand for sensitive content, while private marketplaces and contextual deals boost yield and CPMs for vetted inventory.

Audience multi-homing

Consumers freely switch among countless content sources as 5.34 billion people used the internet in 2024, making multi-homing the norm; low switching costs erode loyalty to any single publisher. Engagement must be re-earned each session, driving higher paid and creative acquisition spend. Strong franchises and communities measurably boost retention and lifetime value.

Performance accountability

Buyers in 2024 pressed BuzzFeed for clear ROI, viewability, and incremental lift, cutting underperforming placements quickly and shortening cycles to weeks, which raises revenue volatility; creative studios and commerce tie-ins allowed BuzzFeed to command premiums on higher-performing packages.

- ROI-driven buying

- Rapid cutoffs

- Short cycles = volatility

- Studios/commerce = premium

Privacy and compliance demands

Buyers demand consented data and compliant targeting, and 2024 surveys show 58% of marketers report reduced addressability after signal loss, pressuring CPMs and bidding transparency. Clean room and first‑party solutions raise cost to serve, increasing integration and measurement spend. Clear, auditable reporting—attribution and viewability—helps preserve advertiser spend despite targeting constraints.

- consented data required

- 58% report lower addressability (2024)

- clean rooms raise cost to serve

- transparent reporting preserves spend

Buyers leverage: US digital ad spend 262.5B, programmatic ~86%

Buyers hold strong leverage: US digital ad spend hit 262.5B in 2024 and programmatic was ~86%, enabling price benchmarking and rapid reallocations. Low switching costs (5.34B internet users) and ROI demands (58% report lower addressability) force short cycles and volatility, though studios/commerce and first‑party solutions can secure premiums.

| Metric | 2024 Value |

|---|---|

| US digital ad spend | 262.5B USD |

| Programmatic share | ~86% |

| Global internet users | 5.34B |

| Marketers reporting lower addressability | 58% |

What You See Is What You Get

BuzzFeed Porter's Five Forces Analysis

This preview shows the exact BuzzFeed Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. It presents competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications in a ready-to-use format. After purchase you get this fully formatted file instantly.

Description

Go Beyond the Preview—Access the Full Strategic Report

BuzzFeed faces intense competitive rivalry in digital media, reliance on ad revenue and platforms increases supplier and buyer power, and low switching costs plus rising content substitutes heighten threat levels; network effects and brand scale offer some defense. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Platform gatekeepers

Distribution depends on Google, YouTube, Meta, TikTok and Apple, which together drove well over 70% of publisher referral and ad inventory in 2024, concentrating supplier power. Algorithm changes have cut publisher traffic and video views by as much as 50% in documented cases, slashing ad yield. Platform revenue‑share terms (eg App Store 30% standard) remain take‑it‑or‑leave‑it, and BuzzFeed lacks exclusive, must‑have assets to force better deals.

Cloud and adtech stack

Dependence on CDN, cloud, DSP/SSP and measurement vendors creates switching costs for BuzzFeed: in 2024 AWS, Azure and GCP controlled roughly 33%, 22% and 12% of cloud market respectively (Synergy Research), while programmatic accounted for about 86% of US display spend (eMarketer), concentrating supplier power. Fee structures and policy shifts from those vendors can compress ad margins and enforcement or outages can halt monetization. Multi-vendor strategies mitigate supplier risk but increase integration complexity and operating cost.

Creative and freelance talent

Writers, video producers and influencers with followings above 1 million command premium rates and stronger negotiation leverage. Talent can exit to independent channels or platforms, raising replacement and audience-reacquisition costs. The 2023 WGA strike (May–Sept 2023) highlighted rising unionization pressures that affect flexibility and expense. Investing in in-house brands reduces individual leverage but requires significant upfront cost.

Licensing and content sources

Agencies, music rights holders, stock media vendors and newswires control key inputs for BuzzFeed, and rights fees plus usage restrictions in 2024 slowed production and raised costs, while takedowns or disputes threaten back-catalog revenue.

- Suppliers: agencies, labels, stock libraries, newswires

- Effects: fees, usage limits, takedown risk on legacy content

- Tradeoff: owning IP reduces exposure but demands high capital

Data and measurement providers

Data and measurement providers (audience, attribution, brand safety) materially shape BuzzFeed sell-through and CPMs; attribution and brand-safety vendor downgrades can cut inventory value by 10–30% and disrupt buyer demand. Methodology shifts and privacy (IDFA/ATT) reduced addressability to ~10–15% by 2024, forcing retooling and incremental tech spend. Expanded first-party data and identity partnerships partially offset supplier power.

Platforms capture > 70% referrals; addressability ~10-15%

Supplier power is high: Google/Meta/TikTok/Apple drove >70% of publisher referrals and ad inventory in 2024, algorithm shifts cut traffic up to 50% and attribution/privacy (ATT) cut addressability to ~10–15%, lowering CPMs 10–30%. Cloud and programmatic concentration (AWS 33%, Azure 22%, GCP 12%; programmatic ~86% US display) raise switching costs; top creators command premium rates.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Platforms | >70% referrals | High leverage |

| Cloud | AWS33%/Azure22%/GCP12% | Switching cost |

| Programmatic | ~86% US display | Revenue pressure |

What is included in the product

Concise Porter's Five Forces review tailored to BuzzFeed, uncovering competitive intensity, buyer/supplier leverage, substitute threats, and entry barriers, with strategic commentary on disruptive digital media trends and implications for pricing, profitability, and market positioning.

A concise Porter's Five Forces for BuzzFeed that turns competitive complexity into actionable strategy—adjust pressure sliders, export-ready radar charts, and copy-ready layouts to speed boardroom decisions and refocus content, ad, and distribution priorities.

Customers Bargaining Power

Advertisers and agencies

Large brands and holding companies secure volume discounts and performance guarantees with publishers, and can reallocate budgets quickly across platforms—US digital ad spend reached about 262.5 billion USD in 2024, amplifying their leverage. Standardized metrics (viewability, iAB benchmarks) heighten comparability and price pressure, while deep agency relationships and BuzzFeed's proprietary formats can blunt demands.

Programmatic buyers

Open-exchange programmatic buyers benchmark CPMs across thousands of sites, driving downward pressure; programmatic made up roughly 86% of US display ad spend in 2024, increasing buyers’ leverage. Header bidding intensifies price competition by surfacing bids across SSPs. Brand-safety filters reduce demand for sensitive content, while private marketplaces and contextual deals boost yield and CPMs for vetted inventory.

Audience multi-homing

Consumers freely switch among countless content sources as 5.34 billion people used the internet in 2024, making multi-homing the norm; low switching costs erode loyalty to any single publisher. Engagement must be re-earned each session, driving higher paid and creative acquisition spend. Strong franchises and communities measurably boost retention and lifetime value.

Performance accountability

Buyers in 2024 pressed BuzzFeed for clear ROI, viewability, and incremental lift, cutting underperforming placements quickly and shortening cycles to weeks, which raises revenue volatility; creative studios and commerce tie-ins allowed BuzzFeed to command premiums on higher-performing packages.

- ROI-driven buying

- Rapid cutoffs

- Short cycles = volatility

- Studios/commerce = premium

Privacy and compliance demands

Buyers demand consented data and compliant targeting, and 2024 surveys show 58% of marketers report reduced addressability after signal loss, pressuring CPMs and bidding transparency. Clean room and first‑party solutions raise cost to serve, increasing integration and measurement spend. Clear, auditable reporting—attribution and viewability—helps preserve advertiser spend despite targeting constraints.

- consented data required

- 58% report lower addressability (2024)

- clean rooms raise cost to serve

- transparent reporting preserves spend

Buyers leverage: US digital ad spend 262.5B, programmatic ~86%

Buyers hold strong leverage: US digital ad spend hit 262.5B in 2024 and programmatic was ~86%, enabling price benchmarking and rapid reallocations. Low switching costs (5.34B internet users) and ROI demands (58% report lower addressability) force short cycles and volatility, though studios/commerce and first‑party solutions can secure premiums.

| Metric | 2024 Value |

|---|---|

| US digital ad spend | 262.5B USD |

| Programmatic share | ~86% |

| Global internet users | 5.34B |

| Marketers reporting lower addressability | 58% |

What You See Is What You Get

BuzzFeed Porter's Five Forces Analysis

This preview shows the exact BuzzFeed Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. It presents competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications in a ready-to-use format. After purchase you get this fully formatted file instantly.